WST - Mettler-Toledo International: Shares Still Expensive Heading Into Q2 Earnings

2023-07-14 09:57:48 ET

Summary

- Mettler-Toledo International Inc. stock has been hit hard despite the company's continued improvement in revenue, profits, and cash flows. The company is rated a "hold" due to its significant share price underperformance.

- The company's financial results for the first quarter of its 2023 fiscal year showed a 3.4% increase in revenue and a rise in net income from $174 million to $188.4 million. However, the stock is down 7.3%.

- Despite the company's robust performance, Mettler-Toledo International remains a fundamentally healthy but unappealing prospect, though Q2 earnings could always change that picture.

One of the downsides about buying shares of companies when those shares are trading at lofty levels is that, even when things go right, you can be in for a world of pain. Rising revenue, profits, and cash flows may seem like a recipe for success. But when the company in question is already trading at multiples comfortably above what it should be trading for, the market will sometimes only grant pain in return.

A really great example of this can be seen by looking at Mettler-Toledo International Inc. ( MTD ), an enterprise that's focused on the production and sale of precision instruments and the provision of related services. Even though the fundamental picture of the company continues to improve year after year, the stock is trading at rather lofty levels.

As a general rule of thumb, I tend to not rate these kinds of firms in a bearish manner. After all, growth is generally rewarded in the long run, and this enterprise in particular is trading at levels that makes it look more or less fairly valued compared to similar firms. So sticking with that tradition, I've decided to keep the company rated a "hold" even in light of significant share price underperformance.

A tough few months

Back in November of last year, I decided to revisit my prior thesis regarding Mettler-Toledo International. From August when I initially wrote that thesis until the publication of the article in November, the stock had risen 18.7% compared to the 1.1% decline seen by the S&P 500 (SP500).

Frankly, I was surprised by this. Yes, the fundamental picture for the company was continuing to impress. But shares looked rather pricey. I concluded that, in the long run, the business would probably do quite well for itself. But because of how expensive shares had become, I could not rate it any higher than the "hold" I had it at previously. Since then , we have seen a reversal of fortune. The stock is now down 7.3% at a time when the S&P 500 is up 11.4%.

