BOWL - Meridian Contrarian Fund Q2 2023 Investment Commentary

2023-08-18 02:21:00 ET

Summary

- Meridian Funds, advised by ArrowMark, are actively managed and focus on market segments and industries that offer the ability to gain a distinct competitive advantage. Our long-only equity strategies primarily focus on the U.S. small- and mid-capitalization universe.

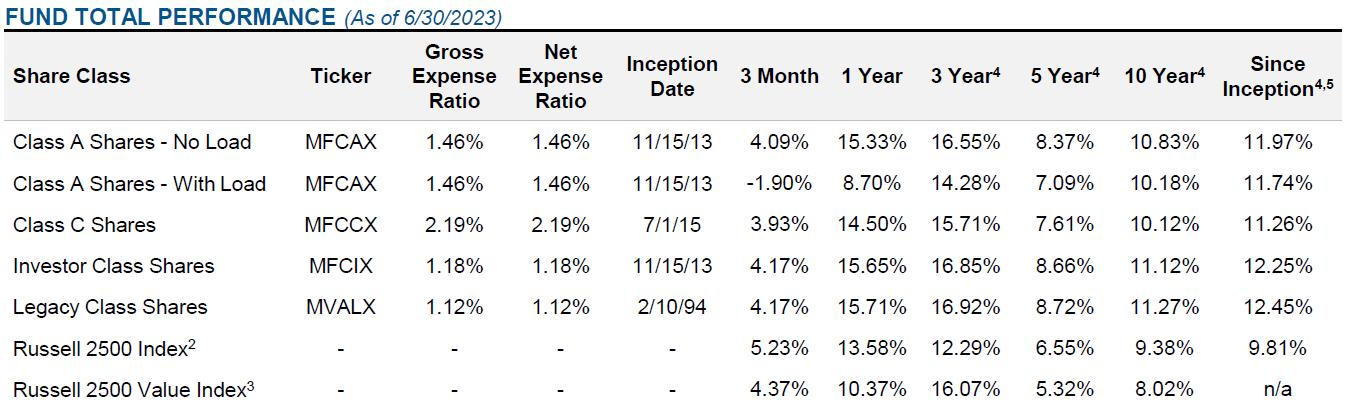

- The Meridian Contrarian Fund returned 4.17% (net) for the quarter ending June 30, 2023, underperforming its benchmark, the Russell 2500 Index, which returned 5.23%.

- The three largest individual contributors to the Fund’s relative performance during the quarter were SMART Global Holdings, Inc., First Citizens BancShares, Inc., and Molson Coors Beverage Company.

Market Summary

With inflation gradually easing and the U.S. economy largely holding firm, stocks generally advanced during the second quarter. Conditions prompted U.S. Federal Reserve (“Fed”) officials to pause their aggressive rate-hike campaign in June and forecast that the U.S. would avoid a recession in 2023. Fed Chair Jerome Powell did assert, however, that markets should expect further rate increases in the coming months, perhaps as many as two more by year-end. Yet a rally in June driven by cyclical names seemed to reflect anticipation of imminent rate cuts. Meanwhile, running counter to stock investors’ general optimism, bond investors drove short- and long-duration yields higher, further sharpening the already inverted U.S. Treasury yield curve.

Fueled by a surge in artificial intelligence-related technology stocks, double-digit gains in large-cap growth stocks led the stock market higher, according to the Russell family of indices. Among midcap and small-cap stocks, growth stocks outperformed value stocks. Within the Fund, consumer sector stocks detracted as slowing consumer spending curtailed gains, while a rebound in semiconductor chip stocks bolstered returns from the technology sector.

Fund Performance

The Meridian Contrarian Fund (the “Fund”) ([[MVALX]], [[MFCIX]], [[MFCAX]], [[MFCCX]]) returned 4.17% (net) for the quarter ending June 30, 2023, underperforming its benchmark, the Russell 2500 Index, which returned 5.23%. Additionally, the Fund slightly underperformed its secondary benchmark, the Russell 2500 Value Index, which returned 4.37% during the period.

