DSKYF - Merck's Soaring Stock: Examining The Euphoria Amidst Potential Pitfalls

2024-01-08 08:01:09 ET

Summary

- Merck is a pharmaceutical giant whose medications and vaccines play key roles in the fight against viruses, cancer, and cardiovascular diseases.

- On October 26, 2023, Merck published results for the 3rd quarter of 2023, which left mixed feelings.

- The exclusivity of most of the company's medications and vaccines is set to expire within the next five years.

- However, in October, Merck entered into an agreement with Daiichi Sankyo to develop and subsequently commercialize three experimental antibody-drug conjugates for up to $22 billion.

- I'm initiating coverage of Merck stock with a "hold" rating.

Merck ( MRK ) is an American pharmaceutical company whose medications and vaccines play key roles in the fight against viruses, cancer, and cardiovascular diseases.

Thesis

Over the past two months, Merck's share price has risen more than 17%, reflecting stock market euphoria about the expected Fed interest-rate cuts in 2024, a partnership with Daiichi Sankyo (DSKYF) to develop and subsequently commercialize three experimental antibody-drug conjugates showing promising results in clinical trials and continued strong demand for Keytruda and Gardasil/Gardasil 9.

{kind=link}

However, in light of declining sales of Merck's diabetes franchise, the loss of exclusivity of many of its drugs and vaccines in the next five years, including Keytruda, which contributed about 39.7% of its total revenue for the third quarter of 2023, and the negative impact of reforms promoted by the Biden-Harris administration, I believe the current share price does not reflect these risks.

I'm initiating coverage of Merck with a "hold" rating.

Slight increase in full-year 2023 guidance, Merck's dividend yield, and the impact of the deal with Daiichi Sankyo

On October 26, 2023 , Merck published results for the 3rd quarter of 2023, which left mixed feelings. On the one hand, demand for its key products remains strong, which also led to an increase in its full-year sales forecast to $59.7-$60.2 billion, slightly higher than its previous guidance of $58.6-$59.6 billion. Nevertheless, due to the partnership agreement concluded with Daiichi Sankyo, the 2023 adjusted earnings guidance was lowered to $1.33-1.38 from the previous forecast of $2.95-$3.05.

On October 19, 2023 , the company agreed to the development and subsequent commercialization of three experimental antibody-drug conjugates: ifinatamab deruxtecan, patritumab deruxtecan, and raludotatug deruxtecan. Under the terms of the deal, Merck may pay Daiichi Sankyo up to $22 billion, depending on various criteria listed below.

{kind=link}

These product candidates continue to demonstrate promising results in clinical trials for the treatment of patients with ovarian cancer, small cell lung cancer, breast cancer, and solid tumors. Moreover, the company expects an FDA decision on the biologics license application for patritumab deruxtecan for the treatment of certain adult patients with NSCLC at the end of June 2024 .

On the other hand, the other two antibody-drug conjugates are being evaluated in phase 1 and 2 clinical studies, and as a result, I do not expect their approval in the next three years, which will also put pressure on Merck's operating income margin.

Over the past 13 years, Merck management has consistently increased dividend payments.

Source: graph was made by Author based on Seeking Alpha

{kind=link}

Meanwhile, the company's 5-year dividend growth rate is 9.3%, which, together with the cash dividend payout ratio [TTM] at 55.77%, indicates that there is no risk associated with a lowering in dividend payments in the medium term. However, Merck's dividend yield is 2.62%, which is not only below US consumer inflation but also below its key healthcare peers. As a result, this is one of the factors making Merck a less attractive asset for conservative investors.

Source: graph was made by Author based on Seeking Alpha

{kind=link}

Merck's oncology franchise has significant potential

In my estimation, the most important of the company's oncology products to its free cash flow is Keytruda (pembrolizumab), which is a monoclonal antibody that binds to the cell surface receptor PD-1, which ultimately enhances tumor immunosurveillance and inhibits further cancer progression.

Based on the results of 2023, the number of approved indications for Keytruda increased by six in the United States. So, on December 15, 2023 , the FDA approved the use of a combination of Merck's flagship product with Pfizer's Padcev ( PFE ) for the treatment of patients with locally advanced or metastatic urothelial cancer.

