KAKZF - MercadoLibre: Wonderful Company Substantially Undervalued

2023-12-22 23:46:19 ET

Summary

- MercadoLibre is a highly profitable company with massive revenue growth momentum and strong long-term earnings estimates.

- The company operates the largest online commerce ecosystem in Latin America, with a focus on Brazil and Argentina.

- MercadoLibre's financial performance has been stellar, with a high free cash flow margin and impressive quarterly earnings.

- My valuation analysis suggests the stock is substantially undervalued.

Investment thesis

MercadoLibre ( MELI ) is an absolute sensation. The company demonstrates monster profitability and the current revenue growth momentum is massive. Long-term consensus earnings estimates are very optimistic and my analysis suggests that it is fair given strong secular tailwinds behind MELI's back. The company's business model is like a snowball where large scale provides it with the massive competitive edge. Furthermore, my valuation analysis suggests the stock is substantially undervalued. All in all, I assign MELI a "Strong Buy" rating.

Company information

According to the company's 10-K report , MercadoLibre is the largest online commerce ecosystem in Latin America based on unique visitors and orders processed. MELI's ecosystem is represented by six integrated e-commerce and digital financial services: the Mercado Libre Marketplace, the Mercado Pago Fintech platform, the Mercado Envios logistics service, the Mercado Ads solution, the Mercado Libre Classifieds service, and the Mercado Shops online storefronts solution.

The company's fiscal year ends on December 31. MercadoLibre generates more than half of its revenue in Brazil, and Argentina is accounting for about a quarter of the total.

{kind=link}

If we look at the company's revenues from the streams perspective, Commerce is the largest one, but Fintech is closing the gap at an impressive pace.

{kind=link}

Financials

The company's financial performance over the last decade has been nothing but stellar. Revenue compounded at a 41% CAGR, and cash flows were following the top line. MercadoLibre is an absolute free cash flow [FCF] champion with almost no stock-based compensation [SBC]. In FY 2022, the company delivered a staggering 23.7% FCF margin.

A wide FCF margin allows the company to successfully balance between investing heavily in growth and sustaining a healthy balance sheet. The company had almost $5.5 billion in cash as of the latest reporting date, which positions itself strategically to continue investing heavily in growth and marketing.

Seeking Alpha

The latest quarterly earnings were released on November 1, when MELI topped consensus estimates. Revenue grew by a staggering 40% YoY, and the adjusted EPS almost tripled. The delivered operating leverage was impressive as the EBIT margin expanded from 11% to 18% on a YoY basis. The stellar revenue growth momentum is expected to be sustained as consensus estimates forecast Q4 revenue at $4.1 billion, representing a 37% YoY growth. The adjusted EPS is expanded to more than double, from $3.25 to $7.66.

Seeking Alpha

If we speak about the company's long-term prospects, they look bright as well. According to Americas Market Intelligence , Latin America's e-commerce market is expected to compound by 22% yearly up to FY 2026. Being the number one player in this field with vast resources and expertise compared to potential new entrants, MELI will highly likely sustain its stellar revenue growth rate over multiple years. Such an optimistic outlook for Latin America's e-commerce industry looks fair, given the overall global secular shift to purchasing items online multiplied by the big economic potential of the region.

MELI has the largest country exposure to Brazil, which is a promising economy due to numerous factors. Brazil is an oil-rich country that is among the world's largest crude oil exporters. The current favorable situation in energy commodity markets with a positive outlook is a solid tailwind for the Brazilian economy. It is also important to understand that Brazil is also rich in metals, and its favorable climate and geographical location also make it a very strong global agricultural player. That said, it is unsurprising that the Brazilian economy is expected to demonstrate decent growth in the next five years .