Our investment process seeks to identify out-of-favor companies that we believe have depressed valuations and visible catalysts for sustainable improvement. Experience has taught us that businesses with the potential for earnings growth and multiple expansion can be a powerful source of outperformance. As such, we employ a fundamental research-driven process that includes screening for companies that have multiple quarters of year-over-year earnings declines; exploring the reason for the declines; and singling out the companies we believe are poised for earnings rebound via a cohesive turnaround plan, a new management team, or through improvements or changes to the business. The outcome of this process is a concentrated portfolio of 50-75 of our best ideas. With a process that prioritizes the management of risk over the opportunity for return, we scrutinize the quality of each prospective investment’s business model and its valuation. Our high standards for quality require that a company have a durable competitive advantage, improving return on invested capital, and free cash flow, as well as sustainable future earnings growth. While we manage the Fund from the bottom up based on individual company fundamentals, we augment this by monitoring overall portfolio characteristics as part of our risk-management process.

Two of our primary risk measures are beta-adjusted weight and downside capture, both of which we measure at the portfolio, sector, and individual company levels. We analyze the beta-adjusted weights of portfolio holdings against the Russell 2500 Index to determine how sensitive each holding is to movement in the broader market and identify where our risk exposure lies within the portfolio. Depending on the degree to which a stock correlates closely with market movement (high beta) or inversely to the market (low beta), we may increase or decrease our weighting to align with the Fund’s risk parameters, as we prioritize risk before reward. Downside capture measures how much a stock will potentially decline, relative to an overall market decline, with lower capture representing lower risk. For both these measures, we focus on absolute levels and changes over time. This is part of our ongoing process of recycling capital, and we are comfortable with the Fund’s current lower-risk profile.

BOTTOM THREE DETRACTORS

The three largest individual detractors from the Fund’s relative performance during the period were Bowlero Corp. ( BOWL ) , First Interstate BancSystem, Inc. ( FIBK ) , and Okta, Inc. ( OKTA ).

Bowlero Corp. owns and operates nearly 350 bowling centers across the U.S., Mexico, and Canada. In a highly fragmented market - it’s greater than six times larger than its nearest competitor - Bowlero is focused on revitalizing the bowling experience for family, corporate, and nightlife entertainment. Centered around bowling, arcades, other amusements, and better food and beverage offerings, Bowlero’s business was greatly diminished during the pandemic, which distorted its underlying profitability and cash flow when it went public via a SPAC in 2021. By early 2022, the valuation was deeply discounted and we invested in the belief that Bowlero could produce significantly higher profits than its bowling center competitors, allowing it to deploy cash to acquire and convert more centers to keep growing for years to come. During the quarter, the company reported strong results and announced its acquisition of the Lucky Strike chain, which operates 14 higher-end bowling centers in nine states. The stock declined, however, as management gave guidance that reflected a return to normal season demand patterns after two years of consistent sequential growth following the pandemic shutdowns. As we viewed the setback as temporary within the context of the continued growth and long-term value creation we believe the company will generate, we added to our position.

First Interstate BancSystem, Inc. is a regional bank with a leading presence in the Mountain West region of the U.S. and approximately $32 billion in assets. The stock lagged the market in late 2021 and early 2022 as a delayed regulatory review of a merger slowed the company’s ability to grow and return capital while it was simultaneously investing in technology to improve operational efficiencies. First Interstate, however, has a history of consistently profitable growth supported by a high-quality deposit base, which has generally led to better-than-peers growth in commercial, real estate, and agricultural lending. Therefore, we invested as we believed conditions created a historical discount to the firm’s normalized earnings. During the quarter, the stock underperformed amid the fallout from the springtime collapse of three regional banks. It was also pressured by themarket’s distaste for banks with elevated exposure to commercial real estate ((CRE)), although First Interstate’s CRE holdings were largely tied to smaller towns in the Midwest through Pacific Northwest, and competitive pressures from larger banks. While the latter contributed to our decision to reduce our position - First Interstate reported deposit losses as savers sought higher interest rates elsewhere - we maintained a stake due to our belief in the bank’s fundamental strength and management’s history of managing through exogenous shocks that ultimately strengthen the business.

