AEM - Metalla Royalty & Streaming: Don't Chase The Stock Here

2023-04-17 05:43:18 ET

Summary

- Metalla is one of the better performing royalty stocks since its Q3-22 lows, up 64% vs. a 10%, 31% and 20% gain for GROY, ELEMF, and SAND, respectively.

- I attribute this outperformance to MTA briefly becoming one of the most attractively valued names in the junior royalty/streaming space and positive developments for its royalty assets.

- However, MTA stock has now become extended short term above US$5.60, and I see the valuation as much less compelling, especially from a relative value standpoint.

- So, while I think Metalla has a solid portfolio and a solid organic growth profile, I don't see any way to justify paying up for the stock here near US$5.65.

2022 was a tough year for investors in the Gold Juniors Index ( GDXJ ), with sharp rallies being sold and several names ending the year deep in negative territory. The significant declines suffered sector-wide were not without reason, with AISC margins for the producer universe plunging over 30% on a two-year basis to ~$510/oz, and this not even factoring in a full year of inflationary pressures with H2-2022 costs worse than H1-2022. However, while the producers saw sharp declines in operating and free cash flow, the royalty/streaming companies had a solid year on balance, sheltered from the inflationary pressures on capital costs and operating costs because of their superior business models.

Unfortunately, the outperformance by the royalty/streaming companies with a (-) 7% average return (GDXJ [-] 15%) did not translate to Metalla Royalty & Streaming ( MTA ). In fact, Metalla Royalty & Streaming ("Metalla") was one of the worst performers with a 29% share price decline in 2022 despite easy comps after being one of the worst performing stocks in 2021 as well (45% decline). I attribute this poor performance to the stock's overvaluation, with Metalla being one of the few junior royalty/streaming stocks to enter 2022 trading well above 1.0x P/NAV. And while the stock was compelling below US$3.70 last fall, this is no longer the case after a ~65% rally off its lows. Let's take a look at its FY2022 results and recent developments below:

Metalla Royalty & Streaming (Company Presentation)

{kind=link}

FY2022 Results & Recent Deals

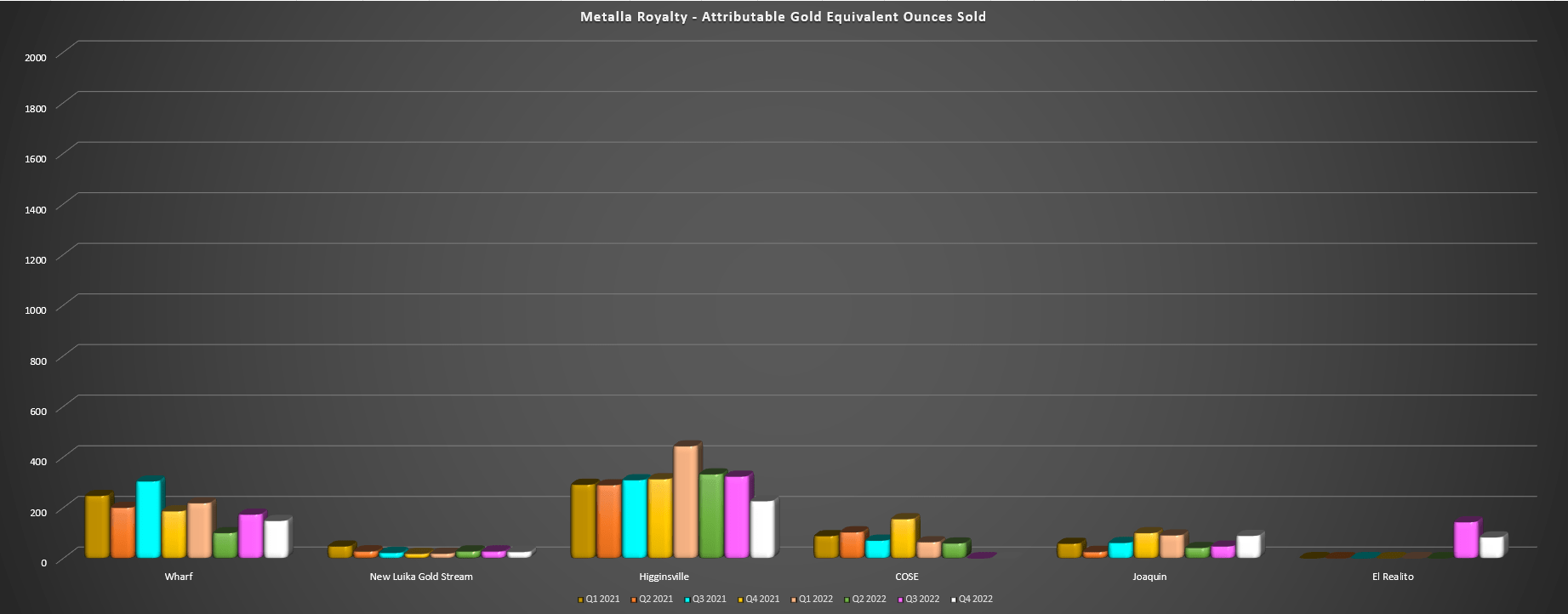

Metalla Royalty & Streaming released its Q4 & FY2022 results last month, reporting attributable volume of 2,681 gold-equivalent ounces [GEOs], an 8% decline from the year-ago period. The decline in attributable GEO production was related to a lower contribution from Higginsville and Wharf, a sharp decline in attributable production from COSE, and a slight decline in production from the New Luika Gold Stream. The two assets that did see increased contributions were El Realito (but this may not contribute for much more than two years in a material way) and Joaquin, which has since been placed on care & maintenance. Unfortunately, this will partially offset new contributions from El Realito, with the two assets contributing 391 GEOs in 2022.

Metalla - Quarterly GEOs by Mine (Company Filings, Author's Chart)

{kind=link}

From a financial standpoint, Q4 revenue came in at $0.63 million (down 28% year-over-year), and FY2022 revenue came in at $2.4 million, with an additional $2.4 million in payments from its Higginsville derivative royalty asset. This represented a sharp decline from a combined total (revenue and payments from Higginsville) of $5.2 million. This resulted in a net loss of $10.9 million (FY2021: $10.4 million) and adjusted EBITDA of [-] $1.5 million, a slight decline from [-] $1.5 million in FY2021. On the positive side, cash operating margins were industry-leading at $1,758/oz, up from $1,711/oz in the year-ago period helped by the higher gold price.

