MTH - Meritage Homes: Initiate Buy On Healthy Demand And Improved Productivity

2023-11-27 04:50:32 ET

Summary

- I have a positive outlook for Meritage Homes Corporation, with a target price of $207.

- MTH has shown strong financial performance and has improved its balance sheet.

- Demand should remain steady if MTH can continue to provide financial incentives.

Investment Overview

With a positive view on Meritage Homes Corporation's ( MTH ) ability to continue providing financial incentives to capture demand and improve productivity (cycle time) to drive operating leverage, I expect the stock to trade at 8x forward earnings, a modest increase from the current 7.5x, which gives me a target price of $207.

Business Description

MTH sells single-family houses to home buyers in the US, with a presence in 10 states, mainly in the eastern, central, and western regions. MTH has been in this line of business for more than 3 decades and has delivered more than 150k homes through the years. MTH's financial performance over the years has been outstanding as well. Since 2011, the business has grown from a revenue size of $861 million to ~$6.5 billion over the last twelve months [LTM], almost 6x in size. Growth was not achieved at the expense of cash burn; the business has been profitable over the past decade, expanding margins to 17% in the LTM and delivering ~$1 billion in EBITDA. A very positive aspect of MTH is that it has gone from a net debt position to almost a net cash position throughout the years. As of LTM, MTH has a cash position of $1.048 billion and $1.057 billion in debt.