{kind=link}

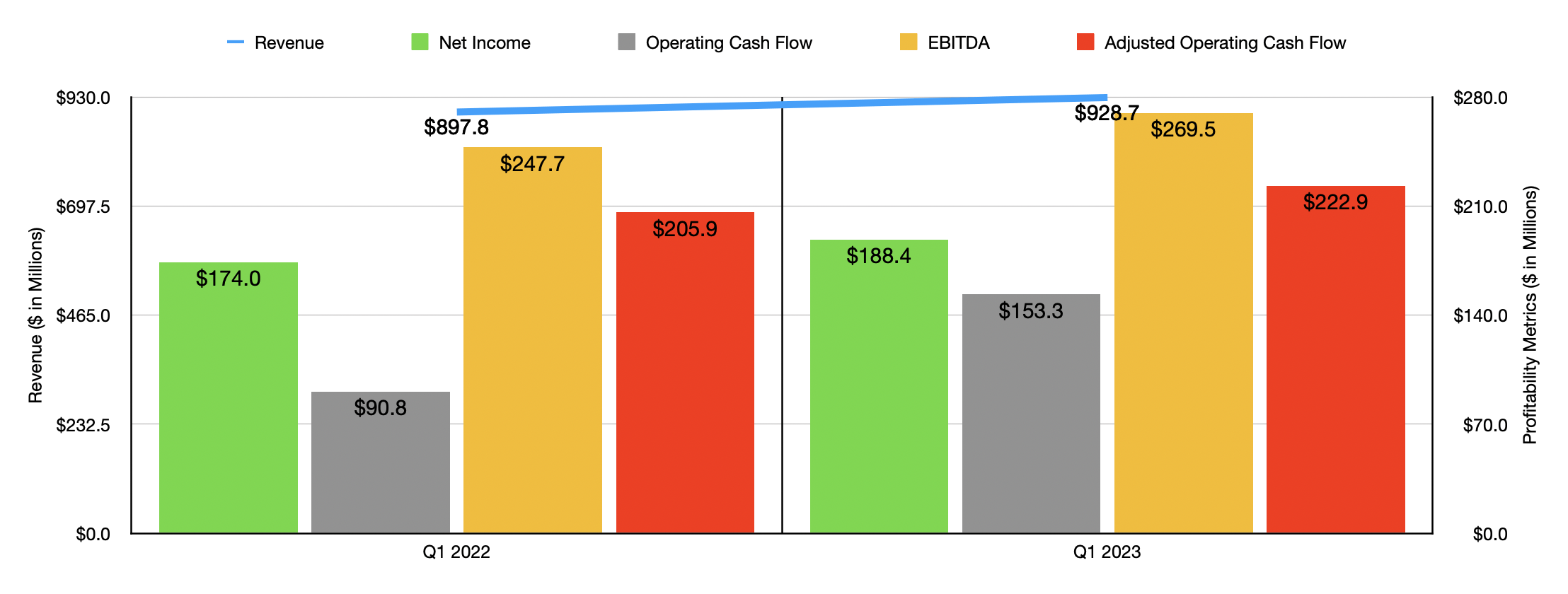

At first glance, you may think that this change in direction can be chalked up to fundamental underperformance. But that is not the case here. Consider financial results covering the first quarter of the company's 2023 fiscal year. Revenue for that time came in at $928.7 million. That's 3.4% above the $897.8 million the company generated one year earlier. Growth would have been even stronger, coming in at about 7%. However, foreign currency fluctuations negatively impacted the enterprise.

Management attributed the growth that they did receive to broad-based growth across most of its businesses and regions. And they seemed to think that this was thanks to factors such as global sales and marketing initiatives, the company's continued innovation, and various investments that it was making. They did, however, caution that economic uncertainty could prove a problem in the future. In particular, they mentioned Ukraine and inflation as primary areas of concern.

The rise in revenue for the company brought with it higher profits as well. Net income popped up from $174 million to $188.4 million. An increase in the company's gross profit margin from 57.9% to 58.9% aided on this front. This, according to management, was driven largely by price increases. Selling, general, and administrative costs declined from 26.2% of revenue to 25.3%. This, according to management, was due to the company's decision to just not scale up its marketing efforts in alignment with the rise in sales.

Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, jumped from $90.8 million to $153.3 million. If we adjust for changes in working capital, the increase was more modest, from $205.9 million to $222.9 million. And finally, EBITDA for the company expanded from $247.7 million to $269.5 million.