Looking ahead to 2023, it's not expected to be a much better year for Metalla financially, with attributable GEOs expected to come in at 2,500 to 3,500, suggesting ~12% growth at the mid-point of guidance. However, this will barely represent any growth on a two-year basis, with this growth coming after a year of easy comps given that attributable GEO volume declined by 8% last year. So, unless metals prices head significantly higher from current levels, I would expect to see another year with less than $7.0 million in annual revenue and contribution from its Higginsville royalty asset.

Finally, Metalla added several new royalties over the past few months, acquiring a royalty portfolio from First Majestic ( AG ) for 4.2 million shares that includes several royalties on silver assets in Mexico, and also acquiring a silver stream on the Esperanza Project and three early-stage royalties from Alamos Gold ( AGI ) for $5.0 million in shares or ~0.93 million shares. Finally, Metalla acquired a 2.75% - 3.75% sliding scale royalty on gold and a 0.25% - 3.0% NSR on all other metals (excluding gold and silver) on the Lama Project in Argentina. The result of these deals was just over 12% share dilution, with Metalla having ~56 million fully diluted shares as of the time of its most recently filed MD&A.

Recent Developments

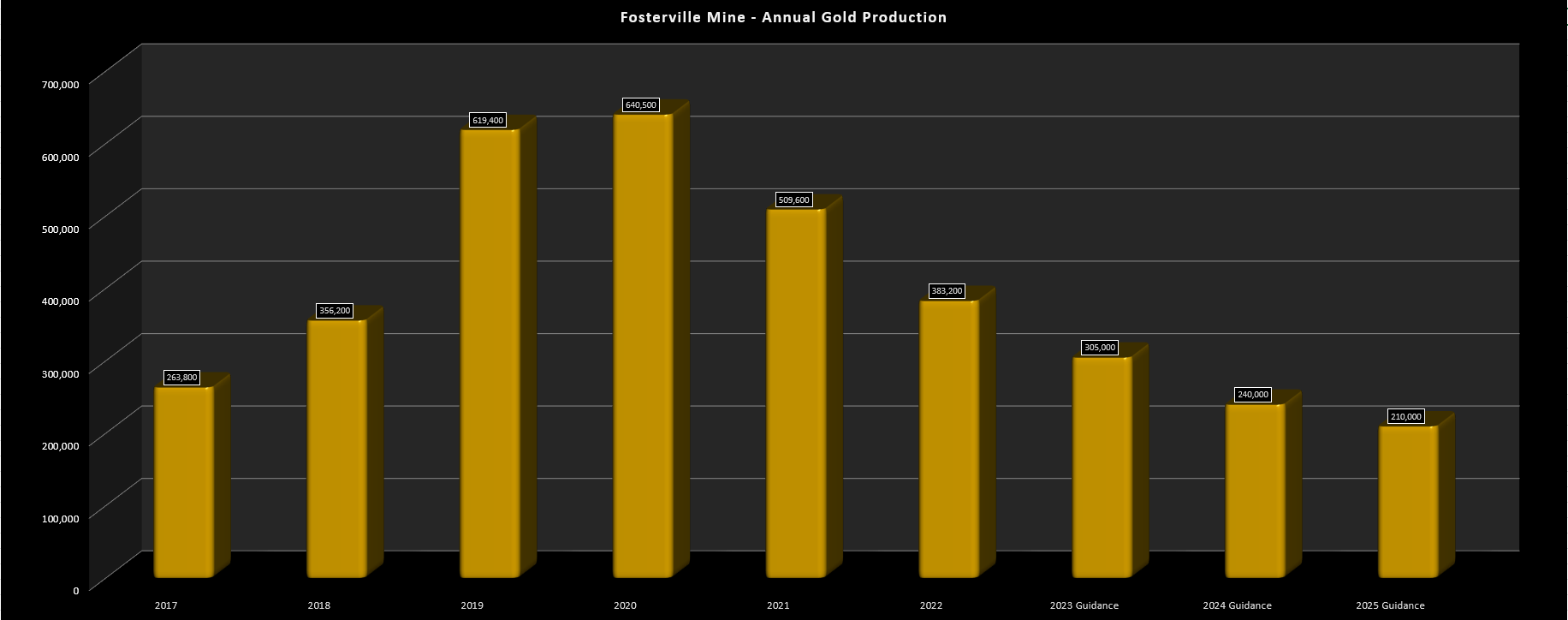

Moving over to recent developments, one negative development on a royalty asset that Metalla acquired in 2020 for ~$4.0 million is that Fosterville has become much less attractive from a production standpoint. Looking at the chart below, the guidance mid-point provided by Agnico Eagle ( AEM ) points to average three-year production (2023-2025) of 251,700 ounces, a significant decline from trailing three-year average production of 511,100 ounces. Much of this decline is related to grades given that the 1.0+ ounce per tonne ore at the Swan Zone wasn't going to last forever. However, it's also impacted by lower than planned mining rates because of operating constraints (surface fans unable to run from midnight to 6 AM due to low-level frequency noise).

Fosterville - Annual Production & Forward Guidance (Company Filings, Author's Chart)

{kind=link}

Unlike Triple Flag ( TFPM ), Metalla is not receiving attributable revenue from this asset currently given that its royalty coverage lies outside of areas with reserves. Therefore, Metalla investors might see this as a non-event. However, I would argue that this decline in production and the current operating constraints are a negative for its royalty asset given that lower mining rates impact economies of scale and it's quite clear that the challenges with the Environmental Protection Authority [EPA] of the Victoria Government are not going away. For those unfamiliar, this has been an issue since 2021 when Kirkland Lake Gold received a notice for investigation and improvement related to noise emanating from the mine.

This notice determined that the low-level frequency noise ( below the level of normal human hearing at 16-20 hertz) was being emitted by the Fosterville Mine and that " additional action may be taken by the EPA that could result in restrictions on the use of certain equipment, primary surface vent fans and surface drill rigs in the south portion of the mining lease. " Fifteen months later, Agnico is now dealing with these issues after the merger, despite two third-party noise consulting specialists in Australia concluding that the noise was within regulatory limits. Not only does this impact profitability at Fosterville with the company unable to mine at previous rates, but it could affect the company's decision to stay in the continent long-term if it's doing everything it can to appease regulators but still land at a reasonable agreement.

