MLNK - MeridianLink: AI Successful M&A Could Imply Undervaluation

2023-05-16 02:49:51 ET

Summary

- MeridianLink is a recognized SaaS company with extensive experience and positioning in the field of financial services, serving banks, private clients, and consumer reporting agencies.

- I would welcome new partnership agreements with artificial intelligence providers like Zest AI.

- I took into account that management will likely continue to explore improvements and development points in the cloud and make exhaustive implementation of data analysis, and intelligence for business.

MeridianLink ( MLNK ) recently noted strong demand for the cross-sell power and configurability of its multi-product platform, and expects EBITDA growth in 2023. Having a close look at the growth of the global digital identity solutions market and global data analytics in banking, I believe that future sales growth would imply a valuation close to $20.067 per share. I know that there are risks from new regulations, failed merger integration, and total amount of debt, however the stock appears undervalued.

MeridianLink

MeridianLink is a recognized company with extensive experience and positioning in the field of financial services, serving banks, private clients, consumer reporting agencies, loan or credit grantor entities, and similar clients for more than 20 years. These services are mainly based on software for the clients of the company.

MeridianLink grows through acquisitions and developing technologies that today allow it to offer control and management software for its clients that include a wide range of possibilities, from the identification of digital and high security standards, verification of information, and consumer reporting for fraud prevention to marketing automation functions, emphasizing data analysis and intelligence for business.

The service is offered as a SaaS, where consumers pay subscription fees for the use of the solutions, generally long-term contracts that start at a minimum of three years for the contracting of the service. These fees are charged as monthly subscriptions, paid for specific features, or fees that translate into profit for the business at the time a customer completes a loan or assignment. In this sense, the profits for the company come from different types of payment for subscriptions for associated professional services, such as installation, training, and consultancy in the use of software, as well as commercial marketing agreements with third parties. The company's operations are grouped into a single business segment.

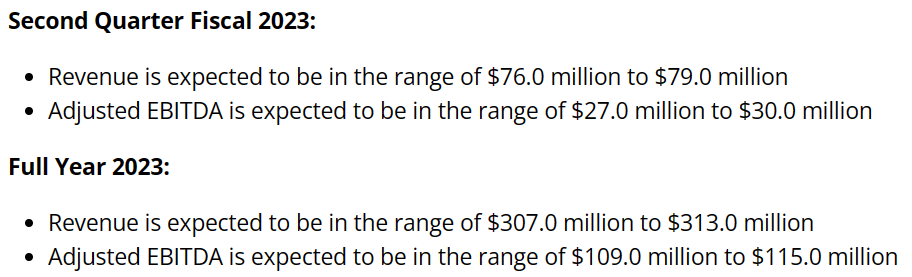

I believe that taking into account the words from management in Q1 2023 report, having a close look at the company makes sense. Management noted strong demand for the cross-sell power and configurability of the multi-product platform, MeridianLink One, to create seamless digital lending experiences. Besides, the company noted 2023 Adjusted EBITDA of $109-$115 million and sales close to $307-$313 million, which are better figures than that in 2022.

Source: Quarterly Press Release

{kind=link}

Market Expectations Include A Rebound In The Net Income In 2025

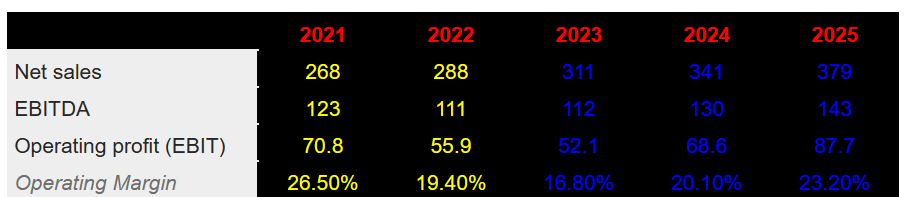

Considering the expectations delivered by market analysts , I believe that readers may have a look at their work. In my view, market expectations are optimistic. Financial forecasters expect 2025 net sales of close to $379 million, with sales growth in 2024 and 2025 as well as operating margin growth.