Source: table was made by Author based on Merck press releases

{kind=link}

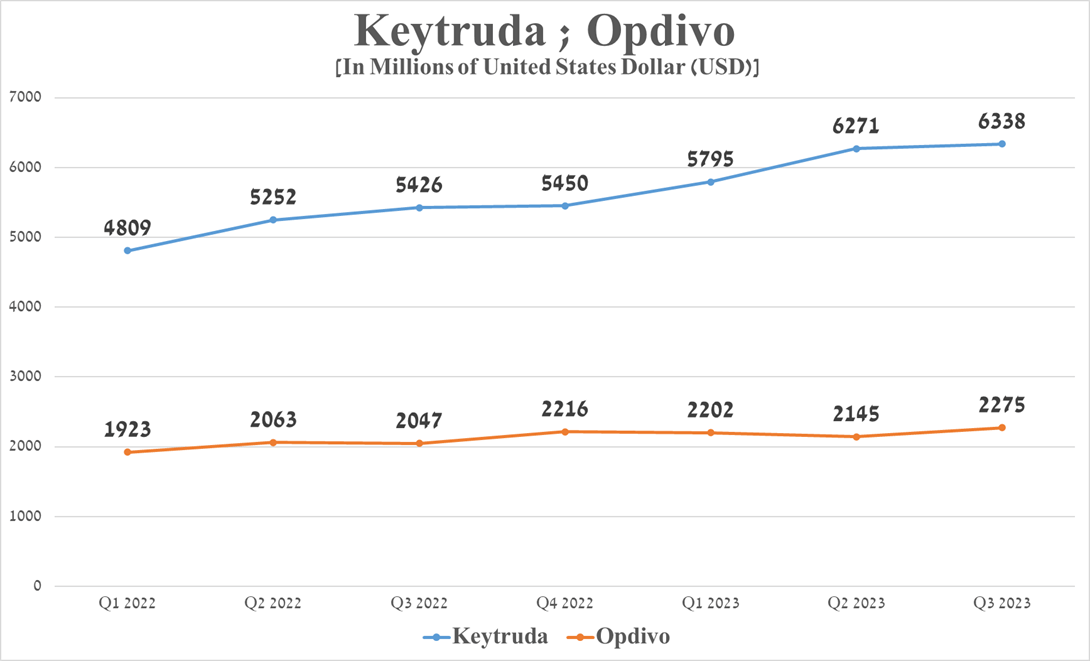

The company's star cancer medicine sales were approximately $6.34 billion in the third quarter of 2023, up $912 million from the prior year, primarily due to increased demand for the treatment of adult patients with breast cancer, melanoma, its label expansions, and geographic use.

Source: graph was made by Author based on 10-Qs and 10-Ks

{kind=link}

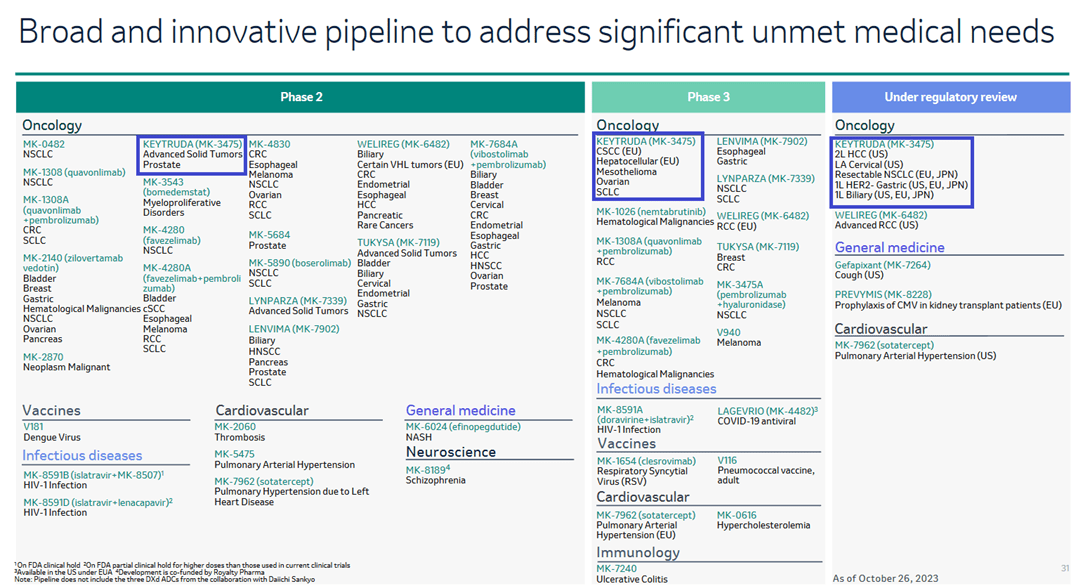

In the upcoming years, I expect continued growth in its sales, driven by an increase in the number of indications for its use since it has a unique mechanism of action that allows it to combat various types of cancer effectively. In addition, Merck continues to evaluate its efficacy in numerous clinical trials , including in combination with favezelimab, quavonlimab, and vibostolimab, which could potentially increase patient lifespan.

{kind=link}

Merck's diabetes franchise continues to fall in sales

Merck has two FDA-approved drugs used to treat type 2 diabetes.