Even ahead of this news, Agnico's CEO Ammar Al-Joundi noted that the company is operating a much larger portfolio and that some assets could be considered non-core in countries where there's a much lower production profile (unless Agnico can find a way to add additional production in that region, given that it specializes in regional mining). So, with Agnico appearing a little frustrated, it may not see the same future for Fosterville that it did at the time of the acquisition if this isn't resolved in a timely manner. And while this doesn't impact Metalla's current financial results as it would Triple Flag, it does affect Metalla's potential future revenue if the company decides to reel in its exploration budget in 2024 if there's still no resolution.

While the operating constraints at Fosterville and a slight change in tone regarding the asset is disappointing and suggests that the $4.0 million investment that bet on extending mineralization outside of current mining areas may not deliver any time soon, Metalla has seen some positive developments, with Agnico confirming that Amalgamated Kirkland will likely represent a future spoke for its regional strategy along the Abitibi Gold Belt. Meanwhile, G Mining Ventures ( GMINF ) continues to make progress at Tocantinzinho, with the project fully-financed and detailed engineering being nearly 60% complete as of year-end. These two assets fit in the near term (1-5 year timeline), with a glimpse at future growth highlighted below:

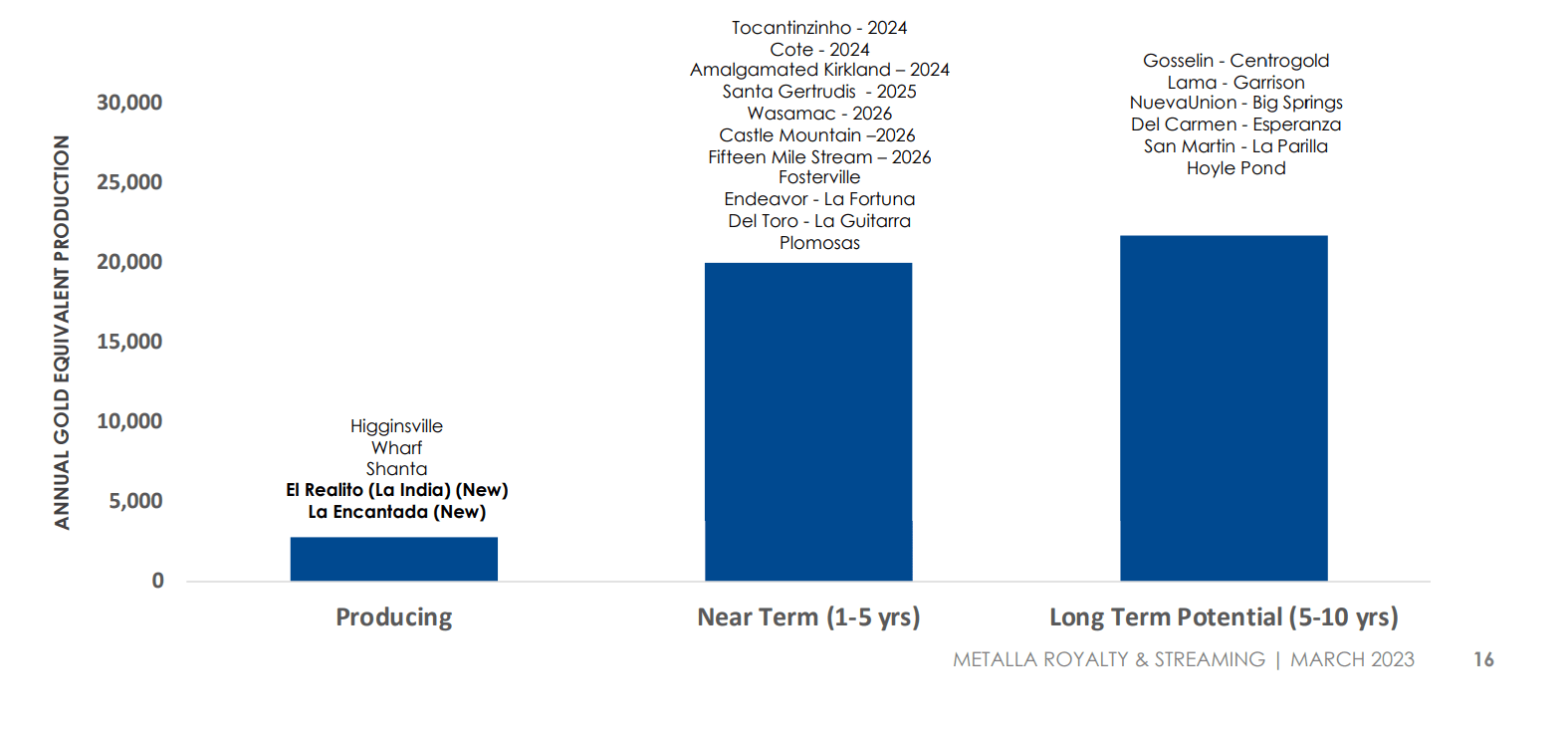

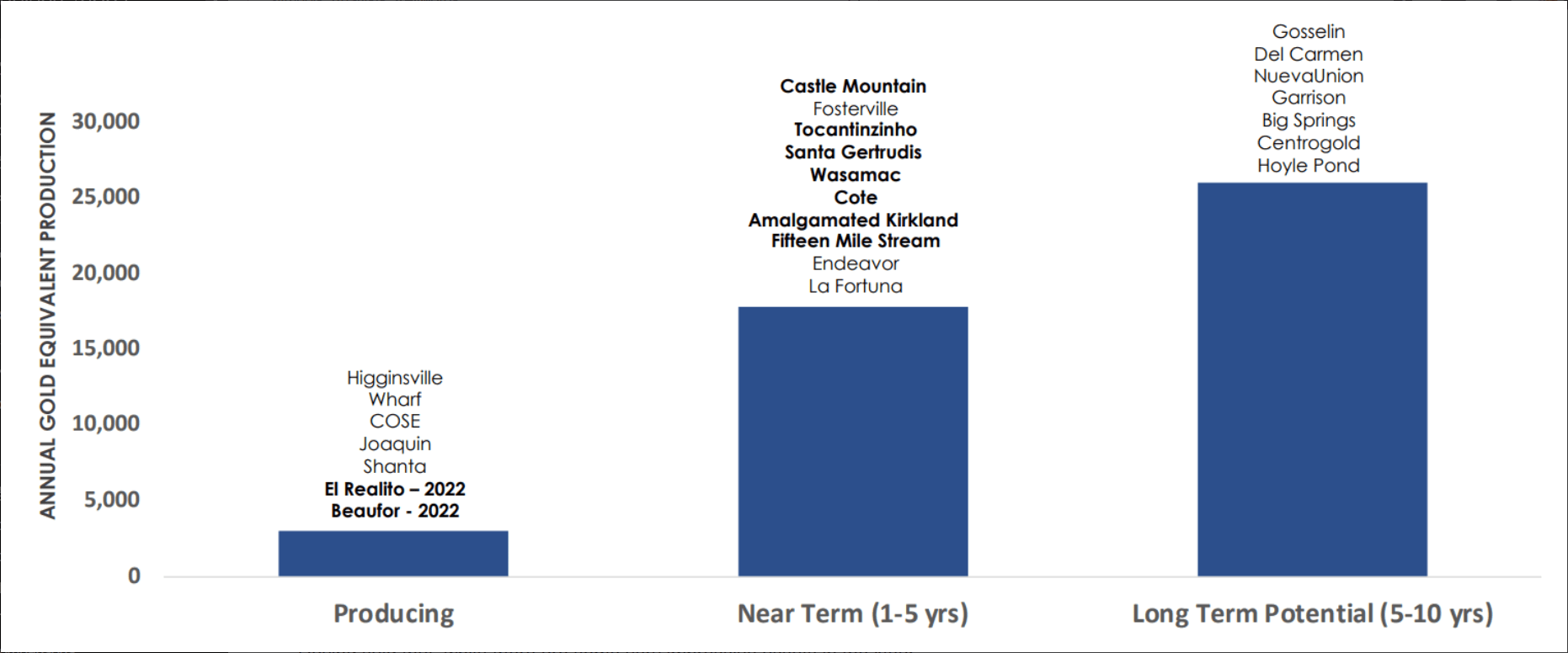

Future Growth & Timelines

