MESA - Mesa Air Group: Get Ready For Another Leg Up

Summary

- Mesa Air Group's Jon Ornstein and team successfully navigated an incredibly tricky series of maneuvers. These actions averted bankruptcy and now position this stock on a great turnaround path.

- Mesa finally signed a new union agreement with its pilots, and United agreed to the higher wages under its CPA agreed. Also, United is taking over America's planes.

- The wind down of the $5 million per money, in losses, from the American CPA, ends on April 3, 2023. Moreover, Mesa's year-end debt will be materially lower.

(This article and idea was originally published on Second Wind Capital, on the morning of January 8, 2023 - see the appendix section.)

Executive Summary:

Mesa Air Group, Inc. ( MESA ) is one of my best (current) ideas. It is under the radar and a compelling micro cap turnaround story. Only a few months ago, the conventional wisdom was Mesa had a high likelihood of getting a 'going concern label' of doom, by its auditors, and given its then elevated debt load, bankruptcy looked highly probable.

Lo and behold, John Ornstein and his group did a remarkable group of hitting all 'green lights' coming home. Not only did Mesa avert bankruptcy, through a series of really strong business moves, by the second half of 2023 (calendar year), Mesa is well positioned to significantly de-leverage its balance sheet, resolve its protracted pilot shortage, and resume generating solid Adj. EBITDA.

Although the stock is up nicely off its December 2022 through lows, I would argue that Mr. Market's lack of imagination and inability to synthesize this turnaround means there is a strong probability of another leg up. Moreover, in turnarounds, it is really more of an art than a science, where it is about being directionally right, as opposed to building a model with pinpoint precision.

Let's talk Mesa Air Group, and why I think there could be another leg up

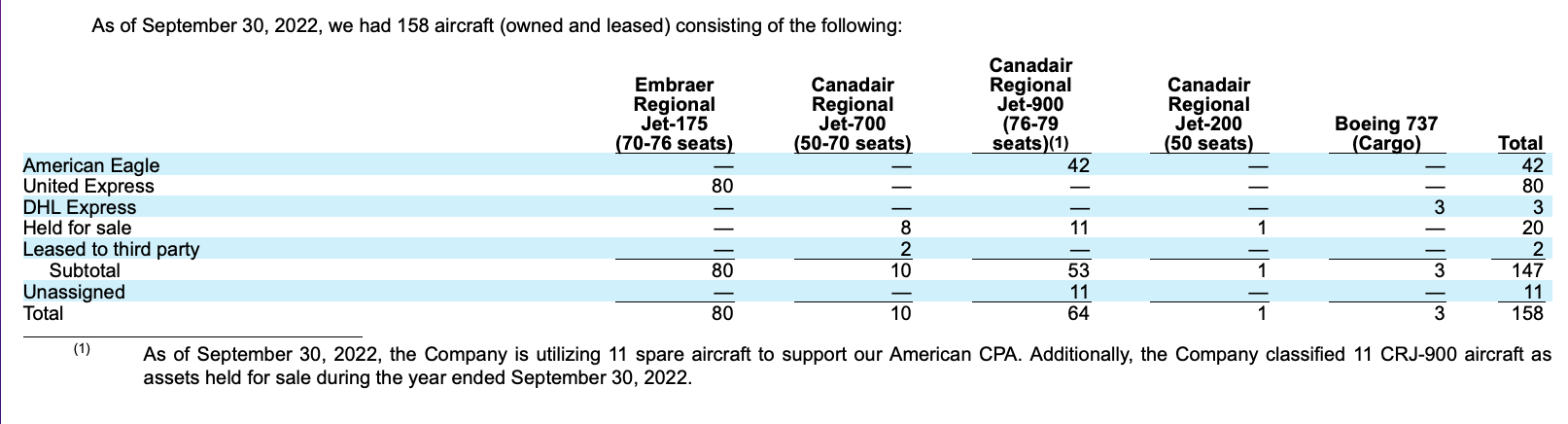

As of September 30, 2022, its fiscal year end, Mesa Air Group, Inc. operated 158 aircraft. Mesa is a regional airline carrier that flies under long term capacity purchase agreements ("CPAs") for American Airlines, Inc. ( AAL ) and United Airlines, Inc. ( UAL ) as well as a Flight Services Agreement ("FSA") with DHL Network Operations ((USA)), Inc. ("DHL").

