MRUS - Merus: Far More Constructive After Q1 Just Too Pricey At 28x Sales

2023-06-17 23:06:34 ET

Summary

- Merus has shown positive developments in clinical trials and regulatory meetings with the FDA, resulting in increased collaboration revenue and a more constructive investment outlook.

- Despite these positive factors, the company's current valuation of 28x forward sales is considered too high in my view, leading to a reiterated neutral view.

- Investors should watch for an improvement in valuations before considering entry, with a potential price objective of $30.

Investment Summary

The investment case for Merus ( MRUS ) is turning far more constructive in my view. Following the last publication in December, shares have certainly caught a strong bid and rated back to previous highs. Driving the results is a combination of:

- Q1 financials, indicating collaboration revenue increases YoY

- Clinical trial momentum in its core clinical programs, with several updates last quarter

- Regulatory tailwinds with positive meetings with the FDA on its pipeline assets

- Revision of analyst forecasts over the last 3-months.

Hence, there are marked improvements in fundamental and sentimental factors for MRUS, as you will see here today. However, these two points are quashed by the fact investors are asking you to pay 28x forward sales to participate in the company's good fortune.

As one might imagine, I can't get there to pay this multiple, not even with the positives discussed earlier. This is a classic case of, "growth at an unreasonable price" investing, something that I tend to avoid with mine and my clients' hard-earned capital. Net-net, I am reiterating MRUS as a hold, but am very constructive on this name and would urge investors to watch for an improvement in valuations to make an entry. I believe $30 would be the next price objective based on these assumptions.

Figure 1.

{kind=link}

Upcoming catalysts for price change

As a reminder, the company operates as a clinical-stage oncology enterprise primarily focusing on developing breakthrough antibody therapeutics. It has proprietary technology that has developed an array of antibody binding domains, known as "Fabs", capable of targeting virtually any desired molecular entity.

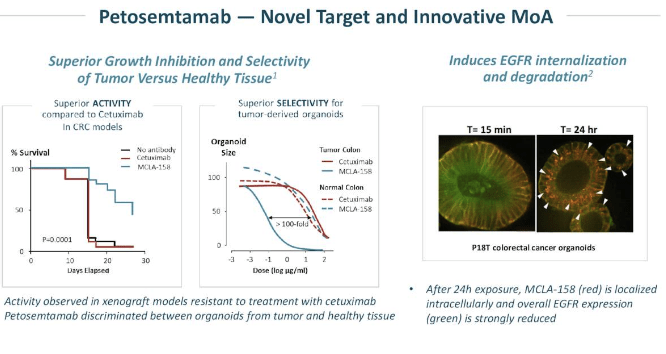

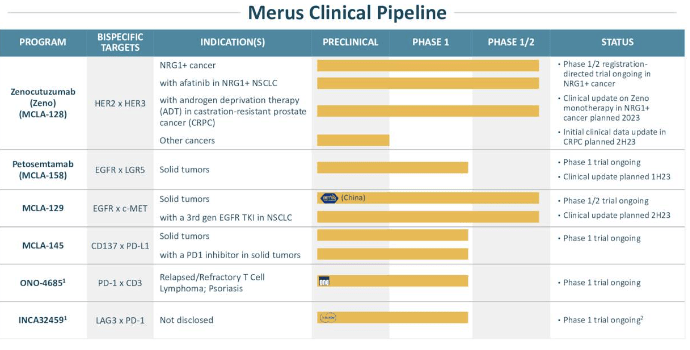

To date, its clinical programs have focused on developing its petosemtamab and Zenocutuzumab compounds. I had covered the underlying pharmacology for these formulas in the last MRUS publication, noting the mechanisms of action and additional factors. In that vein, the central catalysts for MRUS in the medium-term all envelope the company's clinical programs.

Figure 2.

{kind=link}

1. Recent clinical developments

MRUS was busy in Q1 on its clinical programs. There were many updates. To name the major few, I have summarised the following critical insights:

- In April the company announced the initiation of its phase 1/2 trial investigating petosemtamab in conjunction with Keytruda, for patients diagnosed with previously untreated head and neck squamous cell carcinoma ("UHNSCC"). This trial will look at safety and clinical efficacy of petosemtamab in the combination therapy.