Metalla - Future Growth Outlook (Company Presentation)

{kind=link}

Looking at Metalla's most recently provided growth outlook above, Metalla is forecasting significant growth over the next several years, with the potential for annual GEOs to climb to 20,000 GEOs or $38 million in revenue using a $1,900/oz gold price assumption. And while there is visibility to some of these assets coming online, like Cote and Tocantinzinho, which are getting close to the finish line, some of the other projections look quite aggressive. For example, there was minimal mention of Santa Gertrudis in the year-end results and annual report, with Agnico noting that it plans to spend a mere $7.3 million at the asset, which pales compared to ~$31.0 million that's expected to be spent at its other exploration project, Hope Bay.

According to Metalla's presentation, it expects contributions in 2025 from Santa Gertrudis, but I would argue that the outlook for Santa Gertrudis has weakened given that this is a ~125,000 ounce per annum asset which doesn't really move the needle for a company of Agnico's size. Prior to the Kirkland Lake Gold merger (when Agnico Eagle was a 2.0 million ounce producer), this looked like a high probability project post-2025. However, with two acquisitions since and a 50/50 joint-venture with Teck ( TECK ) at San Nicolás which looks like a more attractive asset in Mexico (high-margin with 200,000+ attributable GEOs per annum), I think Santa Gertrudis has taken a backseat to other projects. Hence, not only is it harder to assign much value to this project, but I think projecting attributable revenue in 2025 is a very aggressive assumption.

