MERC - Mercer International: Current Pessimism Represents A Good Long-Term Opportunity

2023-04-04 19:00:41 ET

Summary

- The company's revenues are slowing down as a result of weakening markets and high leverage.

- High cash and equivalents and inventories provide a safety cushion amidst current headwinds and a potential recession.

- This represents a good opportunity for long-term investors seeking a good dividend entry point.

- In the short to medium term, there is a risk of a dividend cut or even its cancellation as a consequence of the current headwinds.

Investment thesis

Mercer International ( MERC ) is a company with a large presence in the pulp and wood markets that is currently experiencing a nearly 50% drop in its share price as a result of recent headwinds related to supply chain constraints and a weakening of the markets in which it operates, which is getting worse as a result of the current energy crisis in Europe.

The company has grown significantly in the past few years thanks to a high pace of acquisitions, but these acquisitions have pushed debt levels to relatively dangerous levels at a time when the ability to generate cash from operations is suffering. Still, high cash and equivalents and inventories provide a safety net that, in my opinion, will allow the company to navigate current headwinds and even a potential recession. Therefore, I consider that the pessimism that currently reigns among shareholders represents a good entry point. But for dividend investors, it is very important to note that there is a significant risk of a dividend cut or cancellation as a result of the current headwinds that I will explain throughout the article.

A brief overview of the company

Mercer International is a global forest products company. The company was founded in 1968 and its market cap currently stands at ~$640 million, employing over 3,000 workers worldwide. Despite its market cap, insiders own 8.91% of the total shares outstanding, which means that the management is likely a direct beneficiary of the price of the company's shares.

Mercer International logo (Mercerint.com)

{kind=link}

The company operates under two main segments: Pulp and Solid Wood. Under the Pulp segment, which provided around 80% of the company's total revenues in 2022, the company manufactures, sells, and distributes pulp, green electricity, and chemicals to Europe, Asia, and North America from its four pulp mills located in Eastern Germany and Western Canada. And under the Solid Wood segment, which provided around 20% of the company's total revenues in 2022, the company manufactures, sells, and distributes lumber, manufactured products (including cross-laminated timber and finger joint lumber), wood pallets, electricity, biofuels, and wood residuals from its sawmills and other facilities located in Germany and the United States.

Currently, shares are trading at $9.69, which represents a 48.76% decline from the peak of $18.91 during the past decade, reached in 2019 and close to being surpassed in 2021. This is certainly a fairly significant drop accompanied by increased risks as revenues are expected to slow down while margins are suffering as a result of weakening markets and economic conditions, especially in Europe.

What is important to note here is that Mercer International is a highly cyclical company, so there are, in my opinion, two acceptable ways to invest in it. The first is to take advantage of the times in which pessimism seizes investors to find a good entry point and thus enjoy a higher dividend yield on cost in the long run, and the second is to close the position at times of greater optimism to obtain profits in the form of capital gains. It is up to the investor to decide what to do based on their investment style, but in the case of dividend investors, it is important to bear in mind that there is a short-to-medium-term risk of a dividend cut or even halt, so it may be eventually necessary to wait for an improving macroeconomic outlook to exit the position with capital gains.

But first, I'd like to start with recent acquisitions as, despite the fact that the company has a high cyclical component, it has grown significantly in recent years boosted by acquisitions.

Recent acquisitions

The company entered into the solid wood segment in 2017 with the acquisition of the Friesau Facility, a German sawmill and bio-mass power plant near Friesau, Germany, for $62 million. Later, in October 2018, the company acquired Santanol, which owns and leases existing Indian sandalwood plantations and a processing extraction plant in Australia, for ~$36 million.