Demand Ahead Remains Healthy

{kind=link}

{kind=link}

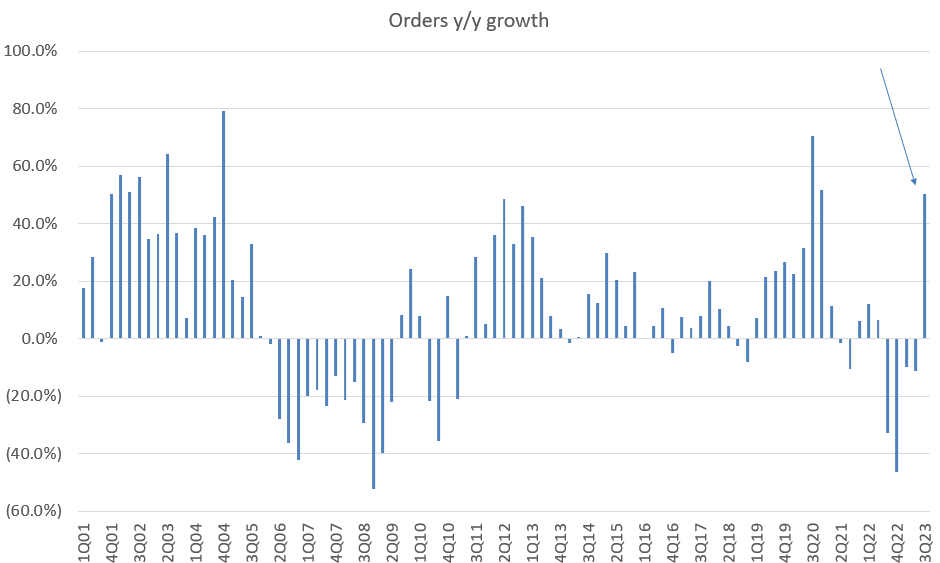

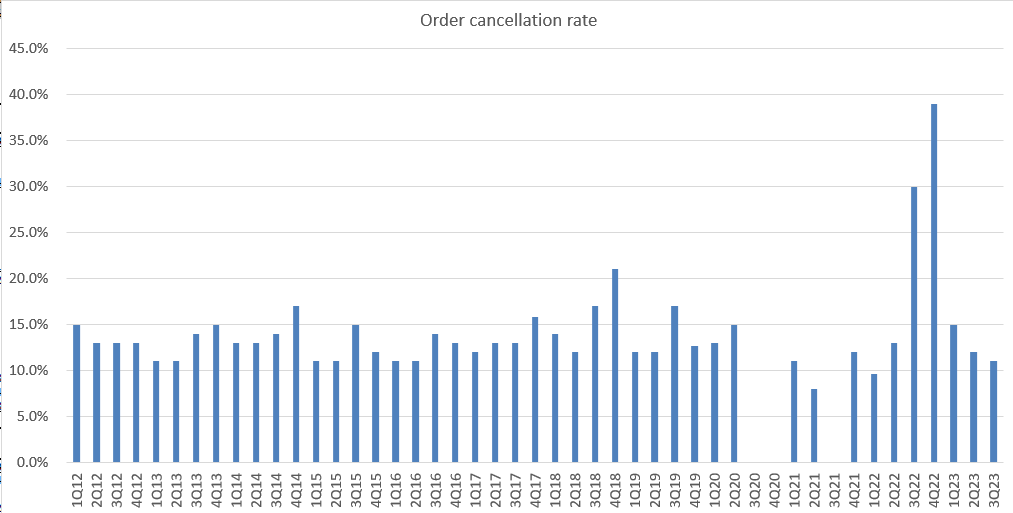

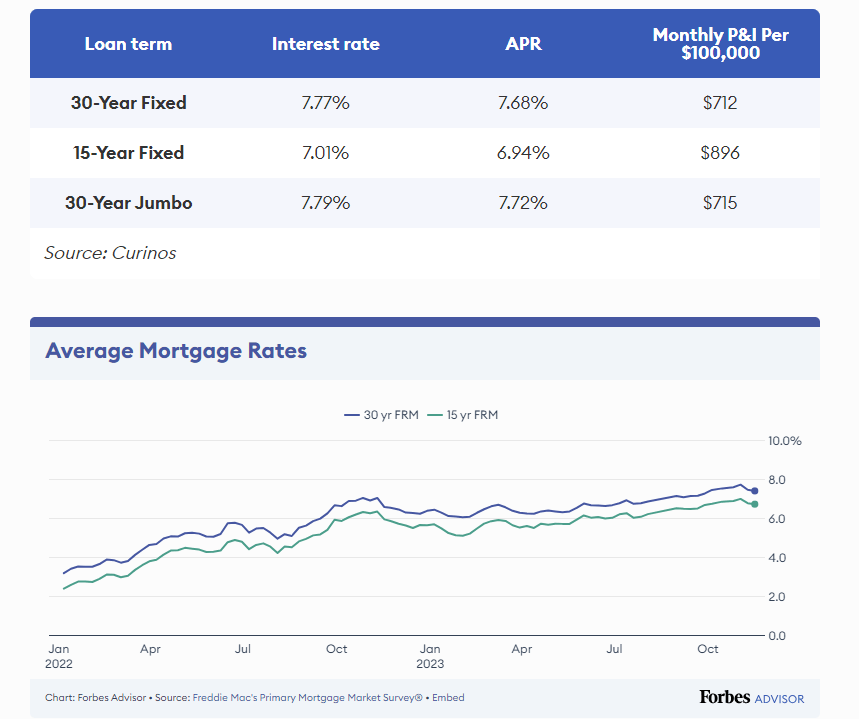

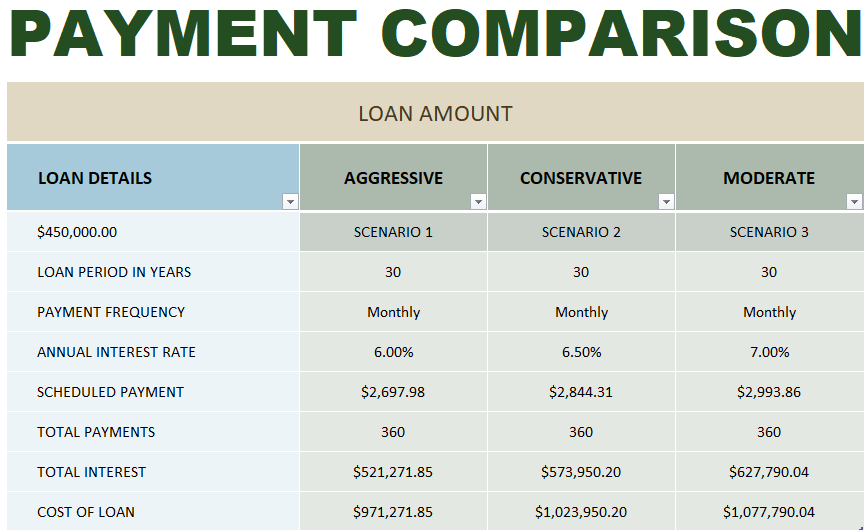

MTH's recent 3Q23 order performance was excellent, as the order increase of 50.4% was driven by absorption. The notable data I took away was the stabilization in cancellation rate (11% for 3Q23), which remains well below last year's 30% cancellation rate and the historical average of 14% over the past 10 years. I believe these show that MTH is somewhat benefiting from the current rate environment, where the current resale market is supply-constrained (as homeowners do not want to sell their house because of the low mortgage rates they are enjoying). The availability of MTH's homes that can be readily moved into is a great value proposition for urgent homeseekers. More importantly, MTH's homes are much more affordable, especially after financing incentives. For comparison, as of 3Q23, the average mortgage rate for MTH's homes was 6%, ~100 bps below the current average mortgage rate in the US. While 100 bps might not sound like a lot at face value, it is huge when compounded over 25 to 30 years at a principal value of $450k. Based on an Excel calculation, the difference between 7% interest and 6% interest overtime amounts to $100k, ~25% of the principal value.

