LRCX - Memory And Logic: Two Different Chips Two Different Trajectories In 2023

Summary

- Micron Technology, Inc. and other memory companies have substantial inventories to work through, as revenues plummet.

- The logic/foundry IC sector will not exhibit the revenue plunge in 2023 as will the memory IC sector.

- Applied Materials and Lam Research have the greatest exposure to revenues from memory IC production among top equipment companies.

- ASML Holding will benefit from the migration to small technology nodes and from a large backlog of DUV and EUV lithography equipment.

There are countless ways to segment the integrated circuit market. In this article I divide the IC market into two main segments - Memory and Logic/Foundry.

Memory chips are further segmented as DRAM and NAND. In the Logic/Foundry segment, it's a bit more complicated. A clear definition is given by Intel Corporation (INTC) CEO Pat Gelsinger, who commented :

"Intel is the sole American company both designing and manufacturing logic semiconductors at the leading edge of technology. When we launched Intel Foundry Services earlier this year, we were excited to have the opportunity to make our capabilities available to a wider range of partners."

Thus, it can be inferred that logic chips are made by companies like Intel that have their own fabs, whereas if these logic chips are designed by a fabless company like Advanced Micro Devices ( AMD ) or NVIDIA ( NVDA ) in a foundry like Taiwan Semiconductor Manufacturing Company Limited ( TSM ), they can be called Foundry chips.

The reason I say this is that equipment companies that sell their products uses these segments as part of their financial metrics. DRAM and NAND are generally segmented, but logic and foundry are sometimes separated, sometimes combined.

Memory Segment

The memory segment has fared badly in 2H 2022. In a December 15, 2022 Seeking Alpha article entitled “Micron: Excessive Capex Spend Responsible For Plummeting Memory Market,” I presented an analysis detailing the plunging sales of memory (DRAM and NAND) ICs during 2022, capex and WFE (wafer front end) semiconductor equipment cuts, and the reason behind the malaise with memory.

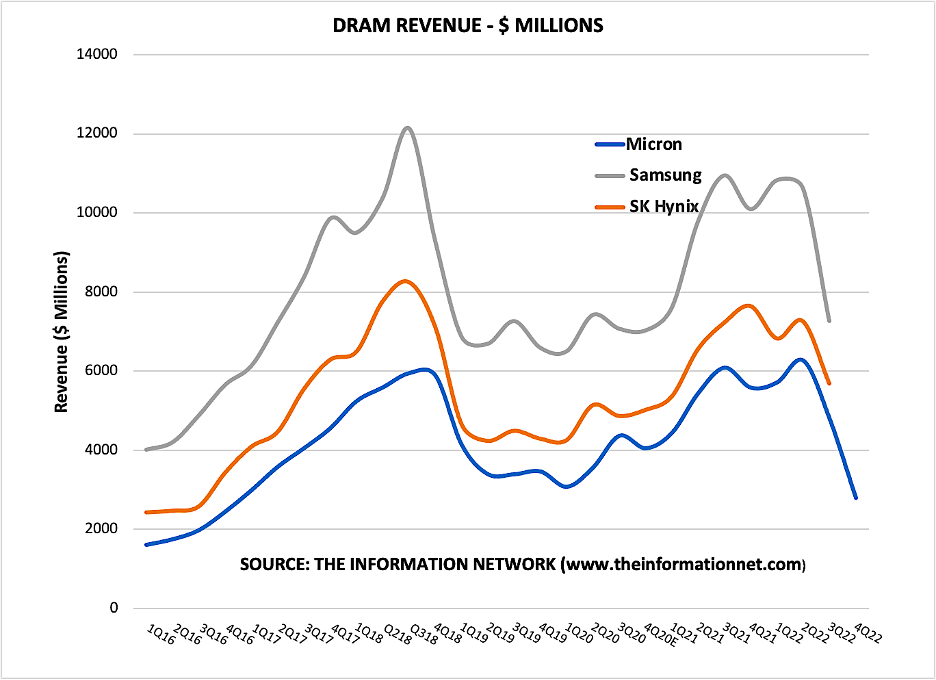

To better understand the memory IC industry, Chart 1 shows DRAM revenue between Q1 2016 and F1Q 2023 (ending November 2023). It shows a peak in revenue in 2H 2018 and another following covid lockdowns. In both cycles, revenue plummeted following the peak. The peaks occurred in Q3 2018 and Q4 2021.

