MTD - Mettler-Toledo: A Great Business At A Lousy Price

2023-04-23 12:22:47 ET

Summary

- Mettler-Toledo is a leading manufacturer of precision instruments with deep customer relationships.

- The company has shown a significant margin improvement over the last decade.

- Buybacks have been used effectively to reduce the share count and boost EPS.

- Although the business is of high quality, the valuation is not justified by the growth rate.

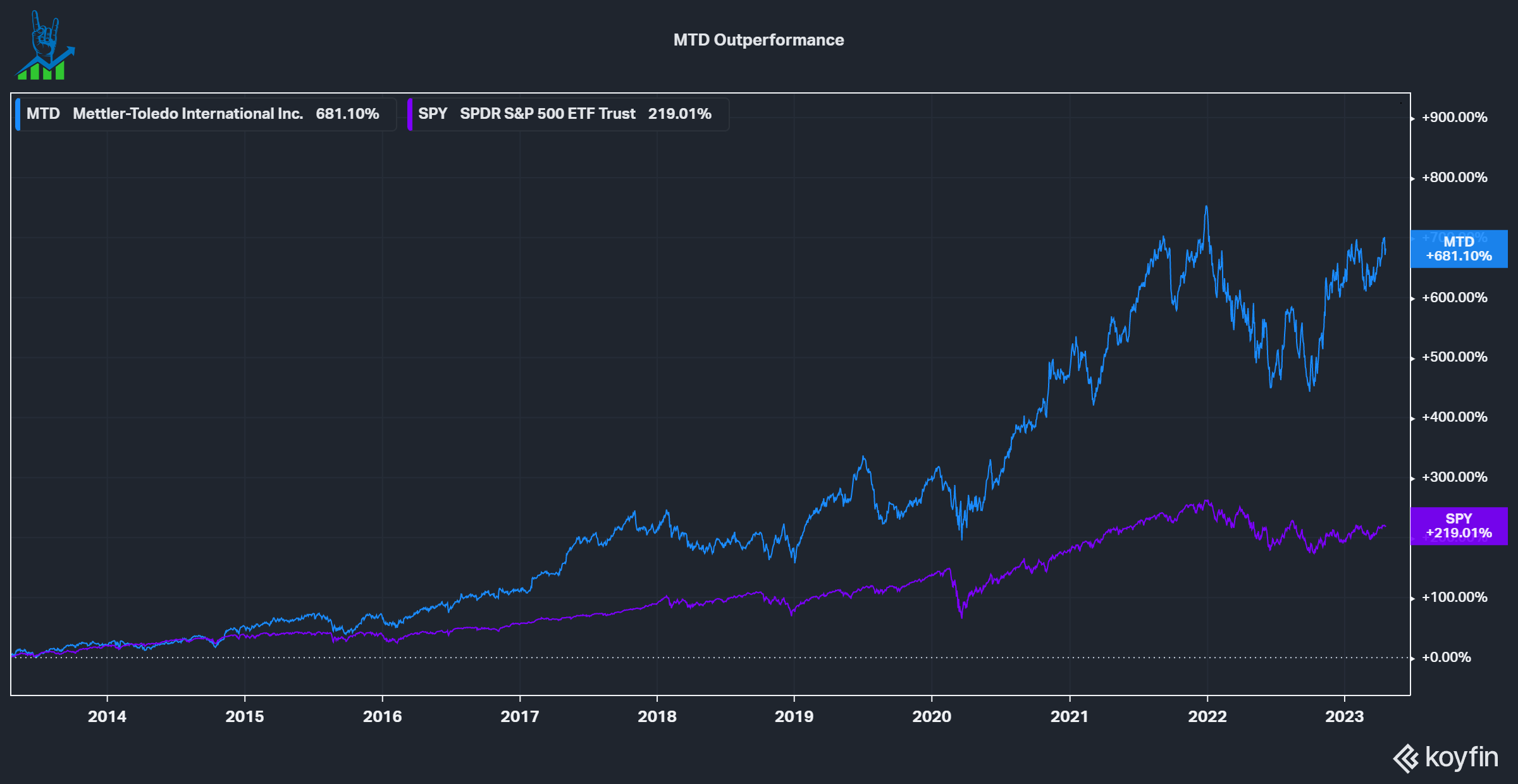

Mettler-Toledo (MTD) is a leading global manufacturer and marketer of precision instruments. Its products are used in laboratories (57% of sales), Industrials (38%) and Food retail (5%). The company has flourished over the last decade and significantly outperformed the S&P 500. During the bear market, it sold off around 33% but is almost at its ATH again. Let's see if the company still offers a compelling investment opportunity.