{kind=link}

To be crystal clear, and so readers understand these important details, Mesa operates, as a regional carrier, flying under the American Airlines banner (under the name American Eagle) as well as the United Airlines banner (under the name United Express). They get paid a monthly minimum and then get paid based on the number of flights and number of block hours actual flown.

See here:

Our agreements also shelter us, to an extent, from many of the elements that cause volatility in airline financial performance, including fuel prices, variations in ticket prices, and fluctuations in number of passengers. In providing regional flying and cargo flight services under our agreements, we use the logos, service marks, flight crew uniforms and aircraft paint schemes of our major partners. Our major partners control route selection, pricing, seat inventories, marketing, and scheduling, and provide us with ground support services, airport landing slots and gate access.

(Source: Mesa Air 10-K)

In addition, and just to be clear, Mesa get reimbursed for fuel, airports fees, etc.

Mesa's role is be an important regional feeder, connecting small and more rural cities with larger and major hubs, to fill in the gaps and enhance the fullness of the major carriers' coverage universe. They play a vital role, in the overall operations of the mainline airline's complex hub and spoke systems.

Why The Stock Has Gotten Dinged And Our Opportunity

COVID was an incredible shock to the entire airline industry. To make a long story short, the U.S. government had to offer the airline industry financial support and reimbursement, as so much flight capacity was forced to be grounded and travel was super depressed, notably during the early to intermediate stages of Covid.

However, as vaccines became more abundant and readily available and hospitals built enough capacity to handle surges and different virus variants, travel and demand to travel picked up sharply. Unfortunately, the overall demographics of the pool of certified U.S. pilots was long in the tooth. Therefore, there were a number of early retirements and there is and continues to be a higher percentage run rate of annual retirements, simply due to demographics of collective pool of certified commercial pilots.

In 2013, there was a law, passed by Congress, that dramatically increased the number of flight hours required to ascertain a commercial flying license, from 250 certified flight hours to 1,500 hours.

As demand snapped back sharply, the supply of pilots moved from slightly over supplied to a deficit, wages increased dramatically. In 2022, it wasn't uncommon to see at least 100% increases, along with various bonuses and other incentives packages. Therefore, what happened was other airlines started picking off Mesa's and other regional airline's pilot workforces by offering them more money. Mesa's attrition rate increased dramatically, and all of a sudden, as of mid September 2022, Mesa easily had demand for 1,100 pilots, and found itself short by upwards of 450 pilots. As the 1,500 hours required for commercial training takes time, you can't easily mint all of these new pilots.

And in the summer of 2022, just as Mesa was on the cusp of signing an agreement with its pilot union, however and simultaneously, other competitors, including its purported long time partner, American offered big pay increases. This torpedoed Mesa's union deal, just before the finish line. Moreover, and American was acutely aware of the situation, due to contractual penalties, for underutilization, American refused to compensate Mesa for the incremental labor cost of paying its pilot more. So, these losses combined with penalties resulted in Mesa losing $5 million per month, on its CPA, with American, and we're only talking about a fleet of 42 planes!

See this commentary from Mesa's CEO, Jon Ornstein, made during Mesa's Q4 FY 2022 conference call (12/29/2022).

No. And I'll tell you why. I mean, primarily, a couple of things that have changed the dynamics at first. The United flying, I mean, obviously, there'll be a transition period but the United flying on a run rate basis will not lose money. I mean we're losing roughly $5 million a month in the American operation, which based on the numbers that we have and where we're going to get -- how we view the United contract will not be loss-making, will be, in fact, profitable. In addition, we are shedding quite a bit of debt through this process and just the savings alone of U.S. Treasury debt, I believe, is $5 million -- $6 million a year. That also obviously will help add both benefit cash flow and earnings.