Chart 1

{kind=link}

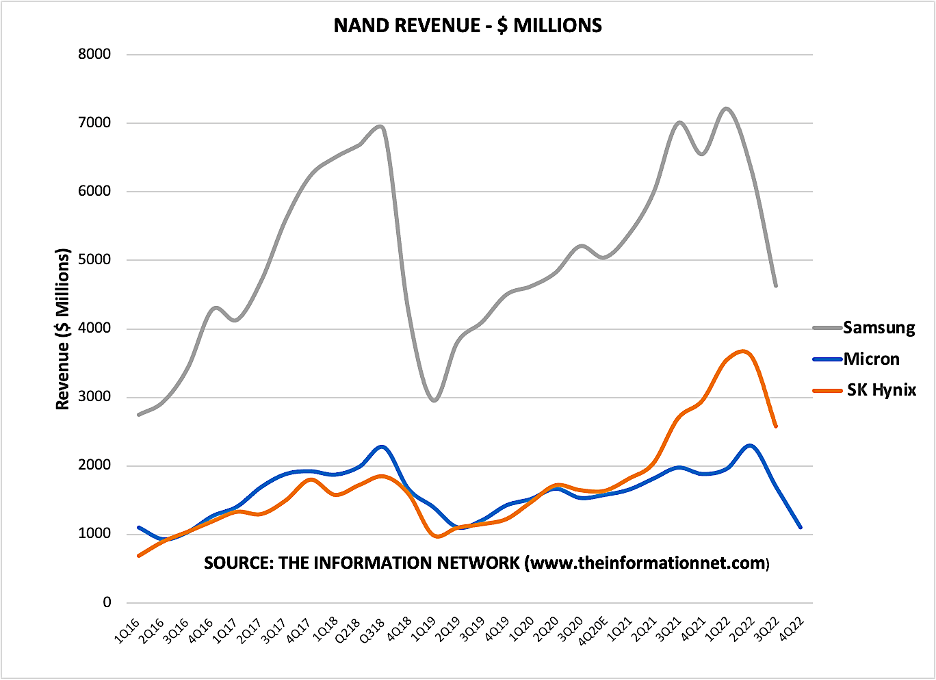

Chart 2 shows a similar peak for NAND revenue. The peaks occurred in Q3 2018 and Q2 2022. As with DRAM, the peaks occurred nearly simultaneously among the three memory companies Micron ( MU ), Samsung Electronics ( OTCPK:SSNLF ), and SK hynix.