{kind=link}

Integrated product offering

The company has a diversified set of customers with its three segments and its wide diversification over the Americas (40% of sales), Europe (26%) and Asia/RoW (34%). This means that MTD is susceptible to foreign exchange rates. MTD is best known for its laboratory balances, which are an integral part of every laboratory and can weigh up to one ten-millionth of a gram of precision. MTD also offers integrated software to analyze the data. Often the same customers also use industrial instruments for the manufacturing part of their operation. This is a great lock-in effect and allows Mettler to be an integrated part of the entire operations of a customer. The company also offers products for packaging and logistics and thus offers solutions for the entire product value chain for its customers. The food retailing segment mainly focused on Point of sale systems with an integrated scale and is probably the most public-facing part of the offering. I noticed one of MTD's devices during shopping this week and that's how I got reminded to continue my research on the company.

Mettler-Toledo retail solution in a local fresh food store (Authors picture)

Industry tailwinds

According to the business research company , the global measuring and control instruments market is expected to grow at an 8.1% CAGR through 2027. This provides tailwinds for Mettler-Toledo for growth, besides taking market share and growing sales within its customer base. Its largest market is instruments for the life sciences industry, which Grand View Research expects to grow even faster at a 10.8% CAGR through 2030.

Going through the numbers

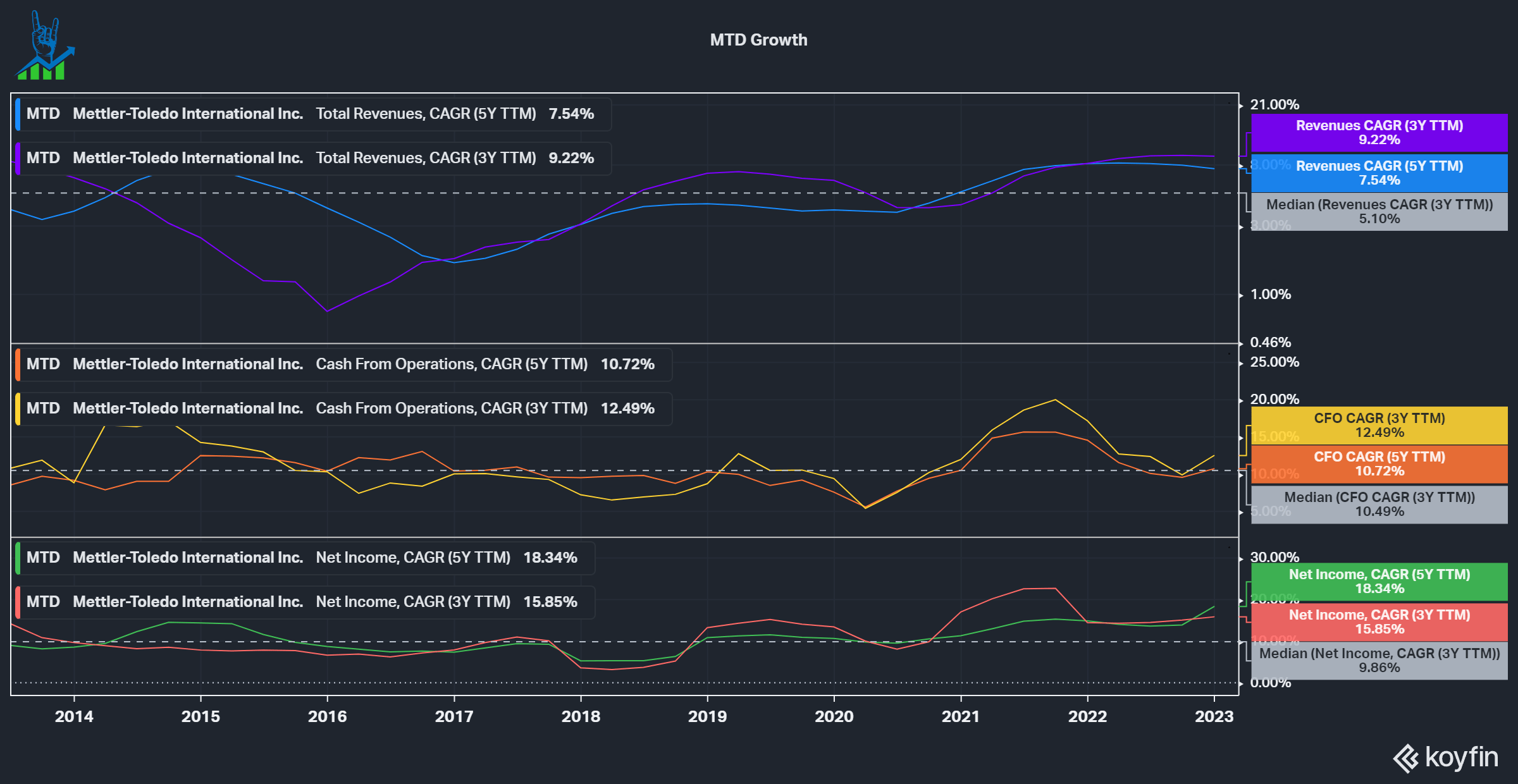

If we take a look at the historical growth rates of Mettler-Toledo we can see that they grew sales within the industry growth rate and even a little lower. The median CAGR over the last decade has been just 5%.

We can also see that profits and cash flows grew significantly faster than sales, especially in recent years. Operating cash flow averaged 10.5% and EPS 9.9% over the last decade.