{kind=link}

2023 EBT and 2023 net income would be negative, however in 2024, financial forecasters expect positive figures with a net income of close to $10.6 million. I believe that stock demand would most likely increase in 2024 as more investors receive beneficial figures.

{kind=link}

Balance Sheet: Recent M&A Acquisitions And Restructuring Plan Announced

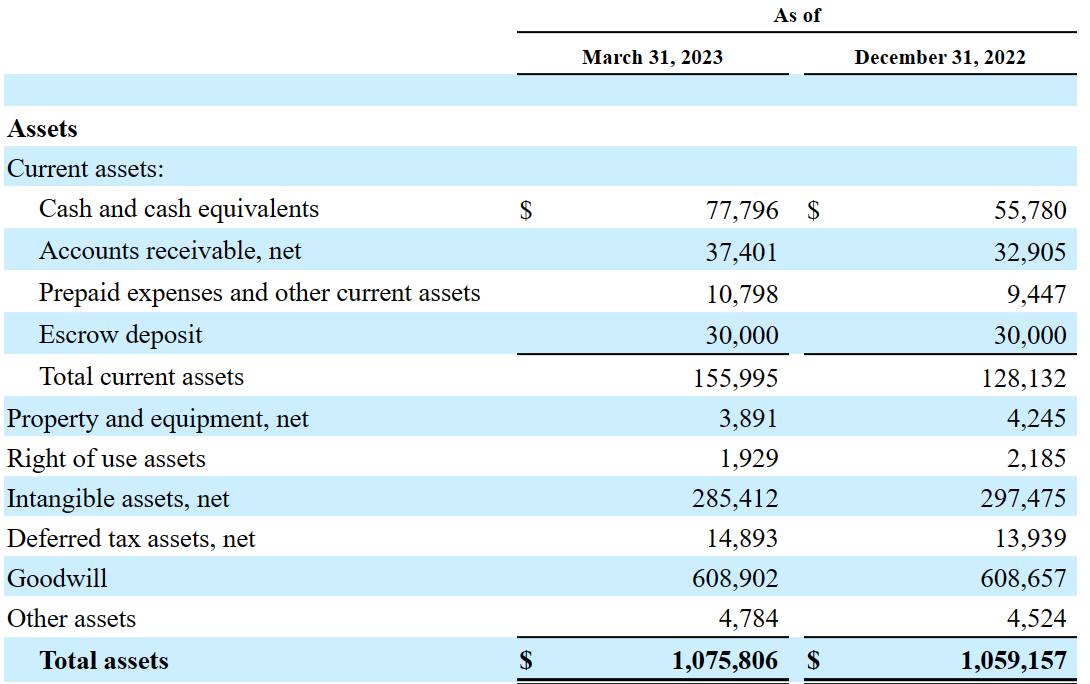

As of March 31, 2023, management reported cash worth $77 million, accounts receivable of about $37 million, prepaid expenses and other current assets of close to $10 million, and total current assets of close to $155 million. Total current assets are equal to approximately two times total current liabilities, so I do not see a liquidity risk here.

Non-current liabilities include property and equipment worth $3 million, right of use assets of $1 million, intangible assets close to $285 million, goodwill of around $608 million, and total assets of $1075 million . As of March 31, 2023, the company reported an asset/liability ratio close to 2x, so most investors would accept that the balance sheet stands in a good position.