Okta, Inc. develops identity and access management software that enhances security while streamlining access to authorized resources for enterprises and consumer-facing applications. We invested in the stock in late 2022 after earnings declined following an acquisition that was unpopular with the market and, more importantly, many inside the company. Although the company experienced significant salesforce attrition and leadership changes in the wake of the deal, we believed that Okta still had the leading product in the industry and that the sales staff turmoil, which is not uncommon in the software industry, was fixable. Furthermore, we found the risk/reward profile attractive as the company’s price-to-sales multiple had plummeted, and the balance sheet remained strong. Since we first invested, Okta stock has performed well, but it declined in the quarter after management discussed a potential macro slowdown during the quarterly earnings call. Despite the potential macro pressures, the company raised earnings estimates due to business improvements that validated our initial investment thesis, and we maintained our position in the stock.

A holding that warranted an additional investment during the quarter was LiveRamp Holdings, Inc. , a developer of a data connectivity platform that sharpens targeted advertisement placements while shielding consumer data privacy. The company’s technology allows improved advertising targeting and measurement across internet-based, streaming, and traditional verticals while meeting the ever-shifting data privacy regulations being enacted globally. We initially invested in the first quarter of 2023 following a difficult 2022 in which advertising spending slowed and LiveRamp rolled out new products and brought on new salespeople - which all combined to drive down earnings. In addition to the investments in future growth, however, management also reduced legacy products, which has lowered costs and improved earnings and cash flow through the first part of 2023, despite a still-tough advertising environment. We added to our position during the second quarter as the company’s internally-driven earnings turn appeared to take hold, emphasizing our approach to opportunistic value and gaining access to one of the fastest-growing advertising verticals such as streaming television.

TOP THREE CONTRIBUTORS

The three largest individual contributors to the Fund’s relative performance during the quarter were SMART Global Holdings, Inc. ( SGH ) , First Citizens BancShares, Inc. ([[FCNCA]], [[FCNCB]]) , and Molson Coors Beverage Company ([[TAP]], [[TAP.A]]).

SMART Global Holdings, Inc. is a diversified technology company that designs and manufactures solutions in the computing, memory, and LED industries. We first invested in the company in 2020 on the heels of an earnings decline due to volatility in the memory business, order delays in the high-performance computing business, and temporarily dilutive investments in new products. Individually, none of these developments are particularly unusual, but it is uncommon for all three to turn negative simultaneously. Our initial investment thesis was that the company’s new management team would smooth out such volatility while driving growth through effective capital allocation and organic investment. We also believed strong secular trends were in place for the memory business, given the increased importance of memory for computing speeds and climbing demand for device memory overall, and the high-performance computing industry due to the rising integration of artificial intelligence ((AI)) and machine learning. During the quarter, SMART Global’s stock rallied as the company delivered an impressive earnings report, led by AI-related strength in its high-performance computing business. Although AI has only recently hit the mainstream, SMART Global has been involved in the space since its acquisition of Penguin Computing in 2018. Additionally, the company sold a volatile Brazil division, a transaction that could temporarily lower earnings, but we believe will improve earnings consistency over time and therefore boost the stock’s valuation multiple. The stock trades at a reasonable valuation, which we believe will improve as the company demonstrates growth and more investors learn of this under-the-radar AI investment. We continued to hold a large position in SMART Global.

First Citizens BancShares, Inc. is a regional bank located in the southeast U.S. with strong legacy relationships and a history of acquiring troubled bank assets at advantageous valuations and folding them into its strong foundation. Thecompany has acquired 16 banks in FDIC receivership since 2009. Its deal to purchase national lender CIT, which was announced in late 2020, diminished earnings through late 2021 and early 2022 as the company tempered its capital use while regulators reviewed and ultimately approved the deal.

This scenario allowed us to initiate a position in the stock at a relatively inexpensive valuation. Our analysis indicated that First Citizens’ long track record of consistent earnings growth due to its focus on relationship lending and conservative underwriting has led to above-peer returns on equity. During the quarter, First Citizens posted strong results due in part to its March acquisition of the assets of Silicon Valley Bank ( SIVBQ ), which doubled the book value of First Citizens when the deal closed. Going forward, we believe the benefits realized from that advantageous deal, along with management’s conservative risk management and the firm’s strong capital position, will enable the company to grow earnings and return capital to shareholders for several years. In keeping with our risk-management framework, we reduced our exposure after the stock’s strong performance, although it remains a top position in the portfolio.

