BZH - Meritage Homes: Still Appealing Despite Signs Of Further Weakness Ahead

2023-07-21 10:36:58 ET

Summary

- The homebuilding market is experiencing difficulties due to rising interest rates, but Meritage Homes Corporation has performed well despite these challenges, with shares looking attractively priced for long-term investors.

- Meritage Homes' revenue increased by 22.4% in 2022, driven by a 10.2% increase in homes sold and a 10.6% increase in average sales price; however, the number of homes ordered dropped by 14.8%.

- Despite short-term struggles, the ongoing housing shortage in the U.S. could serve as a long-term catalyst for higher home prices.

Pretty much any angle you look at it from, the home building market is in a state of severe pain. Initially, there was a boom in the space, with inflationary pressures enabling companies to pump up their margins by passing on significant price increases to their customers. But when interest rates started rising, it became a question of when, not if, the market would see a meaningful decline.

One of the companies in this space that has performed extremely well over the past year or so despite signs of weakness ahead is Meritage Homes Corporation (MTH), a fairly sizable player with a market capitalization of $5.4 billion. Moving forward, I do believe that fundamental performance for the company will continue to worsen for at least the next few quarters. But even if you factor this into the equation, shares of the company look attractively priced and, in the long run, I believe that upside exists for investors to benefit from.

Great performance, all things considered

The last article that I wrote about Meritage Homes was published in the middle of January of 2022. That's about a year and a half ago. In that article, I talked about how the company was continuing to grow its revenue and cash flows, with both of those driven by booming backlog. Add on top of this how cheap shares were at the time, and I could not help but to take a bullish stance and rate the enterprise a "buy" to reflect my view that the stock should outperform the broader market for the foreseeable future.

Since then, that is precisely what transpired. While the S&P 500 (SP500) is down 3.5%, shares of this homebuilder are up a whopping 34.7%.

