MRK - Merus: Petosemtamab And Zeno The Driving Forces Behind Investment Returns

2023-08-30 21:22:13 ET

Summary

- Merus stock has cooled down after a strong rally, but long-term investors are sitting on a 47% gain since January.

- The company's pipeline includes promising clinical assets, but sentiment towards the stock is mixed and price structure has broken down.

- Updates from its major clinical programs are the key drivers to equity returns for MRUS at this stage in its lifecycle.

- Net-net, reiterate hold.

Investment updates

The mercury has cooled down in the equity stock of Merus ( MRUS ) after it staged a strong rally from January—July this year. It has since rolled over, and sells roughly in line with the June publication . Nevertheless, those investors holding it in the long account from January are still riding a c.47% gain as I write.

MRUS's differentiated programs offer plenty of upside potential as it passes each clinical milestone along the approvals process. Its hypotheses in various carcinomas are interesting and could provide a medical breakthrough to what are otherwise complex disease segments.

Critically, however, the company is pre-revenue and will require a series of funding rounds to raise capital to grow its pipeline-conversion-probability. Whilst this is the norm for clinical-stage companies, the question of opportunity cost immediately presents itself in this era of tight money, higher rates, and a higher cost of capital.

Net-net, considering the abundance of selective opportunities with more predictable, stable cash flows, I continue to rate MRUS a hold, but am watching the name closely as we walk through H2 FY'23. Reiterate hold.

Figure 1.

{kind=link}

Critical factors within the MRUS investment debate

Overview of operations

MRUS is a clinical-stage company that utilizes a range of patented technologies to facilitate the generation of antibodies. In essence, MRUS is looking to transform antibody innovation—a noble purpose, and potentially lucrative one if the company eventually gets it right. The company's methods centre around its recently developed MeMo mouse , which allows for the synthesis of a wide range of heavy-chain antibodies, in conjunction with a shared 'light chain' that can bind to virtually any antigen target. By the way—this is an actual mouse, not a computer mouse. MRUS immunizes these MeMo mice with a selection of antibodies, which can then be used for functional screening in clinical studies or drug research. MRUS offers the mice on license as well, creating a potentially differentiated revenue stream with added benefits to society.

MRUS' heavy-chain and CH3 domain dimerization technology has produced a number of bispecific and trispecific antibodies, distinguished for their reported purity. These breakthroughs have impacts on the development of various therapeutic agents. For reference, both bispecific and trispecfic antigens are routinely used in the study of treatments for cancer, including immunotherapy.

Critically, being a clinical–stage firm, MRUS has not generated any revenue from product sales as of yet. The company's focus has been on advancing antibody candidates through various stages of development. It is therefore positioned at all points along the value chain, including discovery, pre-clinical development, clinical trials, and regulatory approvals.

As a result of it being pre–revenue, MRUS will need external financing to fund its operations for the time being. To date, it has completed a number of public and private equity placements, the most recent in early August. It raised another $150mm at $22/share in that round by issuing 6.8mm shares. As a quick history, it raised $55mm at $18/share in 2018, $120mm at $24.75/share in 2021, and another $110mm at $28.50/share in late 2021. Hence, the latest stock offering values the company at a lower mark than 2 years ago, but I wouldn't say this is surprising given 1) the state of capital markets from 2020–'21, and 2) the higher cost of capital we're now dealing with from 2022 onwards.

Key clinical assets that could move the needle

The company's pipeline holds several clinical assets that have interesting formulations and potentially interesting economics if approved on market. Petosemtamab and Zenocutuzumab are the 2 standout formulations in my view, and offer the most promising outlook in the mid-term.

- Petosemtamab

The critical pipeline asset for MRUS in my opinion is p etosemtamab . It is a part of its 'Biclonics' platform. The company is currently evaluating the compound in recurrent or metastatic head & neck squamous cell carcinoma ("HNSCC") through a dose-finding phase 2 study . Outcomes from the trial will determine optimal dosage levels and a therapeutic range for MRUS' future trials.

