MCG - Membership Collective Group: A Pricey Community

Summary

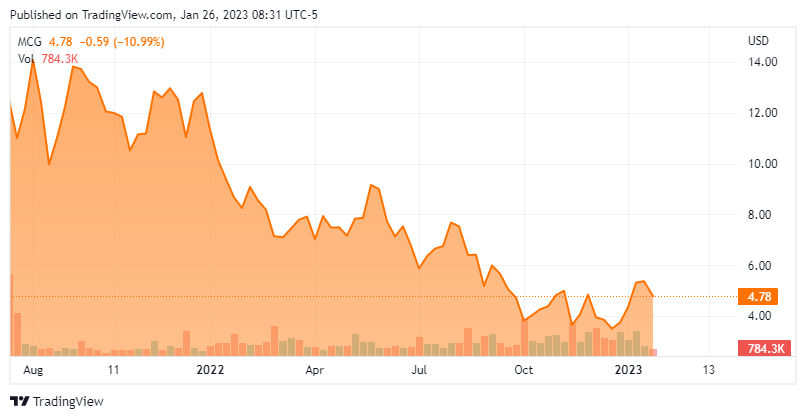

- Shares of Soho House operator Membership Collective Group Inc. are down some 60% since its July 2021 IPO, as higher labor costs and forex translations from a weak Europe hurt.

- The company is slowing down the pace of Soho House openings from eight to ten annually in an effort to maintain quality and slow its burn rate.

- The recent share repurchase program and insider buying merited a deeper dive, as did the Membership Collective Group Inc. stock's recent rebound.

- An investment analysis follows in the paragraphs below.

One can acquire everything in solitude except character ."? Stendhal.

Today, we are going to take our first look at a services firm that provides a unique membership club. The stock is deeply in Busted IPO territory after coming public in the second half of 2021. The decline has brought in some recent insider buying and the company is also repurchasing shares. The shares have been in rally mode over the past month. A dead cat bounce or start of a larger up move in the stock? An analysis follows below.

{kind=link}

Company Overview:

Membership Collective Group Inc. ( MCG ) is a UK-headquartered exclusive membership platform that functions as a social club and (in many instances) a lodging facility in 15 countries around the world. Its portfolio includes 38 Soho House properties (24 with lodging) that have attracted a worldwide membership totaling 211,400 (and a wait list of ~85,000) as of October 2, 2022. The company was founded in 1995 with the opening of its first Soho House - a three-story house-cum-members club in the Soho section of London - and went public in July 2021, raising net proceeds of $388 million at $14 per share. Its stock trades around $4.75 a share, equating to an approximate market cap of $950 million.

Membership Collective Group Inc. is capitalized by two classes of stock. The 56.1 million shares of publicly traded Class A stock bestow economic interest and one vote per share. The 141.5 million shares of privately held Class B stock confer economic interest, ten votes per share, and are convertible into Class A shares. Hospitality investor Ron Burkle and his Yucaipa Companies owns 56% of the B shares, with Founder Nick Jones and current CEO Andrew Carnie owning the majority of the balance.

The company operates on a fiscal year ending the Sunday closest to December 31st.

Membership

The cornerstone of MCG memberships are access to the well-appointed and very upscale "Houses" across North America, Europe, and Asia. They appeal to the media, fashion, restaurant, and art industries with 21 properties providing screening rooms that (along with other on-site event spaces) host hundreds of events annually - many of which are streamed digitally on the company's app. Soho House memberships in the U.S. typically range anywhere from ~$2,500 (single property) to ~$4,500 (all properties) annually. There are ~152,000 Soho House members, who pay for food and beverage, accommodation, and spa products and treatment - somewhat similar to belonging to a country club without the monthly minimum (just the annual or monthly fee).

That said, new members are required to purchase House Introduction Credits that function as cash at the Houses and expire three months after issuance. To keep it trendy, members under 27 are given a 50% membership discount. There are other memberships, such as Cities Without Houses, that permit club access when individuals who don't reside near a Soho House location are travelling to a location with one. A Soho Friends membership ($130 annually) allows access to lodging and other amenities but does not provide full access to the Houses.

November Company Presentation

Model

After functioning as either an owner-operator or leasing with a material investment to makeover its rental properties for two decades, MCG switched to an asset-light model that leverages its reputation as an excellent tenant. Any new property is leased with the landlord funding a substantial portion of the buildout in exchange for higher rent. This approach has lowered its upfront investment in full-sized Houses (i.e., those with lodging) from ~$10 million to ~$5 million. And with a significant wait list, MCG has essentially zero customer acquisition costs. Owing to the high-net worth of its membership and the social aspect of said membership, retention is very sticky (~95%), with that rate relatively unaffected by the pandemic.

Portfolio

In addition to the 38 Soho Houses, MCG's portfolio includes ten Soho Works offices for an additional fee, 11 Soho Studios, The Ned member's club and hotels in New York, Doha, and London, The LINE and Saguaro hotels in North America, and Scorpios Beach Club in Mykonos. It also has an interior and lifestyle retail brand dubbed Soho Home with five locations globally.

Revenue Disaggregation

MCG disaggregates its revenue by geography (North America, UK, Europe/RoW, and All Other) and by type: Membership, In-House, and Other.

The North America segment generated revenue of $279.4 million in first 39 weeks of 2022 ending October 2nd (YTD22), up 87% versus a similar period in FY21 and 40% of MCG's total; UK accounted for YTD22 revenue of $212.7 million, a 101% improvement over YTD21 and 30% of total; Europe/RoW was responsible for YTD22 revenue of $106.1 million, up 108% over YTD21 and 15% of total; and All Other, which consists of retail, Soho Works, Cities Without Houses, and restaurants, generated YTD22 revenue of $103.7 million, representing a 60% increase over the prior year period and 15% of total.