{kind=link}

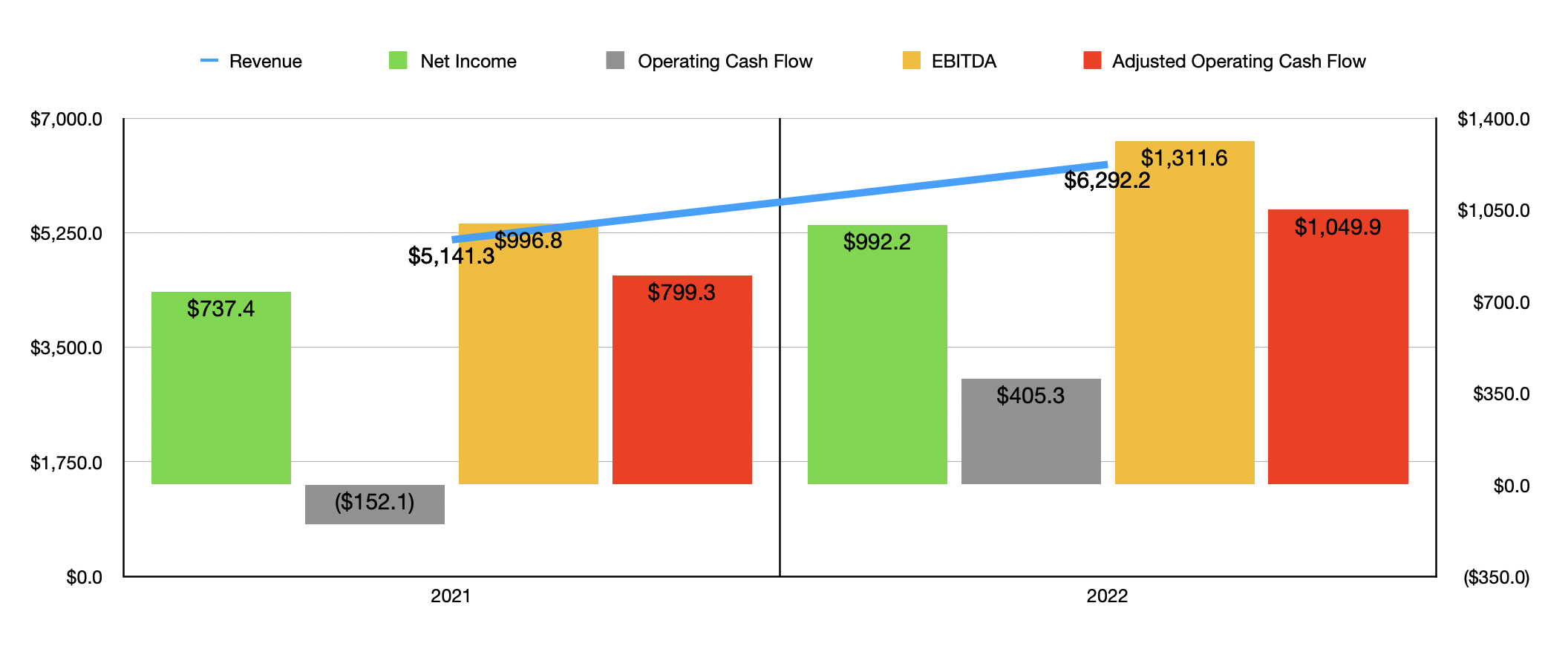

Based on this return disparity alone, it might be tempting to think that everything is great when it comes to Meritage Homes Corporation prospects. But that's not exactly what's occurring. First, we can start with the good news. In 2022 , revenue for the company came in at $6.29 billion. That's 22.4% above the $5.14 billion in revenue generated in 2021. This increase was really driven by two primary things. For starters, the number of homes closed, also known as sold, jumped 10.2% from 12,800 to 14,106. Second, the average sales price for a home shot up 10.6% from $398,000 to $440,100.

{kind=link}

On the bottom line, the picture for the company also showed tremendous strength. Net income jumped from $737.4 million to $992.2 million. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, went from negative $152.1 million to $405.3 million. If we adjust for changes in working capital, the increase would have been from $799.3 million to $1.05 billion. And finally, EBITDA for the enterprise jumped from $996.8 million to $1.31 billion.

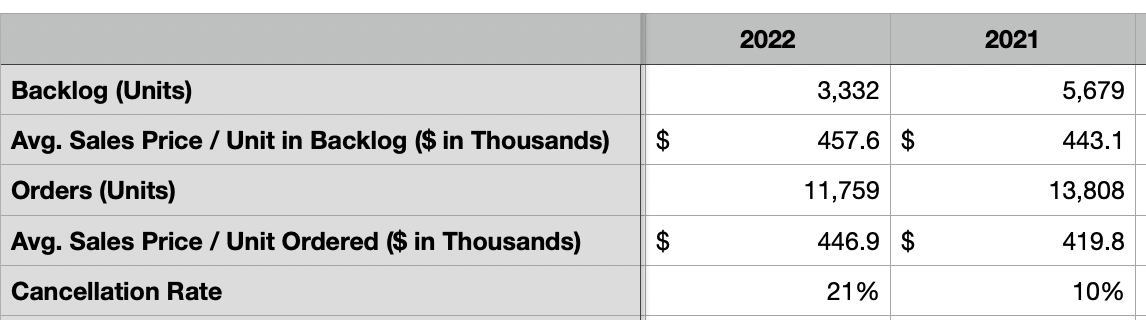

At first glance, all of this data is really positive. However, even then the cracks began to show. During 2021, as an example, the number of homes ordered by customers totaled 13,808. In 2022, this number dropped 14.8% to 11,759. Overall backlog for the company plummeted from 5,679 homes to 3,332, which translates to a year over year decline of 41.3%. And even though overall pricing was really strong for the year, the average sales price of a home in backlog was only 3.3% higher in 2022 than it was in 2021. Part of what made the backlog picture so bad was that cancellation rates also surged, jumping to 21% compared to the 10.2% seen one year earlier.