Chart 2

{kind=link}

WFE Equipment Revenues

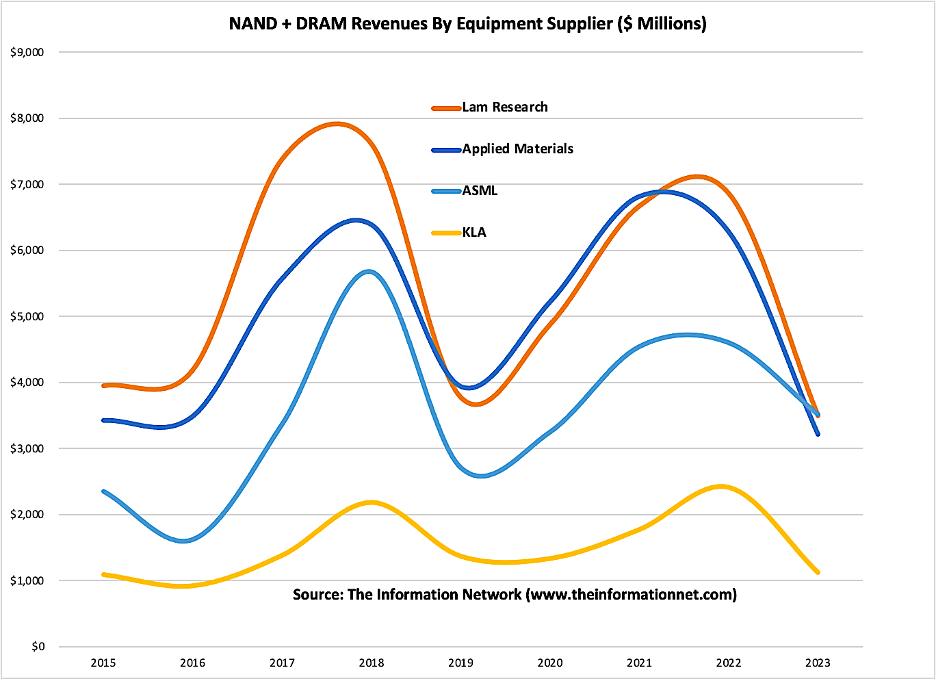

In Chart 2, I show WFE equipment revenues paid by the memory companies for equipment purchases. Also, data are on a yearly basis. DRAM and NAND are combined as some equipment companies don’t separate the two. There are two important takeaways:

Cycle Peaks

There are two peaks in WFE, as with DRAM and NAND revenues. The peaks occur in 2018 and 2021 for Applied Materials ( AMAT ) and 2022 estimated for Lam Research ( LRCX ), ASML ( ASML ), and KLA Corporation ( KLAC ). Final results will be known in each company’s earnings call in January, 2023.

Note the DRAM cycle (Chart 1) lasted three years and the NAND cycle lasted four years (Chart 2). Thus, the three and four-year cycle for WFE equipment in Chart 3 is consistent with peaks in memory IC revenues.

The correlation in peaks in memory revenues and equipment is not coincidental, but typical of a cycle. Companies buy equipment to increase chip capacity (capacity purchases) or to move to a smaller node (technology purchases).

For capacity purchases, chip output increases to a point where supply outpaces demand, and prices and revenue drop. Companies attempt to judiciously monitor WFE expenditures but when they make more chips than then need. Once demand catches up with supply, a new cycle begins.

Chart 3

{kind=link}

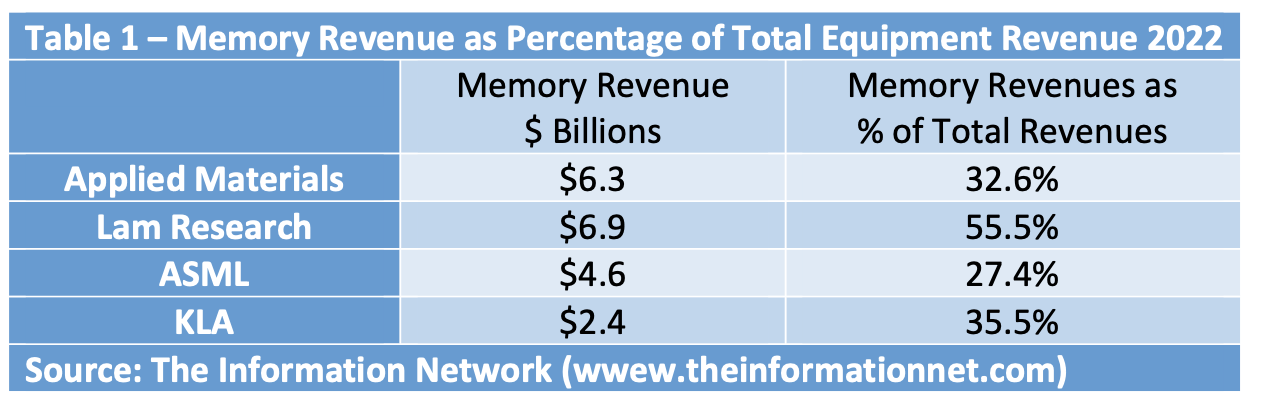

In 2022, both AMAT and LRCX will have generated the largest revenues from memory, as shown in Table 1. Applied’s revenues from memory companies should reach $6.3 billion, slightly less than Lam’s $6.9 billion but well ahead of ASML’s $4.6 billion and KLA’s $2.4 billion.

Table 1

{kind=link}

Importantly, AMAT and LRCX will be the most impacted equipment companies on the basis of revenue.

Even more important is the percentage of memory revenue to total revenues. Here we see that Lam’s exposure to memory represented 55% of total revenues, significantly greater than peers, which were generally similar to each other.

