MERC - Mercer International: Might Just Be Enough For A Dividend Investment

2023-06-30 00:41:44 ET

Summary

- Mercer International is expected to yield around 4% annually and has the potential for growth and compounding returns in the long run, despite the volatility of these industries.

- The company has maintained a stable business environment despite fluctuating prices of wood pulp and paper and has seen a post-pandemic surge in demand due to increased construction in its dominant markets.

- Despite risks such as a high debt load and industry volatility, MERC is believed to be in a healthy financial position.

- I'm optimistic about the company's potential to sustain and possibly increase its dividend payout, and I plan to add shares of the company to my investment portfolio.

Mercer International ( MERC ) operates a diversified set of businesses in the pulp, paper and timber industries, as well as offering logistics and transport solutions in those industries. Although these industries can be volatile at times, demand has remained relatively steady and the company's sales have been on a steady upwards trajectory.

What's got my attention is the company's yield and its potential to grow and compound returns in the long run. It currently yields around 4% annually, as of their latest payment of $0.075 per share in the most recent quarter, yet their payout remains relatively low at around 10% of earnings.

There are 2 factors in my optimism surrounding shareholder value. The first is that the company has had a payout ratio of over 30% for 3 years back before the pandemic, so it's not a huge stretch to think that management can authorize a dividend hike to lure in investors. The second is that the stability of their current dividend payout even if they don't increase it allows for diversification within higher yielding companies.

Adding a 4% annual return to the projected growth rate of the various industries which Mercer International operates in brings a projected return to above the broader market, creating opportunity in a rather steady industry.

The Stable Business Environment

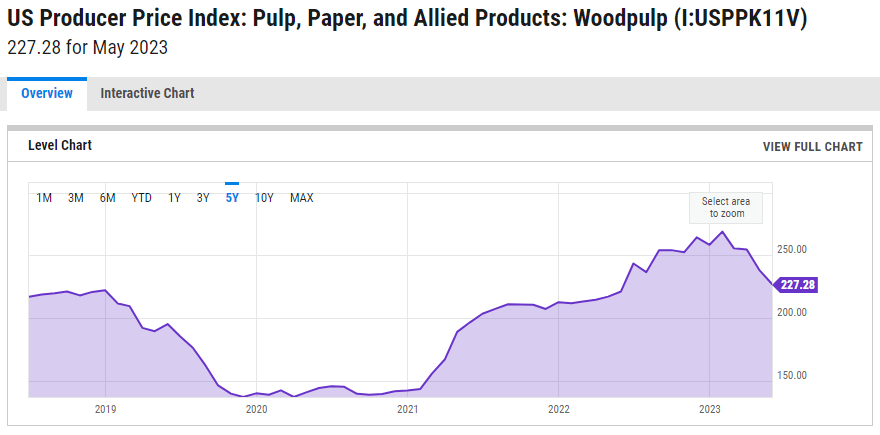

Mercer International's volatility comes from prices of wood pulp and various paper prices, which tend to fluctuate due to usual supply and demand issues. During and in the immediate aftermath of the COVID-19 pandemic, the company felt these headwinds as supply issues meant that getting raw material in and delivering any finished materials or products took a hit.

The company did, however, enjoyed a post-pandemic surge due to the pulp and paper pricing, as well as timber, through increased demand in construction in the company's dominant regional markets in China, Germany and US.

{kind=link}

The company was able to enjoy the boost in demand and sell a lot of product it had some trouble shipping through the pandemic, but it was able to increase pricing a bit to boost margins. In 2019, the company reported a slight gross margin expansion from 28% to 30% on behalf of these price increases and I'm optimistic that even as shipping and pulp pricing has stabilized that margins remain stable and the company isn't forced to lower prices with markets.

In more recent news is where we see the company's drop from drop off in pulp pricing in China in particular and globally in general. I believe these are temporary headwinds and I'll discuss it later on.

Industry & Company Growth

The company operates in a few different industries:

The pulp market is by far its largest and where it generates most of its revenues. While the pulp and paper markets are projected to report a CAGR (compound annual growth rate) of just 0.91% through 2028 globally, the China market is projected to grow at a faster clip of 6% through 2031 and the European Union region, with Germany at its center, is projected to grow at a 3.8% compound annual growth rate.