{kind=link}

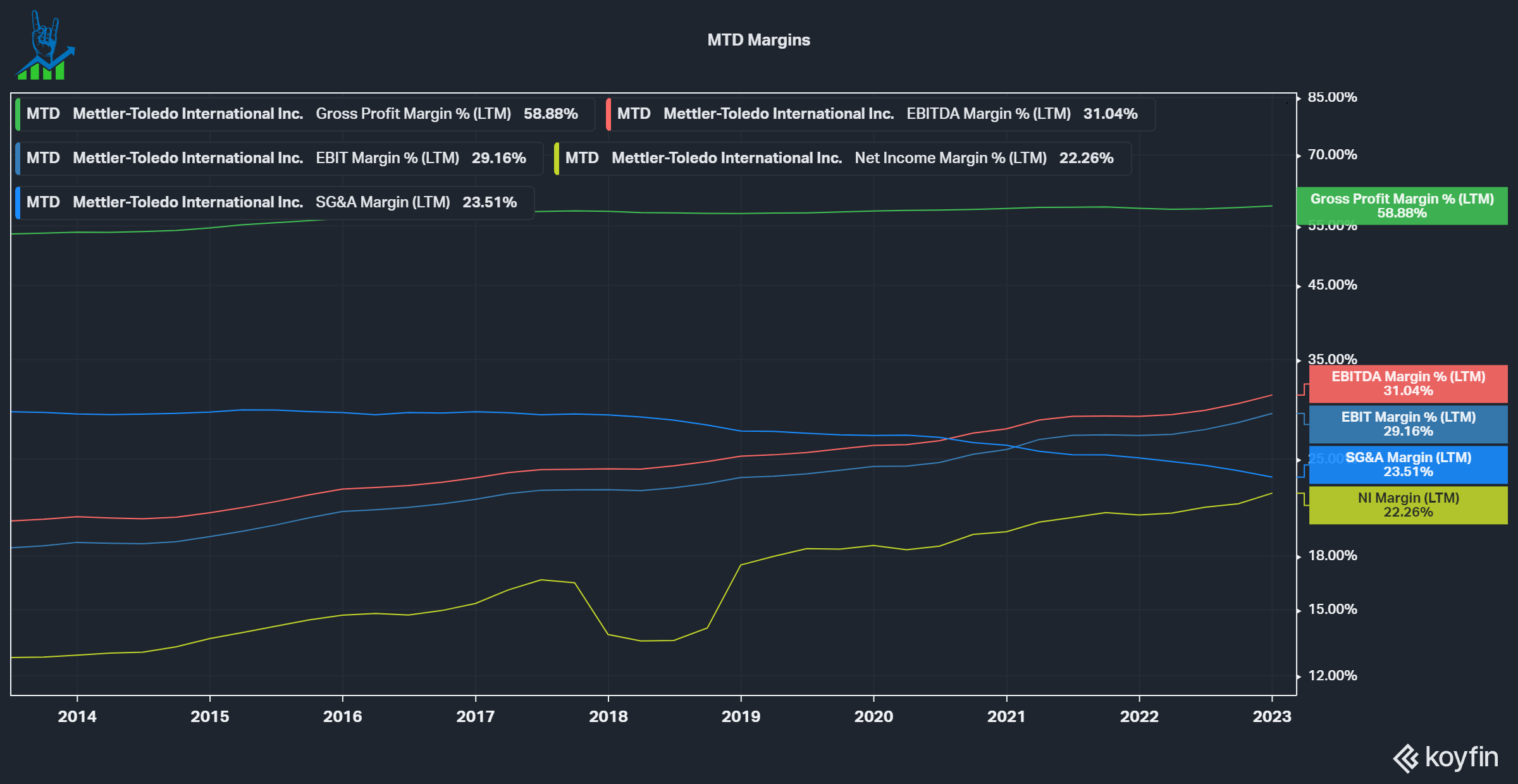

As you can imagine the margin profile development looks very attractive for the company to achieve such a difference between sales and profit growth. Gross margins improved slightly by 500 bps, but profit margins grew around 1000 bps across the board, while SG&A margin declined by 600 bps.

