MRSN - Mersana: When Reality Bites A Neutral Stance Prevails

2023-07-22 03:21:52 ET

Summary

- Mersana Therapeutics' stock price has had a turbulent year, with shares soaring over 100% before plummeting by 60% due to failure to demonstrate clinical benefits in ongoing studies.

- The recent clinical hold and Grade 5 bleeding events raised serious concerns, leading me to reevaluate MRSN's potential for approval and success, downgrading to Hold from Strong Buy.

- Despite the near-term overhang, I believe Mersana's current valuation and upcoming events are attractive and set a 12-month price target of $4.7 a share.

It's been quite the journey tracking Mersana Therapeutics (MRSN) throughout the year, and let me tell you, my feelings about it have had their own share of ups and downs. Just to give you a quick recap - when I covered MRSN in April , I was all-in on MRSN, waving my "Strong Buy" flag high and proud. Back then, MRSN was trading ~$4 per share, and I was bullish. I firmly believed people were getting too caught up in the risks and not seeing the potential rewards.

Lo and behold, not long after I shared my two cents, the stock price took off like a rocket, shooting up over 100% to a peak of $9.62 from a modest $4.38 when my article was published. Suddenly, the overblown concerns I had talked about were no longer overblown, and my thesis needed a bit of a reality check (though I didn't have a chance to publish an update about this change).

Then, just when we thought MRSN was on a tear, hitting a 52-week high, the unexpected happened. The stock price took a nosedive, dropping by over 60% in just a few days. The culprit? A realization of one of the risks I mentioned in my previous article: a failure to demonstrate clinical benefits in ongoing studies for UpRi.

So here I am, after having weathered this storm, shifting my stance from an enthusiastic "Strong Buy" to a more guarded "Neutral/Hold". In this article, I will review my thoughts on these rapid changes and the road ahead for MRSN.

The Recent Rise and Fall of MRSN

Following my last article, Mersana was trading at nearly $4.3 per share. Weeks later, the price dipped further to about $3.7. This kind of volatility - swings of 20-30% - is common in early-stage, small-cap biotech firms, so I remained undeterred; my thesis remained unchallenged by these fluctuations.

In May, however, MRSN experienced a dramatic leap to $7 due to promising Ovarian Cancer data from ImmunoGen ( IMGN ) - a sphere where MRSN's key asset is active. Fueled by momentum and FOMO, MRSN's price kept escalating, touching $8, then $9, and eventually reaching YTD highs at $9.62. This surge was not prompted by MRSN's own clinical data, hence not reinforcing my thesis. Consequently, the risk/reward scenario began to skew unfavorably. Since peaking, MRSN's price has dropped around 60% - a development I'll dissect below:

Mersana Therapeutics - Updates and Expectations

If you are not already aware of what triggered the downfall of MRSN, Edmund Ingham covered this event for MRSN in-depth, and this link here also explains the event. Briefly, MRSN was dealt a partial clinical hold, and the news is on some rather serious Grade 5 bleeding events. This news caught me by surprise that morning, making me take a second look at things.

I'll admit - I may have jumped the gun on MRSN back in April. I had a pretty optimistic outlook on the company, and I even made it my first "Strong Buy". At the time, I had done quite a bit of homework on it. I was listening in on all the earnings calls, looking through surveys, and even reading through street analysts' notes from their experiences attending dinners at ASCO or in discussions with Key Opinion Leaders. I was really hopeful about the near-term readout. But these new cases of fatal bleeding have certainly put a dampener on things.

Now there have been a total of seven fatal cases from the program due to either ILD or bleeding events. That's hard to overlook. Sure, there's a possibility that the UPLIFT readout, which I expect to get by early August, might have positive results in terms of efficacy. But considering the safety concerns, I'm finding it harder and harder to recommend investors to buy into MRSN and stick with my earlier enthusiastic stance.

Thinking about the US approval and weighing the benefits against the safety risks, as well as the commercial attractiveness of the drug with potential black-boxed warnings for ILDs and now bleeding, I've become more cautious. It feels like these concerns will hang around for a while and remain at the forefront of any discussion about MRSN. That's why I am shifting MRSN to Hold.

To recap a bit here. Before the market opened one day, MRSN reported that the FDA had placed a partial clinical hold on two of its UpRi studies named UP-NEXT and UPGRADE-A. This happened after a safety database review of ~560 patients dosed with UpRi revealed higher-than-expected occurrences of serious bleeding events.