{kind=link}

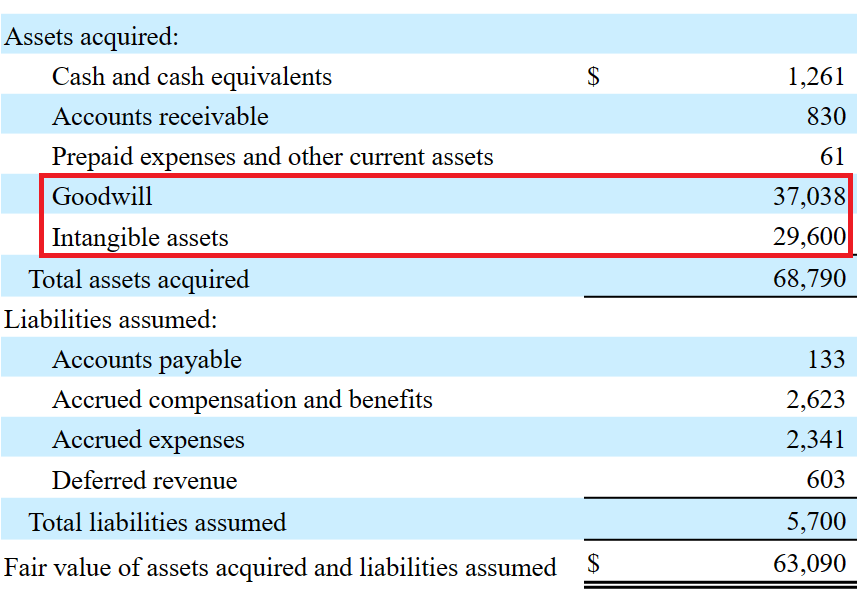

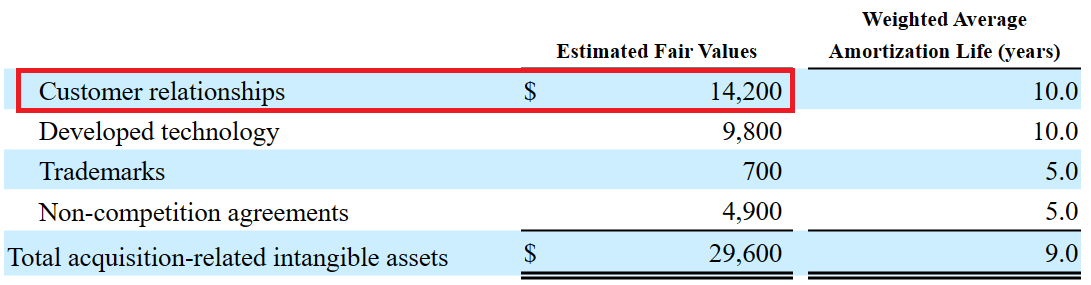

Considering the total amount of goodwill, I believe that studying the previous acquisitions signed by management appears relevant. The most recent acquisition is that of Beanstalk Networks L.L.C, which was paid with the available cash in hand. Beanstalk provided mortgage lending technology, and its balance sheet included a significant amount of intangible assets. I think that MeridianLink was mainly interested in the customer relationships, which were worth close to $14 million, a bit more than the value reported for the developed technology.

