MBINP - Merchants Bank Undervalued Preferred Stocks

Summary

- Merchants Bank of Indiana is a small bank with excellent profitability and investment grade credit rating from Moody's.

- Merchants Bank currently has four preferred stock issues outstanding.

- Two of the preferred stock issues appear to be undervalued compared to larger bank preferred issues.

- The two fixed-to-floating rate issues appear to be good candidates for income-seeking investors.

Introduction

Bonds, preferred stocks, and other fixed income investments took a severe beating in 2022 as a result of the Federal Reserve's aggressive interest rate increases and quantitative tightening to combat inflation. The aggressive Fed monetary tightening has provided investors with an opportunity to secure solid returns with fixed income securities from investment grade companies. This is an opportunity we have not had for roughly the last decade.

The Fed has consistently stated that the Federal Funds rate will be higher for longer. I believe we will see at least one more 25 basis point increase and maybe two through March. As a consequence, bonds and other fixed income securities may see continued weakness through the first quarter of 2023. However, my crystal ball is not any more clear than anyone else's. I want to capitalize on this opportunity so I've started accumulating a portfolio of bonds, baby bonds, and preferred stocks. With the preferred stocks, I'm focusing on fixed-to-floating securities with near term (less than 2 years) conversion dates as these should provide the best total returns. I believe two of the preferred stocks issued by Merchants Bank of Indiana ( MBIN ) will provide solid returns with low risk.

Merchants Bank of Indiana

MBIN is a diversified bank holding company headquartered in Carmel, Indiana operating multiple lines of business, including Federal Housing Administration multi-family housing and healthcare facility financing and servicing; mortgage warehouse financing; retail and correspondent residential mortgage banking; agricultural lending; and traditional community banking. Merchants Bancorp, with $12 billion in assets and $10.3 billion in deposits as of September 30, 2022 is ranked as the 151st largest bank in the US.

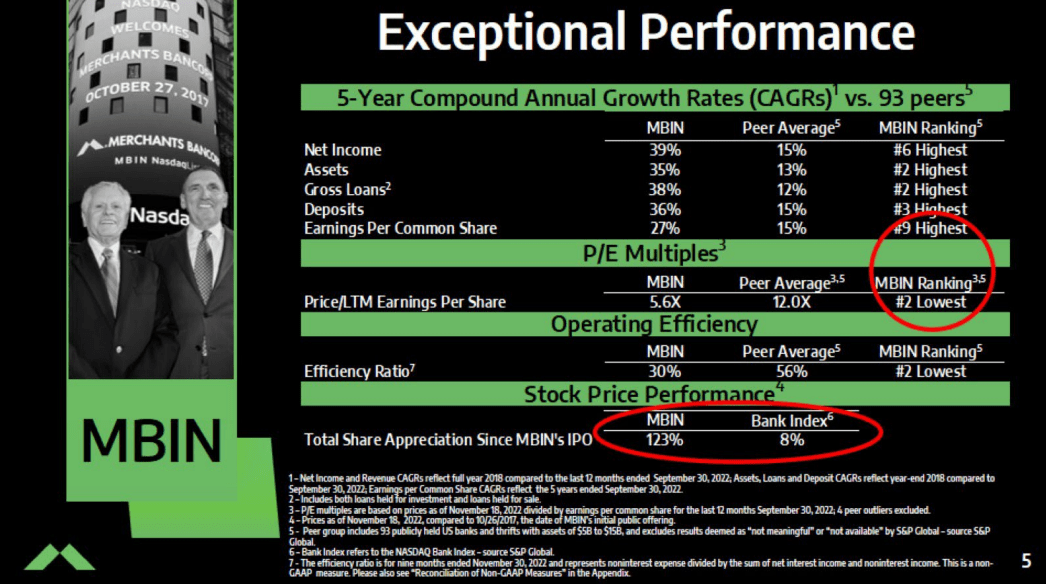

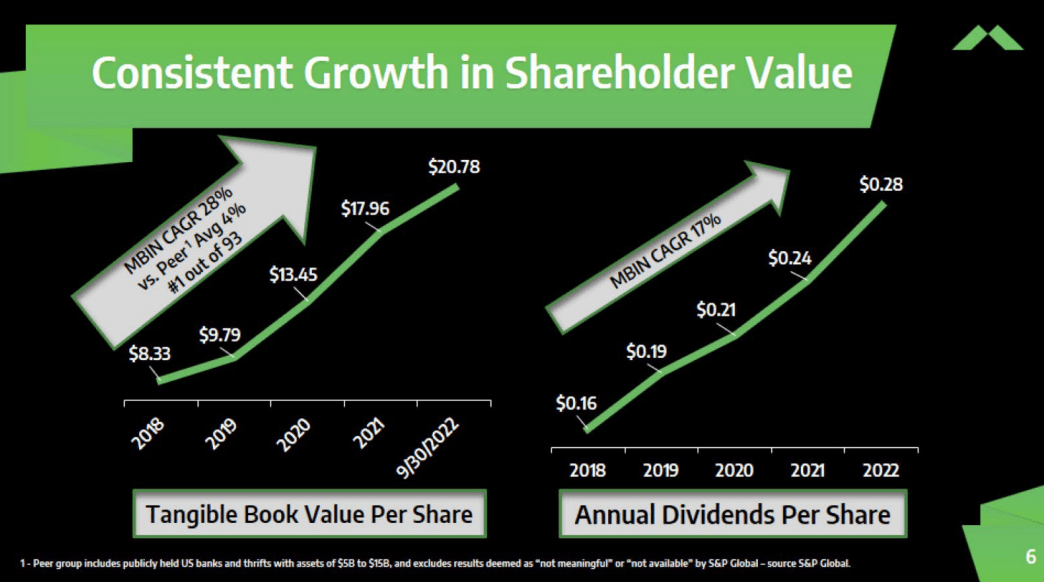

Since its 2017 IPO, MBIN's financial performance has been exceptional. Standard and Poor's Global Market Intelligence ranked MBIN as the best-performing U.S. public bank for the year 2021. MBIN's November 2022 Investor Presentation provides an excellent summary of the bank's financial performance over the last 5 years. Pages 5 and 6 of that presentation are provided below.