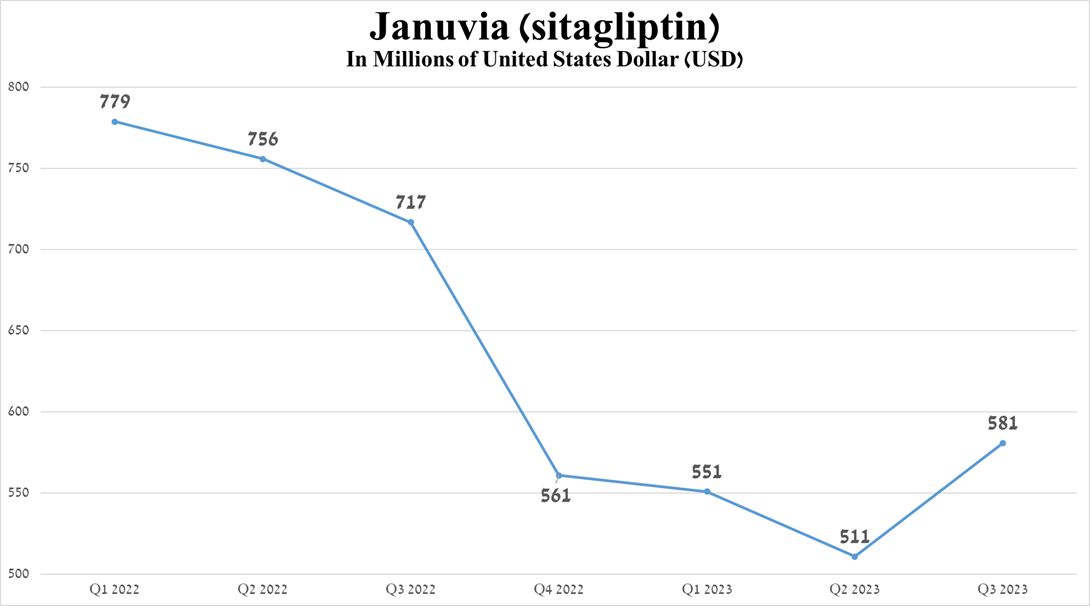

The first of these is Januvia (sitagliptin), whose mechanism of action is based on the inhibition of DPP-4. Its sales were $581 million for Q3 2023, down 23.4% year-over-year due to increased competition from its generic versions in Europe.

Source: graph was made by Author based on 10-Qs and 10-Ks

{kind=link}

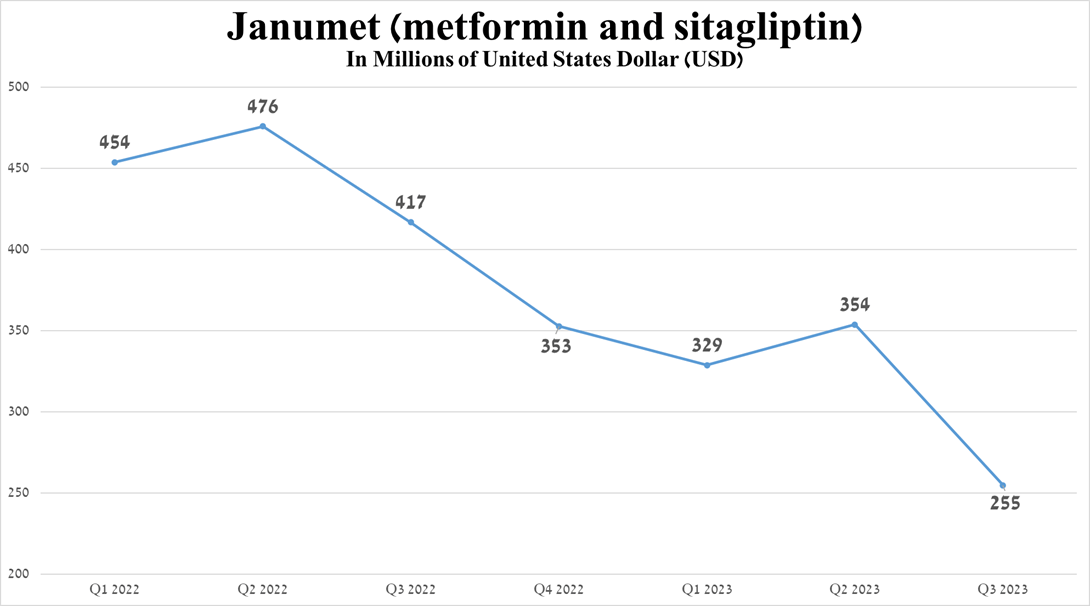

The company's second product is Janumet (sitagliptin and metformin HCl), whose sales were $255 million in the three months ended September 30, 2023, down 63.5% from the third quarter of 2023, due to the continued negative impact of the loss of its exclusivity and decline demand for it as a result of the launch of more effective drugs, including Novo Nordisk's Ozempic ( NVO ) and Eli Lilly's Mounjaro ( LLY ).

