MRCY - Mercury Systems: A 'Show Me' Stock

2023-12-26 03:40:31 ET

Summary

- Military focused Mercury Systems, Inc. is experiencing a decline in top-line growth and profitability, leading to a drop in share prices.

- However, the company's cash flow and net leverage situation are expected to improve in the latter half of FY24.

- The newly onboarded CEO, insider buying, and activist involvement warrant further analysis of the company's prospects.

- A full investment analysis follows in the paragraphs below.

An evil enemy will burn his own nation to the ground to rule over the ashes ."~ Sun Tzu

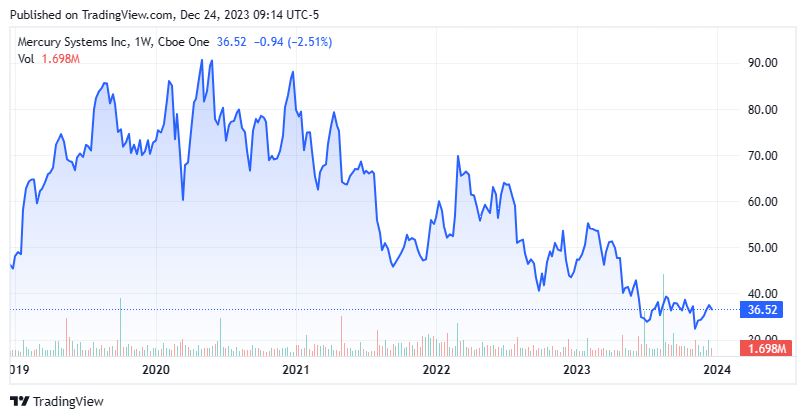

Shares of military semiconductor concern Mercury Systems, Inc. (MRCY) are trading near five-and-half year lows as top-line growth and profitability have ground to a halt. However, the company's cash flow and net leverage situation should improve in the latter half of FY24 as finished programs result in unbilled receivables and costs in excess of billings converting to cash. With valuations still somewhat elevated despite shares of MRCY falling 65% since April 2020, a newly onboarded CEO aligned with activists, the recent insider buying merited a deeper dive. An analysis follows below.

{kind=link}

Company Overview:

Mercury Systems, Inc. is an Andover, Massachusetts based provider of processing power to defense contractors and the commercial aviation industry. The company has grown through 15 acquisitions since 2015, allowing it to offer a suite of products from its end-to-end processing platform, including electronic warfare, sensor, scanner, display system, server, hardware, radio frequency, and microwave solutions. Mercury was formed in 1981 and went public in 1998, raising net proceeds of $18.6 million at $5.25 per share, after giving effect to a two-for-one split in 1999. Shares of MRCY trade just over $36.00 a share, translating to an approximate market cap of $2.15 billion.

The company operates on a 52- or 53-week fiscal year (FY) ending the Friday closest to June 30th. For the avoidance of doubt, the 52-week period ending June 30, 2023 is FY23.

Mercury has spent the past decade evolving from a provider of advanced embedded processing components (circuits, switches, and sensors) for the defense industry - including core radar processors for Patriot missiles and Predator drones - to entire subsystems, such as aircraft displays and flight control units. This shift in strategy was accomplished through the purchase of complementary component concerns, whose output could be combined into modules, subassemblies, and subsystems, which are larger ticket items with higher gross margins than semiconductors. The 15 acquisitions have cost Mercury just shy of $1.5 billion since FY14, with the last four being financed by debt.

Revenue Recognition

Part of the confusion as it relates to assessing the company relates to its two types of contracts. With performance obligation contracts, Mercury recognizes revenue at point in time (i.e., when the finished product is delivered). This method accounted for 44% of its FY23 revenue. The company also engages in contracts for the design, development, production, or modification of complex modules and subassemblies or integrated subsystems where the revenue is recognized over time. However, with over-time contracts, a significant majority of the cash may not be received until after the product is delivered, resulting in significant unbilled receivables and costs in excess of billings. Over-time contracts represented 58% of Mercury's FY23 revenue.

Operational & Share Price Performance

Owing to this growth-by-acquisition strategy, revenue surged from $208.7 million in FY14 to $924.0 million in FY21 as Adj. EBITDA climbed from $23.5 million to $201.9 million. Earnings also improved markedly, from a loss of $0.13 a share (GAAP - continuing operations) to $2.42 a share (non-GAAP) over the same period. The market applauded these results, rallying shares of MRCY 749% from $11.34 at the end of FY14 to an all-time high of $96.29 in April 2020, representing a priced-for-perfection PE multiple on FY21 EPS of 39.8.

Mercury was then beset with supply chain issues and execution challenges at some of its 300+ programs, resulting in operational disappointment. An initial FY22 forecast of $2.50 a share (non-GAAP) and Adj. EBITDA of $223.5 million on revenue of $1.02 billion (all based on range midpoints) proved overly optimistic with the company ultimately posting $2.19 a share (non-GAAP) and Adj. EBITDA of $200.5 million on revenue of $988.2 million. This relative underperformance attracted the interest of activist investor Jana Partners, who pushed for the sale of Mercury as early as December 2021. Management responded with a poison pill measure. That move incurred the wrath of another activist investor Starboard Value, who publicly asked management to rescind its shareholder rights plan and consider selling Mercury.