But I think it's fair to say that there is a transition period that's going to require some time, and there are training expenses, which are still extremely high, and it's going to take some time to work through that. But again, shedding the loss-making operations, like I said, which was about $5 million a month, is actually pretty significant.

And remember that as part of the transaction, which really was the heart and soul of the transaction is that United has agreed to pay the same wage rates that we offered the -- that were offered at United throughout the system as well as to the American -- the former American pilots that will now be flying on behalf of United. I mean that is singularly the biggest reason that this deal moved forward the way it did, and we're just very pleased and thankful that United has seen obviously some value for themselves as well to see this additional flying being done as we head into March and the summer of 2023.

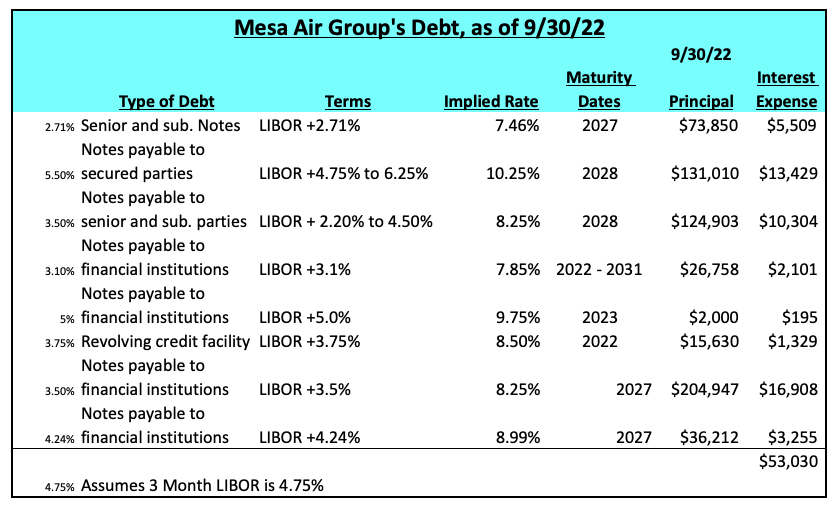

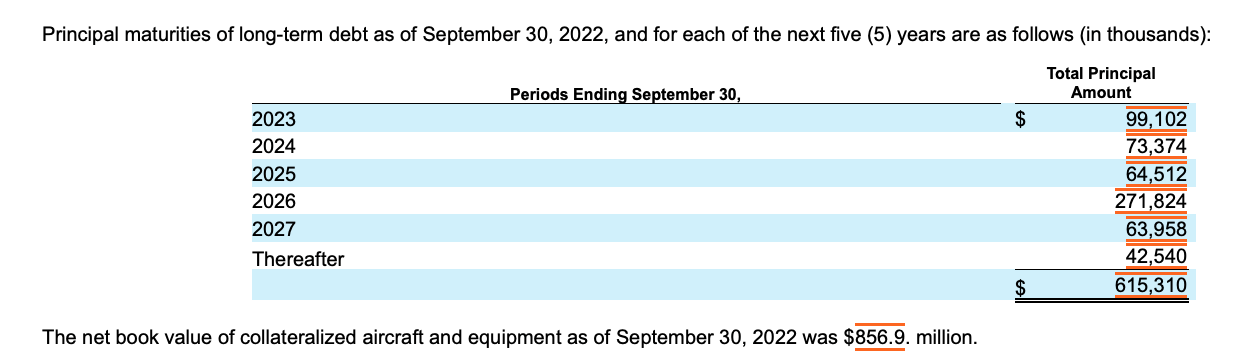

In addition to the pilot shortages, Mesa has a fairly leveraged balance sheet. So the ongoing interest expense, as well as upcoming maturity dates in FY 2023, meant Mesa literally had a gun to its head.

{kind=link}

And just to be clear, and in case you're wondering, the underlying net book value of the collateral tied to its aircraft and equipment was $856.9 million, as of September 30, 2022.