Molson Coors Beverage Company is the second-largest brewing company in the U.S. and ranks among the Top 5 globally. For several years, the company struggled to grow earnings as domestic beer lost share to imports, craft brewers, seltzer, and other alcoholic beverages, and we avoided investing in it due to a lack of a solid strategy to revitalize growth. In the third quarter of 2021, however, we decided the risk/reward profile tipped in our favor as management was following a coherent innovation plan, our industry research indicated improved optimism within the distribution network, and the valuation and company expectations were low. Our patience paid off during the quarter as the stock gained due largely to broader market share improvements by beer relative to seltzer as well as a boycott of key rival Bud Light, which benefitted Molson Coors’ Coors Light and Miller Lite brands. We trimmed some of our exposure as the stock gained for risk management purposes but maintained a sizeable position.

OUTLOOK

Many of our more cyclical industrial and consumer companies are increasingly cautious regarding the strength of their businesses in an economic slowdown. While the market is forward-looking, it would be historically unusual for stocks to rally straight through even a mild recession that will likely result in earnings disappointments. Nonetheless, by sticking to our fundamentally driven, bottom-up approach, we are comfortable with our risk/reward approach and remain focused on investments we believe can do well regardless of the macro outlook.

Should volatility materialize, however, we’re poised to explore opportunities within our growing investable universe. Especially as we believe the strength of our investment strategy lies in the bottom-up analysis of companies and long-term business fundamentals. As always, we seek to invest in high-quality companies at valuations that offer us an asymmetric risk/reward opportunity, and we believe that we can prudently exploit current market conditions to make attractive long-term investments.

Thank you for your continued partnership with ArrowMark.

