MKKGY - Merck KGaA: Expect A 10% CAGR EBITDA Increase In 2024-2025

2023-08-13 11:40:00 ET

Summary

- Merck KGaA reported disappointing Q2 results with a decrease in gross profit and EBIT compared to the previous year.

- The company remains confident in its 2025 targets despite reducing its full-year guidance for 2023.

- Anticipated double-digit revenue growth in 2024 and 2025 makes Merck a potential investment opportunity.

Introduction

In April, I had another look at Merck KGaA ( OTCPK:MKGAF ) ( OTCPK:MKKGY ), the German life science and technology company (not to be confused with Merck ( MRK )), so whenever I discuss "Merck" in this article, I will be referring to the German company.

{kind=link}

The ticker symbol on the Deutsche Boerse exchange is MRK and the stock is trading with an average daily volume of just over 330,000 shares. As Merck trades in Euro and reports in Euro, I will use the EUR as base currency throughout the article. The current share count is approximately 434.8M shares as investors need to use the theoretical number of shares to correctly reflect the general partner's interest. The stock closed at 163.30 EUR in Germany last Friday, resulting in a market capitalization of approximately 71B EUR.

The H1 results are now in

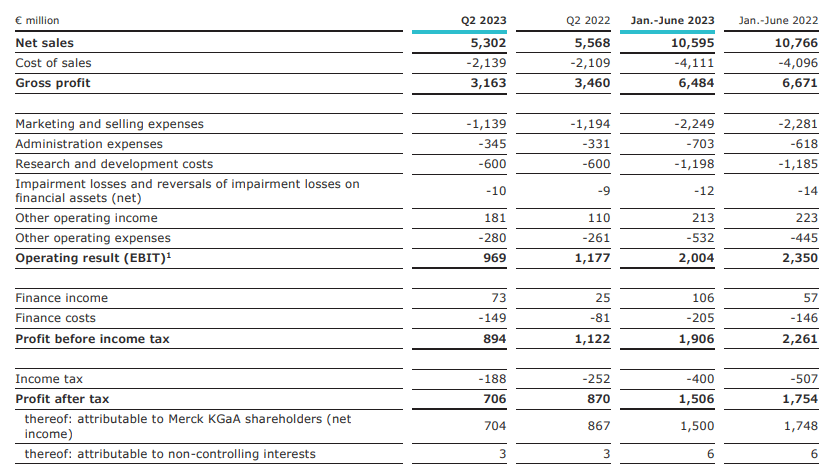

The second quarter was perhaps a little bit disappointing as the company reported an organic revenue decrease of 1.1% to 5.3B EUR while the EBITDA decreased by 7% to 1.6B EUR on a similar organic basis. As you can see below, the gross profit in the second quarter decreased by approximately 300M EUR while the EBIT came in at 969M EUR compared to almost 1.18B EUR in the second quarter of last year.

{kind=link}

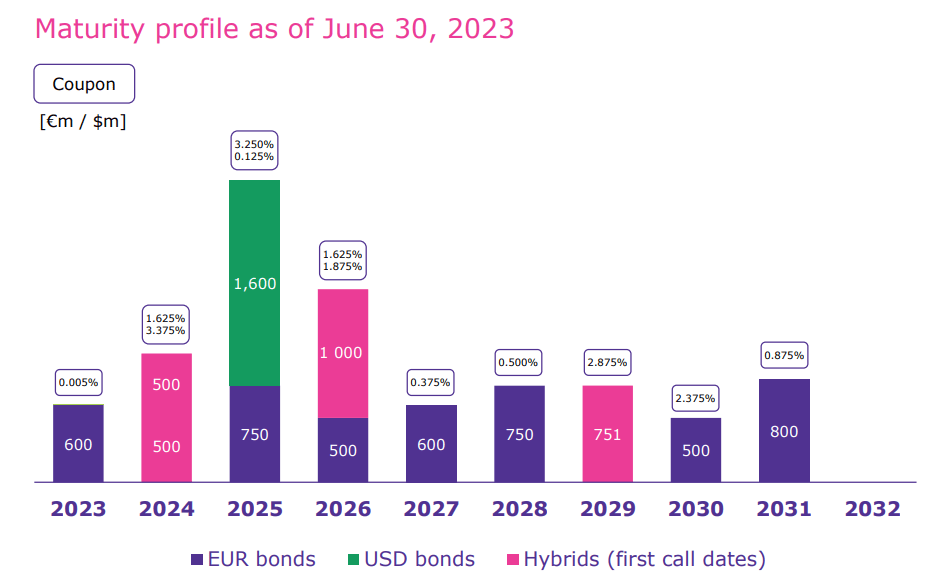

Needless to say the higher interest expenses and finance costs also are weighing on the result (the interest expenses will only gradually increase throughout the next decade as Merck’s debt maturity profile is well-staggered as you can see below). Whereas Merck reported a net finance cost of 56M EUR in Q2 2022, this already has increased to 76M EUR in the second quarter of this year. This ultimately resulted in net income of 706M EUR of which about 704M EUR was attributable to the shareholders of Merck. This represents an EPS of 1.62 EUR per share.

{kind=link}

That’s definitely a weaker result compared to the first quarter of the year, and the H1 EPS of 3.45 EUR per share is almost 15% lower than in the same period last year.

I originally liked Merck for its smart M&A approach. The balance sheet would temporarily expand due to the debt-funded acquisitions but Merck was always pretty good at focusing on generating free cash flow to reduce the debt again.