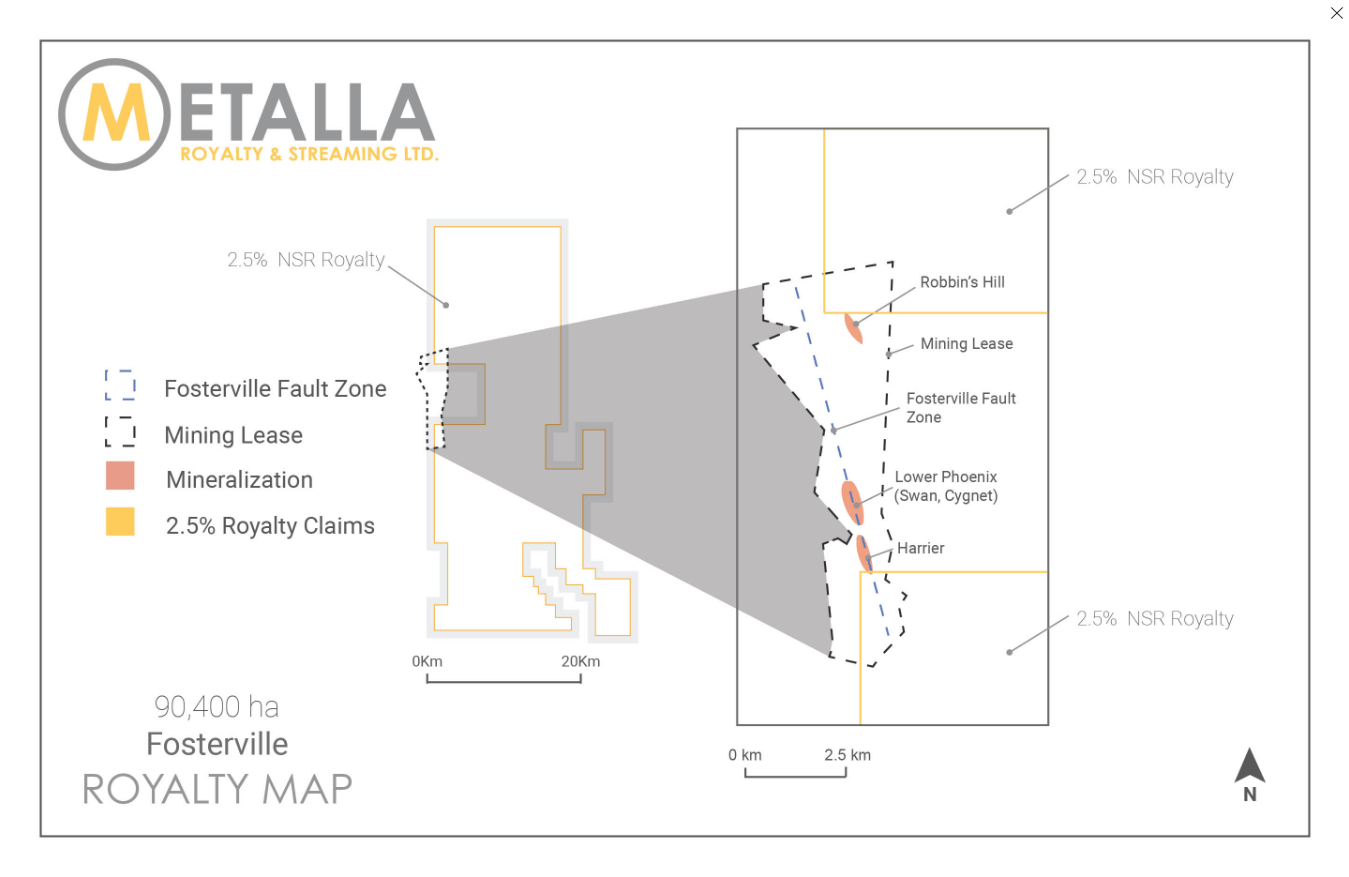

Meanwhile, and in line with the comments previously regarding challenges at Fosterville (lower grades as grades normalize at Fosterville plus lower mining rates because of directions from Victorian EPA), I have a less optimistic outlook regarding Fosterville remaining a core asset without these issues resolved in a timely manner. For Triple Flag, this isn't a huge issue as it's still receiving royalty revenue even if output has declined. However, Metalla's royalty coverage is south of Harrier and north of Robbins Hill ( not in current production areas), and if this is less of a core asset, I would expect exploration to focus on lower hanging fruit near current reserves and less on greenfield exploration (just $1.3 million budgeted in regional exploration for 2023) while it takes time to decide if this is still a core asset.

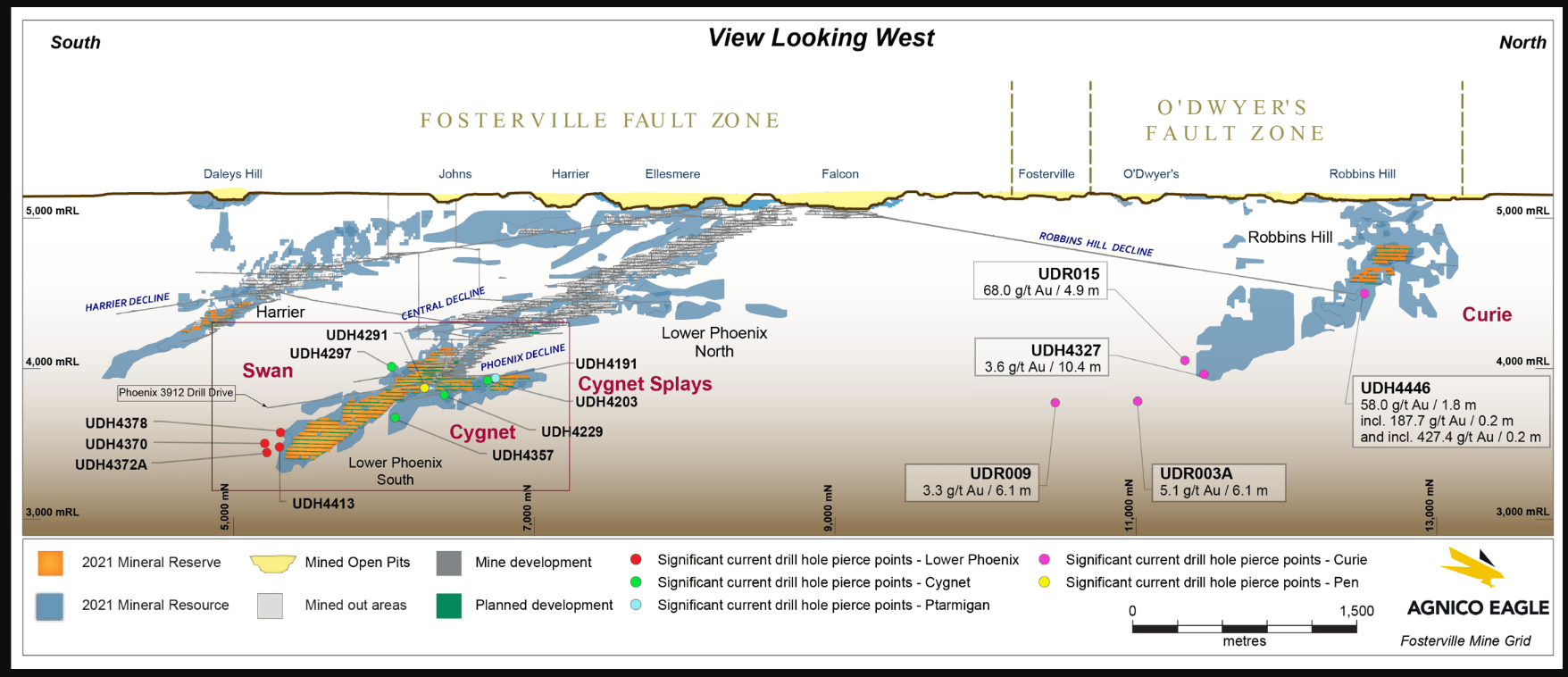

Metalla Royalty Coverage at Fosterville (Company Website) Fosterville - Exploration (Agnico Eagle Website)

{kind=link}

{kind=link}

Regarding recent drilling results, the bulk of high-grade hits and the recent focus has been at Lower Phoenix (Swan, Cygnet, Cygnet Splays) and less at Harrier, which does not favor Metalla given that Agnico will need to define reserves south of Harrier to benefit Metalla. Meanwhile, at Robbins Hill, the focus appears to be down-plunge and the best intercepts have been arriving at depth, with Agnico also focused on lateral extensions to the west. Given that Metalla's royalty coverage is in the opposite direction (north of Robbins Hill or to the right on the above map), this doesn't favor Metalla either, which will only benefit if Agnico Eagle adds reserves north of existing resources at Robbins Hill, not down-plunge and at depth beneath the historic O'Dwyer's Pit.

