MTH - Meritage Homes: Rating Upgrade As Growth Expected To Accelerate

2023-09-05 05:44:47 ET

Summary

- I upgraded my rating on MTH from hold to buy, as I expect growth to accelerate in the near-term.

- MTH's 2Q23 earnings exceeded consensus estimates with an EPS of $5.02, driven by impressive revenue and EBIT margin in the homebuilding sector.

- Positive indicators include a substantial backlog, reduced build cycle times, and the ability to raise prices, all of which suggest improved revenue conversion and profit margins in the future.

Summary

Following my coverage on Meritage Homes Corporation ( MTH ), I recommended a hold rating due to my expectation that investors might lock in some profits by selling the stock (after the 100% rally previously) as the risk/reward ratio was less attractive. This post is to provide an update on my thoughts on the business and stock. With my revised outlook on the business, I am upgrading my rating from a hold to a buy as I see a visible path to growth accelerating in the near term, which should drive valuation upwards, back to its historical discount vs. its peer group.

Investment thesis

For a start, I believe my decision for a hold rating was right as the stock went into profit-taking mode (share price down by 11.5% since my post in May). However, I was wrong not to follow up closely as the stock went into another round of rally from $114 to the peak of $152 in late July (pre-earnings).

I have summarized my findings since my last report, and they all bode well for the foreseeable future, as you will see below. MTH's EPS of $5.02 for 2Q23 far surpassed the consensus estimate of $3.45. The superior results were driven by homebuilding's impressive revenue and EBIT margin. First of all, MTH's 2Q earnings demonstrate the company's ability to execute by capitalizing on the better-than-expected demand environment (in light of rising rates). In addition, the current supply and demand dynamics enabled a lowering of incentives and a few price hikes (more on this below) during the quarter, which boosted earnings. I expect this growth trend to continue in the near future as management increases land spending to fuel expansion; they are aiming for a sales rate of 3–4 per month with a conversion rate of over 80%. Naturally, this goal was questioned during the earnings call as the sales pace per month dropped to 3.9 from 4.4 in 2Q23, which was caused in part by a large number of communities closing in April and opening in June. However, I have faith that MTH can do this because the company's management has stated that online absorptions have been in line with expectations throughout the quarter, with July showing little sign of seasonality. Therefore, I anticipate a pick-up in pace as the business heads into the second half.

Secondly, other metrics also indicate positive growth ahead. For instance, as of the end of 2Q23, the company had a backlog of about 3,800 units and a spec count of 4,500. The time spent on building also decreased by about three weeks between the first quarter of this year and the end of June. I expect build time to further decrease back to the normalized 120–140 days from the current 160 days (it was more than 200 days at the peak due to COVID and supply chain situations). This reduction in cycle time should help translate backlog into revenue at a faster rate.

Thirdly, it became evident that when it comes to pricing, potential homebuyers are growing more at ease with the current interest rate situation, while the availability of homes for sale remains limited .

“Buyers are acclimating to the higher mortgage interest rates, and the favorable demographics of millennials and baby boomers looking for entry-level product, provide a large buyer pool for our homes.” 2Q23 earnings results call

Due to these two factors, MTH managed to raise prices and boost its profit margins. This was noticeable during the quarter as the ASP increased by 2% compared to the previous period, mainly due to MTH implementing modest price hikes and reducing incentives. Consequently, I anticipate further enhancements in gross margins in the near future. My confidence in this expectation is reinforced by management's guidance, as they indicated an expected margin improvement of 50-100 basis points sequentially through 4Q23.