In December 2018, the company acquired Daishowa-Marubeni International, the owner of a bleached kraft pulp mill in Peace River, Alberta, and also the owner of a 50% interest in the Cariboo Pulp & Paper Company, a joint venture which operates a bleached kraft pulp mill in Quesnel, British Columbia, for ~$345 million. The acquired company generated revenues of $351.6 million, net income of $8.2 million, and an EBITDA of $55.3 million in fiscal 2017. And later, in October 2019, the company acquired a log harvesting, road building, and trucking services business for $6.94 million, and named it Mercer Forestry Services Ltd .

As of recent times, in August 2021, the company acquired a cross-laminated timber facility in Spokane, Washington, for $51 million, and named it Mercer Mass Timber LLC . And in September 2022, the company completed the acquisition of Holzindustrie Torgau, the owner and operator of an integrated timber processing facility that produces wood pallets, lumber, biofuel, and energy, for €270.0 million, in order to expand the company's solid wood operations in Germany. The acquired company generated net revenues of €227 million, net income of €31 million, and Adjusted EBITDA of €68 million in 2021, and made Mercer International the largest German pallet producer.

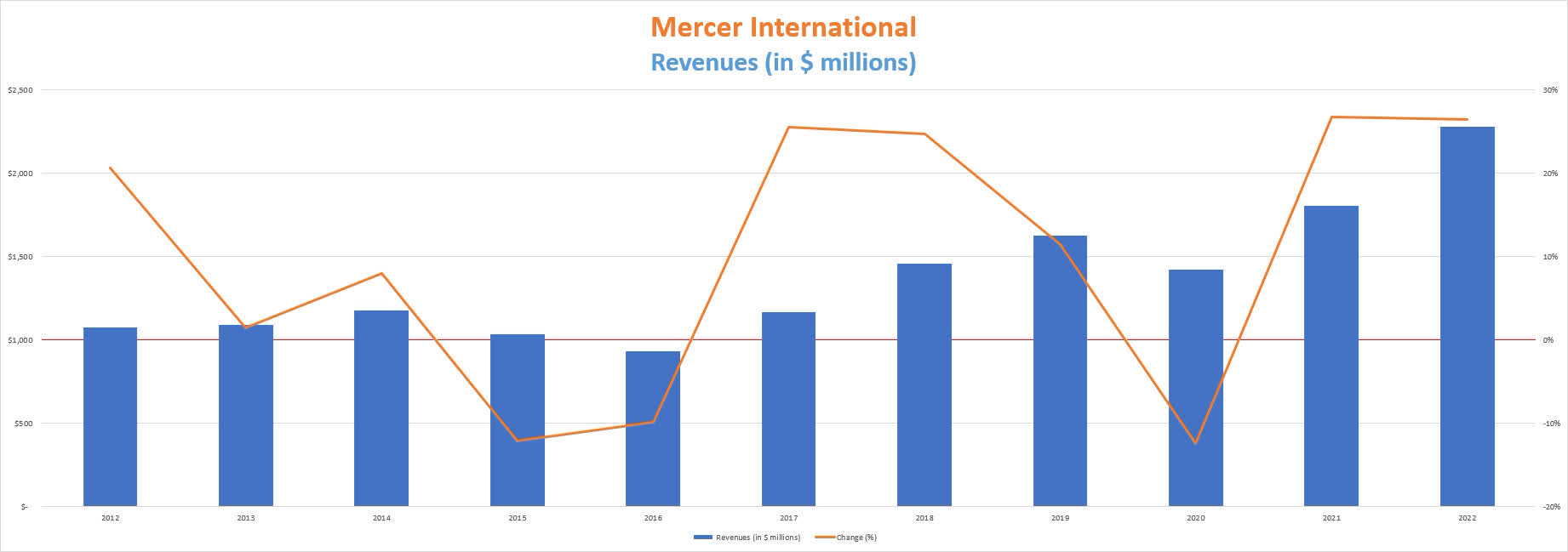

Revenues are stabilizing after a significant boost in 2022

The company has more than doubled its revenues in the last 10 years thanks to these acquisitions, and although revenues decreased by 12.39% during the coronavirus pandemic in 2020, they recovered in 2021 with a rise of 26.71% and continued to grow in 2022 by another 26.49%. Using 2022 as a reference, 18% of the company's revenues are generated within the United States, whereas 31% is generated in Germany, 22% in China, and 29% in the rest of the world.