{kind=link}

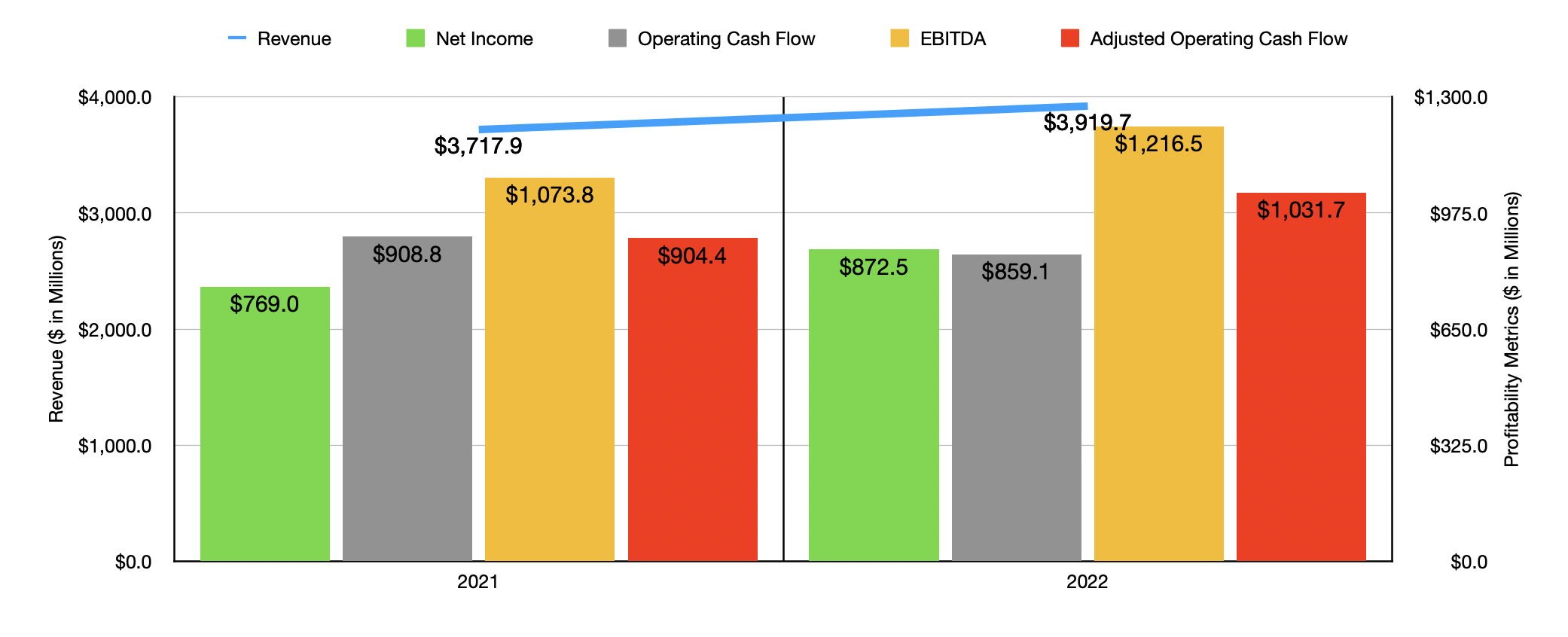

The results experienced by the company for the first quarter of the year were part of a larger trend for the enterprise. In the chart above, for instance, you can see financial performance for the 2022 fiscal year compared to 2021 . The same factors that drove robust performance during the first quarter of 2023 compared to the same time last year were also instrumental in pushing up revenue for 2022 compared to 2021. With the exception of operating cash flow, all of the company's profitability metrics grew year-over-year. And even with the operating cash flow picture, the adjusted figure for it expanded nicely.

