MLAB - Mesa Laboratories: No Economic Earnings At 18x EBIT Is A Tough Ask

2023-06-08 01:47:11 ET

Summary

- Mesa Laboratories' FY'22 results show a decline in revenues and profitability, leading to a hold rating on the stock.

- Despite growth opportunities in the clinical genomics segment, the company's lack of economic earnings and expensive valuations make it a less attractive investment.

- MLAB is potentially overvalued, trading at 16x forward earnings and 18x forward EBIT, with further downsides in profitability expected in the next 2-3 years.

Investment Summary

In December 2021, investors in Mesa Laboratories, Inc. ( MLAB ) equity stock copped a bat to the face. After a decade-long rally, investors unloaded shares ad infinitum, to instigate an 18-month long correction. In my last report, I had continued my hold rating on the name after the 4th review (see it here, all other MLAB publications here ).

The company's FY'22 numbers had potential to paint a new mural on the market's wall however as you'll see here today, this wasn't to be the case. With the company reporting just last week it is fruitful to revisit the investment thesis and plan for my clients accordingly. With the selloff, there's chatter on whether or not MLAB is worth a look or not. Well, I can tell you, at 18x forward EBIT, that's not the case, and in my view the market is still overly optimistic on MLAM's prospects even at the current market valuation.

Net-net, the lagging returns on incremental capital, lack of economic earnings and expensive valuations are 3 critical factors that see me retain a hold rating on MLAB for the coming months. I believe more data is required to determine whether it can throw off meaningful piles of cash to its shareholders. Looking forward, my estimates suggest this could be a challenge, and that more selective opportunities are available elsewhere. Reiterate hold.

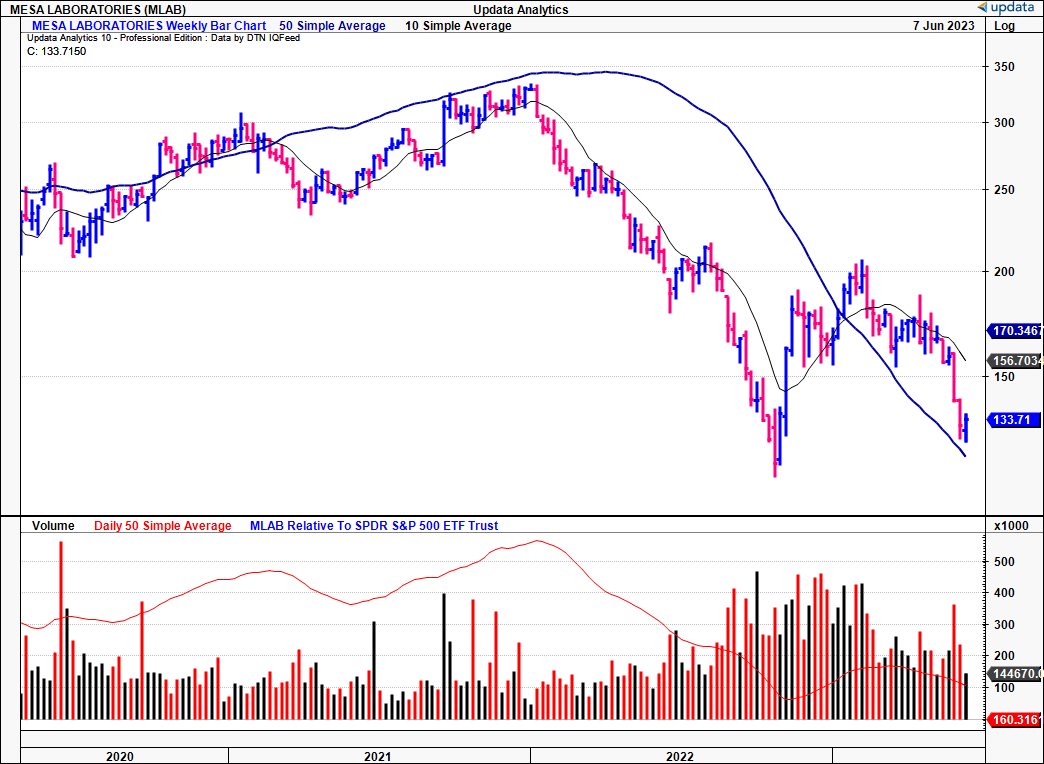

Figure 1. MLAB 3-year price performance

{kind=link}

A year of growth challenges

MLAB had one of its less profitable years in FY'22 . First looking to Q4, it booked quarterly revenues of $55.5mm, a 5.6% decline to the core business. This decline can be attributed to several factors- adverse currency effects, reduced biopharma spending, and a significant decrease in COVID-related revenues [in fact, the bolus of downsides stemmed from this same point, not unlike the bulk of its peers]. For the year, MLAB clipped $219mm in top-line revenues, a tidy 18% growth route on $37mm core EBITDA and $0.9mm in total earnings.