{kind=link}

Now, let me underline the company's offerings and why I believe they stand out. Unfortunately, I did not have experience using MercadoLibre's ecosystem. However, based on what I have read about the company's integrated set of services, it looks very much like the Kaspi.kz ( OTC:KAKZF ) "super app", which is widely used in my home country, Kazakhstan. Kaspi started building its super app relatively recently, and now it has become everyone's must-have in our country, like electricity or the internet. It became so because it saves people lots of hours to complete simple everyday tasks like shopping and banking with literally just a couple of taps on their smartphones. The business model of Kaspi and MELI is literally a snowball: more users attract more merchants, and vice-versa. That said, the business scale is very important and creates a wide moat in this business. Why would people need another MELI/Kaspi if they already have a super app where they can find everything they need to accelerate their pace of life? That said, the fact that MELI is the largest commerce and fintech ecosystem in its region of operations means the company has a massive competitive edge.

Valuation

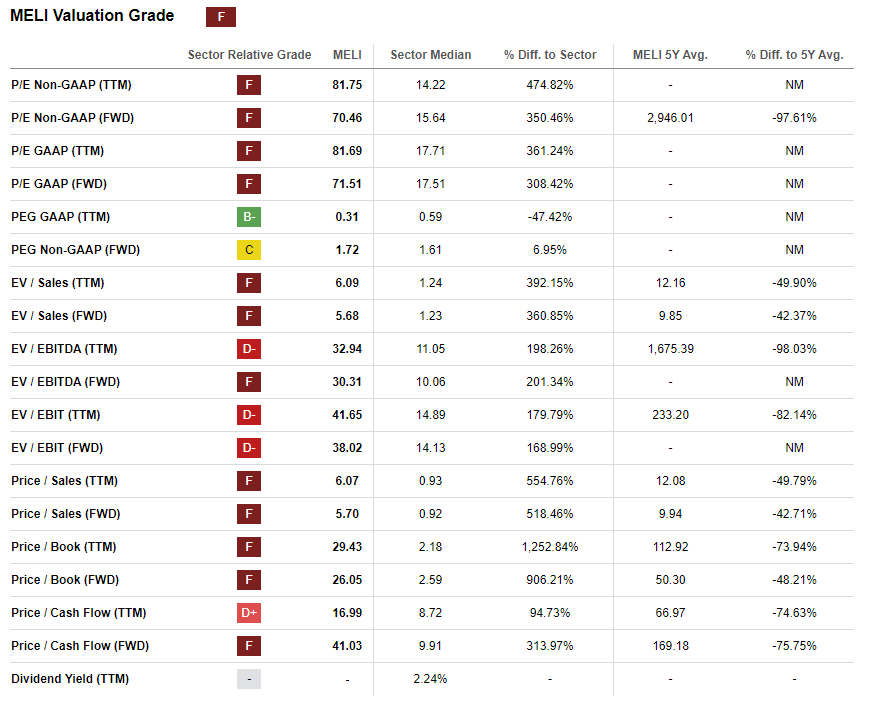

MELI rallied by a massive 93% year-to-date, far outperforming the broader U.S. stock market. Valuation ratios look very hot compared to the sector median. However, it is crucial to acknowledge that MELI's growth profile and profitability are best-in-class, and the company deserves a premium compared to its peers. The current valuation ratios are also substantially lower than MELI's historical averages, which indicates valuation attractiveness.