- Also in April, the company presented interim clinical data during a plenary session at the American Association of Cancer Research ("AACR") Annual Meeting. Here it shed light on the ongoing phase 1/2 trial of petosemtamab in previously treated UHNSCC as a monotherapy. MRUS reported that 49 patients, who had once received treatment for UHNSCC, were administered the 1500 mg dose intravenously bi-weekly.

- The median age was 63 (ranging from 31–77), with males constituting 78% of the cohort. Moreover, patients had a median history of 2 prior lines of systemic therapy, with 94% of the cohort previously receiving chemotherapy.

- Among the 43 patients deemed suitable, notable antitumor activity was observed in the data. The overall response rate ("ORR") was 37.2%, including 15 confirmed instances of partial responses.

In addition to the trial updates, the company also held discussions with the FDA. Here, it presented interim results from the previous cohort of UHNSCC patients who received petosemtamab in their phase 1/2 trial. As a potential tailwind, the FDA provided clear recommendations regarding a potential pathway to registration for petosemtamab. This could be exciting in my book, especially if we get some movement on this before the end of FY'23.

Further to this, given the compelling clinical data, plus the productive exchanges with the FDA, MRUS is expanding its petosemtamab clinical program. It is looking to start an RCT with patients who previously received treatment, or at least remain untreated for HNSCC. The primary endpoint is the ORR, and has the potential to facilitate accelerated approval in my view– especially given the talks with the FDA. It will also determine dosage in these studies. It has started registrations for the trial. The company's full clinical pipeline is observed in Figure 2.

Figure 2a.

{kind=link}

2. Market-generated data

Given the lack of raw earnings data from MRUS, due to its current steady-state operations, price and market studies are invaluable sources to guide price visibility going ahead.