To top it off, there were 5 Grade 5 bleeding cases in the data set that were reviewed - definitely not what I was expecting. Looking through the press release from June 15th and other updates from conversations that street analysts have had with the CEO and CFO, here are my takeaways on what the management team is saying:

- When they discuss the Grade 5 cases, it is not entirely clear how they were distributed among Phase 1 and the ongoing key trials. From the press release, though, it seemed like a big portion came from the plt-resistant OC ((PROC)) trials like the Phase 1 dose escalation/expansion and UPLIFT. I did not get a clear picture of the location and nature of these bleeding cases.

- Regarding the partial clinical hold, the FDA has only verbal questions for the company right now. They have less than a month to provide the questions in writing (early August). The management didn't share what materials they expected to need to answer these queries or when they expected to get back with the answers.

After all, I can't help but feel wary about UpRi's chances of getting approved in the US and being widely adopted commercially. Even if the UPLIFT data due in early August comes out positive, I think the safety concerns will still be a roadblock for investors, at least in the near term.

Cash Runway and Cash/Share

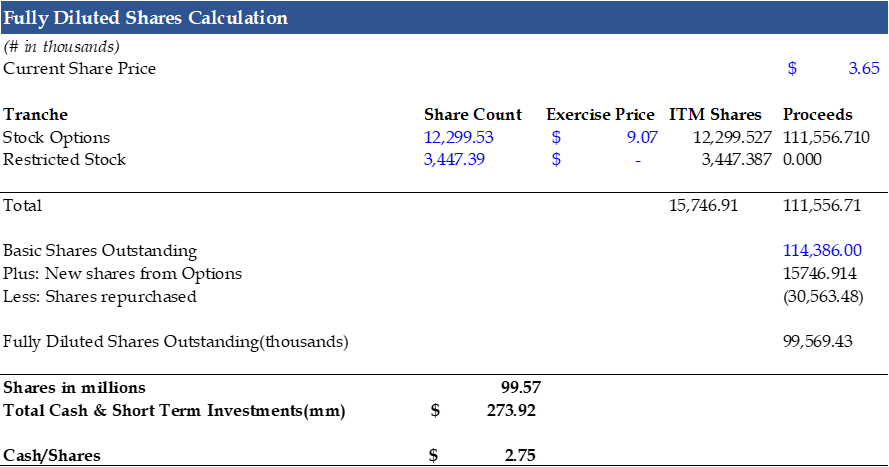

In my last article, I mentioned Mersana's cash runway, when they held $280.7 million in cash & short-term investments - now slightly lower at ~$274M. Still, with their average of ~$100M in R&D expenses annually, MRSN has a cash runway of over 2.5 years (largely unchanged from early April).

What I had not mentioned last time was their cash/share valuation. At $281M in cash & STI to the ~100M in fully diluted shares, that is ~2.8x cash/per share (same as it is now)

However, that $281M was when MRSN traded at an equity value of ~$500M. Meaning that you would buy MRSN's shares knowing that 56% of the value was backed by cash & STI. Now, that valuation has grown more attractive to 66% of the equity backed by cash & STI. Another way to look at it is from the price being $4.38 in April, $2.81 of that is backed by cash, and $1.57 is equity at risk; now, $2.75 is backed by cash, and $0.9 is equity at risk, as of writing. This valuation will likely get less attractive as MRSN's cash balance will likely continue to get less attractive as they continue to invest in R&D - but it also depends on the price swings.

{kind=link}

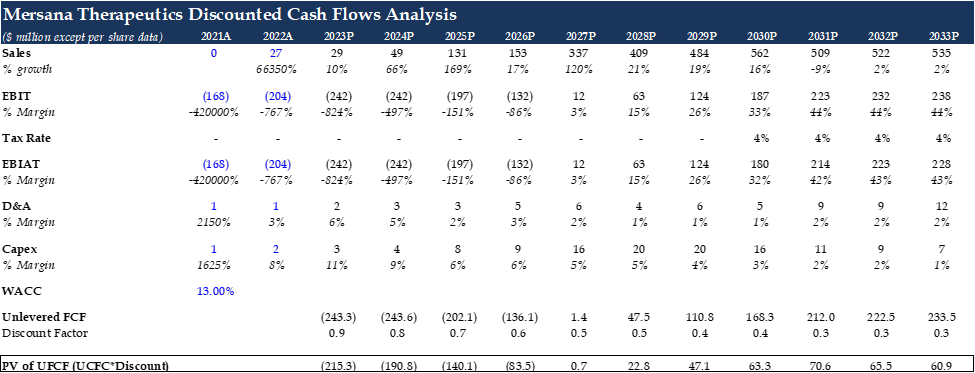

Discounted Cash Flows Analysis

I have made some changes to my P/L forecasts for Mersana, and you can find the updated DCF analysis below. The changes were primarily in the sales predictions. To be more conservative, I recalibrated the peak market penetration for UpRi to 25%. This was done considering the street estimates were a bit optimistic, hovering around 30%. Also, the estimated cost of the drug remained unaltered as the consensus suggests it to be around 20% of the TAM sales, aligning well with my previous assumptions.