Source: graph was made by Author based on 10-Qs and 10-Ks

{kind=link}

Merck's Financial Results And Outlook

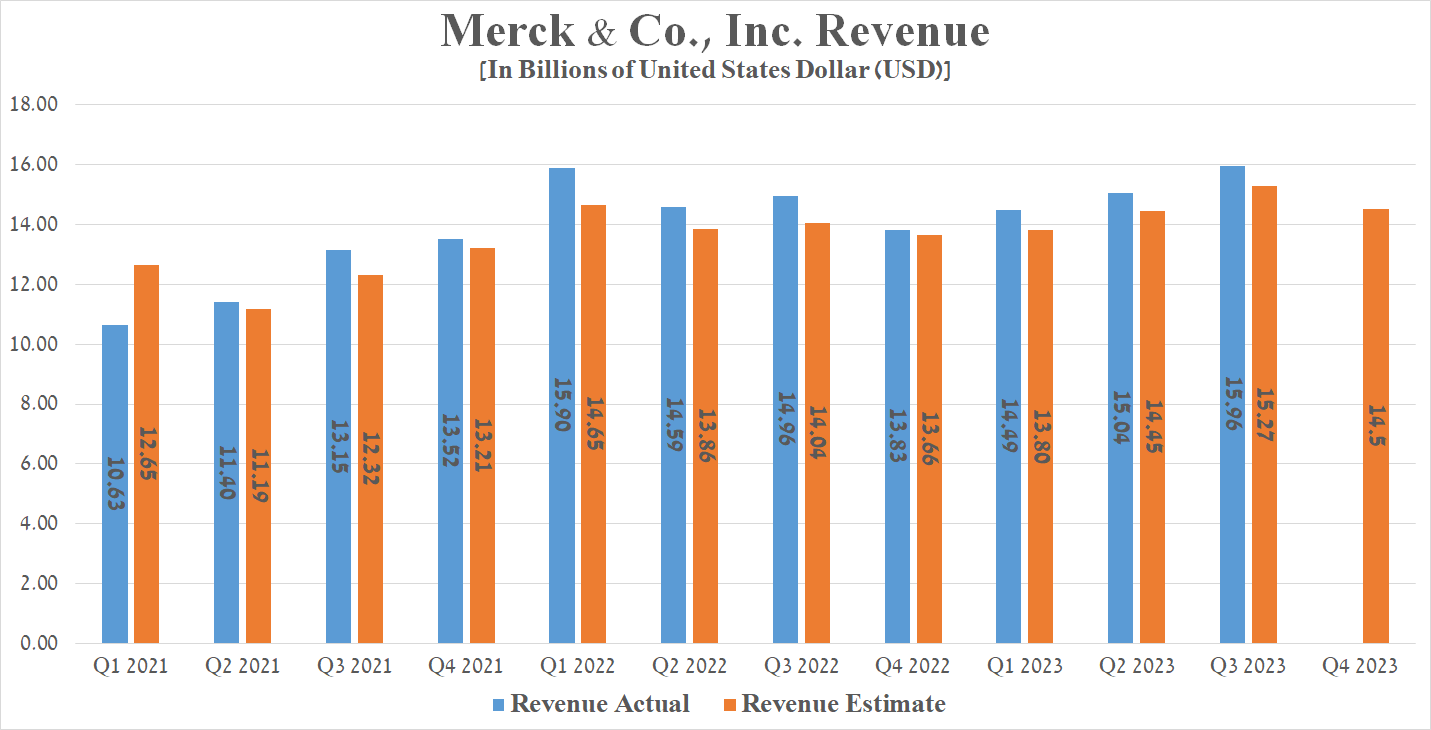

Merck's revenue for the three months ending September 30, 2023, reached about $15.96 billion, a 6.7% increase over the previous year, and beat analysts' expectations by $730 million.

{kind=link}

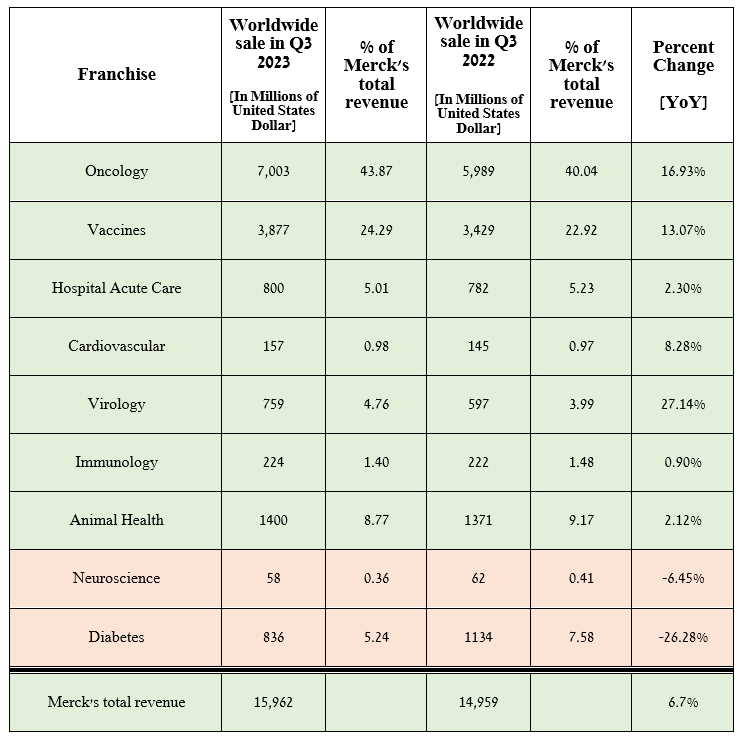

The growth of this indicator was primarily due to an increase in sales of oncology, vaccines, virology franchises, and the Animal Health segment.

