SGA - Merion Road Capital Q4 2023 Investor Letter

2024-01-20 04:30:00 ET

Summary

- Merion Road Capital Management LLC is a registered investment adviser. We focus on value-oriented investing through rigorous fundamental analysis of a company's operations.

- The long only portfolio increased 9.8% in Q4 2023, bringing our full year results to 38.7%.

- The Small Cap Fund increased 11.2% in Q4 and 11.5% for the entire year.

| Merion Road Small Cap Fund |

| IWM (Russell 2000) |

| Barclay Hedge Fund Index |

| Annualized Since Inception |

| 16.6% |

| 9.0% |

| 5.5% |

| Q4 2024 |

| 11.2% |

| 13.6% |

| 5.0% |

| 2023 YTD |

| 11.5% |

| 16.4% |

| 9.3% |

| 2022 |

| (16.9%) |

| (20.4%) |

| (8.5%) |

| 2021 |

| 42.5% |

| 14.5% |

| 10.0% |

| 2020 |

| 29.5% |

| 20.0% |

| 11.0% |

| 2019 |

| 17.9% |

| 25.4% |

| 10.6% |

| 2018 |

| 15.7% |

| (11.1%) |

| (5.2%) |

| 2017 |

| 35.7% |

| 14.6% |

| 10.3% |

| 2016 (Jul-Dec) |

| 1.3% |

| 18.7% |

| 5.4% |

| MRCM Long Only Large Cap |

| SPY (S&P 500) |

| Annualized Since Inception |

| 11.9% |

| 11.6% |

| Q4 2024 |

| 9.8% |

| 11.2% |

| 2023 YTD |

| 38.7% |

| 25.7% |

| 2022 |

| (34.9%) |

| (18.2%) |

| 2021 |

| 20.4% |

| 28.7% |

| 2020 |

| 54.3% |

| 18.3% |

| 2019 |

| 25.2% |

| 31.2% |

| 2018 |

| (6.0%) |

| (4.6%) |

| Dec 18 - Dec 31 |

| 0.1% |

| (0.5%) |

| Note: All returns are net of management and performance fees. Past performance is not indicative of future results. Returns for the Merion Road Small Cap Fund for the period prior to fund launch (01/13/22) reflect a basket of SMAs. |

The long only portfolio increased 9.8% in Q4 2023, bringing our full year results to 38.7%.

In my previous year-end letter, I reviewed our three largest positions (Ferguson, Alphabet, Copart) and the rationale for holding them despite their recent underperformance. These positions accounted for our largest dollar contribution this year, increasing 52%, 59%, and 61% respectively. Of course macro factors helped with inflation slowing, a resilient economy, and a shift in the rate outlook from hikes to cuts. Nonetheless, these companies demonstrated strong fundamentals that reflect their attractive business quality and market positioning. While we are not out of the woods yet, the recent volatility is yet another reminder of the importance of having a long investment horizon.

During the quarter I meaningfully increased our position in Summit Materials ( SUM ) which I just discussed in my Q3 letter. In October the company released the preliminary proxy statement for their pending acquisition of the U.S. operations of Cementos Argos ( CMTOY ). This document contained two positive factors. Most notably, in the background section of the merger the company announced that it had received a proposal from a third party to acquire SUM at a price of $38/share. The board concluded that this offer was not a superior proposal to the value creation from their own acquisition of Argos. While an acquisition of SUM is off the table at this point, it highlights the strategic value of SUM assets. Secondly, management’s internal projections for SUM on a standalone basis and pro forma for the acquisition were quite strong (combined EBITDA is projected to grow at an 11% CAGR over the next 3 years inclusive of synergies). Near-term I believe SUM is worth $45 (+25% from current levels) with longer-term upside as infrastructure plans hit the market.