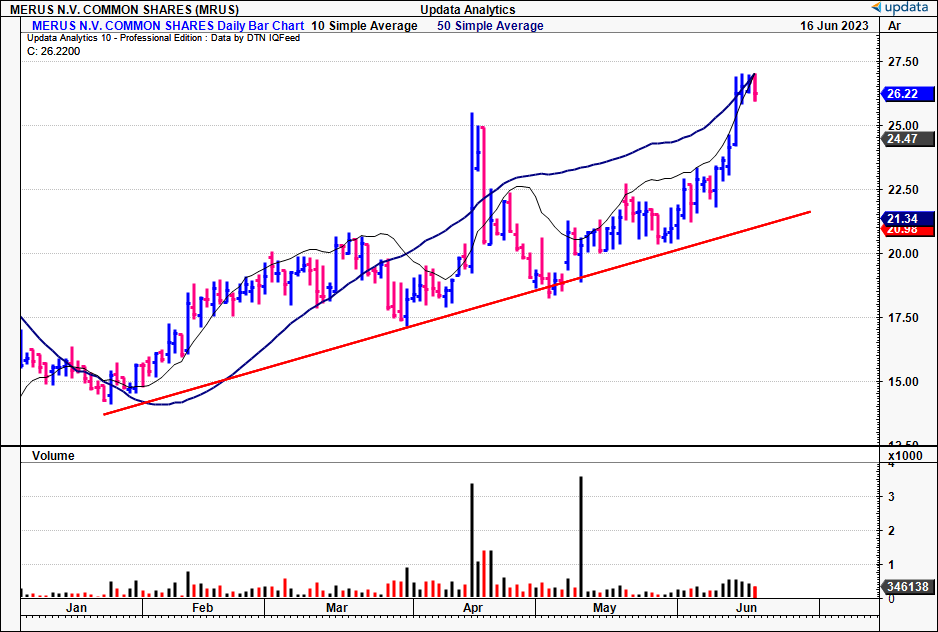

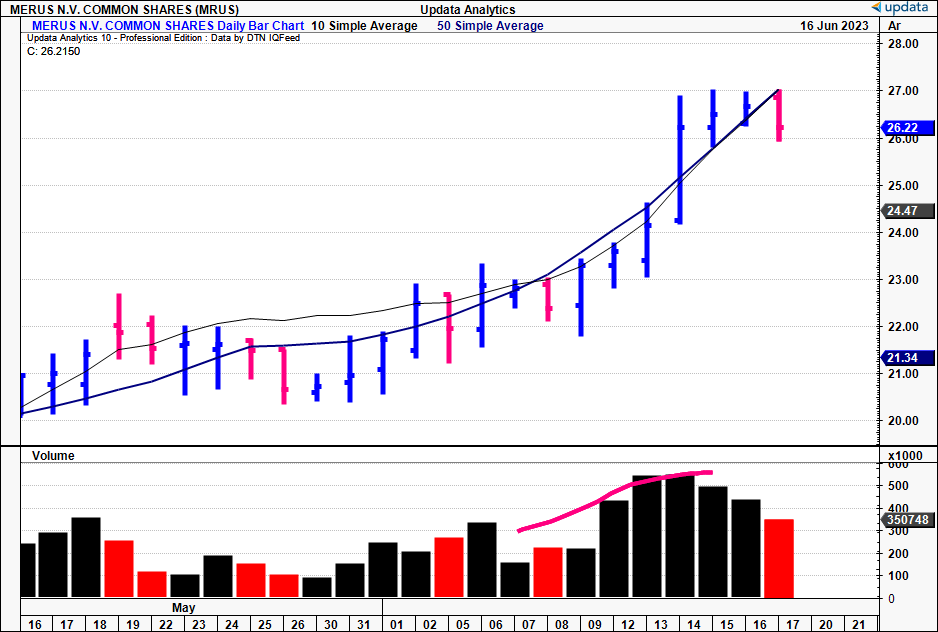

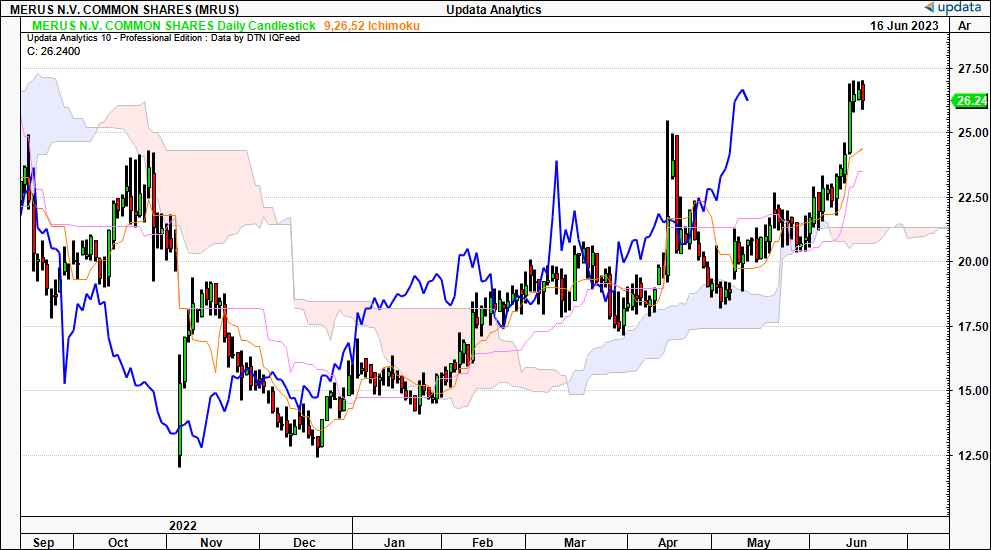

Figure 3 shows the recent rally that's begun in May for MRUS. It has curled up off lows and now trades at YTD highs, eclipsing a YTD gain of 67%. A couple of things are noted here:

- The stock has broken above the 50D and 10-week moving averages and rode these as support to the current session. A recent pullback with a liquidity grab has it positioned right at the precipice of both MA's.

- The rally was bought on high-volume buying adding weight to the move and showing the presence of large accounts/orders. You need this kind of demand in order to see a move sustain itself, as it shows the presence of strong hands buying the stock in my view.

- This volume was >50% higher than what we've seen over the last 3-months to date in 2023 for MRUS.

As such, it tells me demand is high on the stock at this point and that the recent shift upwards in price was done on high volume buying.

Figure 3.

{kind=link}

It is quite a spectacle to see the breakout in trend-terms. The daily cloud chart shows this well. MRUS has broken above the cloud in June and the lagging line is equally as bullish in its position. To me this chart is bullish. The gap up above the cloud is telling, suggesting the trend is strong, and has an allowance for some pullback and will remain on trend. I don't have much more to say on this than that point.

Figure 4.

{kind=link}

On these bullish factors, we've got upside targets from the point and figure studies shown below to $29.50. This is bullish as well and supports a buy rating when the fundamental data arrives. Note these have provided good clarity to date, and use mathematical calculations in order to derive objective price targets. I would be looking to $29.50 as my next technical target based on the market generated data.