Source: graph was made by Author based on 10-Qs and 10-Ks

{kind=link}

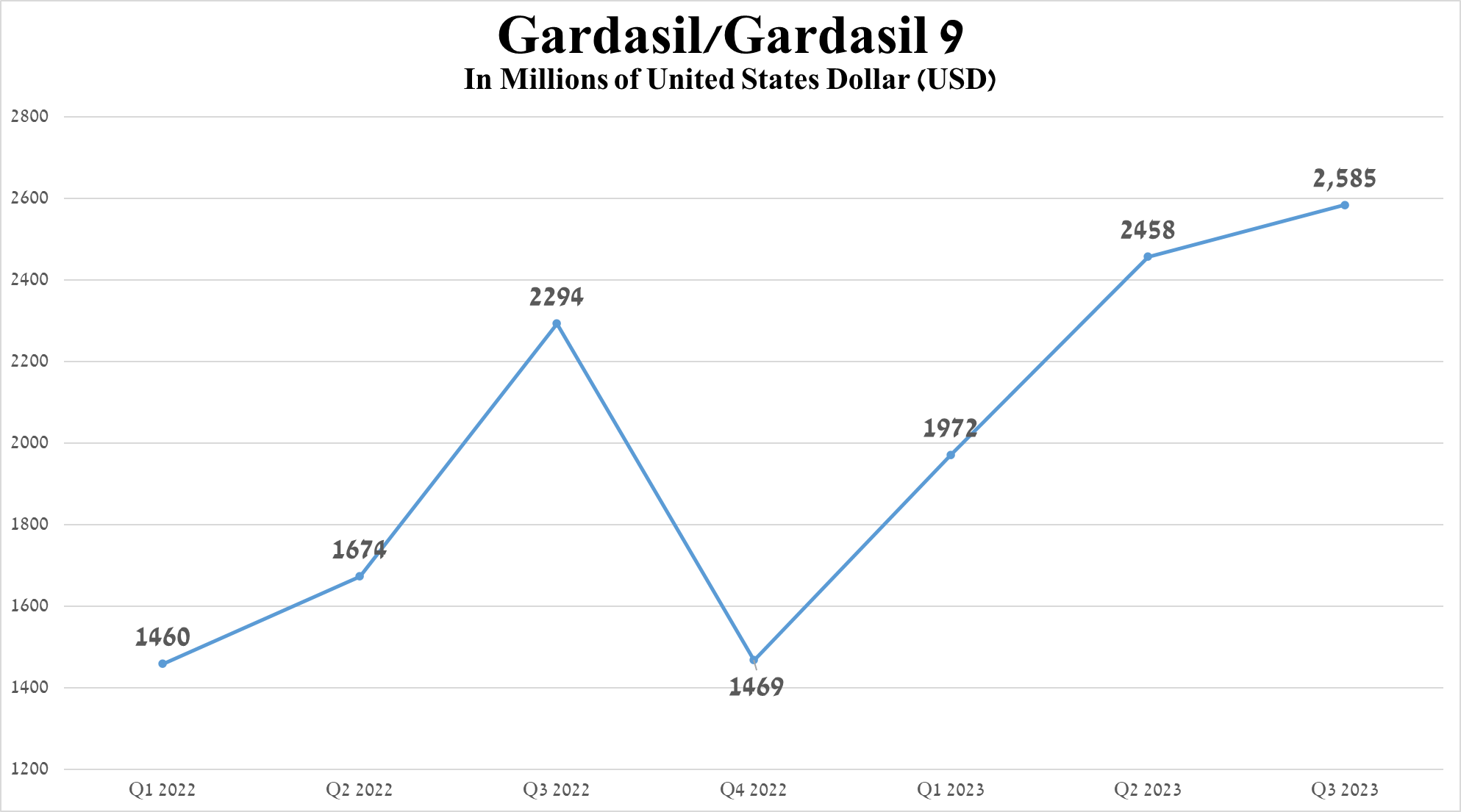

For example, sales of Gardasil/Gardasil 9, a vaccine that protects against several strains of the human papillomavirus ((HPV)), reached $2,585 million in the three months ended September 30, 2023, an increase of 12.7% compared to the third quarter of 2022 due to increased demand in the United States and the European Union and also the label expansion of Gardasil 9 in China.

Source: graph was made by Author on 10-Qs and 10-Ks

{kind=link}

I expect sales of the Gardasil franchise to continue to grow until it loses US exclusivity in 2028, as human papillomavirus is a common infection and a contributing cause of cancer, including colorectal, oropharyngeal, cervical, and squamous cell carcinoma. So, according to the CDC , HPV-attributable cancers are diagnosed in tens of thousands of people every year.

{kind=link}

Seeking Alpha offers financial data on Wall Street analysts' expectations for the coming quarters. So, Merck's revenue for the fourth quarter of 2023 is expected to range from $14.2 billion to $14.8 billion, which is about 5% more than the fourth quarter of 2022

On the other hand, the company's price/sales [FWD] is 4.96x, indicating that it is trading at a premium to most of its competitors in the cancer therapeutics market, including Bristol-Myers Squibb ( BMY ), Roche Holding ( RHHBY ), and Pfizer.