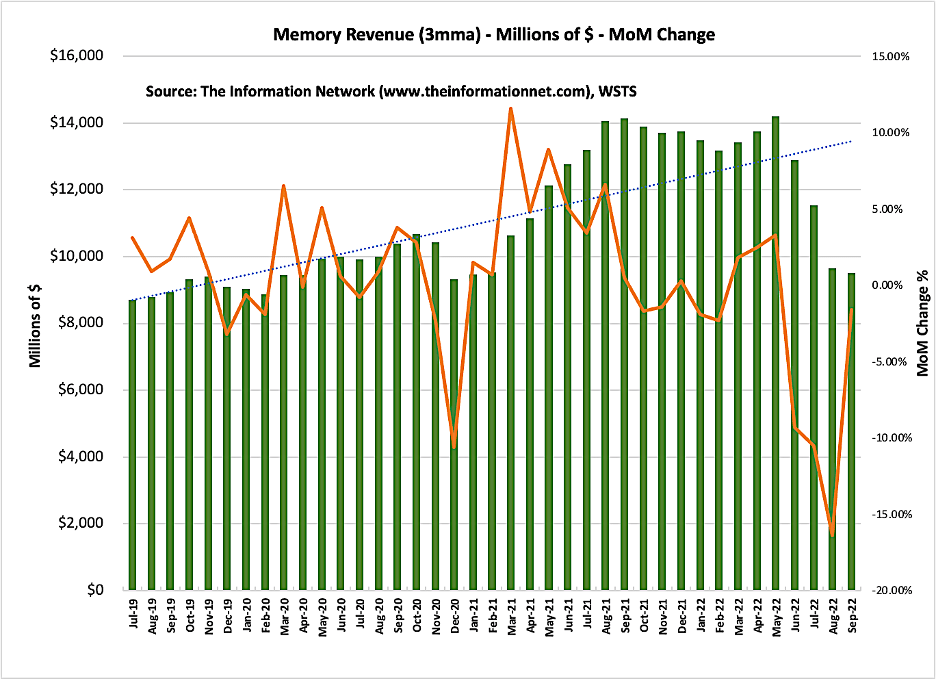

Memory IC Revenues

Chart 4 shows Memory (NAND and DRAM) revenues between July 2019 and September 2022. Memory revenues also began decreasing in June 2022. Revenues decreased 34.7% between the peak in May 2022 and October 2022. YTD memory revenues decreased 7.7%.