Based on the early data from its phase 1/2 arm, the company has slated for a phase 3 progression, potentially starting in mid-2024. It will examine petosemtamab's efficacy as monotherapy or combination therapy with Merck's ( MRK ) Keytruda label. Overall response rate ("ORR") and clinical benefit will be the main outcome measures, so if the label holds up well in safety and efficacy testing, this could be a potentially bullish point for its stock price in my view. It would certainly require the company to raise more money to get the ball rolling, but that's not the worst scenario either, because if it can attract sophisticated capital, it's a sign said investors—who will have done their homework—might see long-term potential in MRUS.

- Zenocutuzumab (aka Zeno)

Zenocutuzumab , or " Zeno " for short, is a potential treatment for NRG1+ cancers and other solid tumours. For reference, NRG1+ cancers are those that display a particular genetic anomaly affecting the NRG1 gene. This gene is responsible for encoding a protein that is crucial in facilitating cell growth, development, and communication.

MRUS is establishing the anti-tumour efficacy of Zeno as a standalone therapy, and in combination with established treatments, in the phase 1/2 eNRGy trial. To date, Zeno has been administered to >175 patients, and already exhibited promising clinical potential. Such is the potential, the FDA granted Zeno 2 breakthrough therapy designations ("BTD"), plus, it awarded fast track designation ("FTD") for the drug in NRG1+ cancers, and orphan drug destination ("ODD") for pancreatic cancer and non-small cell lung cancer ("NSCLC").

Consequently, there's plenty of clinical trial momentum building around Zeno . Along with its petosemtamab compound, it could be another event-driven catalyst to see MRUS trade higher, provided trial results are favourable. For example, the stock sold off with authority in late 2022 after the FDA said it needed more enrollments in its phase 1/2 trial in order to grant a biologics license application ("BLA"). Such is the case with clinical-state biotech's—the stock returns are basically all event-driven, given the lack of fundamentals. And, just as it can be a lucrative ride on the way up, any hiccups along the way in terms of trial data or FDA overhang can send prices on the same course to the downside—and at pace.

Sentiment in MRUS = balanced

Given the lack of economics to square off and fundamentals to go by, what the market is saying in terms of sentiment is critical in appraising MRUS equity stock as an investment. Sentiment is mixed in MRUS' equity stock and we see this in three primary ways.

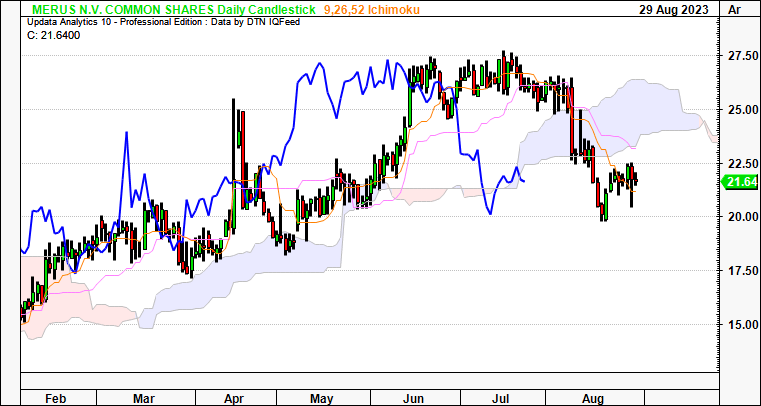

One, price structure has broken down in MRUS rolling into August. This aligns with the selloff in broad healthcare equities around the same time. It would appear the company's Q2 filings didn't help the matter, posted around the same time.

- The daily cloud chart in Figure 2 is helpful to this regard. It shows the price line below the cloud, but the lagging line testing the cloud base as I write. The cross over the cloud in August isn't the best sign for mid-term pricing in my view. You'd need a break to $24.00 then above $26.00 to see it sell near previous highs, currently the cloud top shown in blue.