{kind=link}

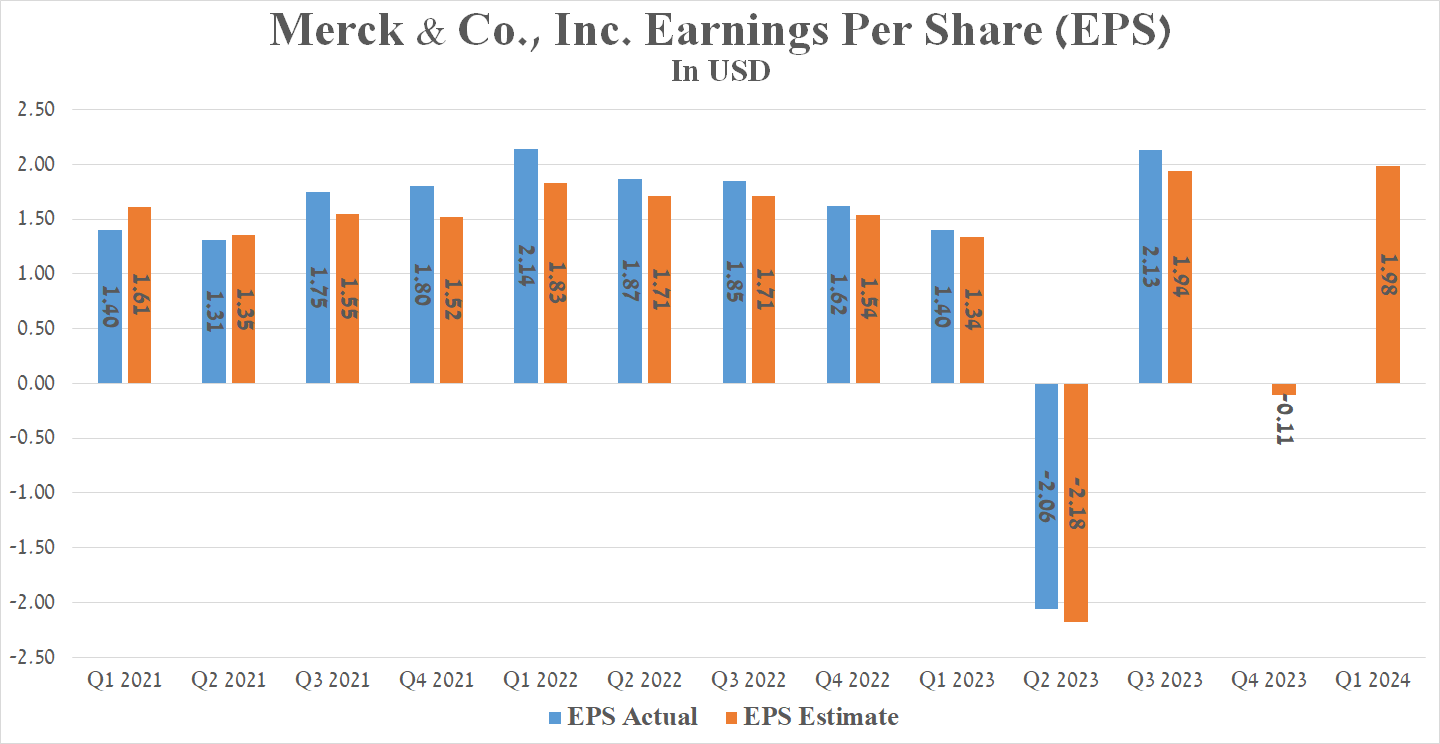

Merck's Q3 Non-GAAP EPS was $2.13, beating analysts' consensus estimates by $0.18. However, its EPS is anticipated to be in the range of -$0.17 to -$0.06 in the fourth quarter of 2023, declining sharply relative to the fourth quarter of 2022 due to the acquisition of Caraway Therapeutics for $610 million and the signing of a partnership agreement with Daiichi Sankyo for a total of up to $22 billion.

{kind=link}

On a more global level, Merck's EPS is expected to grow through 2028. The increase in this financial metric is accompanied by an anticipated decrease in the Non-GAAP P/E ratio from the current 16.25x to 13.17x.

As a result, this indicates that some financial market participants continue to remain optimistic despite my expected technical correction in Merck's share price and the potential impact of the risks that will be presented later in the story.

