MESA - Mesa Air Group: High Risk Buy Opportunity

Summary

- Mesa Air Group surged after United Airlines deal.

- Operational performance should improve significantly as attrition eased.

- Mesa Air Group increased liquidity, but its outstanding debt remains high.

- Improved performance and acceleration in debt repayment provides a high-risk, high-reward opportunity.

In a recent report, I discussed Mesa Air Group ( MESA ) ending its capacity purchase agreement with American Airlines ( AAL ) in favor of an agreement with United Airlines ( UAL ). As a result, the company decided to postpone the release of its fourth quarter results, which put share prices under pressure. The report was ultimately filed a couple of days ago along with an earnings call that I listened to. So, it is time to look at those results but more importantly how Mesa Air Group is restructuring.

How Did Mesa Air Group Stock Perform?

In June 2022, I covered Mesa Air Group for the first time and concluded that while the business case for regional airlines is quite appealing in an undisturbed market, shares of Mesa Air Group were not a gem as the market was in fact disturbed by widespread pilot shortages. That call, while almost a no-brainer, was correct as shares have shed nearly 35% of their value since I wrote the report compared to the broader markets gaining little over 1%.

So, share price performance has not been great. Shares were already on a downtrend, but it got worse in mid-December when the airline announced it would be postponing the fourth quarter and full year earnings release. The cause of the further drop was that the market feared that Mesa Air Group was in financial distress that would affect its continuity going forward. In fact, Mesa Air Group delayed its earnings release as it was working with United Airlines on an amended capacity purchase agreement while winding down its business with American Airlines, which had become a loss-making agreement for Mesa Air Group. From the point of announcing the postponement until the capacity agreement was finalized, shares shed 27.4% so the way Mesa Air Group handled things definitely was not good for the company’s stock price.

I did not provide a sell rating for Mesa Air Group despite not being charmed by the way they handled things, but did note that the pop we initially saw on the announcement of a to-be-finalized agreement with United Airlines would fade as the company provided little useful information supporting a reversal and that did happen. The reversal, however, did happen once the agreement was finalized and shares gained 44.3% to date. So, holding shares was the right call and it would have been.

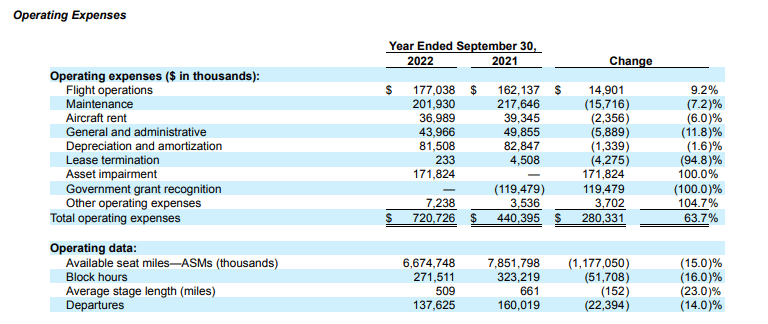

Mesa Air Group Results Continued To Slide

In Q3 2022, Mesa Air Group reported revenues of $134.4 million and adjusted EBITDA of $20.1 and million and an adjusted loss of $8.7 million. For the fourth quarter, revenues of $125.6 million declined by another 6.5% sequentially and 3.9% year-over-year. Adjusted EBITDA was $13.8 million marking a 31% decrease quarter-over-quarter and a 46.5% reduction year-over-year and an adjusted net loss of $13.5 million which was 55% higher quarter-over-quarter and 6.4x the net loss in Q4 2021. So, the fourth quarter was worse on all metrics driven by lower block hours execution.

{kind=link}

While it seems that things completely fell apart for Mesa in terms of revenues, this was not the case when looking at the full year. While block hour execution was 16% lower, operating revenues were up 5.4%.

{kind=link}

What hurt the airline was flat top line also driven by penalties from American Airlines for Mesa’s inability to operate the contracted capacity while costs rose significantly. Even when adjusting for the government grant recognition, costs rose 28.7%. Factoring out the asset impairment this year, costs rose by 2%. You could really wonder what the big issue is here because looking at operating expenses and revenues for the year, we see no big issues. That is because the full year numbers do not quite reflect the annualized effect of a continued worsening operational environment for the regional jet airline. So, Mesa had to step in to stop the bleeding and they did that by restructuring before the pains would become visible on annual basis more dominantly.

Why Mesa Switched From American Airlines To United Airlines?

While I would have liked to be able to present an overview of the costs related to the American Airlines operations the non-liner non-performance for the American Airlines operations with no quarterly visibility on the revenue split between American Airlines and United Airlines operations by Mesa does not allows us to do so. What we do know is that over the last few quarters losses on the operations for American Airlines were $5 million per month and that pushed Mesa into a loss position on adjusted level. So, pulling out of that agreement makes sense, but it was also driven by the fact that under the capacity purchase agreement, American Airlines had the right to reduce the number of aircraft part of the agreement if Mesa could not live up to the contractual agreement which was certainly the case and if that non-performance was of structural nature occurring multiple months in a row it gave American Airlines the space to pull out of the agreement which it did.