Chart 4

{kind=link}

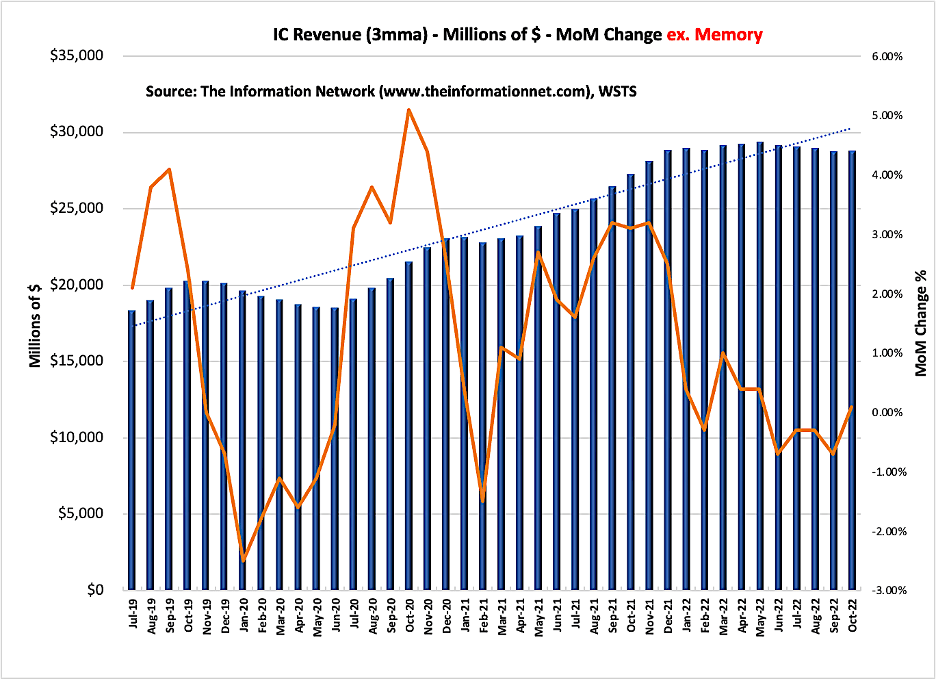

IC Revenue Excluding Memory

Chart 5 shows IC revenues between for the same period, and excludes memory. The drop off from the peak in May 2022 until October 2022 was 2.0%. YTD, ICs excluding memory increased 15.8%. This compares to memory in Chart 4 above where Revenues decreased 34.7% between the peak in May 2022 and October 2022. YTD memory revenues decreased 7.7%.

Chart 5

{kind=link}

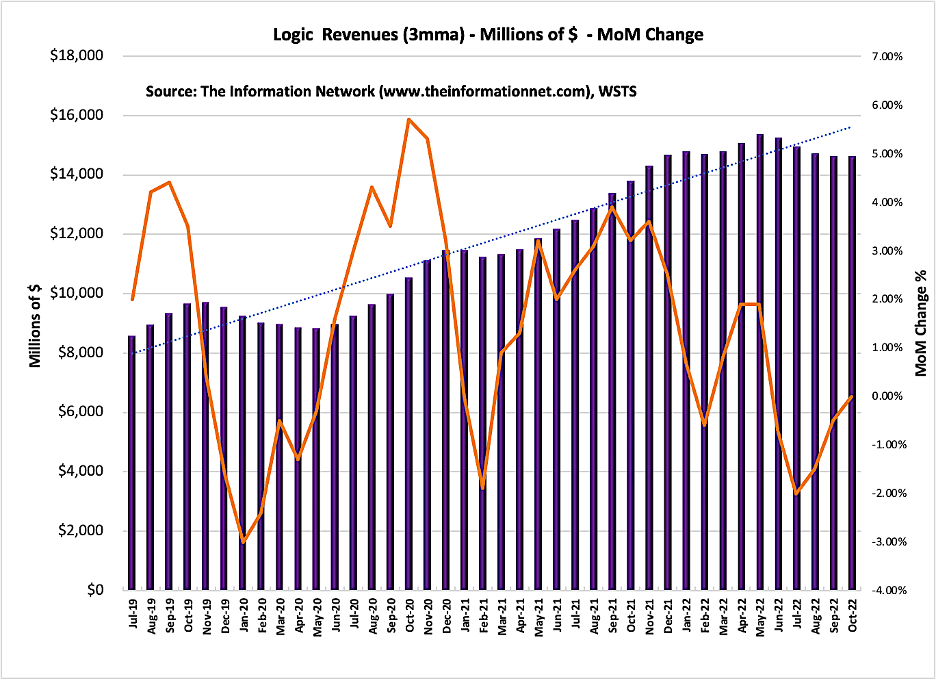

Logic IC Revenues

Logic revenues are shown in Chart 6. The drop off from the peak in May 2022 until October 2022 was 4.7%. YTD, Logic increased 18.9%.