{kind=link}

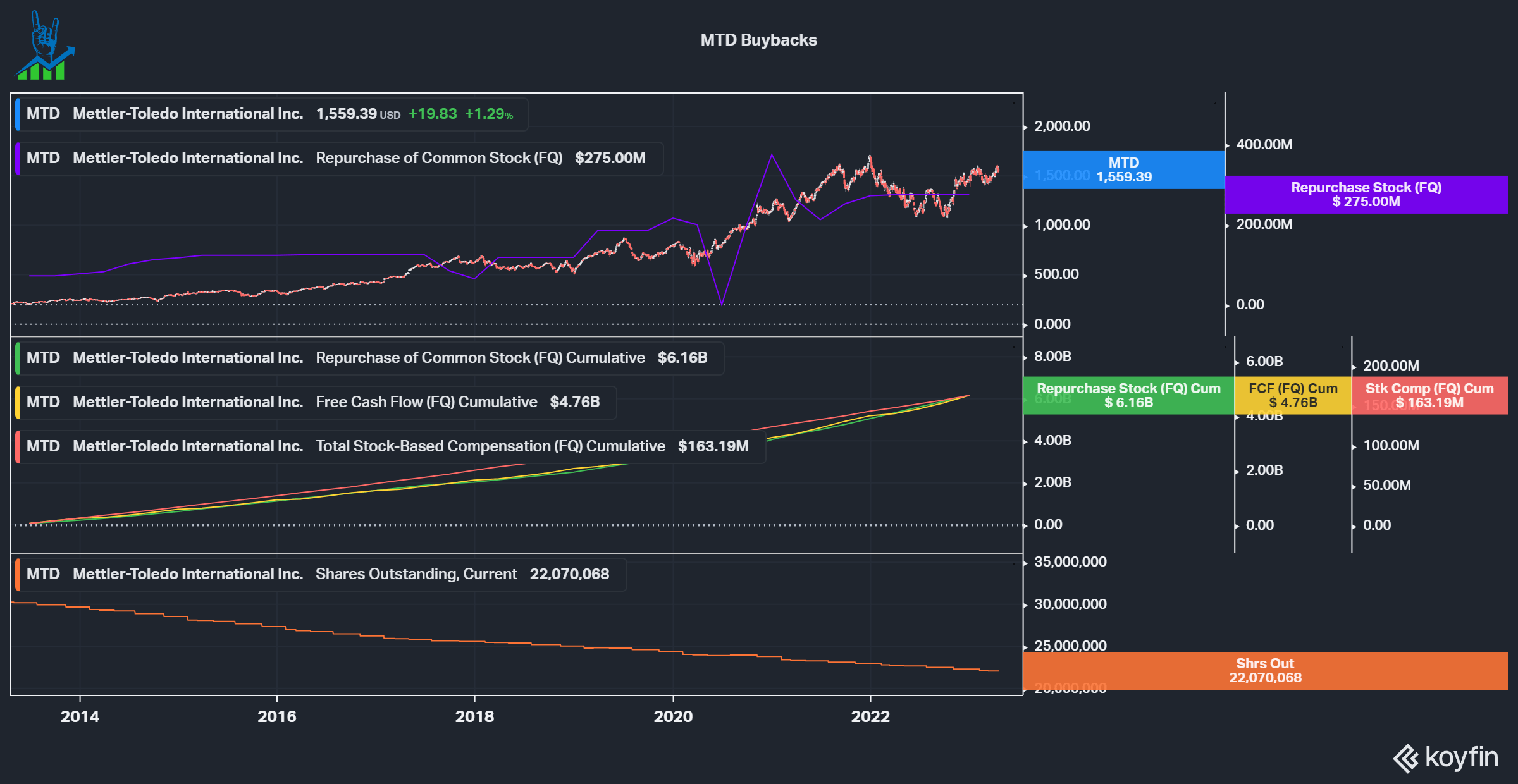

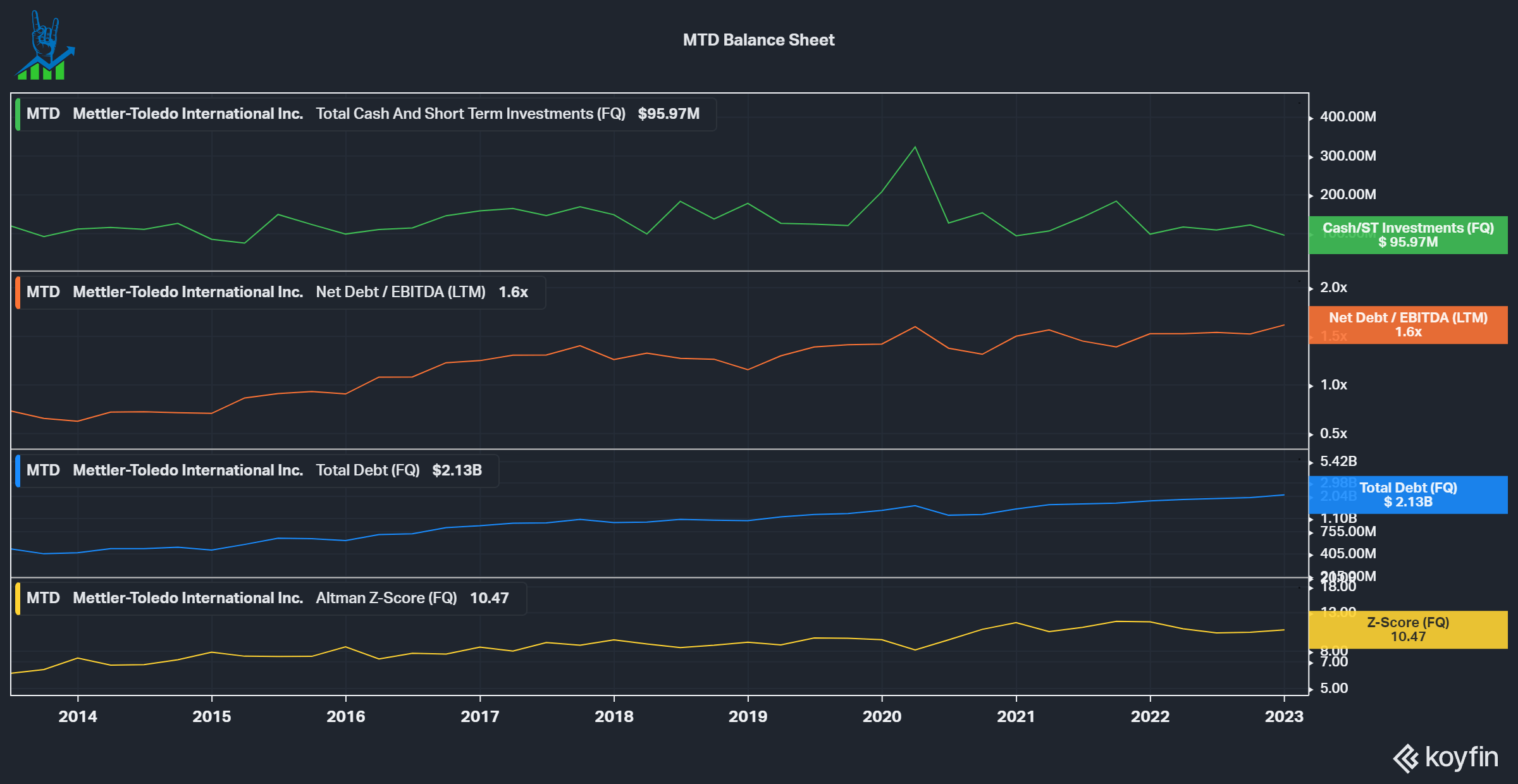

Another way MTD boosted earnings was via buybacks. Over the last decade, the company spent $6.16 billion on buybacks. This compensated the modest $163 million in stock-based compensation over the period and reduced the share count by 27%. If we compare this to the current market cap of $34.4 billion, then we see how effective the buybacks have been: They spent 18% of the current market cap to reduce shares by 27%. This is how we want to see buybacks done. We have to keep in mind though that these buybacks weren't fully funded from operations. The company generated $4.76 billion of free cash flow and also spent $514 million on M&A; no dividends were paid over the last decade. This means that the company used $1.9 billion in debt to fund additional buybacks.

{kind=link}

As you would imagine we can see continuous levering throughout the last decade going from 0.7 times net debt/EBITDA to 1.6 times. This is not a critical level and looks healthy; I personally aim for companies within 2 times. Especially given the good use of