Membership accounted for YTD22 revenue of $195.7 million, up 43% from YTD21. In-House, which includes food and beverage, accommodation, and spa products and treatments, contributed YTD22 revenue of $305.9 million for a 137% improvement over the prior year period. That jump was partly a function of the lifting of pandemic-related social distancing mandates at its Houses. Other, which includes all revenues realized outside of MCG's Houses (Scorpios, Soho Works, standalone restaurants, Soho Home inter alia), accounted for YTD22 revenue of $200.2 million, up 81% from YTD21.

Operational and Share Price Performance

As can be gleaned by the gaudy growth rates, MCG has been aggressively expanding, opening six Soho Houses in FY21, with five launched in the YTD22 and another four originally scheduled to open before YE22. This growth has occurred at the expense of profitability, an approach shunned by the market over the past year. Add in the fact that the strong dollar (due to a weak European economy) is impacting its top line with ~60% of its revenues generated overseas, and it is easy to see why shares of MCG have not traded at their IPO price since November 2021 and are now down 75% from its public debut.

November Company Presentation

The company's 3Q22 financial report of November 16, 2022 highlighted these issues. MCG reported a loss of $0.46 a share ((GAAP)) and Adj. EBITDA of $20.3 million on revenue of $266.0 million versus a loss of $0.72 a share ((GAAP)) and Adj. EBITDA of $8.8 million on revenue of $179.6 million in 3Q21, representing top-line growth of 48%. Year-over-year currency translations impacted the top line by $53.9 million and the bottom line by $0.27 a share. Assuming no Street analyst factored currency into their models - very unlikely - earnings were still $0.07 a share shy of expectations. Revenue was more or less in line with expectations.

On the plus side, In-House revenue grew 62% year-over-year (90% on a constant currency basis) as food and beverage demand surged and the company realized an 18% increase in like-for-like revenue per available room versus 3Q21 and 23% higher than 3Q19.

As a result of higher labor costs and forex translations due to a weak macro backdrop in Europe, management was compelled to lower its FY22 Adj. EBITDA forecast from $75 million to $57.5 million (based on a range midpoint), meaning 4Q22 Adj. EBITDA of ~$20 million. Admitting "pressure on the business," MCG returned to its original target of five to seven new Soho Houses per annum, down from a previous objective of eight to ten. As part of its depressurizing, MCG is delaying the openings of Soho Houses in Mexico City and Bangkok to 2023, bringing the total number of openings in FY22 to seven.

November Company Presentation

The company also announced that Founder and CEO Nick Jones was transitioning to strictly the former role after winning a battle with prostate cancer. President Andrew Carnie is ascending to the top executive position. Given the CFO's departure in June 2022, the recent moves in the c-suite have also contributed to the stock's decline.

Balance Sheet & Analyst Commentary:

Another reason for pumping the brakes on the company's expansion are interest rates. MCG assumed an additional $100 million of debt in the prior twelve months to primarily finance its growth, and with the market for unprofitable growth concerns requiring a much higher financing rate, tabling an uber aggressive buildout for a mildly aggressive one makes sense. Case in point: in YTD22, operating cash flow of $38.1 million could not keep pace with property capex of $63.0 million. As of October 2, 2022, it held unrestricted cash of $227.9 million and debt of $697.7 million for a concerning net leverage of 11.5 (or 8.0 using management's FY22 Adj. EBITDA guidance). It has access to an additional ~$79 million on a revolving line of credit.

November Company Presentation

Curiously, against this negative free cash flow backdrop, the board approved a $50 million stock repurchase program in March 2022, on which the company has bought back 4.9 million shares during YTD22 at an average cost slightly above $7 per.

The Street leans decidedly negative on MCG's prospects, featuring only one buy rating against three holds, one underperform, one buy and one sell. Their median twelve-month price target is $7. On average, they expect the company to lose $1.30 per share ((GAAP)) on revenue of $951 million in FY22, followed by a loss of $0.41 a share ((GAAP)) on revenue of $1.2 billion.

It should be noted that Roth Capital initiated the shares as a new Buy with $7 price target citing " member pricing increases, in-house margin opportunities, and the potential rationalization of MCG's smaller businesses ." for their newfound enthusiasm.

Board member Mark Ein is diametrically opposed to the Street's bearish consensus sentiment, having purchased 456,936 shares of MCG at an average price of $3.91 on December 8th-9th. Another insider purchased just over $1.1 million in aggregate just two weeks later at slightly lower average prices.

Verdict:

With significant exposure to a weak European macro backdrop, the perceptions that club usage may drop precipitously in FY23 is likely unfounded, as experiences in past economic downturns suggest otherwise. The real issue is that with the dislocations created by the pandemic, labor costs have skyrocketed. However, with Soho Houses it is not simply a case of cutting back on staff. The clubs' service is a huge draw and expectation for its membership. Assuming MCG hits its Adj. EBITDA projection for FY22, its stock is trading at an EV/FY22E Adj. EBITDA of over 25, suggesting the stock appears fully valued after its recent rally.

On the 3Q22 conference call , management spoke of better realignment of work schedules with customer behavior (i.e., when they arrive and depart the clubs) on a club-by-club basis as a remedy. This approach is unlikely to make a significant impact on its profitability. Unless it passes along its higher cost structure onto its membership in the form of meaningful membership fee increases (which stick), Membership Collective Group Inc. is unlikely to reach profitability in the near future. As such, the investment recommendation is to stay on the sidelines.

That which is not good for the swarm, neither is it good for the bee ." ? Marcus Aurelius

For further details see:

Membership Collective Group: A Pricey Community