{kind=link}

What Happened

With literally a gun to their heads, Jon and team, turned lemons into lemonade! Let me walk you through their leadership actions. This leadership is the difference between bankruptcy and a nice turnaround for equity holders. Mesa's pivotal relationship with United is the primary reason why Mesa's isn't going bankruptcy and why the equity has value. Absent a series of events, and Jon Ornstein needed to hit all green lights, coming home, and he did, Mesa's equity was TOAST!!!

So let me walk you through what happened...

1) They reached a collective bargain agreement with is ALPA, at 118% to 172% pay increases. This stemmed the hemorrhaging of pilots to other carriers, in search of more pay.

In August 2022, we entered into a Letter of Agreement with the Airline Pilots Association ("ALPA"), which provided for increased overall hourly pay increases of nearly 118% for captains and 172% for new-hire first officers. While we remain engaged in negotiations with ALPA over other areas of our collective bargaining agreement with ALPA, we believe these pay increases will positively impact our ability to attract, hire, and retain pilots in future periods.

(Source: Mesa's FY 2022 10-k)

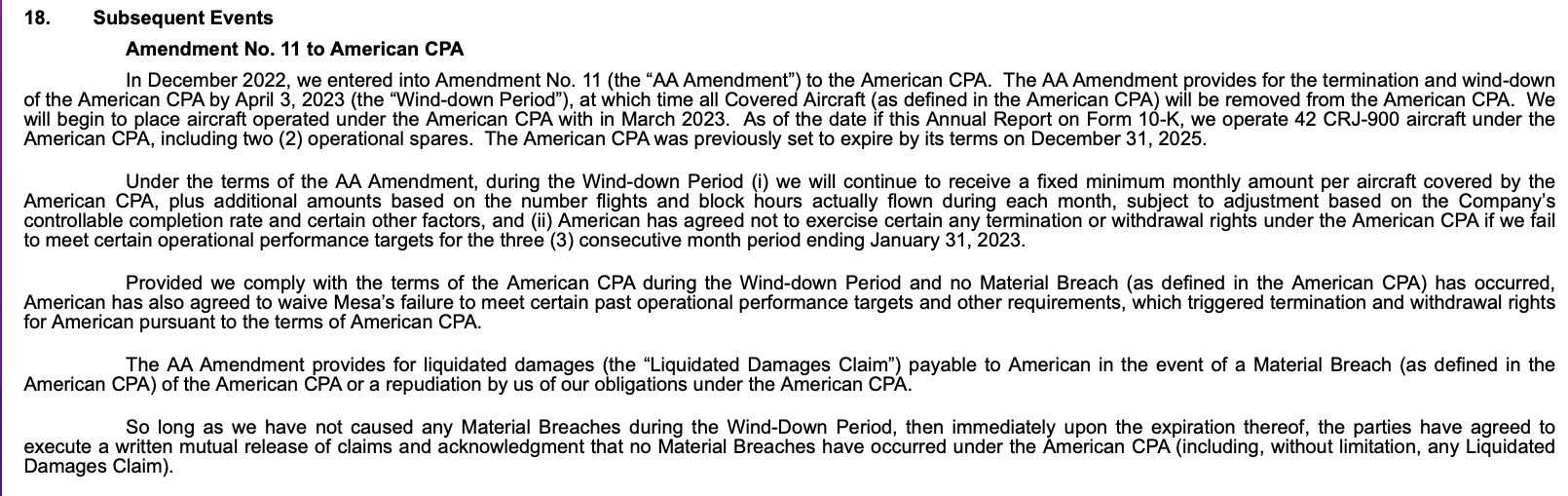