{kind=link}

{kind=link}

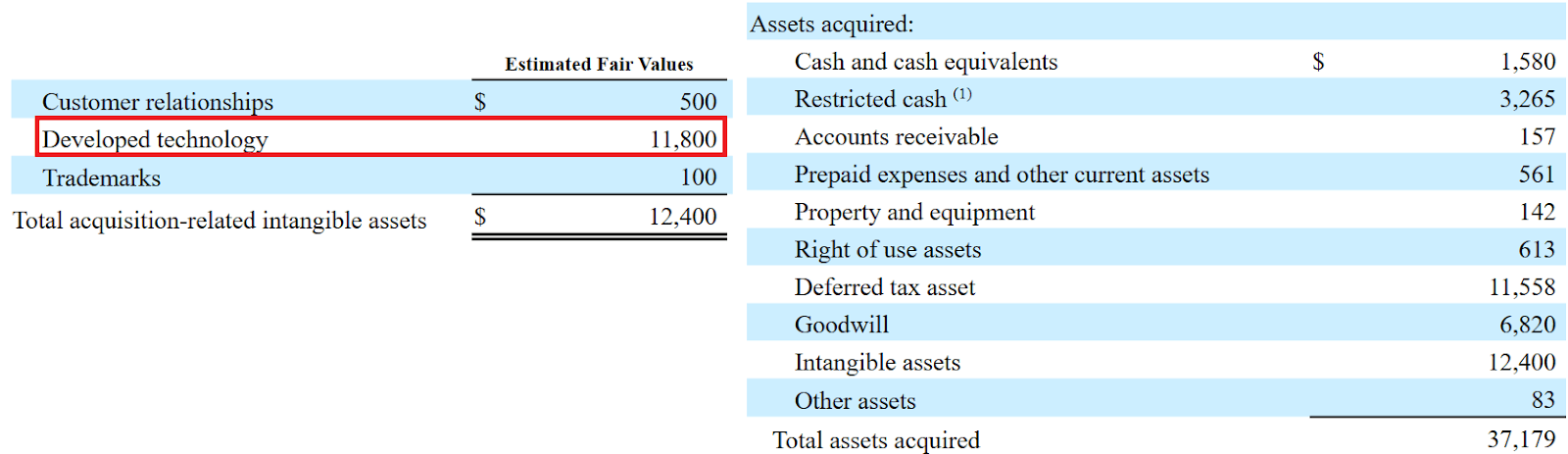

MeridianLink also seems to acquire technology from smaller companies. On April 1, 2022, the company acquired StreetShares, Inc., which included total assets worth $37 million and developed technology of $11.8 million.

{kind=link}

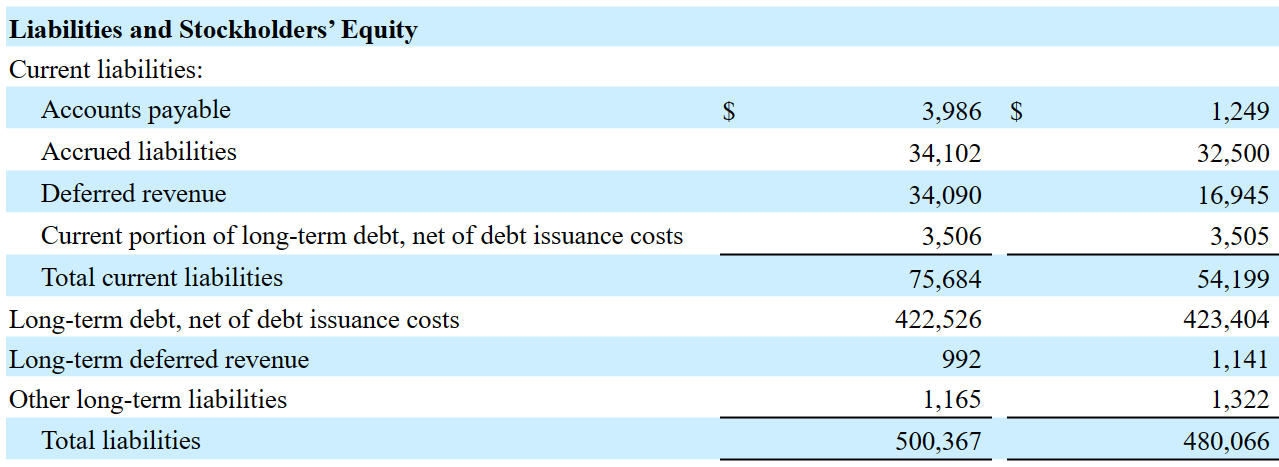

The list of liabilities reported in the last quarter included accounts payable of $3 million, accrued liabilities close to $34 million, deferred revenue of $34 million, and current portion of long-term debt of $3 million. Besides, long-term debt stands at $422 million with total liabilities worth $500 million.

{kind=link}

Taking into account the acquisitions expected in the past and the expertise in the M&A markets, we could expect significant inorganic growth in the coming years. However, I would not expect a lot of M&A activity in 2023 because the company recently noted a new restructuring plan. In 2023, MeridianLink plans to prioritize customer-centric areas of the company as well as to improve efficiencies.