{kind=link}

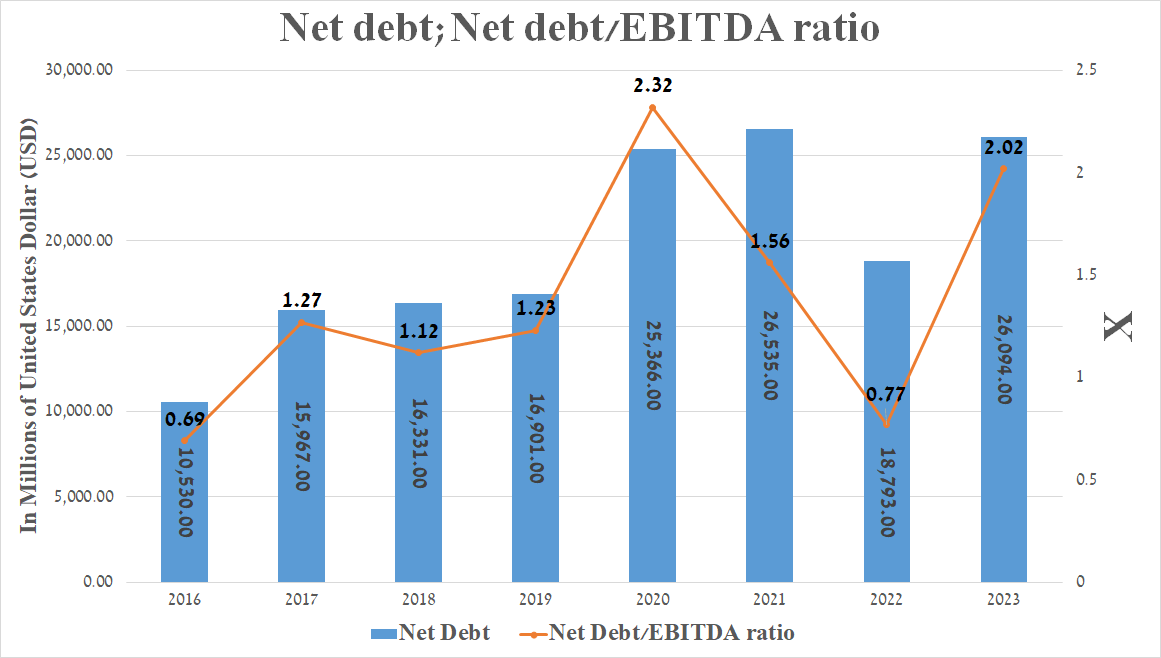

It is equally important to discuss Merck's debt, which, in my opinion, is not a risk to its financial position since it has a stable cash flow, growing sales of Keytruda, and a rich pipeline of experimental drugs.

So, its net debt amounted to about $26.1 billion at the end of September 2023, while its net debt/EBITDA ratio increased significantly compared to 2022 due to the need to finance the acquisition of Prometheus Biosciences and an agreement with Daiichi Sankyo.

{kind=link}

Key Risks To Consider

I highlight two main risks due to which I initiate coverage of Merck with a "hold" rating. Financial market participants must consider these risks to make informed decisions aimed at minimizing possible losses.

Exclusivity for most Merck products expires in the next five years

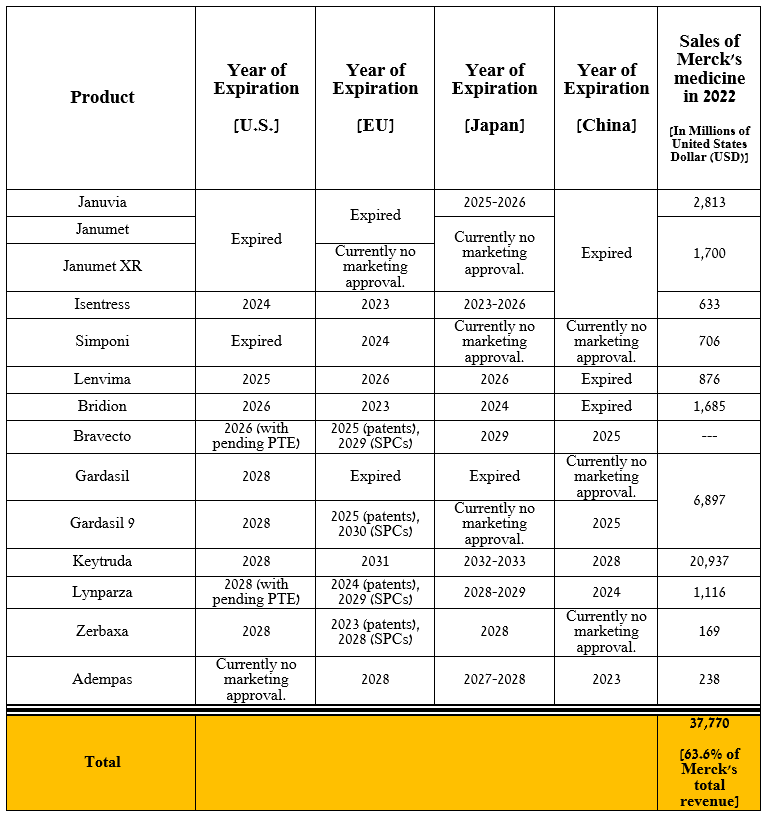

The first risk I highlight, which is crucial to the company's long-term financial position, is the expiration of exclusivity for most of its medications and vaccines in the next five years. Merck's sales of these products amounted to $37.77 billion in 2022, or 63.8% of its total revenue, which is a significant figure.

Once the exclusivity of the drug and vaccine expires, pharmaceutical companies will have the right to commercialize generic versions or biosimilars, ultimately leading to a sharp drop in demand for Merck's products. In my assessment, its management will have to continue pursuing an aggressive M&A policy to strengthen and diversify its oncology and vaccine franchises.