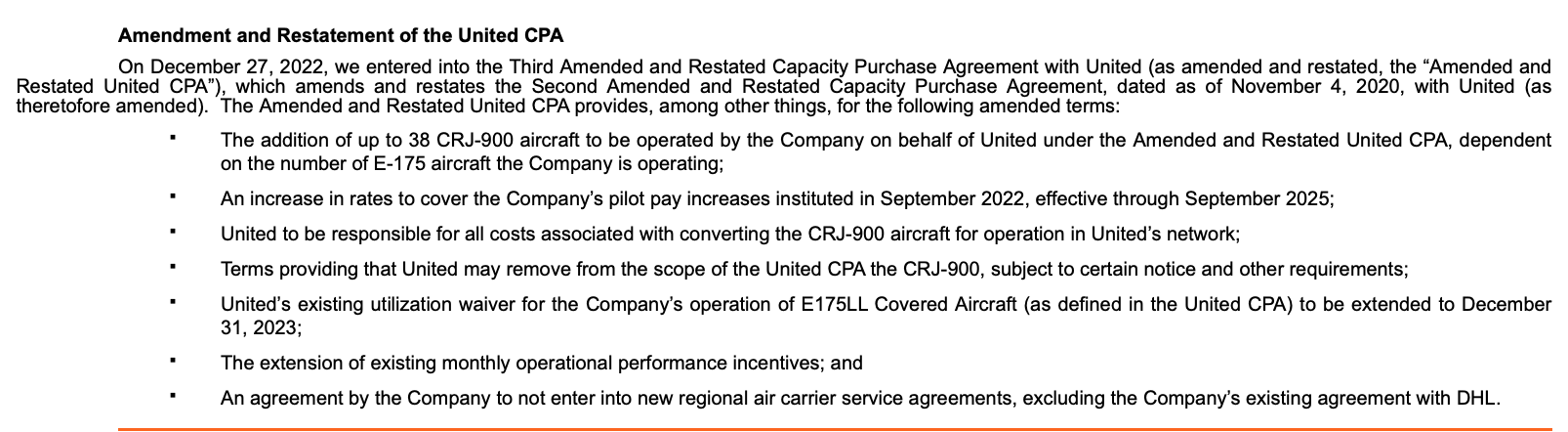

2) They ended their long term relationship with American Airlines.

America made it clear that they didn't value the relationship by enforcing the penalties and by their unwillingness to reimburse at the higher pilot wages despite the fact that American's own regional pilots signed a new and lucrative union deal. Enclosed below are the details. Importantly, Mesa will mostly be finished flying for American Eagle, by March 2023. Also, if I'm reading the fine print correctly, it doesn't appear that American will pursue any breakage fees or additional penalties.

{kind=link}

3) United really stepped up to the plate and saved Mesa.

United agreed to pay Mesa at the new ALPA wage scale, to take on the additional capacity, from the soon to be former American Eagle fleet, and to pay the cost to modify them to match United Express' planes. The only thing Mesa had to do was agree not to embark on any other or new CPAs. The only exception is that its existing DHL relationship, which is only 3 Boeing 737-400 planes currently, can continue.

{kind=link}

4) From a balance sheet perspective, Mesa dramatically increased its liquidity, and paid down debt.

Here are the actions that they took:

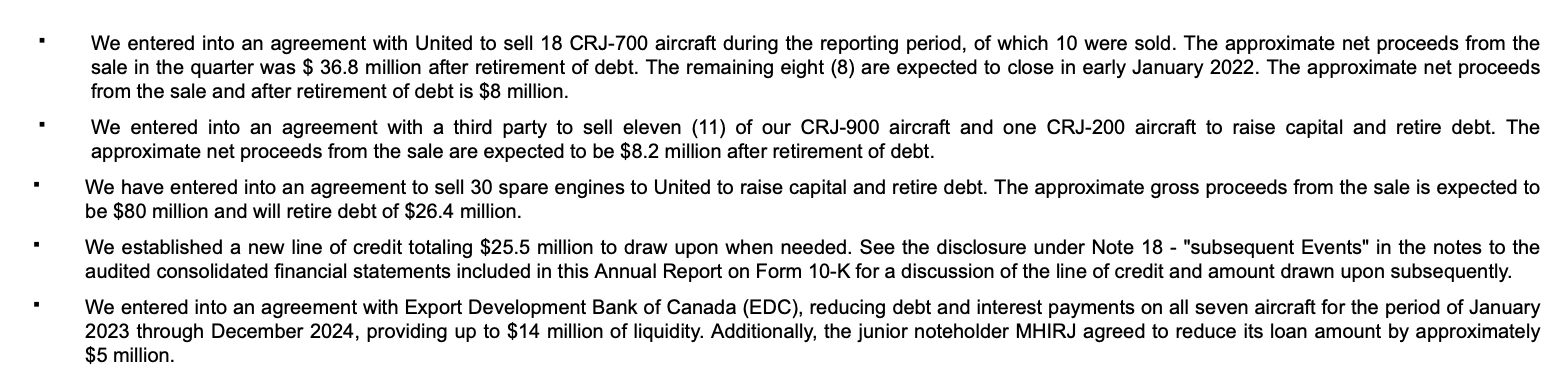

- They sold 18 CRJ-700 planes. 10 were already sold, yielding $36.8 million cash over and above the collateralized debt, which was retired. And the remaining eight planes will yield $8 million, net of debt tied to them as collateral, by January 2023.

- Entered into an agreement to sell 11 CRJ-900 plans to raise $8.2 million net of debt.

- Entered into an agreement with United to sell 30 spare engines that will results in $80 million of proceeds. Specifically, after $26.4 million of debt is retired, Mesa will net $53.6 million of cash proceeds that can used for working capital and debt repayment. And they still own 20 spare engines that could be sold as an additional liquidity source.

- Established $25.5 million credit line for working capital

- Negotiated reductions in debt tied to operating leases with other financial partners.

{kind=link}

See below, from Mesa's Q4 FY 2022 conference call:

Additionally, we have completed a number of transactions to strengthen our capital structure. In mid-December, we renegotiated improved terms and conditions with EDC, Export Development Bank Canada on debt associated with 7 next-gen CRJ-900 aircraft, reducing debt service by approximately $14 million from January 2023 to December 2024. The junior noteholder, Mitsubishi, has also agreed to forgive 50% of the outstanding note balance or approximately $4.2 million if the notes are fully repaid prior to December 31, 2023.

Additionally, we negotiated an agreement with RASPRO, a Canadian special-purpose finance company on our leases of 15 CRJ-900 aircraft, which reduces the effect of purchase price at or prior to March 2024 lease termination by approximately $25 million. Concurrently, Mesa plans on closing on the sales of the remaining 8 CRJ-550s to United in January 2023; and 11 surplus CRJ-900s to a third party, resulting in net cash proceeds of $16.2 million. These sales are expected to reduce Mesa's U.S. treasury debt by approximately $65 million and reduce annual interest expense by approximately $4.5 million at current rates.

And get this... which is very bullish for the equity: (Debt moves from $599.7 million (9/30/22) to pro-forma $435 million (9/30/23)!!

Total debt at the end of the quarter was $599.7 million, down $36.3 million from the prior quarter. During the quarter, we made scheduled debt payments of $42.9 million. Most importantly, combined, our sales transactions will reduce debt by $84 million by as early as March 2023. We also have $80 million of scheduled principal payments in 2023 resulting in projected end of fiscal year '23 debt of approximately $435 million.

Putting It All Together

As of August 2022, Mesa hadn't yet reached a new labor agreement with its pilot union. The company had north of $600 million of debt and was losing its pilot workforce left and right, as they were getting picked off by competitors. Since then, as described in this piece, the money losing segment, at a rate of $5 million per month, specifically, the CPA deal with American winds down in less than 3 months. Moreover, the updated United CPA dramatically improves Mesa's outlook, as United stepped up to the plate, and agreed to Mesa's new union terms (Win-Win), and provided them with more liquidity. Mesa sold older aircraft, and paid down debt and raised some modest and incremental cash to shore up its balance sheet and be in a position to make its FY 2023 principal payments.