{kind=link}

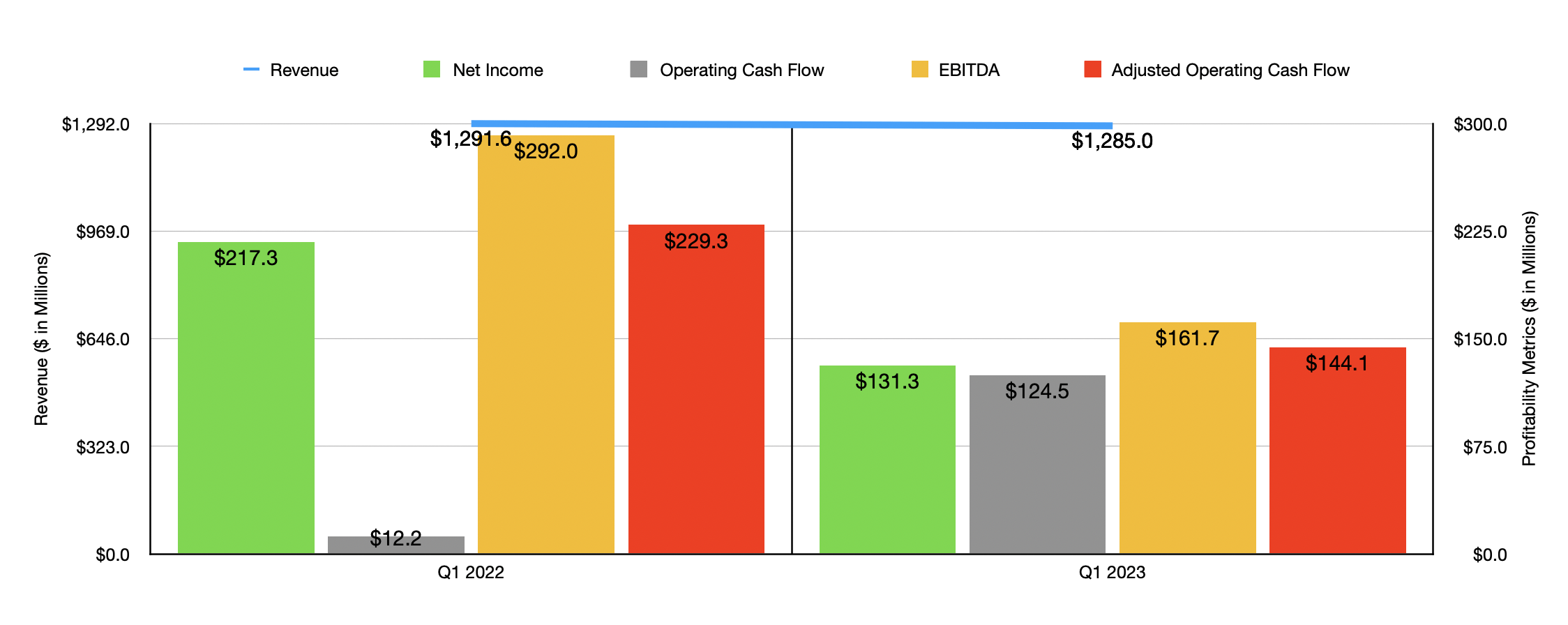

The financial pain for the company really began to show in the first quarter of 2023. Revenue dipped slightly from $1.2916 billion to $1.285 billion. Interestingly, home closing revenue actually grew during this time by 1.3% as the number of homes closed increased by 1.4% and as pricing remained virtually unchanged. But a drop in land closing revenue from $41.5 million to $17.4 million more than offset this.

On the bottom line, the picture for the company showed greater signs of weakness. Net income of $131.3 million during the first quarter of 2023 was substantially lower than the $217.3 million reported one year earlier. It is true that operating cash flow increased from $12.2 million to $124.5 million. But on an adjusted basis, it dropped from $229.3 million to $144.1 million. And finally, EBITDA for the company shrank from $292 million to $161.7 million.

{kind=link}

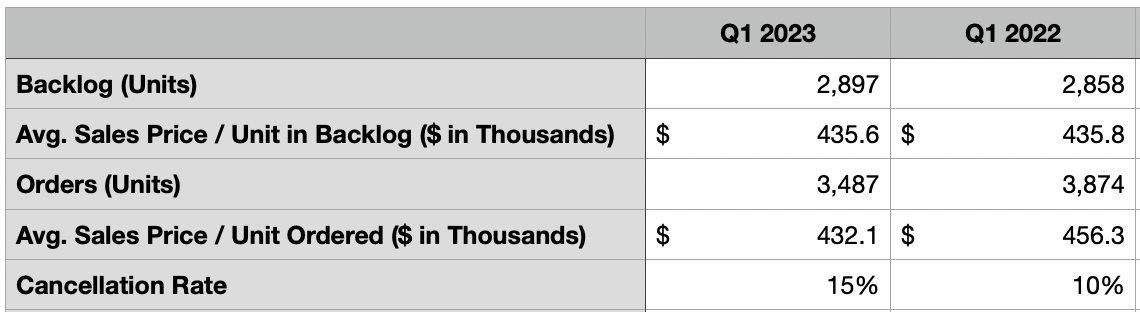

We need to dig deeper though you start to see where the pain really lies. The number of homes ordered for the company fell 10% year over year from 3,874 to 3,487. The average sales price also fared poorly, dropping 5.3% from $456,300 to $432,100. Cancellation rates of 15% exceeded the 10% reported one year earlier. And overall backlog for the company plummeted 41.4% from 6,695 homes to 3,922.

This is not an isolated event, either. As I wrote about in articles here and here , this is happening all across the industry. As I also detailed in one of those articles, however, I do view this as a short-term problem. The fact remains that we have a housing shortage in this country. So, what is currently a short-term issue will likely end up serving as a long-term catalyst for even higher home prices in the next year or two.