In February 2023, the Company's board of directors authorized a restructuring plan that is designed to consolidate the Company's functions and investments to prioritize customer-centric areas of the Company's organization, align teams with the Company's highest business priorities, and improve efficiencies. The Restructuring Plan includes a reduction of the Company's current workforce by approximately 9%. Source: 10-k

Further Development Of New Products, Points In the Cloud, Digital Identity Solutions, And Geographic Expansion Would Lead To Valuation Of $20.067 Per Share

Under my financial model, I assumed new geographic expansion and positioning in the market through new clients. I also assumed that the company has sufficient cash in hand to reach and develop new products to expand its offer as well as to expand its marketplace monetization for partners. In particular, I would welcome new partnership agreements with artificial intelligence providers like Zest AI. As a result, new products and new markets will likely lead to FCF generation in the coming years.

MeridianLink, Inc., a leading provider of modern software platforms for financial institutions, together with Zest AI, a leader in automating underwriting with more accurate and inclusive lending insights, today announced the expansion of their partnership, increasing momentum as the integration enables more shared customers with access to AI-enabled underwriting. Source: MeridianLink and Zest AI Expand Partnership

I also took into account that management will likely continue to explore improvements and development points in the cloud, and make exhaustive implementation of data analysis, intelligence for business, and digital identity solutions. Considering the growth expectations of these markets, I believe that we could expect substantial net income growth.

The global data analytics in banking market was valued at $4.93 billion in 2021, and is projected to reach $28.11 billion by 2031, growing at a CAGR of 19.4% from 2022 to 2031. Source: Data Analytics in Banking Market Size, Share and Analysis

The global digital identity solutions market size is projected to grow at a CAGR of 20.4% to reach $70.7 billion in the upcoming five years. Source: Digital Identity Solutions Market Size, Share, Trends, Growth Drivers, Opportunities & Statistics