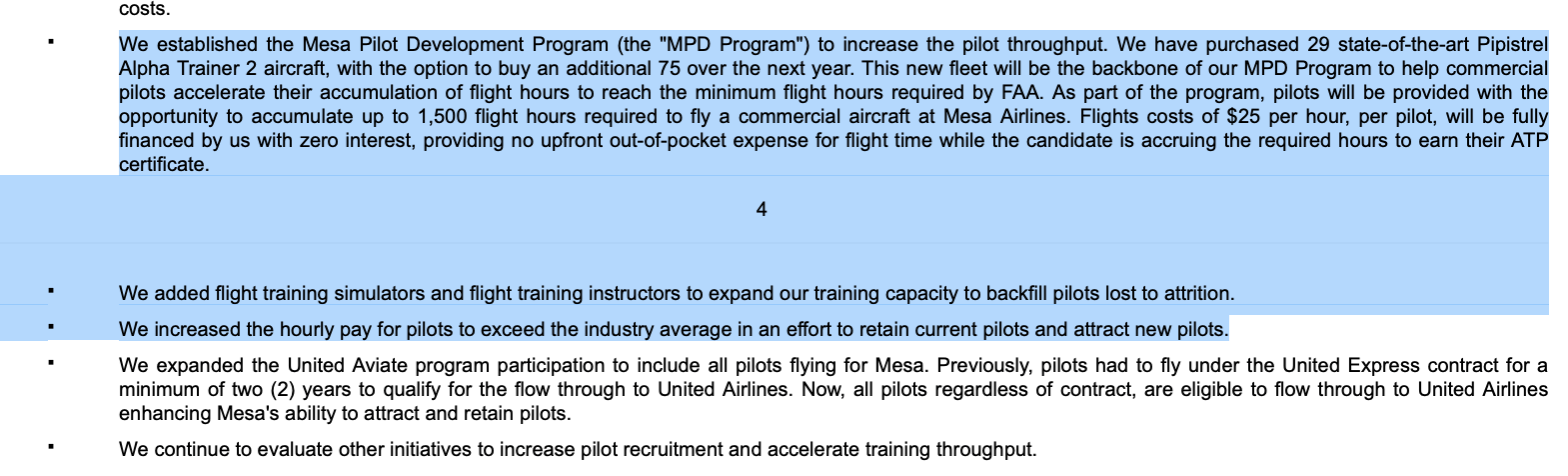

From an operating standpoint, the company has hired a number of new instructors, and made investments in new flight simulators and new equipment such that new pilots, and they have a pipeline of 400 recruits, are able to get their training and get certified (get their wings).

{kind=link}

If you take a step back, and Jon Ornstein discussed this or alluded to its on recent calls, United really values its relationship with Mesa. United views Mesa as a critical partner and thinks of this as a WIN-WIN partnership. From United's view, they are dramatically adding capacity to its network, as the underlying demand is robust, and they view Mesa as its farm team, where pilots fly regionally, with Mesa, for a few years before getting called up to the big leagues, so to speak, and get the chance to make more money, over the course of a career.

From a valuation perspective, Mesa only has 36.4 million shares outstanding. United is taking a 10% equity stake, as part of its series of recent agreements. So we are talking about 41 million pro-forma diluted shares.

If you take a step back, Mesa's equity has moved from say $1.50 (as the trough low of $1.05 was related to the delayed 10-K filing and fear of not getting an audited auditor's opinion, think going concern) to $2.50. This a lot in percentage terms, but very small from a market capitalization perspective, as it doesn't really change the total enterprise value.

I would argue Mesa's earnings profile will dramatically reset and get back on track, by the second half FY 2023. Management is calling for an ending debt balance, ending September 30, 2023, to get to $435 million, or down over $200 million from its high water-mark, this past summer.

In closing, from an enterprise value perspective, I don't think the market is coming anywhere close to fully appreciating that the overall enterprise value, from the summer of 2022, to pro-forma March 2023, after the debt repayments is actually lower. If Mesa does a good job of getting those 400 potential pilots (pilot in training) successfully trained and up in the air, there is exceptional demand for Mesa's service. Mesa's block hours will increase markedly and its positive business operating leverage will kick in.

My back of the envelope price target is $4.

Archives:

{kind=link}

Also, I have a 5% sized long position, at $2.24, as I averaged up.

{kind=link}

For further details see:

Mesa Air Group: Get Ready For Another Leg Up