{kind=link}

{kind=link}

MBIN does pay a $0.28/yr dividend on shares of its common stock and, with a current EPS of $4.50, the payout ratio is a very conservative 6.2%. More important to those investing in the preferred shares, the net income for the 9 months ending September 30, 2022 was $163M and the dividend payments for 9 months would be $23M giving a coverage ratio of 7.1x against a net income that is growing at a CAGR of 39% for the last 5 years. The bottom line here is that the preferred stock dividends are very well covered and likely to be better covered in the future.

Merchants Bank Preferred Shares

MBIN has a total of four different preferred stock issues as shown in the table below along with two Wells Fargo ( WFC ) fixed-to-float preferred stock issues for comparison.

{kind=link}

A bit of explanation is probably in order so we are all on the same page with respect to the table headings.

- Credit ratings are all based on S&P or S&P equivalent ratings. Preferred shares are often rated by one or more of the big three credit rating agencies (Fitch, Moody's, and S&P). I convert the Fitch and Moody's ratings to S&P equivalent ratings for consistency in the table above.

- The Yield column reflects the current fixed payment divided by the current share price.

- The Reset Rate is based on an assumed 3 month LIBOR (or equivalent) rate of 4.8% and a 5 year Treasury rate of 4%. Numbers I've estimated based on the fixed-to-float or reset rate conversion dates.

- The Yield on Cost is based on the Reset Rate x ($25/Price). In other words, the yield on cost I would receive if I bought at the current price after conversion to the floating or reset rate.

MBINM carries a very high coupon rate but is selling significantly above its $25 par value lowering its yield from 8.25% to 7.45%. It might be interesting if the price falls below $25 but not at the current price. The risk is that MBINM is called in at $25 per share giving you a sub-par return of 5.6%. I'm carrying it on my watch list at this point.

MBINN is a traditional fixed rate issue currently priced at $19.22 giving a current yield of 7.8%. This is a very decent yield but at a coupon rate of 6%, it is unlikely to be called in unless and until short rates get back to near zero and the 10 year Treasury is below 2%. I don't see that happening anytime soon so the yield to call of 15.6% is probably not meaningful.

MBINP is a fixed-to-floating issue with a conversion date of 3/15/24 and a spread to the 3 month LIBOR rate of 4.6%. At the current $24.19 price, the current yield is 7.23%. With an estimated reset rate of 9.4% (new coupon rate), this issue is likely to be called in at or shortly after conversion to the floating rate. However, the yield to call is not stellar at 9.89%. I'd be a lot more interested in this issue at a lower price and so I'm carrying this on my watch list.

The most interesting issue of the four is MBINO with a fixed-to-floating conversion date of 10/1/24 and a spread to the 3 month LIBOR of 4.57%. Like MBINP, I believe MBINO is likely to be called in at or near the floating rate conversion date. Unlike MBINP, MBINO has a higher current yield of 7.38% and a much higher yield to call of 19.6% due to its current $20.33 price. If MBINO does not get called, I'll be happy collecting the 11.5% yield on cost as a consolation prize. Comparing current yields between the four MBIN preferred issues, you would come to the conclusion that they are fairly consistent yields and efficiently priced. If you make the comparison based on yield to call or yield on cost, you would come to the conclusion that MBINO is mispriced low.

I included in the table above WFC-Q and WFC-P as they are similar fixed-to-floating rate issues with roughly similar initial coupon rates. The WFC preferred issues carry a credit rating only one step higher than the MBIN preferred issues yet they carry a higher current price and significantly lower spread to 3 month LIBOR. Granted WFC is a much larger bank than MBIN but WFC also has "issues". WFC was recently fined again, I believe for the third time, for opening fake client accounts and assessing clients bogus costs and fees. It is not possible to weigh all of the WFC issues to come up with an apples to apples comparison of MBIN preferred issue pricing to WFC preferred issue pricing. However, in my estimation, it appears that MBIN preferred shares MBINN and MBINO are undervalued in comparison to WFC-PQ and WFC-PR.

Conclusion

We have a current opportunity to invest in fixed income securities with a legitimate expectation of solid returns going forward. This is something we have not had for roughly a decade. Fixed income returns for the next couple of years should be very satisfying.

MBINO, at its current valuation appears to be mispriced to the low side. If the issue is called at or near the floating rate conversion date, investors stand to receive a 19% annual yield. If MBINO is not called, investors stand to receive a safe double digit yield on their cost after MBINO converts to a floating rate.

Given the current financial health of MBIN, its financial performance since its 2017 IPO, the 7.1x preferred dividend coverage, and its current corporate credit rating of Baa3 from Moody's (BBB- S&P equivalent) with stable outlook, the risk of dividend suspension or non-payment is very low.

For further details see:

Merchants Bank Undervalued Preferred Stocks