Chart 6

{kind=link}

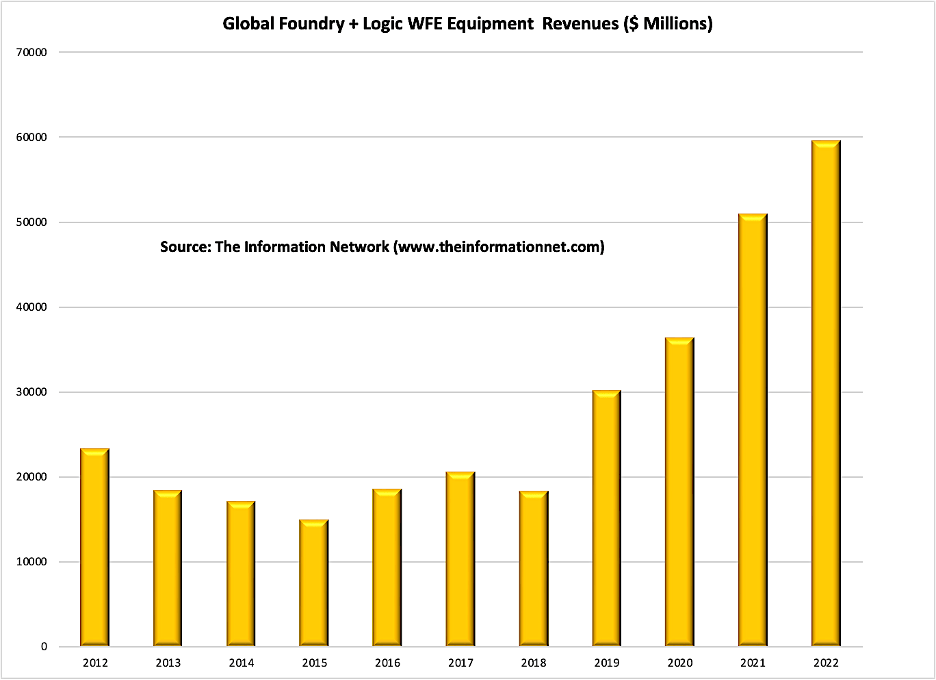

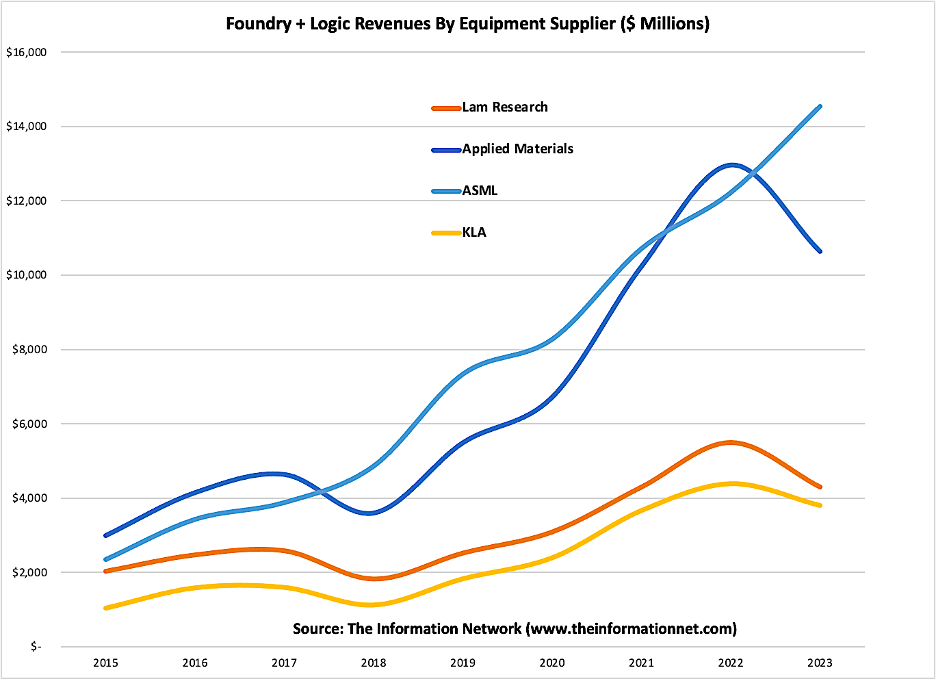

Logic/Foundry Equipment Revenue Growth

WFE revenues generated by semiconductor equipment companies for shipments to logic/foundry customers is shown in Chart 7 on a Yearly basis between 2012 and 2022. Revenues increased 17.8% YoY in 2020, 42.2% in 2021, and 17.0% in 2022.

Chart 7

{kind=link}

In 2021 WFE equipment revenues for Logic/Foundry increased 42.2%. Chart 8 shows Logic/Foundry revenues by company. According to The Information Network’s report entitled “ Metrology, Inspection, and Process Control in VLSI Manufacturing. AMAT exhibited strong growth in 2022, particularly in F4Q 2022, when it pulled-in revenues of $1.7 billion coming from TSMC, up from $1.3 the prior quarter.