Metalla noted in its MD&A that it estimates the Metalla royalty boundary on the southern end of the mining license at Fosterville is 650-800 meters down-dip from recently reported results in the Lower Phoenix Zone.

So, between operating constraints, less exploration success than I expected, declining grades, and exploration at heading in the opposite direction at Robbins Hill and at Phoenix vs. Harrier, I am amazed that Metalla has Fosterville contributing in the "near-term" and I see these developments as a downgrade for the outlook for this royalty asset. Of course, the bigger downgrade would be on the off chance that Agnico decides to divest Fosterville, which it appears open to, given that it is not focused on an absolute ounce figure company-wide but on regional hubs delivering high-margin ounces. Fosterville is high-margin but it's less so with declining grades and impacted mining rates, but it's tough to justify staying in a separate continent for just over 200,000 ounces per annum.

Elsewhere, Metalla expects Wasamac to come online in 2026, and while this is a very solid asset that has a high likelihood of being developed, I think 2026 is a very aggressive timeline. This is because Agnico will likely take at least a year to better evaluate the project and I would be surprised to see full permits granted before H2-2025. This is especially true when Agnico now appears to be considering an adjustment to its permit application with the potential to increase mining rates to 9,000 tonnes per day (7,000 tonnes per day contemplated previously). With no real rush to develop Wasamac until 2028 when the Canadian Malartic Mill sees a significant increase in available capacity once open-pit operations are complete, I think H2-2027 is a more realistic bet.

Wasamac Drill Core (Agnico Eagle Website)

{kind=link}

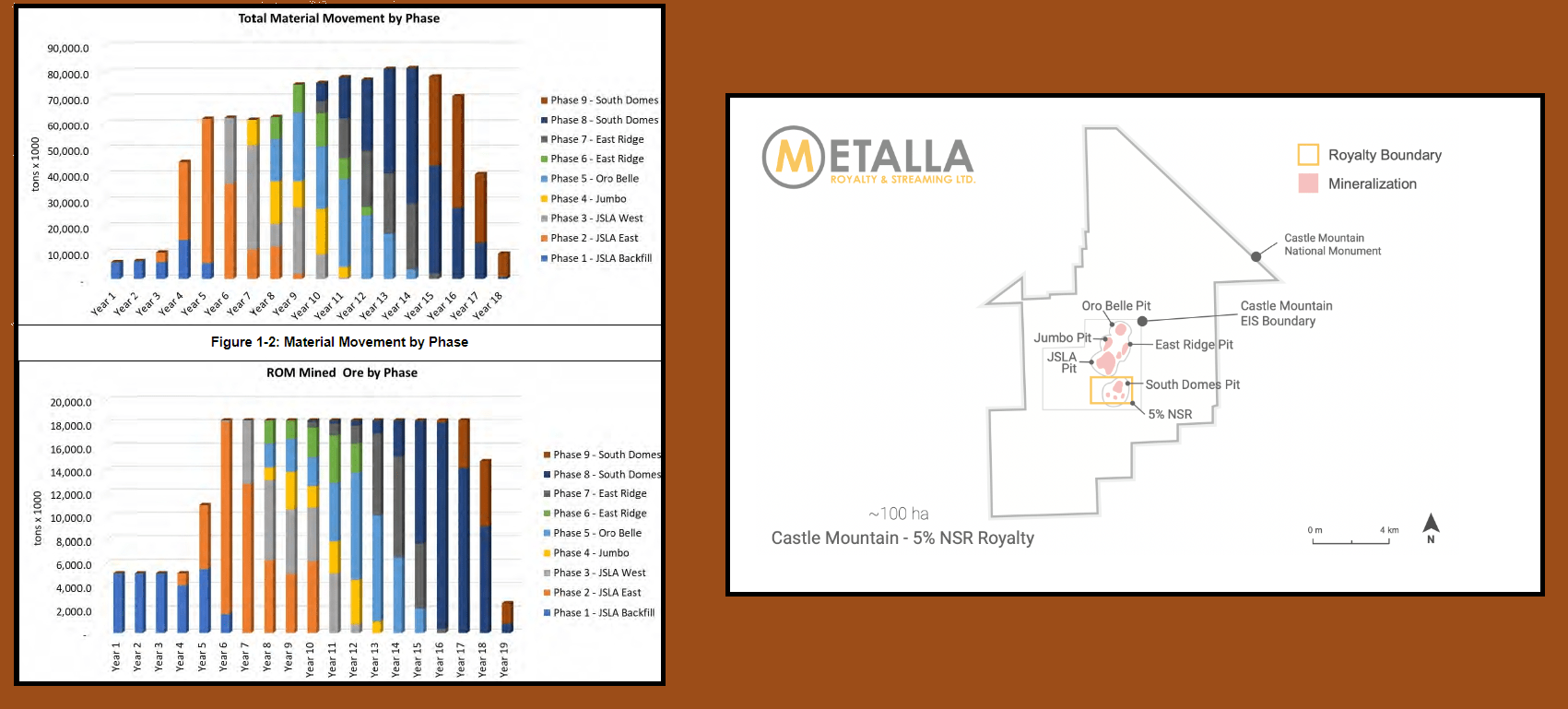

Lastly, Metalla appears confident that its 5.0% NSR at Castle Mountain Phase 2 will begin contributing in 2026 and with the extensive United States Bureau of Land Management [BLM] permitting process, I would be just as shocked to see the expansion permitted before 2026, with Equinox ( EQX ) noting that it could take four years from the start of permitting (March 2022), and it typically being safer to add a year to permit timelines. Hence, I would be surprised to see Castle Mountain Phase 2 start delivering attributable revenue to Metalla before Q2 2027 (if permitted) with 2026 also being a very aggressive assumption. Plus, per the 2021 Technical Report, South Domes (where Metalla holds its royalty) was expected to sequence in last behind East Jumbo, Oro Belle, and East Ridge. Hence, I'm not sure mining even begins here before late H2 2028 without changes to the schedule.

Castle Mountain 2021 TR & South Domes Royalty Coverage - Material Movement/ROM Mined Ore by Phase (2021 TR, Metalla Website)

{kind=link}

To summarize, while there's no denying Metalla's future growth, many of the near-term timelines look too aggressive, and some I don't know whether they're even worth including in here (Fosterville Extensions/Santa Gertrudis, Endeavor). In fact, in the case of the Endeavor Silver Stream, Sandfire Resources withdrew from the earn-in agreement with CBH Resources, a downgrade for this asset as well. Therefore, without new near-producing assets added to the portfolio, I think it's a stretch that we'll see ~18,000 GEOs by Q2 2027, which is roughly what Metalla was guiding for in its Q2 2022 Presentation (shown below).