Based on the information provided, 3 critical facts emerge:

- Despite the decline in reported revenues, ex-Covid, MLAB's core organic revenues grew by 5.2% for the full fiscal year, indicating the company's ability to expand in '24. FY'23 would mark the year when most companies absolve their Covid-19 revenues as well, so the core business trends are noted here.

- The closure of Sema4's expanded carrier screening business had a significant impact on the MLAB's clinical genomics ("CG") division. This flowed through to hurt profitability and free cash flow. Specifically, it booked 61% gross and 19% adj. operating margin, including $10.7mm in Q4 operating income, $45.8mm for the year. However, excluding this impact, the division did another 10% extra business for the quarter and 15% for the year. To me this says MLAB still has plenty of adjacent opportunities for organic expansion, so you'd want to its CG segment closely going forward to see how it rebounds - it may be an upside surprise.

- Gross profitability was a standout both on margin and scaled related to total operating assets (discussed later). All of this was driven by a more favourable product mix and reduced raw material costs, indicating the potential for future margin expansion in my view.

Segment Analysis:

It is apparent by now the impact of declining Covid-19 related sales to MLAB's divisional performance. Including all extraordinary and reported items, the portfolio was heavily weighed down by the underperformance of the CG business, noted in Figure 2.

Figure 2.

Note: All dollar [ "$" ] figures are shown in [ $000' ] format. (Data: Author, MLAB 10-K)

Turning to the specific divisional highlights, my analysis found the following:

- Q4 CG revenues came to $13.77mm, resulting in an organic decline of 12.9%. As mentioned, the decline was primarily the result of the closure of Sema4's expanded carrier screening business. Excluding this, core organic growth would have been ~10% for the quarter and ~15% for the year.

- The sterilization and disinfection control ("SDC") division turned a 3.5% growth in fourth-quarter revenues, reaching $16.5mm. This pulls to 12.2% annually. Notably, annual growth was underscored by gains made from the firm's biopharmaceutical verticals. FX had a 200bps headwind to gross margin.

- Quarterly revenues for the biopharmaceutical development ("BD") segment pulled to $12.6mm, yielding decline of 6.2% YoY due the high comps period in 2021. However, underlying business growth was strong, with BD core turnover up 10.9% driven by demand (volume) and pricing. As such it booked a 240bps and 130bps decompression in Q4 and FY'22 BD gross margin respectively.

- Revenues for the Calibration Solutions division in the fourth quarter were $12.6mm, down 360bps YoY. MLAB is building momentum here as sales were up 17% sequentially, so you saw 450bps margin liftoff in Q4 and another 110bps added to gross margin for the year.

Critical facts

A more thoughtful analysis beyond the company's financial results is required to gauge the investment value. Profitability has been a concern for MLAB stockholders, who are currently treated with a 0.24% trailing return on their equity and 0.32x turnover on assets.

From the annual results, there are two factors that warrant critical discussion:

-

The softness in new systems orders and CapEx

-

MLAB observed softness in new systems and CapEx orders for both its CG and BD divisions, confirmed by management's language in the 10-K.

-

It is difficult to immediately say, but he weakness may be indicative of broader industry trends, with higher capital charges and significant pullback in capital spending from healthcare/laboratory service providers. I'll be watching closely moving forward.

-

-

Growth opportunities in its CG markets

-

The core business trends in its CG division are worth noting. Management are optimistic about growth opportunities now that Covid-19 is behind us. Given this and the SDC segment makes up the bulk of MLAB's turnover, it needs a major reversal in profits generated by its CG business this year. In my view, the company's performance hinges on that point in FY'23.

-

Both factors related back to the firm's usage of capital in order to make investments for future growth. From FY'20-'22, this was somewhat of a challenging exercise for MLAB.

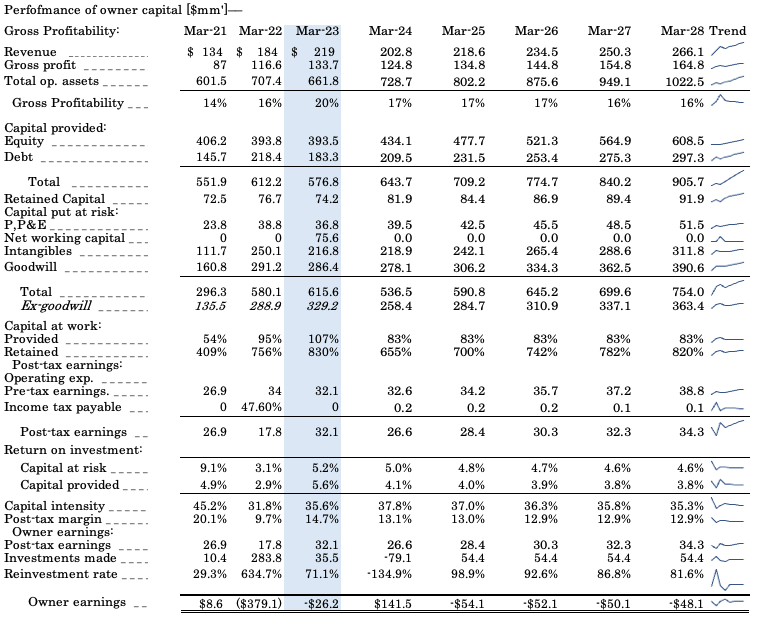

Let me illustrate. Given a firm is simply a conduit between its investors and the equity/assets tied up in the business, a report showcasing the performance of MLAB's owners' capital is shown in Figure 3.