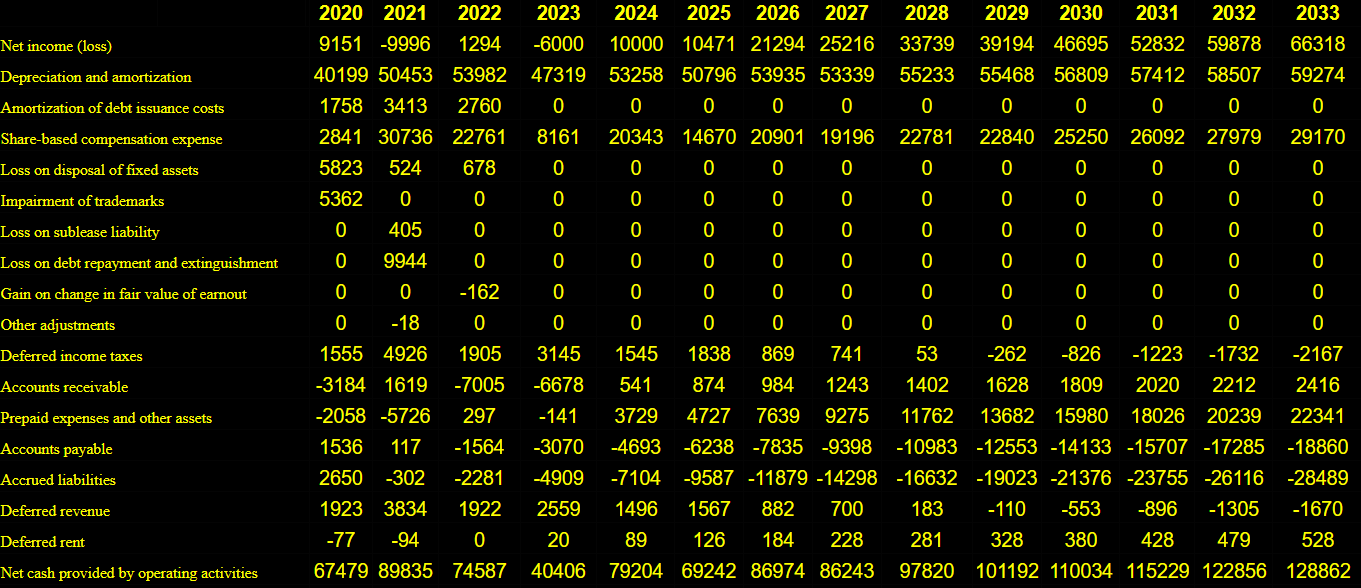

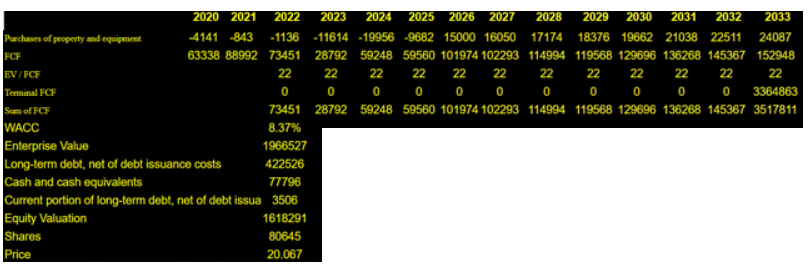

My numbers in my cash flow model included 2029 net income worth $66 million, with depreciation and amortization close to $59 million, changes in accounts receivable of $2 million, prepaid expenses and other assets close to $22 million, accounts payable of -$19 million, and accrued liabilities around -$29 million.

Also, with changes due to deferred revenue of -$2 million, the net cash provided by operating activities would be close to $128 million. Besides, if we assume 2023 purchases of property and equipment close to $24 million, 2033 FCF would be close to $152 million.

Source: My Financial Forecasts

{kind=link}

Now, if we assume an EV/FCF multiple of 22x, 2033 terminal FCF would be close to $3.364 billion. If we also assume a WACC of 8.37%, the implied enterprise value would be close to $1.966 billion. Also, with long-term debt of $422 million, cash and cash equivalents close to $77 million, and current portion of long-term debt, net of debt issuance costs of $3 million, the equity valuation would be $1618 million, and the implied price would be $20.067 per share.

Source: My Financial Forecasts

{kind=link}

Competition And Risks

In Meridian's development and operations area, competition is high and is given by companies with similar approaches and service formats as well as hybrid models, in offering core solutions for managing the entire business as well as particular functions within these services. Some of the companies that compete with MeridianLink are Fiserv ( FISV ), Jack Henry ( JKHY ), Temenos ( OTCPK:TMNSF ), nCino ( NCNO ), Q2 ( QTWO ), OpenClose, and CRIF.

Meridian needs to develop products that allow it to expand its current customer base and reach new customers, especially internationally. I believe that lower sales growth in the coming future because of a decrease in the customer count will likely lead to lower stock prices.

Regarding the relationship with its customers, the inability to integrate its products and solutions with those of the users is also a relevant risk factor. I would also add that the success of the company needs to be accompanied by the fulfillment of a trend regarding the adoption of tech products mainly by clients in the financial field. At this point, it is good to say that the company is totally dependent on the development of these markets, thus possible disruptions or drastic changes in this market can generate complications for the company.

Successful integration of targets into the operating model of MeridianLink can be a risk factor for the company. Shareholders will most likely suffer goodwill impairment if the recent acquisitions are not properly integrated. As a result, management may report book value per share, which may lead to lower stock price.

Finally, we can name new regulations as a risk factor, mainly regarding the use of data from customers. If the company carries out its expansion internationally, it has to take into account this factor in other regions, mainly in Europe.

Conclusion

MeridianLink delivers products in growing target markets, and benefits from sales growth in the global digital identity solutions market and global data analytics in banking. Geographic expansion from 2024 and 2025 along with successful integration of new acquisitions will likely lead to significant FCF growth and EBITDA growth. Even considering risks from new regulations, total amount of debt, or M&A integration, in my opinion, MeridianLink could be worth more than what the market currently discloses.

For further details see:

MeridianLink: AI, Successful M&A Could Imply Undervaluation