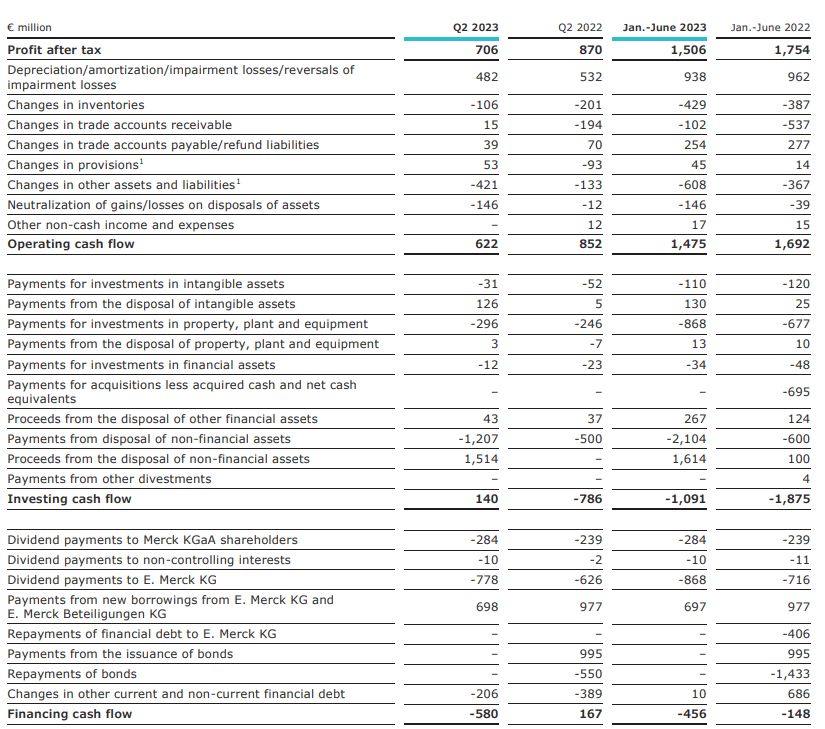

The cash flow statement for the first semester shows a total operating cash flow of 1.48B EUR including an 840M EUR investment in the working capital. There doesn't appear to be any noticeable lease liability payments (there are some lease liabilities though), and the adjusted operating cash flow after taking the 10M EUR dividend to non-controlling interests into account was approximately 2.3B EUR.

{kind=link}

The total capex was approximately 978M EUR (excluding the impact from asset disposals) which subsequently results in a net free cash flow of 1.32B EUR or approximately 2.91 EUR per share. Definitely not a spectacular result.

What does this mean for the full-year expectations?

Merck doesn’t seem to be too worried about the somewhat disappointing results in the first semester. The company emphasized it considers 2023 to be a transition year and confirmed its targets for 2025 are still valid.

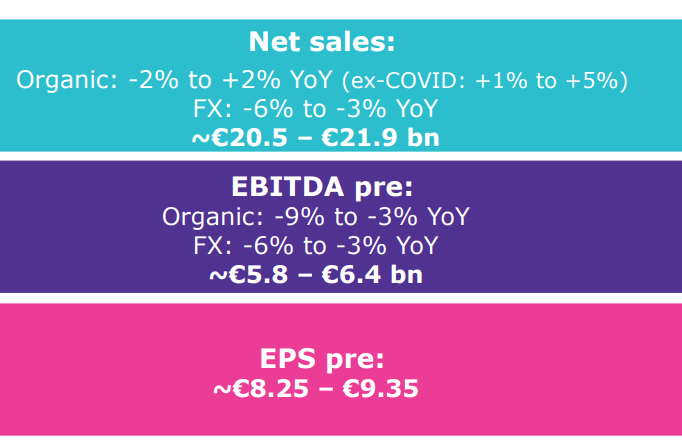

When it comes to 2023, the company did reduce its full-year guidance. Merck now expects to see a total revenue of 20.5-21.9B EUR which should result in an EBITDA of 5.8-6.4B EUR before non-recurring items. Considering the company already reported an EBITDA of 3.15B EUR in the first half of the year (also before non-recurring items), the guidance implies the second semester likely won’t be materially better with an EBITDA of 2.65-3.25B EUR. The full-year EPS will come in at 8.25-9.35 EUR (again before taking the non-recurring items into account).

{kind=link}

This means that at the current share price, Merck is trading at about 18.5 times earnings (using the midpoint of the 2023 earnings guidance). That’s not expensive given the track history of the company.

It’s also not ultra cheap but keep in mind the company has confirmed its guidance for 2025 wherein it expects to achieve a total revenue of 25B EUR. This means the total EBITDA should exceed 7B EUR and this should result in a pretty strong net income uplift of about 750M-1B EUR as well. This would boost the normalized EPS (before non-recurring items) to 10-11.50 EUR per share and the current share price represents a multiple of 15 times the forward 2025 earnings. Of course there are no guarantees, but in the past, Merck has proven to be pretty strong on the M&A front and as the free cash flow continues to pour in (albeit at a slower pace than initially expected), the German company is in an excellent position to take advantage of the weakness of others as the year-end net debt to EBITDA ratio should come in below 1.3, dropping to about 0.75-0.8 by the end of next year (assuming the 2025 target will be confirmed at the Capital Markets Day which has been scheduled for Q4 of this year).

Investment thesis

Would I be interested in Merck if I’d just take this year’s performance into account? Probably not. But the anticipated annual double digit revenue growth rate in 2024 and 2025 (and corresponding EBITDA growth) makes Merck worth considering. In my previous article I mentioned I was in no rush, and I still don’t think there is any urgency. But if 2023 should indeed be considered a "transition year," I’ ll likely have to establish a position before the capital markets day in October as the market could likely positively react to seeing the 2025 targets being confirmed once again.

I may consider writing put options perhaps with a strike price in the low-150 EUR range. I will provide an update in the comment section of this article once I have made a decision.

For further details see:

Merck KGaA: Expect A 10% CAGR EBITDA Increase In 2024-2025