At the same time, I can imagine that Mesa Air Group did not feel it was treated well as a partner by American Airlines as the airline disrupted the market by increasing pilot pay at its fully owned regional airlines, which did lead to significant attrition while American Airlines was not willing to match the pilot pay at Mesa Air Group. In fact, because of the attrition Mesa was unable to execute its contracted capacity and was punished by this for American Airlines. So, that was a death spiral for Mesa Air Group.

What made an agreement with United Airlines attractive are the following items:

- United Airlines would pay to match increased pilot pay.

- United Airlines would pay for the reconfiguration of the CRJ-900 aircraft.

- United Airlines would provide Mesa with a liquidity injection in various ways.

- Operations under the United Airlines CPA is profitable.

How Does Mesa Pay Its Debts?

By June 2022, Mesa’s long-term debt stood at $523.2 million with $112.8 million in long-term debt maturing in twelve months with cash and cash equivalents at $54.4 million and that also provides some background on what was really bothering Mesa Air Group. The company simply did not have enough cash on hands to fund its debt obligations and the operational environment was not such that this would change any time soon.

By the end of the fiscal year, cash and cash equivalents increased to $57.7 million while long-term debt decreased to $502.5 million, and the current portion of the long-term debt decreased to $97.2 million reflecting several actions taken to reduce debt and improve liquidity.

To achieve this, Mesa Air Group engaged in several transactions:

- United Airlines bought 10 CRJ-700s for which the debt was retired and brought in $36.8 million.

- Another eight aircraft will be sold in January 2023, bringing another $8 million in proceeds after debt retirement.

- United Airlines will buy 30 spare engines for $80 million with $26.4 million of associated debt to be retired bringing the net proceeds to $53.6 million.

- United Airlines provided $41.2 million in liquidity.

- Eleven CRJ-900s and one CRJ-200 were sold bringing in $8.2 million after debt retirement.

- Debt and interest payment for 7 aircraft were lowered for the next year providing $14 million in liquidity tailwind next year and $5 million in loans were forgiven.

- With RASPRO, Mesa Air Group agreed to lower buyout pricing giving the airlines a lower purchase price for the aircraft once the lease is terminated.

So, what we see is that Mesa Air Group took the rather undesired approach of shaving off assets in order to fund its debt obligations. For next year, we do see that Mesa has some liquidity arrangements in place to retire more debt. The company also has another 20 spare engines which it can use to raise liquidity. With around $600 million of debt still to be repaid we do see a positive and a negative. The positive is with debt being retired, the associated interest payments are extinguished as well, providing the company with more cash to accelerate debt repayment. The negative is that from free cash flow perspective, Mesa Air Group is not quite a money machine which makes me wonder for how long they will actually have to keep selling engines and aircraft to met debt obligations. Some savings on interest payments can be applied on debt repayment which can ultimately snowball, but it will require Mesa Air Group to do better in terms of operations else what the company saves on interest will be spent on operations.

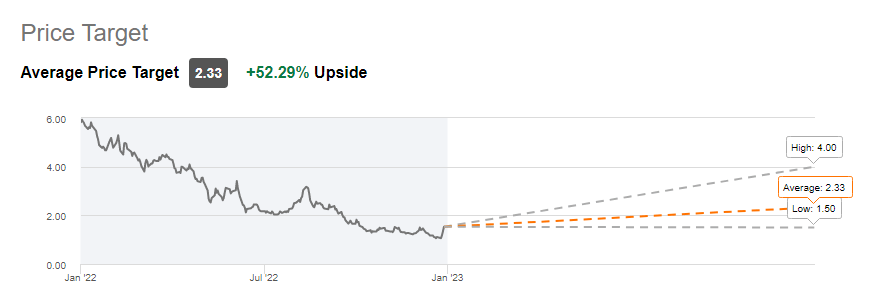

Wall Street Thinks Mesa Continues To Be A Buy

{kind=link}

I am not particularly convinced by Mesa’s actions to put a buy rating on it. Does it mean there is no improvement or upside? No. There most certainly is, but the risk profile simply does not appeal to me. Wall Street analysts believe Mesa could be heading 52.3% higher and that could indeed be true. If they execute perfectly, we will see Mesa shares fly higher again but any investor should be mindful about the fact that this is a high risk, high reward kind of thing.

In terms of operations, we see some bright spots. Six months ago, Mesa had 200 pilots in the training pipeline. Today that number has already doubled. A more competitive pilot agreement has been put in place, which United Airlines will support, which significantly reduced attrition. This means that as Mesa rotates out of the American Airlines agreement it should also see start to see block hours improve as more pilots are coming in. Mesa provides a more predictable path for pilots to leave Mesa and become a mainline pilot and that helps the company keeping the pipeline filled and reducing unexpected attrition, both of which should improve performance.

Conclusion: Mesa Air Group Stock Is High Risk, High Reward

In recent days, Mesa stock has shown that it can be extremely rewarding but I would say that this is a potential high risk, high reward play as Mesa has significant debt and its cash from operations is not extremely strong. So, we will see Mesa reducing some of its assets to pay down the debt and from there lower interest payments should help the company bring down the debt even further, but it needs a very smooth 2023 and 2024 for that and if there was anything that Mesa was missing over the past twelve months it was smooth operations. So, that provides both the risk as well as the opportunity in Mesa stock.

For further details see:

Mesa Air Group: High Risk Buy Opportunity