{kind=link}

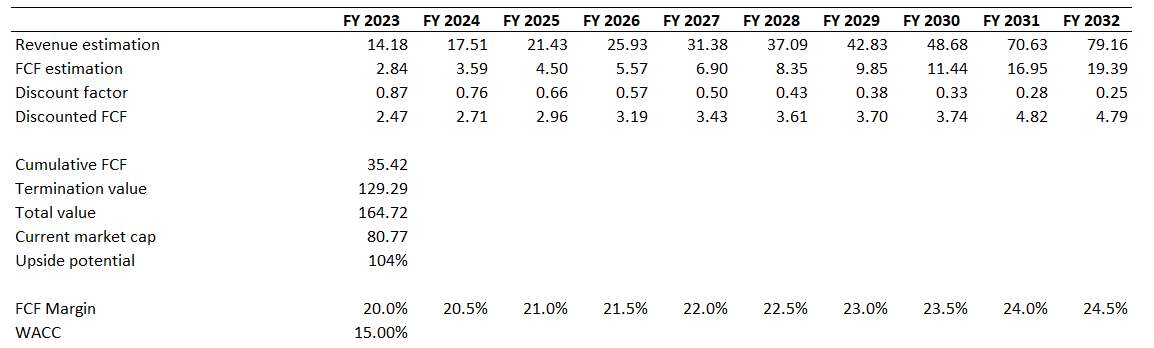

For an aggressive growth company like MELI, the best option to proceed with is to simulate the discounted cash flow [DCF] model. Gurufocus suggests that MELI's WACC is around 13%, but I prefer to be super conservative when we speak about companies outside the U.S. and around the discount rate of up to 15%. Revenue consensus estimates project a 21% CAGR for the next decade, which looks fair given the current strong momentum and bright prospects I have described in the previous section of my article. I use a conservative 20% FCF margin for my base year with a 50 basis points yearly expansion.

{kind=link}

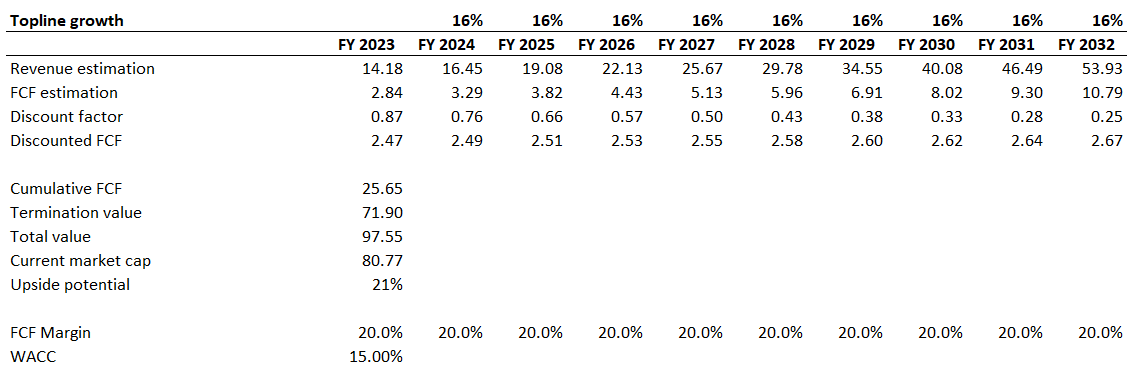

My DCF simulation shows the business's fair value is $164 billion. This is two times higher than the current market cap, indicating a massive upside potential. MELI bears might argue that the 21% CAGR will be quite challenging over the next decade. Therefore, I want to simulate a more pessimistic scenario with a five percentage points lower revenue CAGR for the next decade and no FCF expansion.

{kind=link}

As we can see, even under much more conservative assumptions, the business's fair value is close to $100 billion. This indicates a 21% upside potential from the current stock price levels. I prefer to be more conservative and set a target price of 21% above the current level, which will be around $1940 per share.

Risks to consider

The company's valuation significantly depends on MELI's ability to sustain its stellar revenue growth and profitability expansion. As we have seen in "Valuation", the fiver percentage point change in revenue growth projections leads the business's fair value to almost half, which indicates massive sensitivity. That said, indications that the company's revenue growth is decelerating faster than expected will highly likely lead to a substantial stock sell-off due to investors' disappointment. That said, potential investors should be ready to tolerate high volatility.

Investing in companies from emerging markets is inherently risky because these markets often demonstrate greater unpredictability compared to more established economies. Political risks are higher in the developing world due to potential sudden changes in government policies, corruption, and civil unrest, which can significantly adversely affect the business environment. Currency risks are also much higher in emerging markets.

Bottom line

To conclude, MELI is a "Strong Buy". The company demonstrates staggering revenue growth and profitability expansion and is well-positioned to sustain this impressive dynamic for longer. Moreover, my valuation analysis suggests the stock is very attractively valued. That makes MELI a compelling investment opportunity.

For further details see:

MercadoLibre: Wonderful Company Substantially Undervalued