Mercer International revenues (10-K filings)

{kind=link}

During the past quarter, revenues of $583.1 million represented a 12.35% increase year over year, and a 9.44% increase quarter over quarter as volumes increased in all the company's products compared to the third quarter. This increase was also boosted by the acquisition of the Torgau mill. But despite recent growth rates, revenues are expected to decline by 4.8% to $2.2 billion in 2023 and increase by only 1.38% in 2024. This is due to, firstly, the weakening of the markets in which the company operates, and secondly, because the company has a debt load that makes the growth rates experienced up to now unsustainable since deleveraging the balance sheet is increasingly essential to allow the sustainability of the company's operations in the long term.

The recent increase in revenues, along with the current share price decline, has produced a significant drop in the PS ratio to 0.283, which means the company currently generates $3.53 for each dollar held in shares by investors, annually.

This ratio is 50% lower than the average of 0.566 during the past decade, and 69.5% lower than the peak of 0.929 reached during the second half of 2017. This reflects the current pessimism among investors as a consequence not only of the expectations of a slowdown in revenues but also of a deterioration in profit margins at a time when long-term debt is at record highs.

Margins are being impacted by current headwinds

The company achieved a record EBITDA of $537 million in 2022 as it increased pulp volumes while increasing the price of its products. But despite this, the trailing twelve months' profit margins are beginning to be impacted by the current macroeconomic context in which pulp and lumber markets are weakening, especially (but not only) in Europe as a result of weakness in economic conditions due to the energy crisis that is currently taking place.

In this regard, the company reported a gross profit margin of 14.51% during the past quarter, and an EBITDA margin of 16.51%, both significantly lower than the trailing twelve months' margins. For this reason, during the fourth quarter of 2022, it reported an EBITDA of $96 million compared to an EBITDA of $141 million during the third quarter as Europe recently implemented energy price caps and pulp fiber and chemical costs were considerably higher, as stated by CFO David Ure during the past quarter earnings call. Also, shipping palette and heating pellet prices decreased significantly, as well as global pulp prices. And finally, fiber supply constraints in western Canada are forcing the company to halt production at the Cariboo joint venture for two months.

These headwinds are coming at a delicate time for the company due to the high indebtedness it is currently exposed to as a result of recent efforts to expand via acquisitions through the use of debt, but the management achieved $6 million in synergies from the Torgau sawmill and expects a potential of $60 million in annual cost savings in the long term.

Long-term debt is at record highs due to recent acquisitions

As a consequence of the latest acquisitions, the long-term debt has increased in recent years to $1.30 billion. This suggests that the company will not be able to keep on with the recent pace of acquisitions indefinitely. Still, cash and equivalents have also improved fairly steadily to $354 million.

This brings the net debt to just under $1 billion. But it is also important to note that inventories have more than doubled since 2018 to $450.47 million, which significantly reduces debt risk since the company can convert said inventories into cash.

The real problem is in the total interest expense, which reached $18.77 million during the fourth quarter of 2022, and what this means for shareholders. During the same quarter, dividends paid were $9.9 million, which means, firstly, that the company must generate enough positive cash from operations to cover both interest expenses and the dividend in order to not rely on cash and equivalents and inventories to do so and, secondly, that dividend growth is currently limited by interest expenses and will continue to be as long as the long-term debt does not decrease.

The dividend is not as safe as it used to be

The company began paying dividends in October 2015 when the management set a quarterly dividend of $0.12 per share, and raised it twice before the coronavirus pandemic crisis. The latest raise took place in the second quarter of 2019 as the quarterly dividend reached $0.1375 per share, but the dividend was cut by 53% to $0.065 during the first quarter of 2020 due to the coronavirus pandemic outbreak. Nevertheless, the dividend was raised by 15% to $0.075 in the first quarter of 2022.