Chart 8

{kind=link}

While it may appear that Applied Materials with its deposition and etch equipment, outperformed KLA with its metrology/inspection business, that is not the case. Table 2 shows that KLAC outperformed AMAT in two of the three years, and is expected to do so in 2023 even though both will exhibit negative growth.

Table 2

{kind=link}

In Chart 8, I forecast that ASML, which has been stymied by supply chain problems in 2021 and 2022, will exhibit positive growth in 2023 because of production limitations, ASML has a backlog of 100 EUV systems with an ASP of $200 million. Unlike memory IC companies, logic/foundry semiconductor companies are not likely to cancel orders despite the downturn and oversupply of chips in 2023 as leading foundry companies migrate to smaller technology nodes.

Nevertheless, as shown above in Chart 8, the other WFE equipment companies will not be as fortunate as ASML, dropping low double digit percentages in 2023.

I estimate Memory 2023 revenues for AMAT, LRCX, and KLAC will drop close to 50% YoY over 2022. KLAC is showing strong revenue growth in 2022 on continued penetration of EUV into memory, which demands metrology/inspection equipment for smaller nodes.

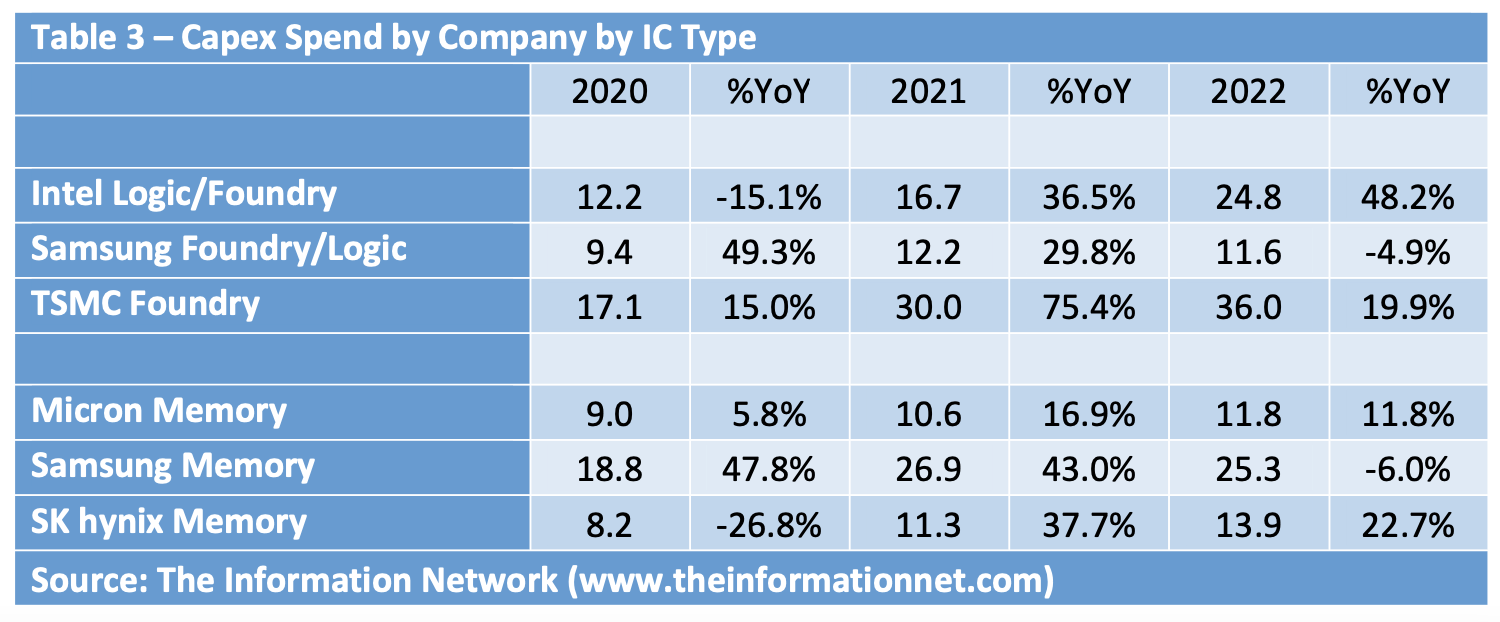

Capex

Memory

In my December 15, 2022 Seeking Alpha article about Micron, I presented an analysis detailing the plunging sales of memory (DRAM and NAND) ICs during 2022, capex and WFE (wafer front end) semiconductor equipment cuts, and the reason behind the malaise with memory.