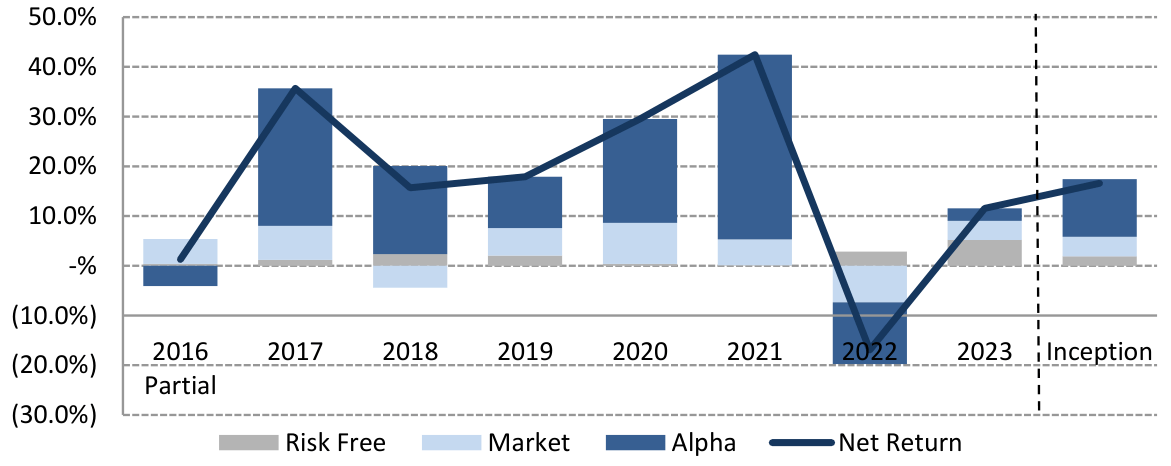

The Small Cap Fund increased 11.2% in Q4 and 11.5% for the entire year. From an attribution perspective, +5.2% came from the risk-free rate, +3.9% from our market exposure, and +2.5% from alpha.

Like the broader small-capitalization market, most ('all') of our returns came in December. Unlike the index, however, this was driven by a few catalysts that positively impacted our portfolio. Entering December our second largest position was in an oil and gas company, Unit Corp ( UNTC ). UNTC declared a special and common dividend equal to 40% of its then market capitalization. The stock traded well following this news as it accelerated the return on our investment and reaffirmed management’s alignment with shareholders. Though I normally shy away from commodity businesses, I felt comfortable with this name given its strong balance sheet, valuation disparity, and dedication to returning capital. Furthermore, I hedged our exposure to energy prices by shorting another company in the sector. Similar to UNTC, our position in the small radio broadcaster, Saga Communications ( SGA ), benefitted from a special dividend equal to 10% of its then market capitalization.

I initiated a new position in Duckhorn Portfolio ( NAPA ) in December. NAPA is a top 3 players in the U.S. luxury wine category (as defined by bottles costing >$15), with the majority of sales coming from its Duckhorn brand and the more affordably priced Decoy label. Like their spirit and beer brethren, NAPA benefits from stable demand, established distribution, and brand equity. Unlike other alcohol categories, the wine industry is highly fragmented as small players with romantic ideations of owning their own vineyard abound. While this dynamic creates a fertile hunting ground for acquisitions, it also creates a greater level of competition that makes the business less reliable than say Jack Daniels.

It’s been tough sledding for NAPA’s stock as it has fallen ~60% over the past few years; this is a result of multiple contraction as earnings have grown. NAPA is an odd-duck (see what I did there) as the only “real” publicly traded wine company – the others are all a fraction of the size and unprofitable. This lack of comparability likely means that it receives less attention than it deserves. Additionally, investors are concerned with macro uncertainty (slow-down in the wine category, distributor destocking) and idiosyncratic issues with the company. Notably, their well-regarded CEO abruptly retired in the middle of last year. Just a few months later, and while operating with an interim CEO, NAPA announced its largest acquisition to date. Add in the fact that the majority of consideration is in the form of equity and there are reasons for investors to be worried. With the stock falling to <8x EBITDA, valuation seems compelling enough to step in.