Valuation

Own calculation

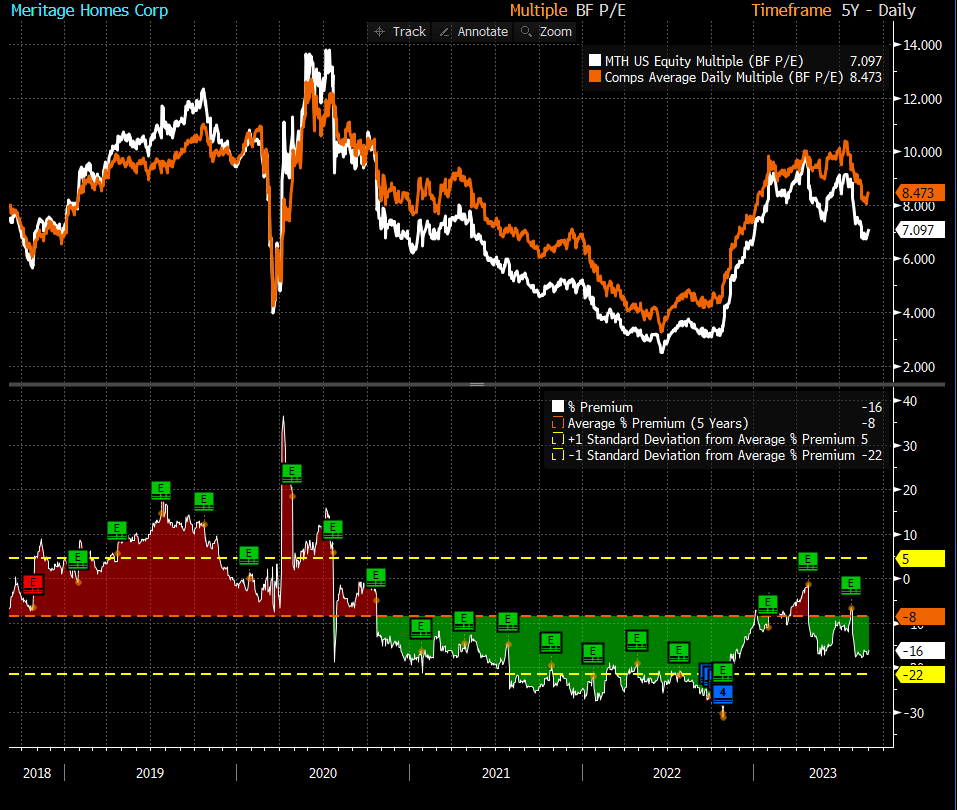

I believe the fair value for MTH based on my model is $176. My model assumptions are that growth will start to reaccelerate in the coming quarters as the demand environment remains strong, driving an increase in units in the backlog. With the decrease in build cycle times, the backlog should translate to revenue at a faster rate in the near term. Growth would likely slowdown from a percentage point of view in FY25 as it lags behind the stronger-performing FY24. Margins would gradually return to historical levels as the business continued to see gross margin expansion from increases in prices. Finally, I expect MTH to trade back to its historical discount vs. peers (8% discount) from the current 16% discount as it continues to show the market that it is growing healthily even in this current rate environment.

MTH peers include: Tri Pointe Homes ( TPH ), Beazer Homes USA ( BZH ), PulteGroup ( PHM ), Hovnanian Enterprises ( HOV ), M.D.C. Holdings ( MDC ), NVR ( NVR ), D.R. Horton ( DHI ), KB Home ( KBH ), Taylor Morrison Home Corp ( TMHC ), LGI Homes ( LGIH ), M/I Homes ( MHO ), Dream Finders Homes ( DFH ), Century Communities ( CCS ), Toll Brothers ( TOL ), Lennar Corp ( LEN ), and Landsea Homes Corp ( LSEA ). The median forward revenue multiple peers are trading at is 8.4x, the expected 1Y growth rate is flattish, and if we assume 8% discount to 8.4x, it is 7.7x

{kind=link}

Risk

While the current rate environment's impact on MTH businesses turned out better than expected, this is not to say that it will not get worse. Mortgage lending standards could get worse if rates continue to go up. When rates go up, it will definitely impact home buyers decisions, likely forcing them to delay purchases, which will indirectly force MTH to reduce home prices to drive sales.

Conclusion

I have upgraded my rating for MTH from hold to buy based on several positive developments. MTH's impressive 2Q23 earnings, with an EPS of $5.02 exceeding consensus estimates, demonstrates the company's effective execution and its ability to capitalize on strong demand, even amid rising interest rates. Management's plans for increased land spending to boost expansion and achieve higher sales rates are promising. Other positive indicators include a substantial backlog and reduced build cycle times, both of which suggest improved revenue conversion. Moreover, MTH's ability to raise prices and improve profit margins due to buyers' comfort with current interest rates and limited housing supply bodes well for future growth.

For further details see:

Meritage Homes: Rating Upgrade As Growth Expected To Accelerate