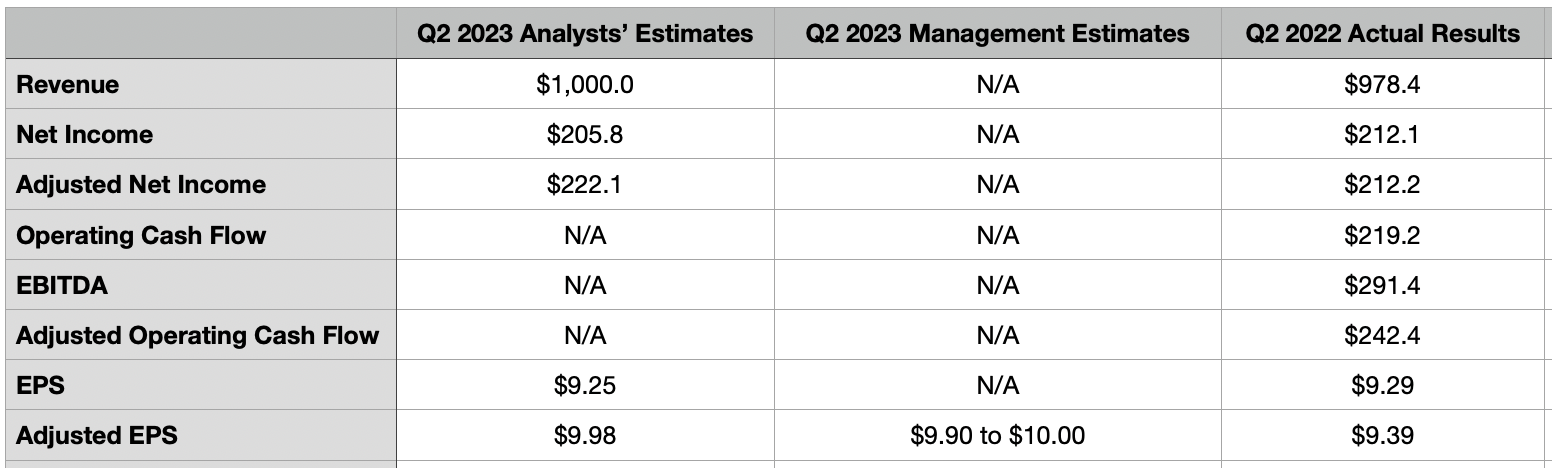

As management highlighted in their first quarter earnings release, economic uncertainty remains an area of focus. This is why investors, now more than ever, should pay careful attention to when the company reports financial results for the second quarter of 2023. This is slated to occur after the market closes on July 27th. Management does not provide sales guidance on a GAAP basis because they don't feel confident in forecasting the impact that foreign currency fluctuations will have on the company's top line. But they did say that they anticipate constant currency revenue to grow by about 3% year over year. Analysts, at the moment, currently anticipate revenue of roughly $1 billion. If this comes to fruition, it would translate to an increase of 2.2% compared to the $978.4 million generated in the second quarter of 2022.

{kind=link}

On the bottom line, analysts expect earnings per share to be $9.25, with adjusted earnings per share of $9.98. To put this in perspective, earnings per share in the second quarter of last year totaled $9.29, while the adjusted figure came in at $9.39. This translated to net profits of $212.1 million, with adjusted earnings per share translating to adjusted profits of $212.2 million. If analysts turn out to be correct, the company should generate net income of $205.8 million, with adjusted profits of $222.1 million.

Management previously forecasted adjusted earnings per share of between $9.90 and $10. At the midpoint, that would translate to roughly $221.4 million. Estimates have not been provided for other profitability metrics. But for context, operating cash flow in the second quarter of 2022 was $219.2 million, while the adjusted figure for it was $242.4 million. Meanwhile, EBITDA totaled $291.4 million.

For 2023 in its entirety, management expects constant currency revenue to grow by roughly 5%. Adjusted earnings per share, meanwhile, should be between $43.65 and $43.95. That is in spite of a 2% hit associated with foreign currency fluctuations. At the midpoint, this would translate to net profits of $974.7 million. That would be 11.7% above the $872.5 million the company generated in 2022. No estimates have been provided when it comes to other profitability figures. But based on my own math, I believe that adjusted operating cash flow should be around $1.15 billion, while EBITDA should total about $1.36 billion.