Figure 5.

Data: Updata

3. Sentiment shifting higher

The impact of investor and broad market sentiment cannot be overstated enough. Sentiment has emerged as a more modern 'factor' to gauge investment insights, but it is perhaps one of the most logical. Investors are either bullish, bearish, or neutral on a company's (and therefore its stock prices) outlook. You'd want to know at which point of the dial the market is sitting before making any calculated investment decision.

Sentiment can be gleaned from analysts forecasts, company internal projections, price momentum, and also options positioning in the derivatives markets. For MRUS, analysts have revised their forecasts for the company's revenue up 7 times in the last 3 months, with a corresponding amount of revisions to earnings. This tells me that Wall Street is expecting 66% growth in turnover in FY'24, and could see MRUS doing $100mm in sales by FY'25. The analyst's revisions are certainly a critical fact in my view.

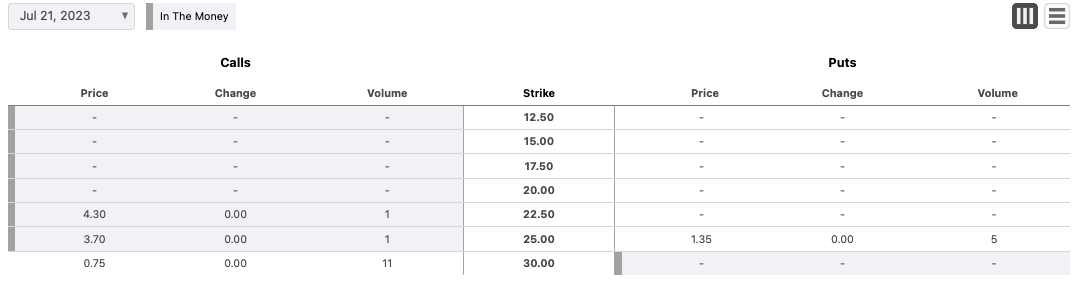

Looking at the options-generated data , market participants are speculating on MRUS pushing to $30 based on the number of calls bought at that strike price. There is no hedging currently in the money at prices around this level. This is critical too as it shows what actual market participants, those with money at risk, and skin in the game, are doing with their actions on MRUS. To me, this says that investors are looking to $30 at least on their speculative buys, in-line with the price targets discovered earlier. This adds another layer of confidence to that potential price range.

Figure 6.

{kind=link}

Finally, momentum is tremendously strong as well. MRUS is trading 25–40% above the 50, 100 and 200DMA's after its recent breakout. Further, the price performance is in the green across all time frames too, as indication of the current investor sentiment, paying higher market prices than 1, 2 and 3 years ago.

Of course, the investor of today doesn't get paid for yesterday's price gains. However, what is important to note is the fact these 3 areas show that sentiment is shifting higher for MRUS. This would be critical in attracting further investment in my view, where investors could pay higher multiples on today's values. This is supported by the clinical trial and regulatory catalysts discussed earlier.

Figure 7.

Data: Seeking Alpha

Valuation and conclusion

Investors have large expectations for MRUS, but there is still no justification to pay 28x forward sales for any equity stock in my view. Yes, there are growth factors to consider, and yes, the regulatory catalysts could warrant a massive rating higher. That much is absolutely true.

But you'd be making those selective bets more based on speculation than not at the current chapter in MRUS growth story. There simply isn't the tangible econometric data to imply MRUS is worth 28x forward sales at the moment. Plus, the payback on this would be unjustifiable either, and MRUS would need to compound its revenues at ~1,000% annually over the next 3-years to get to a c.$1.3Bn market cap (MRUS' value at the time of writing).

Unsurprisingly, I can't get there, and despite all of the positive factors discussed here today, the company is not investment grade at this point on valuation factors. This supports a reiterated neutral view.

In that vein, I am reinstating the hold thesis on MRUS from my account. I am very constructive on the company's clinical programs– both what it achieved in Q1, and what's to come. That, and sentimental factors are appealing as well, suggesting investors will be indeed buyers of the stock into the coming future. However, you can't ask me to pay 28x forward sales to buy a company that did $41mm in sales last year with a $160mm operating loss, it just isn't worth it my view. Net-net, reiterate hold.

For further details see:

Merus: Far More Constructive After Q1, Just Too Pricey At 28x Sales