- Thing is, as I mentioned earlier—it's all event-driven for MRUS' market pricing at the moment. Without such catalysts as trial readouts, FDA tailwinds, and so forth, it may be a long ride for those holding MRUS inventory in their portfolios. Those with the MRUS inventory on hand may find it difficult to find buyers without these in situ.

Hence, the below chart corroborates a neutral view in my opinion.

Figure 2.

{kind=link}

- The point and figure studies below support the notions raised above. Critically, there is breadth in the price objectives spun off by the P&F studies. We've got upside targets to $35.50, followed by downsides to $14. The divergence in both directives provides little confidence in a directional bias, but does support MRUS pushing further sideways into more congestion.

- Hence, I'd be looking to $14 if MRUS breaks lower, and optimistically eyeing the $35 mark if it were to reverse and rally higher. Again—you'd need a set of catalysts that aren't already baked into the current market structure to see it do this.

Figure 3.

Data: Updata

Two, t here have been 5 revisions to MRUS' revenue outlook by Wall Street analysts over the last 3 months.

Like it or not, but these targets are used extensively by a number of market participants. Hence, you've got the view—and potential positioning—of a large capital pool by observing these numbers.

These targets have made revisions out to the coming 5 years or so, and it's the 2027/'28 updates that offer the most perspective. Consensus now sees $270mm in sales by FY'27, followed by $440mm the year after. Granted, this is still 4, 5 years out. But these could very well be the periods to look out for, especially if MRUS makes mention of similar time frames in its projections. Think of it more rationally as well—the sell-side has undoubtedly done the heavy lifting in market modelling and gauging the addressable market size for MRUS. In that vein, you're getting one view of what the market opportunity could be for the company once at commercial stage. This is potentially bullish, offsetting current market-generated data.

Three, options generated data points to a balanced chain in September and October. September calls are showing most demand around the $25 strike price, with the bulk of September puts at a $20 strike depth. Out to October, you've still got the $25 exercise, but there's heavy put demand at a $22.50 strike depth on the puts side. Hence, those with actual money at risk are looking to the $22–$25 region to either buy or sell MRUS stock. There's no saying if these are strategies that look to profit in sideways markets, either. Nevertheless, this is a neutral point in my view.

Valuation and conclusion

The stock still sells at 28x forward sales, in line with where it was priced in the June publication. After the latest equity raise, it's been priced at a $1.25Bn market cap, and ~$950mm when stripping out $265mm in cash on the balance sheet.

Say consensus is right, and MRUS does hit $440mm in sales by FY'28. That's still 2.85x revenues at today's market value (1,250/440 = 2.85). In other words, in the above scenario, MRUS is priced to nearly 10x its top-line over the coming 5 years to trade fairly at current multiples (28/2.85 = 9.8x). Thing is, on the company's TTM collaboration revenues of $41.2mm, that's not an unrealistic expectation based on The Street's estimates (41.2x10 = $412mm). So I'm keeping a focused eye on MRUS moving forward, especially if trial readouts imply it will move along with commercializing its two main clinical assets at a faster speed than anticipated.

It's also worth noting MRUS is rated as a 'buy' from the quant system , using a blended composite of objective factors. Hence, there are multiple facets to this debate, both on the bullish and neutral side.

Figure 4.

{kind=link}

In short, MRUS has a number of promising clinical programs to mine from its pipeline. Each of the clinical assets are equally as promising should they move towards approval. But without the raw economics or company fundamentals to work from, it's difficult to prescribe an accurate price objective for MRUS in my view. There is scope for it to trade higher on the tactical side, but as a strategic allocation, the required rate of return would be in multiples of our required 12% hurdle rate (in line with long-term market rates). Hence, I'm watching MRUS with a close eye over H2 FY'23, looking for any identifiable catalysts that could see it sell higher. But I'm not able to advocate it as a screaming buy just now, based on reasons from above. Net-net, reiterate hold.

For further details see:

Merus: Petosemtamab And Zeno The Driving Forces Behind Investment Returns