{kind=link}

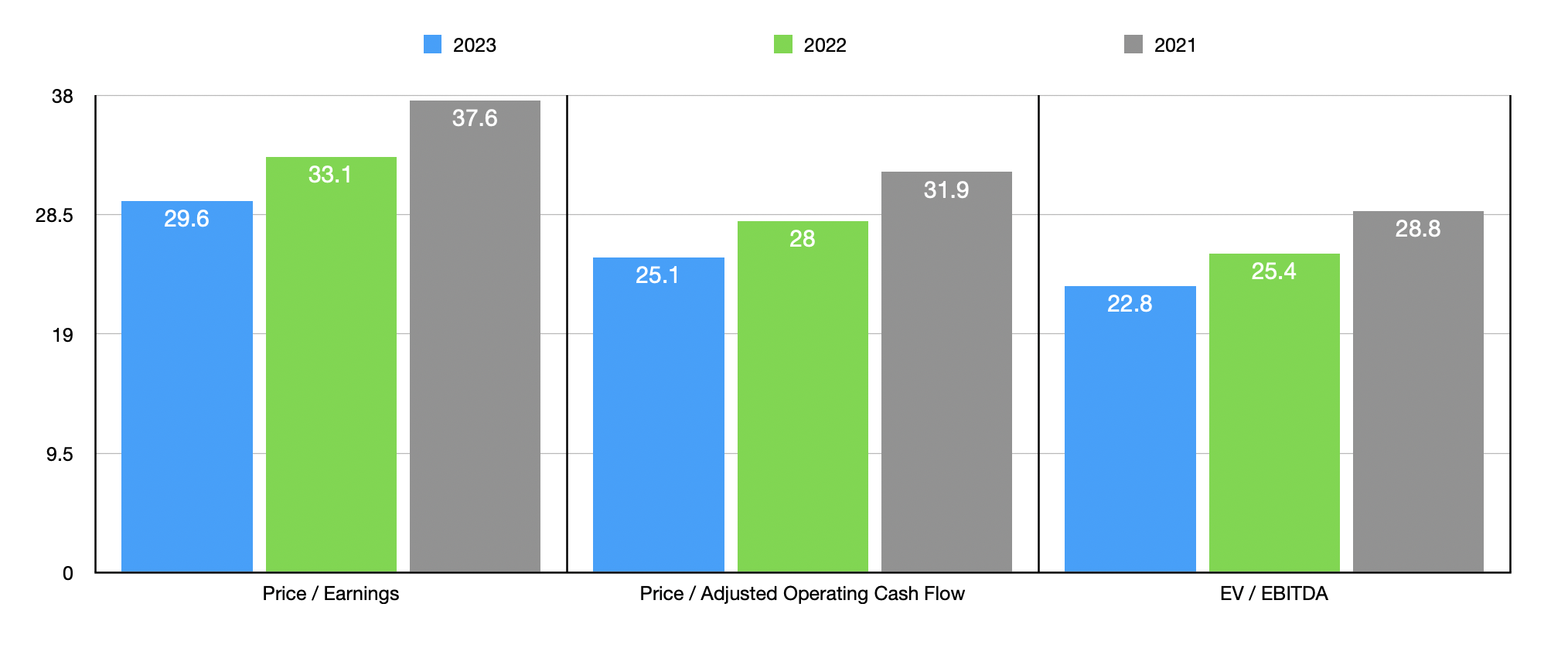

In the chart above, you can see how shares are priced on a forward basis for 2023. You can also see how the stock is priced using data from 2021 and 2022. Even though the company is getting cheaper from year to year, it does look rather lofty on an absolute basis. In the table below, meanwhile, you can see how shares of the company are priced compared to five similar enterprises. Using both the price to earnings approach and the price to operating cash flow approach, I calculated that two of the five firms ended up being cheaper than Mettler-Toledo International. Meanwhile, using the EV to EBITDA approach, three of the five ended up being cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Mettler-Toledo International |

| 33.1 |

| 28.0 |

| 25.4 |

| Illumina ( ILMN ) |

| N/A |

| 127.9 |

| 79.8 |

| West Pharmaceutical Services ( WST ) |

| 51.8 |

| 40.1 |

| 35.1 |

| Agilent Technologies ( A ) |

| 26.3 |

| 24.2 |

| 18.2 |

| Waters Corporation ( WAT ) |

| 23.2 |

| 26.2 |

| 16.7 |

| ICON Public Limited Company ( ICLR ) |

| 39.0 |

| 38.8 |

| 17.3 |

Takeaway

At this point in time, Mettler-Toledo International remains fundamentally healthy. And if management is correct, that should continue to remain the case. Ultimately, however, this does not mean that the company makes for an appealing prospect for value-oriented investors. The stock looks quite pricey and, in retrospect, I was probably too optimistic when I wrote about it previously.

Having said that, I do think that Mettler-Toledo International Inc. stock still makes for a solid "hold" at this time. But it is always possible that, when management does report financial results for the second quarter, that picture could change. So investors would be wise to keep a close eye on how things go on that front.

For further details see:

Mettler-Toledo International: Shares Still Expensive Heading Into Q2 Earnings