At the current share price, the dividend yield is ~3.1%, which is more than acceptable due to its enormous potential in the long term since interest expenses are almost twice as high as dividends paid. This means that the management will be able to raise the dividend once the long-term debt is reduced. Once interest expenses are reduced, the cash payout ratio will be, in my opinion, low enough to enable further dividend raises. To calculate the cash payout ratio, I have calculated the percentage of cash from operations that has been used each year to pay the dividend and, later, I will explain its current status.

| Year |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $159.22 |

| $140.78 |

| $141.93 |

| $236.67 |

| $244.28 |

| $41.57 |

| $182.21 |

| $360.66 |

| Dividends paid (in millions) |

| $7.42 |

| $29.73 |

| $29.87 |

| $40.72 |

| $35.28 |

| $21.89 |

| $17.17 |

| $19.85 |

| Interest expenses (in millions) |

| $53.89 |

| $51.58 |

| $54.80 |

| $51.46 |

| $75.75 |

| $80.75 |

| $70.05 |

| $71.50 |

| Cash payout ratio |

| 38.51% |

| 57.75% |

| 59.65% |

| 38.95% |

| 45.45% |

| 246.93% |

| 47.86% |

| 25.31% |

As we can see in the table above, the cash payout ratio has been quite conservative in recent years, except in 2020 as a result of the coronavirus pandemic. In 2022, the cash payout ratio was as low as 25.3% despite interest expenses of $71.5 million, but during the past quarter, cash from operations was $50.6, which was enough to cover interest expenses of $18.7 million and $9.9 million of dividends paid. Furthermore, inventories increased by $64.5 million quarter over quarter while accounts payable increased by only $5.7 million accounts receivable declined by only $28.1 million, which suggests that the company can continue to cover the dividend and interest expenses in current market conditions.

Risks worth mentioning

The current macroeconomic context and the particular situation of the company make it important to assess the various risks that the company is currently facing. Especially, I would like to highlight the following risks:

- The pulp and timber markets could continue to weaken if the energy crisis continues to hit the European economy and if the world's economy weakens in 2023 and beyond. Furthermore, a potential recession as a result of recent interest rate hikes to alleviate high inflation rates could further impact demand, which could have a significant impact on the company's operations, especially volumes and profit margins.

- The company's long-term debt is at a high level as a result of the acquisitions carried out in recent years. This not only carries a significant risk of revenue stagnation as a consequence of the need of deleveraging the balance sheet but also a risk of interest expenses eating up a large part (or even more) of the cash from operations if market conditions keep weakening.

- Despite the recent 15% dividend raise, the management could decide to cut the dividend again, or even cancel it, as a result of the recent weakening of profit margins, which would have devastating consequences for dividend investors. In this regard, the balance sheet is, in my opinion, strong enough to withstand current headwinds and even a potential recession, but the management could decide to cut (or cancel) the dividend in order to preserve cash until the macroeconomic landscape is more favorable.

Conclusion

Mercer International's outlook is currently delicate, and proof of this is the almost 50% decline in the share price from its decade-highs. Revenues are slowing after two very positive years following the lifting of coronavirus restrictions and significant efforts to expand operations through acquisitions. Now, the company finds itself with a high level of debt and margins are suffering due to the weakening of both pulp and lumber markets, especially in Europe as a result of the current energy crisis. In addition, there is the risk of a recession in the medium term due to recent interest rate hikes, which could weaken the markets even further.

Despite this, the company is currently able to cover both the dividend and interest expenses with cash from operations, in addition to having high cash and equivalents of $354 million and inventories of $450 million that will serve as a safety net in case operations continue to weaken in the coming quarters, which makes me think that this represents a good opportunity for investors with enough patience to wait for an improved macroeconomic landscape that encourages more optimism for the company's prospects.

For further details see:

Mercer International: Current Pessimism Represents A Good Long-Term Opportunity