There are also other market where the company operates in which are going to enjoy a higher overall growth rate over the next few years and it's encouraging that the company is branching out more organically and through acquisitions. The timber logistics market is projected to grow at a 6.6% CAGR and the mass timber construction market is projected to grow at a similar clip of 6 % annually through 2031.

Taking a look at how these translate into growth to the company's top and bottom lines comes from current analyst projections , which expect the company to report a rather flat growth environment due to the drop this year and return to last year's levels in the next.

While having rather stagnant growth figures for the next 2 years is disappointing, it does provide me with clarity that the company will be fine with their shareholder value programs. Not only is their $300 million in cash enough to sustain a few years of dividend payments, I believe that these projections, done during a significant downturn in the pulp and paper market, represent as close to the bottom of the company's potential as you can get.

Shareholder Value

As I mentioned, the company has the potential to not only maintain their current shareholder value in their dividend payments but also increase it down the line.

Right now, they pay out around 10% of their earnings in cash dividends, which is easily manageable given that their income is not expected to dip in a significant way in the longer run (outside of the upcoming year). They pay less than $20 million annually in cash dividends while they generate anywhere from $125 to $250 million annually in income from continuing operations.

I do believe that the company has the potential to attract more investors by increasing their payouts. This isn't to say that they'll return to the high payout they had previously, but I do believe we could be them hike it consistently over the coming years.

This means that the company's yield will increase as time goes on for investors who get in at current prices, allowing for the investment to compound at a faster clip. 4% is already quite good and it will likely aid in the company outperforming the broader market in the long run. This isn't to say there aren't risks.

Risks Persist

The main risk which I believe can ultimately dissuade the company from increasing their quarterly dividend payout is their debt load. It's not only that they've been taking on more debt to finance operations and expansion, but in a rising rates environment it means they're paying a good chunk of change in interest expense.

In the last reporting year, the company paid over $70 million in interest expense on just over $1.3 billion in long term debt . The main issue I see here is the trend in which their long term debt load is headed. The company was paying down their debt throughout the years and reached roughly $600 million by 2017, but then began taking on some debt to finance acquisitions even though the company was making a decent amount of net income.

They since continued taking on long term debt to finance various acquisitions. Since 2017, the company added around $770 million in long term debt while they made cash acquisitions worth about $670 million over that time period. They've always had relatively healthy cashflows over the years but opted to take on more debt, with the most recent $266 million in long term debt this past year being the most puzzling in a rising rate environment.

In order to mitigate this risk, the company is going to have to show some willingness to pay down their debt and deal with lowering interest expense. With over $70 million in interest expense and about $375 million in operating income, paying this down will constitute one of the best uses of cash they can do to make sure that they remain in good financial health through years which may be more difficult.

The second risk is obviously the volatility which can come to the pulp, paper, timber and logistics markets, as we've seen in the past few years. The company had a few years where they faced a tough operating environment by seeing both declining revenues and lower margins on behalf of selling prices. Having a few years of this, while also having a higher interest expense environment than back then can lead to the company burning through cash and getting into trouble.

They try and mitigate this risk as best they can by hedging and diversifying their offerings, and I do believe this will be enough to weather some pretty bad storms, but it is something that investors need to keep in mind when investing in a company so closely tied to an industry with volatile seasons.

Investment Conclusion: Worth A Dabble

While risks due exist, and this coming year is showing that, the company is in a healthy financial position where they'll not only be able to sustain their dividend payout but as they emerge from these headwinds, as I believe they will, they may be able to offer a hike in payments to lure in shareholders.

With a good amount of cash, diverse industries with higher-than-average growth rates and the potential to boost net income by using some cash to pay down higher interest rate debt - I believe that the company would make a find addition to companies with relatively high yields.

This will help me diversify from REITs and other high-yield companies like Icahn Enterprises ( IEP ) which have some sentiment headwinds and offer exposure to a market that may be a little volatile but has steady demand in construction, manufacturing, paper and pulp supply and more.

I am bullish on the company's ability to beat the broader market over the next 3 to 5 years and I will be adding shares in the company to my investment portfolio.

For further details see:

Mercer International: Might Just Be Enough For A Dividend Investment