this debt, I don't see a problem with it. If we look at the latest annual report , we can see that the debt is in attractive conditions with most of it maturing after 2030 and with rates below 4%. A highlight would be the 125 million Euro note due March 2036 at just 1.06%. $1.25 billion are fixed rate senior notes plus $700 million flexible debt from a $1.25 billion credit they can draw on.

{kind=link}

Management compensation

If we look at the latest proxy , we can see how management is compensated. This can often tell us something about the focus of the company.

The company awards its executives short-term (1 year) cash incentives based on Adjusted Non-GAAP EPS, net cash flow (operating cash flow) and Group sales. This shows the focus on growing sales and cash flows. Long-Term targets are purely based on total shareholder return: If the stock is below the 30th percentile then the long-term compensation is 0% and goes up to 200%. I generally like the compensation structure. We can also see that management is incentivized to do lots of buybacks, given the EPS part of the compensation.

Sadly management does not own a significant stake in the company. All insiders own 3% of the company. Ideally, we want to see at least 5-10%, but at least we have some skin in the game.

Valuing Mettler-Toledo

To value Mettler-Toledo, I'll use an inverse DCF Model. I use both free cash flow and owner earnings, which I define as Free cash flow + Growth CapEx - Stock-based compensation. I approximate the Growth capex by subtracting Depreciation and Amortization ($73 million) from Capital Expenditures ($121 million). We can see that Mettler-Toledo is very expensive here, requiring a 20% growth rate for the next 5 years, followed by 15% for the following 5 years. This is significantly above its historical growth rates and the projected growth rate of the industries they operate in. Even though the company is of high quality, I am not willing to pay this type of premium for it. Valuation multiples show a similar picture, where MTD's valuation almost doubled over the last decade. MTD is a hold due to its high quality, but nothing more.

MTD Inverse DCF Model (Authors Model)

For further details see:

Mettler-Toledo: A Great Business At A Lousy Price