Table 3 shows Memory capex spend as a percentage of revenues for the three companies for 2020-2022. Micron cut capex in 2021 only to increase it in 2022. Samsung’s increase in 2021-2022 was because the EUV tech migration increased the ratio of capex to revenue to 44.8%.

Table 3

{kind=link}

- Micron indicated it would reduce 2023 capex by 30%, which includes 50% equipment and 50% building, which would imply a 15% cut in equipment. But MU is actually cutting back WFE equipment purchases by 50% in fiscal 2023, a significant impact on equipment suppliers to the company.

- SK hynix announced in late October it plans to reduce its investment next year by more than 50 percent due to poor demand in memory chip business. The move comes after the company’s third quarter operating profit fell to 1.7 trillion won ($1.2 billion), missing analysts’ estimates of 1.87 trillion won. Revenue fell 7 percent to 11 trillion won.

- Samsung electronics has no plan to cut dram output artificially or adjusting capex. Samsung plans a semiconductor capex spend of 54 trillion won, of which 47.7 trillion won ($38.5 billion) of which 33 trillion won (29.1 trillion won for semiconductors) has been spent so far in 2022.

Logic/Foundry

Also shown in Table 3 are capex spend plans for TSMC, Intel, and Samsung between 2020 and 2023. Samsung's capex is for foundry only and does not include DRAM or NAND capex.

In 2021, TSMC was the biggest spender, with capex at $17.1 billion, an increase of 75.4% from 2020, growing 19.9% in 2022. Samsung capex increased 49.3% in 2020 to $9.4 billion. In 2022, Intel is forecast to increase capex 48.2%.

Nevertheless, between 2020 and 2023, TSMC's capex spend is higher each year than competitors Intel and Samsung. This increased spend will result in increased fab capacity and increased chip output.

Investor Takeaway

The Chips Act will have limited near term benefits. The $53 billion in the Chips Act, intended to increase semiconductor production in the U.S., is forecast to increase semiconductor capacity just 1% between 2021 and 2025. This is detailed in my October 31, 2022 Seeking Alpha article entitled “$53 Billion Of Handouts For Chips Act And U.S. Forecast To Gain Just 1% Share By 2025!”

These are logic/foundry fabs, and based on my thesis from mid-2021 that the excessive WFE spend in 2021 and 2022 will result in an oversupply of chips in 2023 and a drop in WFE spend. It can be read in my article entitled "Applied Materials: Tracking A Likely Semiconductor Equipment Meltdown In 2023."

Semiconductor companies may build the fab shell, reaping handouts, but will closely monitor the supply/demand dynamics before installing equipment and moving into production at an inopportune time.

Financial Metrics

Chart 9 shows share price for the past 1-year period. While all stocks are down, KLAC dropped 12%, beating out peers. ASML has dropped 27%, as the company continues to have supply chain problems. The worst performance is from AMAT and LRCX with nearly identical results.

Chart 9

YCharts

AMAT and LRCX will be the most impacted equipment companies on the basis of Memory revenue. Lam's high exposure of 55% of revenues makes the company the most susceptible to plummeting demand for memory ICs.

The logic/foundry IC sector through 2022 has not been impacted by capex and WFE overspend as has the memory sector. Nevertheless, the overspend in equipment purchases in 2020 and 2021 will result in negative growth for AMAT, LRCX, and KLAC.

ASML will benefit in 2023 from the continued tech migration to smaller nodes, as its DUV and EUV lithography equipment are required for sub 7nm nodes. It’s DUV immersion lithography equipment has only one competitor, Japan’s Nikon ( OTCPK:NINOY ), and its EUV systems have no competitors. The huge backlog of equipment will mitigate any revenue loss that will impact its competitors analyzed in this article.

Another strong company is KLAC. While the company will be impacted in 2023 with a pause in WFE equipment demand by semiconductor companies, the company has demonstrated its superiority among peers in stock performance.

For further details see:

Memory And Logic: Two Different Chips, Two Different Trajectories In 2023