Metalla Previous Growth Outlook (Q2 2022 Presentation)

{kind=link}

So, what price are investors paying for this future growth?

Valuation & Technical Picture

Based on ~56 million fully diluted shares and a share price of US$5.65, Metalla trades at a market cap of ~$316 million. This has left the stock trading at a slight premium to an estimated net asset value of $310 million, with Metalla currently trading at ~1.02x P/NAV. While this is certainly a discount relative to peers like Osisko Gold Royalties ( OR ) and Triple Flag Precious Metals and even larger peers in the sector, I don't see any reason that junior royalty/streaming companies that lack scale should trade above 1.10x P/NAV, and I see a fair multiple range being 0.90x - 1.10x P/NAV. Currently, Metalla is bumping against the upper end of this conservative valuation range, and even if we use a higher multiple of 1.10x P/NAV, I see a fair value for the stock of US$6.00 using an estimated year-end share count of 57 million fully diluted shares.

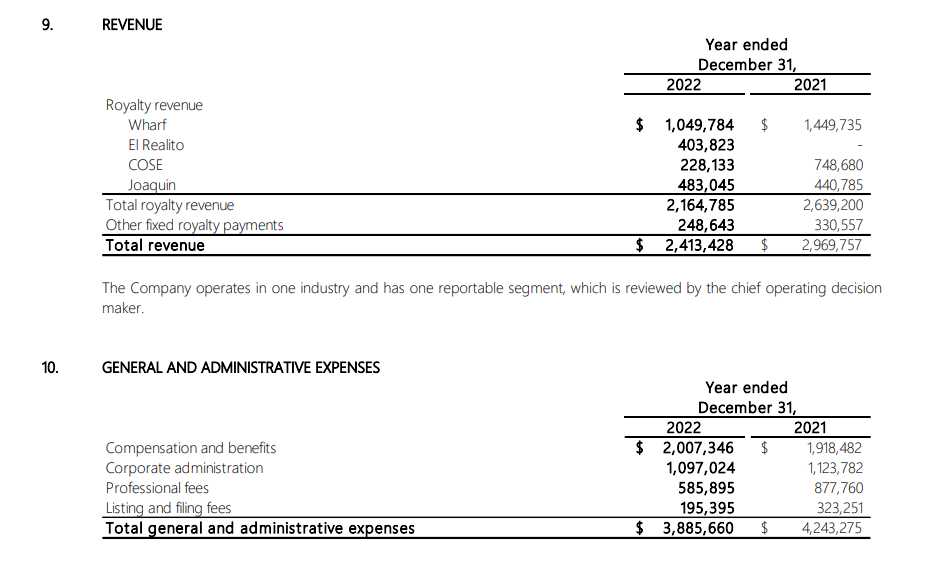

Metalla - Annual Revenue & G&A Expenses (Company Filings)

{kind=link}

Although this points to moderate upside from current levels, I am looking for a minimum 35% to 40% discount to fair value to justify starting new positions in junior royalty/streaming companies, and especially those with smaller market caps. In Metalla's case, one could make an exception at 35% given the quality of this portfolio (solid assets that are in mostly Tier-1 and Tier-2 jurisdictions). After applying this discount, Metalla's ideal buy zone comes in at US$3.90 or lower, over 30% below current levels. Obviously, there's no guarantee that the stock pulls back by this magnitude, but I don't see any margin of safety here and while some may not believe that the stock can decline to these levels, some investors were equally apprehensive to be mindful of downside potential when I noted to sell the stock above US$13.00 in Q1 2021.

Metalla - January 2021 Article (Seeking Alpha PRO/Premium)