{kind=link}

| The Fund’s performance data represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance data shown. The investment return and principal value of an investment will fluctuate so that you may have a gain or loss upon sale. You can obtain performance data current to the most recent month-end at Meridian Funds . 1 Listed holdings are presented to illustrate examples of the securities the Fund has bought and do not represent all of the Fund’s holdings or future investments. Information about the Fund’s holdings should not be considered investment advice. There is no guarantee that the Fund will continue to hold any one particular security or stay invested in any one particular sector. Holdings are subject to change at any time and are as of the date shown above. 2 The Fund’s Index, the Russell 2500™ Index, measures the performance of the small to mid-cap segment of the U.S. equity universe, commonly referred to as “smid” cap. The Russell 2500 is a subset of the Russell 3000® Index. It includes approximately 2500 of the smallest securities based on a combination of their market cap and current index membership. One cannot invest directly in an index. 3 The Fund’s second Index, the Russell 2500™ Value Index, measures the performance of the small to mid-cap value segment of the US equity universe. It includes those Russell 2500™ companies that are considered more value-oriented relative to the overall market as defined by Russell’s leading style methodology. One cannot invest directly into an index. 4 Performance is annualized. 5 Since inception returns are calculated using the month-end data prior to the Fund’s Legacy class inception date of 2/10/94. A Class: Prior to 7/1/15, the A Class was named Advisor Class. The historical performance shown for periods prior to inception on 11/15/13 was calculated using historical Legacy class performance as adjusted for estimated class-specific expenses, for distribution, shareholder servicing, and sub-transfer agency fees without consideration to any expense limitation or waivers. The annual gross expense ratio is 1.46% as of 12/30/22. The annual net expense ratio is 1.46% as of 12/30/22. If the class had been offered prior to 11/15/13, the actual performance and expenses may have differed from the amounts shown. Performance shown for class A shares with load includes the Fund’s maximum sales charge of 5.75%. C Class: The historical performance shown for periods prior to inception on 7/1/15 was calculated using historical Legacy class performance as adjusted for estimated class-specific expenses, for distribution, shareholder servicing and sub-transfer agency fees, without consideration to any expense limitation or waivers. The annual gross expense ratio is 1.12% as of 12/30/22. The annual net expense ratio is 2.19% as of 12/30/22. If the class had been offered prior to 7/1/15, the actual performance and expenses may have differed from the amounts shown. Investor Class: The historical performance shown for periods prior to inception on 11/15/13 was calculated using historical Legacy class performance as adjusted for estimated class-specific expenses for shareholder servicing and sub-transfer agency fees without consideration to any expense limitation or waivers. The annual gross expense ratio is 1.18% as of 12/30/22. The annual net expense ratio is 1.18% as of 12/30/22. If the class had been offered prior to 11/15/13, the actual performance and expenses may have differed from the amounts shown. Legacy Class: Legacy class shares of the Fund are no longer available for purchase by new investors, except under certain limited circumstances which are described in the Statement of Additional Information. The annual gross expense ratio is 1.12% as of 12/30/22. The annual net expense ratio is 1.12% as of 12/30/22. Investors should consider the investment objective and policies, risk considerations, charges and ongoing expenses of an investment carefully before investing. The prospectus contains this and other information relevant to an investment in the fund. Please read the prospectus carefully before you invest or send money. To obtain a prospectus, please contact your investment representative or access the website at Meridian Funds . Principal Investment Risks There are risks involved with any investment. The principal risks associated with an investment in the Fund, which could adversely affect its net asset value, yield, and return, are set forth below. Please see the section “Further Information About Principal Risks” in the Prospectus for a more detailed discussion of these risks and other factors you should carefully consider before deciding to invest in the Fund. An investment in the Fund may lose money and is not a deposit of a bank or insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. Investment Strategy Risk: The Investment Adviser uses the Fund’s principal investment strategies and other investment strategies to seek to achieve the Fund’s investment objective of long-term growth of capital. There is no assurance that the Investment Adviser’s investment strategies or securities selection method will achieve that investment objective. Equity Securities Risk: Equity securities fluctuate in price and value in response to many factors including historical and prospective earnings of the issuer and its financial condition, the value of its assets, general economic conditions, interest rates, investors’ perceptions, and market liquidity. Market Risk: The value of the Fund’s investments will fluctuate in response to the activities of individual companies and general stock market and economic conditions. As a result, the value of your investment in the Fund may be more or less than your purchase price. Growth Securities Risk: Because growth securities typically trade at a higher multiple of earnings than other types of securities, the market values of growth securities may be more sensitive to changes in current or expected earnings than the market values of other types of securities. In addition, growth securities, at times, may not perform as well as value securities or the stock market in general and may be out of favor with investors for varying periods of time. Small Company Risk: Generally, the smaller the capitalization of a company, the greater the risk associated with an investment in the company. The stock prices of small capitalization and newer companies tend to fluctuate more than those of larger capitalized and/or more established companies and generally have a smaller market for their shares than do large capitalization companies. Foreign Securities Risk: Investments in foreign securities may be subject to more risks than those associated with U.S. investments, including currency fluctuations, political and economic instability, and differences in accounting, auditing, and financial reporting standards. Foreign securities may be less liquid than domestic securities so that the Fund may, at times, be unable to sell foreign securities at desirable times or prices. In addition, emerging market securities involve greater risk and more volatility than those of companies in more developed markets. Significant levels of foreign taxes are also a risk related to foreign investments. Glossary : Beta :A statistical measure of the Fund’s volatility relative to the broader peer group is measured against the benchmark Index, which is deemed to equal 1.00. Free cash flow : A measure of a company’s financial performance, calculated as operating cash flow minus capital expenditures. Basis Point : A common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument. ALPS Distributors, Inc., a member FINRA, is the distributor of the Meridian Mutual Funds, advised by ArrowMark Colorado Holdings, LLC. ALPS, Meridian, and ArrowMark are unaffiliated. The statements and opinions expressed in this commentary are as of the date of the commentary. All information is historical and not indicative of future results and is subject to change. Not FDIC Insured, Not Bank Guaranteed, May Lose Value |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Meridian Contrarian Fund Q2 2023 Investment Commentary