{kind=link}

{kind=link}

In my opinion, so long as MTH can continue to provide incentives to make their homes more affordable, it should continue to see steady growth in the current rate environment. The reason for my emphasis on affordability is that 88% of MTH 3Q23 orders are for entry-level homes. Given that MTH's balance sheet strength has significantly improved over the years, reaching a close to net cash position, I believe they are in a better financial position to provide incentives. Using consensus estimates, MTH is expected to generate close to $500 million in FCF in FY24. That would elevate the business to a net cash position, giving it more financial stability to provide incentives.

As such, for the near-term growth outlook, I believe it will continue from the 3Q23 momentum.

Margin Soft In The Near Term But Should Expand Over Time

There are two moving parts here: gross margin and operating expenses/leverage.

For gross margin, management implied 4Q23 guidance (based on FY23 guidance) suggests that MTH will see a decline of around 70 to 170 bps to 25-26% when compared to 3Q23. This is in line with my expectations that management will continue to utilize financial incentives to grow topline and capture demand in the current macro environment.

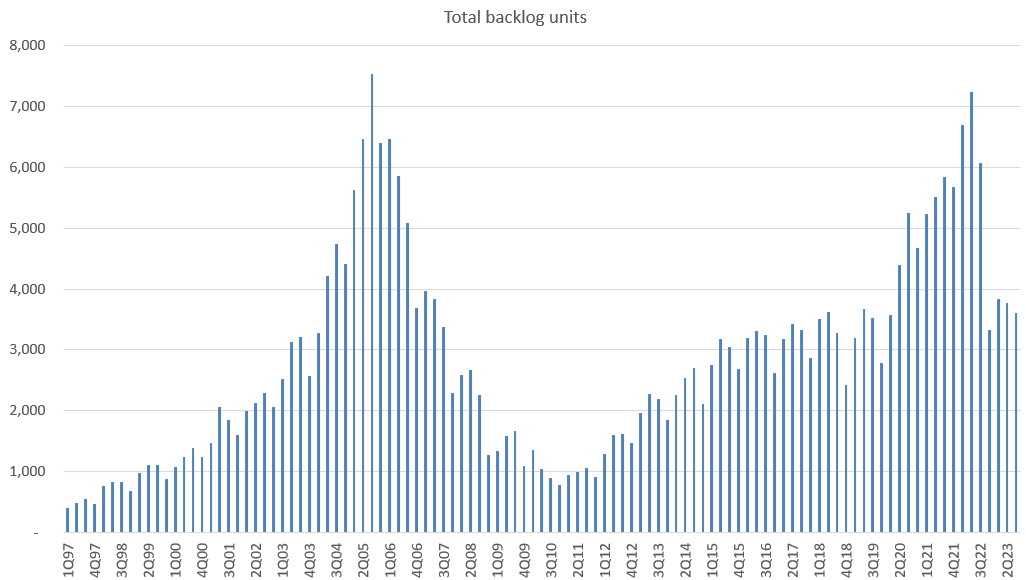

However, down the income statement, I also expect MTH to see operating leverage as it grows its topline, which should have a positive impact on the EBIT line. Several data points from the latest quarterly performance support my view. For instance, cycle times fell 15 days in the quarter to 140, and they are down by more than 50 days from a year-to-date perspective. While this is a few weeks above pre-pandemic norms given persistent challenges at the front end of the build process, I believe focus should be on the fact that it is normalizing. This is an important development, as with a normalized cycle time, MTH will be able to deliver homes faster, which also means inventories will leave the balance sheet faster, converting into cash that can be used for further financial incentives. More importantly, this will enable MTH to clear its backlog at a faster pace (driving topline growth and operating leverage). Looking back at MTH's historical data (back to 1997), MTH's current backlog still stands at a slightly elevated level in recent history (ignoring the COVID period).