{kind=link}

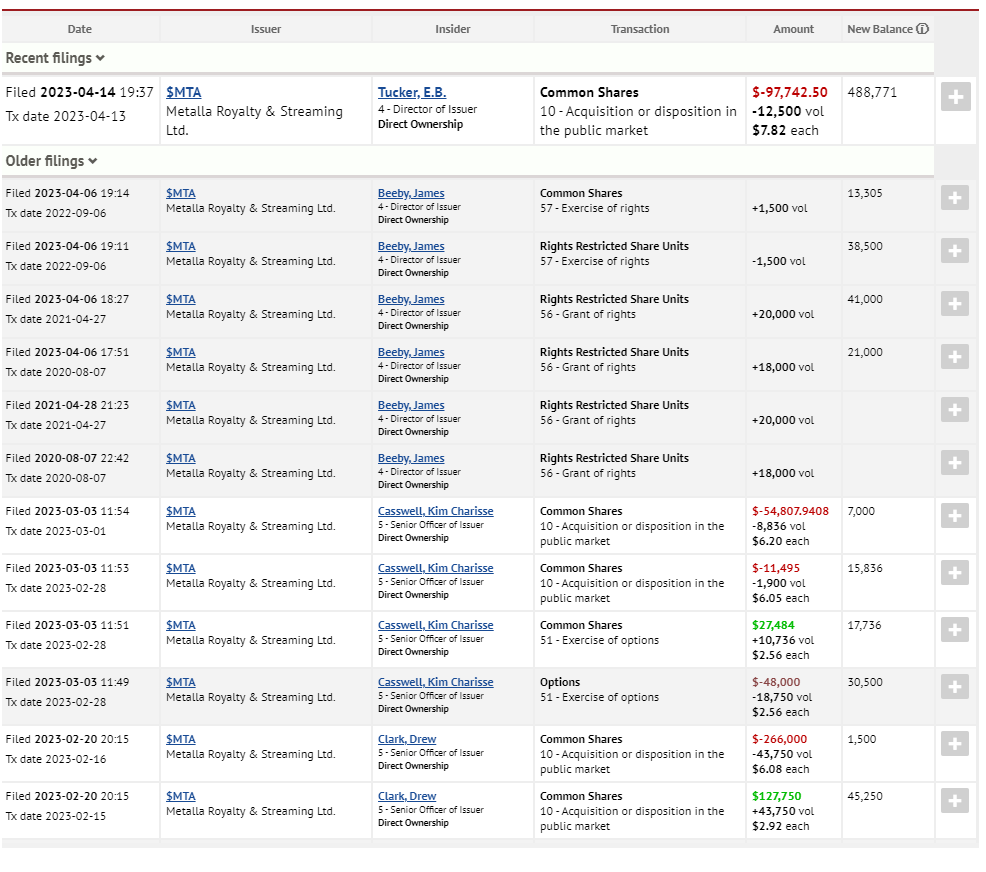

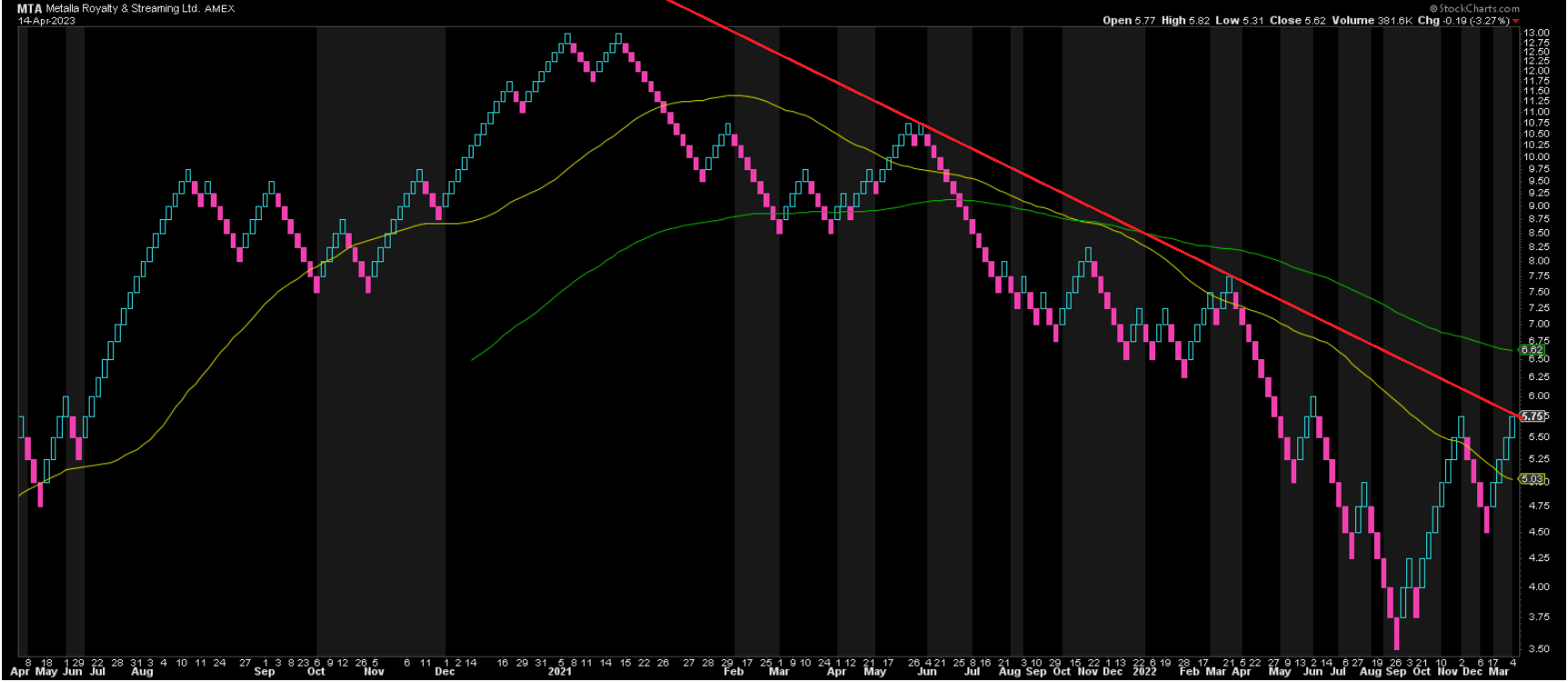

Finally, when we look at the technical picture (shown below), I noted that the stock would move into a low-risk buy zone below US$3.70 in my September update, and the stock has since soared over 60% from this level and we've seen some insider sales recently. This doesn't mean that the stock has to go lower, but with the stock rallying towards technical resistance, no longer being attractively valued, and additional selling pressure that could come from insiders or its ATM which can have an impact in a less liquid name like Metalla (average volume of less than $800,000 per day on US Market), I see an elevated risk to paying up for the stock here. This is especially true when the reward/risk ratio has moved from better than 7.0 to 1.0 in favor of the bulls in October 2022 to less than 0.35 to 1.0 currently based on the current support resistance/range (US$4.35 - US$6.10).

The most recent insider sale is shown in Canadian Dollars (C$7.82) or the equivalent of US$5.80).

Metalla - Insider Activity (SEDI Insider Filings) Metalla - Insider Activity (SEDI Insider Filings) MTA Daily Chart (StockCharts.com)

{kind=link}

{kind=link}

Summary

Metalla had another busy year in 2022 and the year is off to a decent start with the recent hike in metals prices and the improvement in sector-wide sentiment that has pushed the stock higher. However, we've seen what I would argue to be a few less favorable developments across the portfolio which include a less clear outlook for Santa Gertrudis, operating constraints at Fosterville, a longer timeline to move Wasamac into production vs. the expedited stand-alone plan expected by Yamana (long-term bullish, but attributable revenue likely to come later than 2026), and continued inflationary pressures that could impact some juniors' ability to finance their projects (early-stage/development portfolio) with 30%+ inflation on greenfield projects, rendering many economic studies as stale and difficult to rely upon from an opex/capex standpoint.

As I noted in my September update , any perceived negatives were more than priced in with Metalla trading near US$4.00, and further weakness below US$3.70 would provide a buying opportunity. However, with the stock now up over 50% from this ideal buy zone, I no longer see the setup as attractive, and the recent high volume selling pressure (down 3.3% on 2x average volume on Friday) combined with a break of the 8-day moving average as a negative development. Hence, I don't see any reason to chase the stock at current levels and if this rally were to persist, I would view any moves above US$5.95 before June as an opportunity to book some profits.

For further details see:

Metalla Royalty & Streaming: Don't Chase The Stock Here