Apart from that, I adjusted the GTN (Gross to Net - the difference between the list price and the net price after accounting for discounts and rebates) from the initial 25% to a more conservative 20%. This adjustment impacts the sales forecasts as it's directly subtracted from them.

As for the WACC, I previously calculated it to be 11%. However, after considering the Probability of Success (PoS) adjustments, I decided to increase it to 13%. The PoS introduced an additional 1% for UpRi and another 1% for '1660.

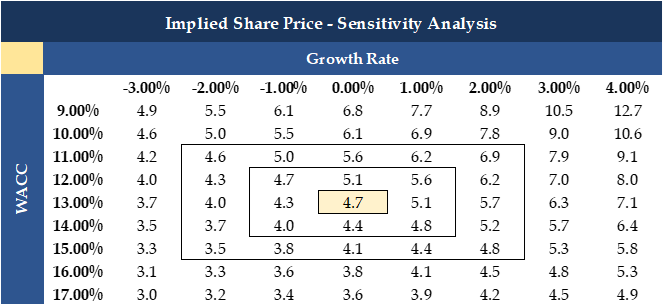

DCF (Author's Data) Calculation of Firm Value (Author's Data) PT Sensitivity Analysis (Author's Data)

{kind=link}

{kind=link}

Now, these are some very conservative estimates in my view, but for the short-term clouds, I feel this fits what the sentiment and stock price is pricing in, and still, the $4.71 price tag suggests an attractive upside to today's prices, and that I hold as my Price Target over the next 12-months until further notice from the management team and the FDA.

Concluding Thoughts and Outlook - My "Hold" Investment Case

There are some pretty pressing safety concerns - specifically, the ILD/pneumonitis and bleeding event. No matter how you slice it, these are not small issues, and they could pose significant challenges for MRSN's lead asset, UpRi. I want to be clear, though, I don't think UpRi is a bust. Quite the opposite, I believe that UpRi's clinical benefits could be pretty significant when stacked up against the current standard of care. But these safety risks are like a cloud looming over us, and they're not going anywhere in the short term.

While we wait for more data to come in, these concerns will remain a dominant narrative, possibly obscuring the potential benefits of UpRi. So, even though MRSN still has some exciting near-term data catalysts coming up, I don't expect them to resolve the safety overhang entirely.

But I would not get pessimistic here! MRSN isn't just about UpRi. They've got quite a few things cooking in the kitchen, with several early-stage clinical programs underway. Also, they've secured a handful of partnerships with other pharma companies, which might give them a bit of a boost in the near term or even lead to a buy-out. So, while I'm keeping a wary eye on the sentiment and the challenges, I'm also eager to see what these other ventures might bring to the table.

And so, as previously mentioned, the company's current valuation (cash per share) is now more attractive than ever, and their intrinsic valuation (DCF even after adjusting estimates) is far from unattractive, and I am setting a 12-month price target of $4.7 a share with a neutral stance for the near-term.

Risks to Rating and Price Target

Downside Risks

With a company like Mersana, there is a lot of potential for setbacks related to UpRi's clinical performance: (1) if UpRi fails to exhibit significant clinical benefits in ongoing studies, it will negatively impact its intrinsic value; (2) if tolerability and safety concerns rise with respect to UpRi, this will continue weighing on the stock price; and (3) UpRi's journey toward global approval is fraught with unexpected regulatory complications that could disrupt its trajectory.

Also, re-mention a couple of risks that I mentioned last time: (4) If Mersana encounters issues ramping up production, it could easily delay the commercial availability of UpRi; and (5) if the commercial launch of UpRi is slower than anticipated, it will continue to weigh on its intrinsic valuation. Likewise, if UpRi fails to extend its usage beyond the initial treatment indication, it will limit its market share potential.

On the upside , I have a few things that could boost my rating and estimates: (1) if Upri shows a more favorable safety profile than currently anticipated, it will positively impact my rating; and (2) should regulatory approvals be granted earlier than expected, it will lead to an upward revision of the street forecasts, along with mine, which will higher it's intrinsic valuation.

For further details see:

Mersana: When Reality Bites, A Neutral Stance Prevails