{kind=link}

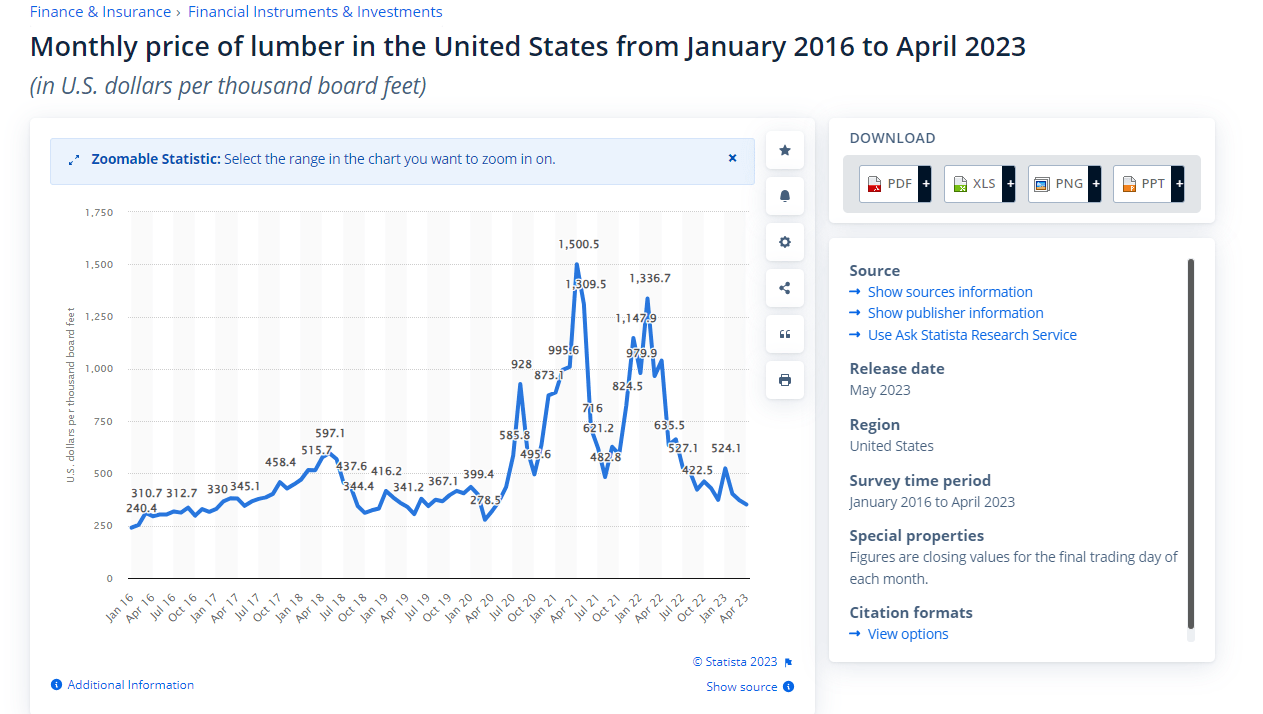

Another implication of a faster cycle time is that MTH can deplete the existing stock of material costs (i.e., lumber) that were previously purchased at a higher price. The depletion allows MTH to purchase new materials at prevailing rates that are cheaper, which should help lift gross margins. Adding on the fact that wages have been steady for MTH, I'd expect margins to expand over the medium term, which will continue to improve productivity and grow topline.

{kind=link}

Valuation

May Investing Ideas

I modelled MTH to see negative growth in FY23, which is in accordance with management's guidance, as FY22 was an outlier year that benefited from the post-covid situation. I expect growth to revert to a more normalized demand level of 7%, slightly above the industry growth level, as I expect MTH to capture share due to its ability to continuously provide financial incentives. As per my margin expectations above, I expect my margin to expand over time. I modelled MTH earnings margin to improve by 100 basis points over the next 2 years, gradually approaching pre-covid levels. Lastly, I modelled MTH to trade nearer to its historical average of 8.7x forward P/E. The reason for using 8x instead of 8.7x is because there is still a macro headwind in place (rates are still high).

Risk

The inherent risk with MTH is that it is still very much driven by the mortgage rate cycle. The higher the rates, the worse the business climate. MTH could continue to provide attractive financial incentives to grow, but there is a limit to how much its balance sheet can withstand. If rates were to continue to see a steep increase, my worry is that overall demand for housing would collapse further.

Conclusion

To conclude, I am recommending a buy rating for MTH as I am positive about demand remaining steady, MTH's improved productivity, and its improved balance sheet to continue providing financial incentives. Specifically, I believe MTH's focus on affordability and faster cycle times bodes well for sustained growth and margin expansion. However, the risk persists due to sensitivity to mortgage rate fluctuations.

For further details see:

Meritage Homes: Initiate Buy On Healthy Demand And Improved Productivity