The desires of Jana and Starboard seemed a longshot with the FTC blocking Lockheed Martin's ( LMT ) attempt to purchase rocket engine manufacturer Aerojet Rocketdyne and the Department of Defense stating that consolidation within the industry could be a threat to national security - both in early 2022. However, the activists were successful in placing two directors on the company's board in June 2022.

The following month, GlassHouse Research issued a short report on Mercury, openly accusing it of prematurely recognizing revenue and calling its December 2020, $310 million acquisition of Physical Optics a "disaster". The company followed that shot across the bow with a FY23 forecast that was both below Street expectations and ultimately too buoyant. Initial guidance of $2.07 a share (non-GAAP) and Adj. EBITDA of $207.5 million on revenue of $1.03 billion did not match actual output of $1.00 a share (non-GAAP) and Adj. EBITDA of $132.3 million on revenue of $973.9 million as 20 'challenged' programs contributed to the preponderance of ~$56 million in cost overruns during FY23.

As that disappointing performance was unfolding, management bent to its activist shareholders' wishes, initiating a review of strategic alternatives in January 2023, citing that the opportunity to pull ~$300 million of cash out of its working capital - namely, its unbilled receivables and costs in excess of billings - should be attractive to a potential investor. However, there were no takers and the company decided to move forward in June 2023, installing one of the two directors placed on its board in June 2022 as its new CEO. Bill Ballhaus was subsequently joined by new CFO David Farnsworth in August 2023 to engineer a turnaround. Mercury's first crack at an outlook for FY24 was $1.31 per share and Adj. EBITDA of $172.5 million on revenue of $975.0 million, representing gains of 31%, 30%, and 0% (respectively) versus FY23, based on range midpoints. Disappointed with no sale, the market shunned shares of MCRY, which were down 18% in calendar 2023YTD and 62% from their all-time high when the company reported its 1QFY24 results after the close on November 7, 2023.

1QFY24 Financials

Mercury posted a loss of $0.24 a share (non-GAAP) and Adj. EBITDA of $2.0 million on net revenue of $181.0 million versus a gain of $0.24 a share (non-GAAP) and Adj. EBITDA of $31.2 million on net revenue of $227.6 million in 1QFY23. These metrics badly missed Street consensus of a $0.17 gain (non-GAAP) on net revenue of $218.6 million.

November Company Presentation

Bookings in the quarter totaled $191.5 million, equating to a book-to-bill ratio of 1.06. The company's total backlog as of September 29, 2023 was $1.15 billion, representing a $73.3 million increase from a year earlier. Management anticipated that $732.8 million would be converted into recognizable revenue over the ensuing twelve months.

A higher mix of low-margin development programs - which should eventually transition into steady revenue generating production programs - cost inflation, and the aforementioned 20 troubled projects were blamed for a year-over-year gross margin decrease of 640 basis points to 27.9%.

Despite the big miss, management viewed these issues as transient and raised the midpoint of its non-GAAP EPS guidance from $1.31 to $1.37 per share without altering the balance of its FY24 outlook. It said it anticipated having the majority (~11 of 20) of its challenged programs completed by YEFY24.

November Company Presentation

The market was unimpressed, selling its stock down 13% in the subsequent trading session to $32.15 a share, eventually bottoming out at a five-and-a-half year low of $31.04 on November 9th.

Balance Sheet & Analyst Commentary:

November Company Presentation

With free cash flow of negative $47.1 million in the quarter, Mercury's balance sheet is getting more tenuous, with debt of $576.5 million and cash of $89.4 million on September 29, 2023. The company's rising net leverage, which now stands at 4.7, prompted the company to obtain an amendment to a net leverage ratio covenant on its revolver from 4.5 to 5.25. It has $190 million of remaining availability on its facility. Mercury does not pay a dividend or repurchase its stock.

November Company Presentation

The Street also leans cautiously on Mercury's prospects, featuring three buy or outperform ratings against five holds and a median twelve-month price objective of just over $35 a share. On average, they expect the company to earn $1.14 a share (non-GAAP) on revenue of $957 million in FY24, followed by $1.60 per share (non-GAAP) on net revenue of $1.01 billion in FY25.

Jana, unable to find a suitor for Mercury and represented on its board by partner Scott Ostfeld, used the post-earnings weakness as an opportunity to cost average, purchasing 259,922 shares at an average price of $33.42 on November 16th-20th to bring its total ownership interest to 8.4%.

Verdict:

Owing to large and early inventory builds during the post-pandemic supply chain crisis, revenue was recognized on some programs as part of the company's protocol, but the actual billing and cash collection hasn't yet occurred. This undercurrent should begin to abate in 2HFY24 as some troubled programs complete, resulting in relatively low revenue recognition but significant cash inflows. Going forward, with supply chain issues on the wane, Mercury will be able to purchase the necessary equipment on a just in time basis, which will also result in superior cash balances. That said, the stock is not especially cheap at an EV/TTM Adj. EBITDA of over 23 and a PE ratio on FY24E EPS of just over 32 or FY25E EPS of 23. Furthermore, there is no growth story, with FY25 net revenue projected to be only 1% higher than FY22. Mercury is a show me stock and investors should treat it as such.

The obedient always think of themselves as virtuous rather than cowardly. "~ George Carlin

For further details see:

Mercury Systems: A 'Show Me' Stock