The pending acquisition is for Sonoma-Cutrer, the Chardonay portfolio currently owned by Brown-Forman ( BF.B ). Sonoma-Cutrer is a great fit for NAPA as it fills out a portion of their portfolio that was previously underserved, maintains extremely strong brands, aligns with their luxury footprint, and provides significant production resources. My understanding is that Brown-Forman wanted to focus on running their core spirits business but also maintain financial exposure to the luxury wine segment. As such, almost 90% of the purchase price is in the form of stock and Brown-Forman will receive 2 board seats at NAPA. I read this as a positive. Perhaps the best run spirits company is taking a large financial and governing position in what is relatively a small company (NAPA boasts a market cap of $1bn compared to Brown-Forman’s $27bn). While it is unfortunate that the company does not have a full-time CEO, they benefit from a proven interim operator in Dierdre Mahlan who formerly ran Diageo North America. Given the stability of the business, NAPA has time to choose the right individual for the long-term.

Ultimately, the stock should re-rate higher as earnings reaccelerate, they name a new CEO, and they close/integrate Sonoma-Cutrer. Pro forma for the acquisition, NAPA is trading at about 8x EBITDA and 12x free cashflow. This is a significant discount to spirit and beer peers that boast double digit EBITDA multiples and high-teen free cash flow multiples.

Over the past 7.5 years the small-cap fund has gained 16.6% per year. +1.9% has come from the risk-free rate and +3.9% from the market (the Russell is up 9.0% during this period but our portfolio has had a beta of 0.43). The remaining +11.6% of returns have come from good stock picking.

Performance Attribution

{kind=link}

I wish everyone a healthy, happy, and prosperous 2024.

Sincerely,

Aaron Sallen

| General Disclaimer This material does not constitute an offer or the solicitation of an offer to purchase an interest in Merion Road Small Cap Fund, LP (the “ Fund ”), which such offer will only be made via a confidential private placement memorandum (the “ Memorandum ”). An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. All statements herein are qualified in their entirety by reference to the Memorandum, and to the extent that this document contradicts the Memorandum, the Memorandum shall govern in all respects. This material is confidential and may not be distributed or reproduced in whole or in part without the express written consent of Merion Road Capital Management, LLC (the “ Investment Manager ”). The information and opinions contained in this document are for background purposes only and do not purport to be full or complete. Unless otherwise stated, the information in this document is not personalized investment advice or an investment recommendation on the part of the Investment Manager. The performance data discussed herein do not represent the performance of the Fund, but rather, represent the unaudited performance of a basket of separately managed accounts managed by the Investment Manager pursuant to the same strategy expected to be implemented for the Fund. Results generated in the Fund once outside capital is admitted could be materially different than those results shown. The results shown reflect the deduction of: (i) an annual asset management fee of 1.5%, charged quarterly; (ii) a performance allocation of 15%, taken annually, subject to a “high water mark;” and (iii) transaction fees and other expenses actually incurred. The management fee and performance allocation were applied retroactively and do not reflect actual fees charged. None of the results shown reflect the deduction of certain organizational and operating expenses common to investment funds, which would serve to decrease profits or otherwise increase losses. Results were achieved using the investment strategies described in the Memorandum. Results are compared to the performance of the Russell 2000 Index, the Russell Micro-cap Index, and the Barclay HF Index (collectively, the “ Comparative Indexes ”) for informational purposes only. The Fund’s investment program does not mirror any of the Comparative Indexes and the volatility of the Fund’s investment program may be materially different from the volatility of the Comparative Indexes. The securities included in the Comparative Indexes are not necessarily included in the Fund’s investment program and criteria for inclusion in the Comparative Indexes are different than criteria for investment by the Fund. The performance of the Comparative Indexes reflects the reinvestment of dividends, as appropriate. This material contains certain forward-looking statements and projections regarding market trends, investment strategy, and the future asset allocation of the Fund, including indicative guidelines regarding position limits, exposures, position sizing, diversification, and other indications regarding the Fund’s strategy. These projections and guidelines are included for illustrative purposes only, are inherently predictive, speculative, and involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. The guidelines included herein do not reflect strict rules or limitations on the Fund’s investment program and the Fund may deviate from the guidelines described herein. There are a number of factors that could cause actual events and developments to differ materially from those expressed or implied by these forward-looking statements, projections, and guidelines, and no assurances can be given that the forward-looking statements in this document will be realized or followed, as described. These forward-looking statements will not necessarily be updated in the future. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Merion Road Capital Q4 2023 Investor Letter