Source: table made by Author based on 10-K

{kind=link}

The impact of Biden's Inflation Reduction Act on Merck's financial position

Government regulation and the Inflation Reduction Act adopted in 2022 may negatively impact Merck's business. These changes include negotiating with Medicare, introducing discounts on medications covered under Medicare Part B and Part D, and introducing penalties if drug prices rise faster than inflation.

{kind=link}

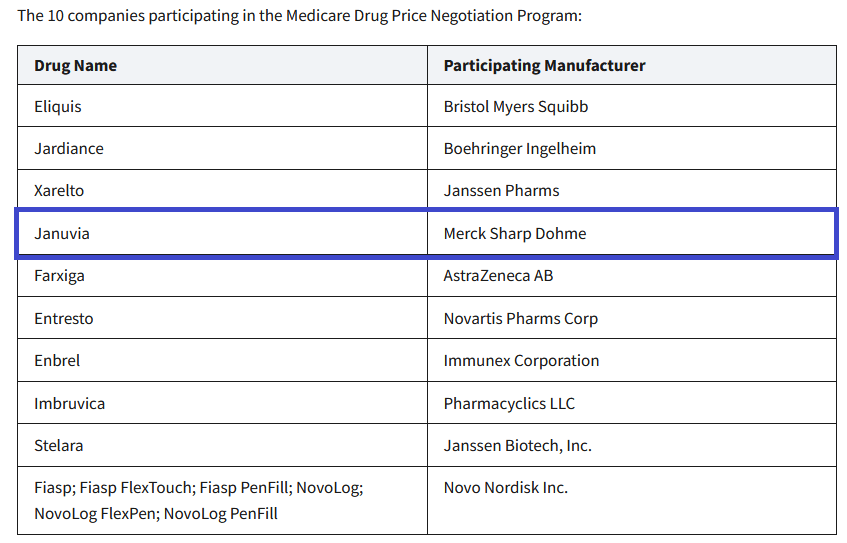

In October 2023 , the Biden administration released a list of 10 Part D-covered medications for which Medicare will negotiate prices. Januvia, which I talked about earlier in the article, ended up on this list, and, as a result, this creates an additional financial risk for Merck's diabetes franchise.

{kind=link}

In my assessment, the impact of the Biden-Harris administration's regulations and reforms on the pharmaceutical industry could slow Merck's revenue growth rate beginning in 2025, and as a result, its management will need to reconsider its R&D policy, including through the suspension of the development of some of its experimental drugs.

Takeaway

Merck is an American pharmaceutical company whose medications and vaccines play key roles in the fight against viruses, cancer, and cardiovascular diseases.

Merck is known worldwide for Keytruda, its star cancer medication that generates tens of billions of dollars annually. Additionally, through its partnership with Daiichi Sankyo, the company has significantly strengthened and diversified its oncology portfolio with three antibody-drug conjugates, one of which could be approved by the end of June 2024.

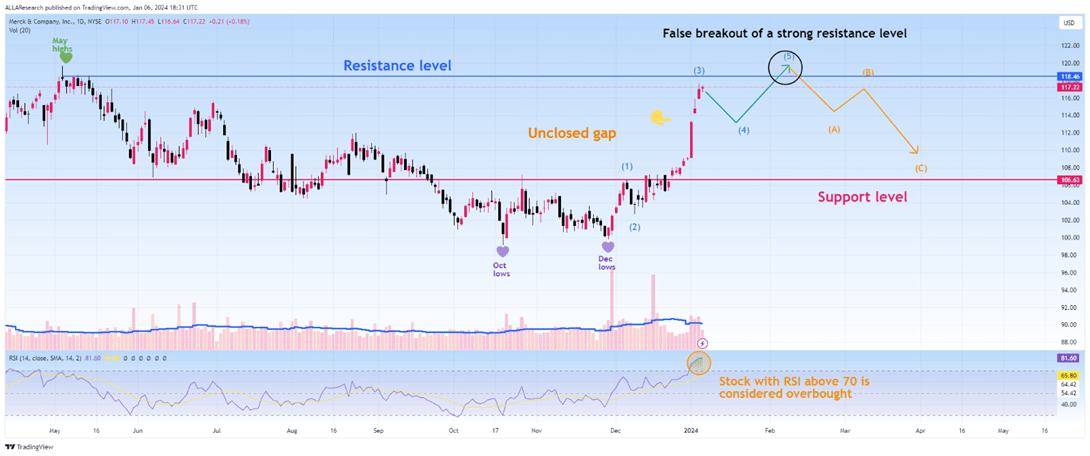

On the other hand, due to a significant drop in sales of the company's diabetes franchise, the loss of exclusivity of fourteen of its products in the next five years, its shares being overbought according to the RSI indicator, and reaching a strong resistance zone, I expect a technical pullback of Merck's stock to $106-$108.

I'm initiating coverage of Merck with a "hold" rating.

For further details see:

Merck's Soaring Stock: Examining The Euphoria Amidst Potential Pitfalls