Gross capital productivity, treated as the gross profit scaled by total assets, managed another 400bps on FY'21 to produce $0.20 on the dollar. But it's down from $0.39 in FY'19, hardly the result required to attract investment. Further, investors had provided $576mm to the firm, to which it had put 107% of this to work (the firm's $0.64/share annual dividend isn't included in this report, but is worth mentioning).

Alas, for their efforts, investors were rewarded with quite paltry returns on the capital they have tied up in the business in FY'22 - 5.2% rate of return, or $32mm in post-tax earnings. Incrementally, this is up $14mm or 80% YoY, but just $5.2mm from FY'21.

Figure 3.

Note: Dates are shown on earnings release dates. Each March period corresponds with December of the previous year. (Data: Author, MLAB 10-K's)

Critically, over the 2020-'22 period, the firm did not produce economic earnings above the opportunity cost of capital (in this case, I've labelled it 12% for the long-term market averages). This is a problem in my eyes, because in order to attract investment, the firm must be economically profitable. That is, producing a return on its investments above what investors could generally achieve elsewhere.

The lack of economic earnings have seen substantial gains in market valuation been wiped from MLAB's equity value these past 2-years. At a time when investors were searching for the highest quality business models (i.e., profitability), MLAB missed the boat and was left stranded on the shores of the selloff coast. Investors weren't to pay a higher multiple for 4-5% ROIC when the risk-free rate was approaching a 5 handle.

Furthermore, detailed analysis of the company's value-creation to date is telling. The differential in capital allocation to the growth in owner earnings is hurtful to investors, evidenced by the following record:

Data: Author, MLAB 10-K's

Despite an additional $545mm investment since FY'13 ($545mm equivalent) the firm's stockholders have incurred an $835mm deficit on their earnings. Moreover, the annual compound rate on its incremental capital is just 7.8%, below that 12% hurdle rate specified earlier. Note the large rolloff in ROIC from 2019-date.

Alas, it is investing 24% at 7.8% turn. It is no wonder that investors have overlooked MLAB in the latest of 2 rallies since October last year. In my view, the firm's lack of economic earnings suggest it will have a hard time creating value for shareholders down the line, discussed later.

Valuation and conclusion

With the company now priced at 16x forward earnings and 18x forward EBIT the question of mispricing is out of the question in my opinion.

For one, these are basically in-line with the sector multiples. Two, if you are paying 18x, you'd expect tremendous earnings growth from MLAB going forward, and I'm just not seeing it. My numbers have the firm doing $26mm in post-tax earnings this year, stretching to $28mm in FY'24 [see: Appendix 1], both declines on the FY'22 results. Three, taking an expectations-based approach reveals discrepancies in the market's projections to my own.

Specifically:

- At the current market valuation of $714mm, and considering a 12% discount rate, the market values the company's future free cash flows at $85.69mm ($85.69/0.12 = $714mm). I have assumed this over a 5-year horizon.

- Over the same horizon, my forward estimates pull to $76.8mm at the same hurdle rate, a 10.4% discrepancy to the market consensus.

On these forward assumptions [also noted in Appendix 1] this would imply MLAB is overvalued in my opinion:

Figure 4.

Note: Future cash flows determined via net present value with 12% rate and internal FCF estimates. (Data: Author Estimates)

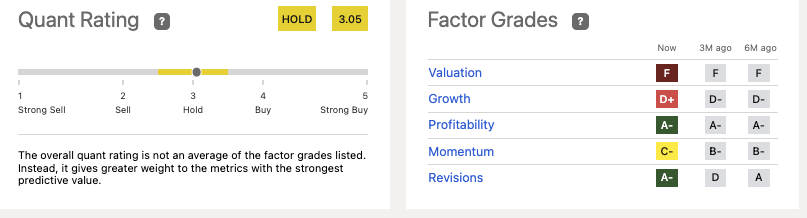

These findings are well supported by findings in the quant grading system , that also suggests MLAB is rated poorly on valuation and growth, two factors I also have uncovered. In that vein, a hold rating is well supported in this instance.

Figure 5.

{kind=link}

In short, the economic characteristics of MLAB's business make it hard to advocate adding its stock to the long account. There are features worth noting that suggest it isn't a short, either. Net-net, the lackluster returns on capital have put the company in a tight space, and investors aren't expecting much from the firm in FY'23. This is evidenced by the sharp selloff in equity this year, coupled with the very pricey multiples that aren't attracting strong hands at this point in time. My numbers point to further downsides in profitability in the next 2-3 years, something I can't advocate my clients to position against. Net-net, reiterate hold.

Appendix 1. MLAB forward estimates, FY'23-'28

{kind=link}

For further details see:

Mesa Laboratories: No Economic Earnings At 18x EBIT Is A Tough Ask