{kind=link}

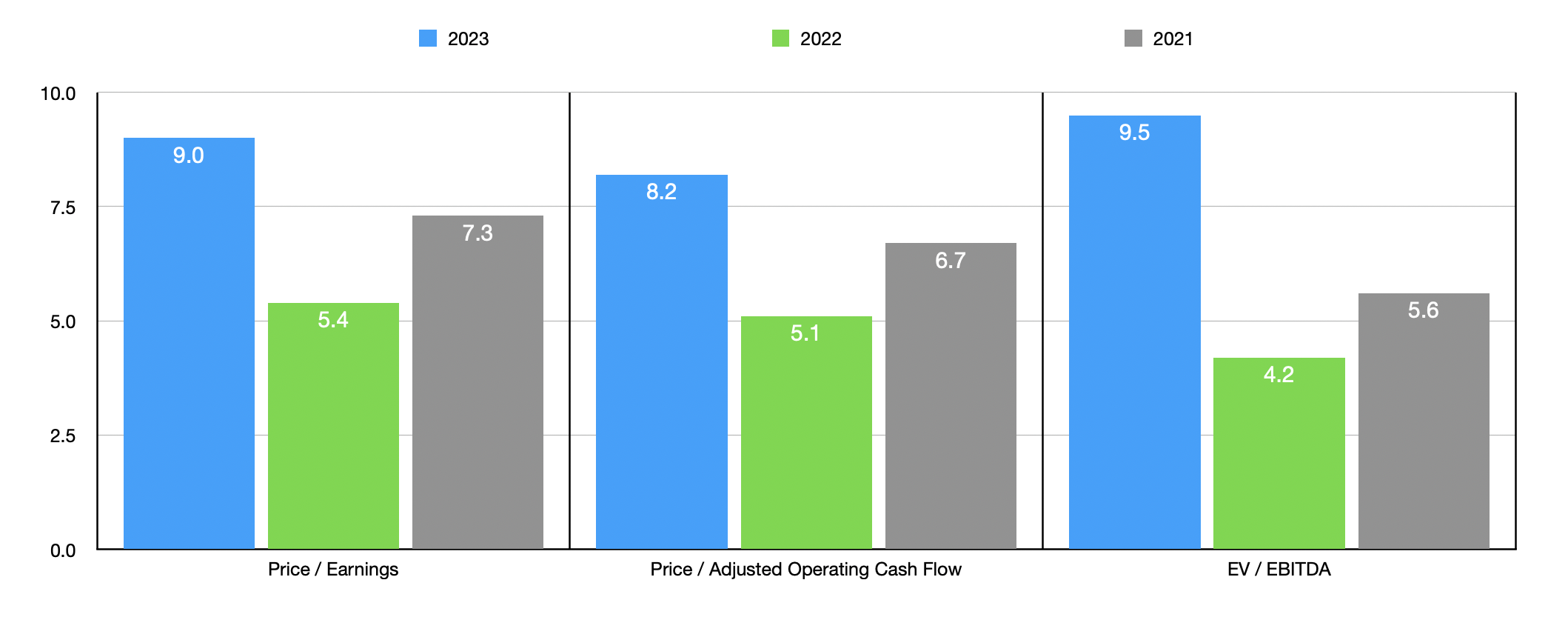

When it comes to pricing the company, we don't really know what to expect for the rest of this year. If we just annualize the results experienced so far, we would get net income of $599.5 million, adjusted operating cash flow of $659.8 million, and EBITDA of $726.3 million. Using these figures, I valued the company in the chart above. That chart also shows how the company is priced using data from 2021 and 2022.

As I do with other companies, I also compared the firm to five similar enterprises in the table below. Even though it may seem odd, I elected to use the data from 2022. But that's because the other five companies are being priced based on a trailing 12-month basis. So from a fundamental perspective and where they are in the housing cycle, they should all be comparable. On both a price to earnings basis and a price to operating cash flow basis, only one of the five firms was cheaper than Meritage Homes. And when we use the EV to EBITDA approach, our target was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Meritage Homes |

| 5.4 |

| 5.1 |

| 4.2 |

| Beazer Homes USA ( BZH ) |

| 4.5 |

| 5.0 |

| 6.4 |

| Century Communities ( CCS ) |

| 6.2 |

| 6.4 |

| 5.7 |

| Legacy Housing ( LEGH ) |

| 9.1 |

| 44.3 |

| 7.0 |

| Dream Finders Homes ( DFH ) |

| 10.9 |

| 49.2 |

| 8.7 |

| Landsea Homes ( LSEA ) |

| 6.8 |

| 8.0 |

| 9.0 |

Takeaway

Based on the data at my disposal, Meritage Homes seems to be showing signs of struggling. You would think that this would cause shares of the business to plunge. But this is the benefit of buying companies that are fundamentally cheap to begin with. Even when things go bad, there tends to be a margin of safety. This margin is doubled by the fact that the Meritage Homes Corporation business is also near the cheap end of the spectrum compared to similar firms.

But make no mistake. I fully anticipate further weakening for at least the next few quarters. But for those who are focused on the long haul, I would say that Meritage Homes Corporation stock is still a reasonable prospect to consider.

For further details see:

Meritage Homes: Still Appealing Despite Signs Of Further Weakness Ahead