MTD - Mettler-Toledo's 2023 Dip Exposes An Opportunity To Acquire This Compounder At A Discount

2024-01-12 16:55:43 ET

Summary

- Mettler-Toledo's stock has dropped 22% in the past year; perhaps now there is an opportunity.

- I believe that Mettler-Toledo is a wide-moat company, and other renowned investors share this belief as well.

- While there are short-term headwinds, the long-term growth prospects remain intact.

- There is the potential for multiple expansion in the foreseeable future.

- For long-term investors only.

My Thesis

Mettler-Toledo ( MTD ) had a rough year, indeed. The stock is down 22% in a one-year chart. However, the company remains very profitable and possesses many quality attributes. Our mission is to understand if this price drop presents an opportunity or if we should wait.

Why am I writing about MTD in the first place? Well, the reason is my firm belief that it is a wide-moat company, and I'm not alone in this opinion—both Terry Smith and Michael Mauboussin share this perspective. Examining the 10-year results, it has undoubtedly proven to be a remarkable compounder.

In my view, for long-term investors who can look past the 2023 and 2024 headwinds, we might have the chance to acquire a long-term compounder at a fair price.

A quick review of the business and its moat

MTD is a leading player in precision and weight instruments, founded in 1945 (another indicator of a great company). The management believes it is the market leader in most of its markets. It divides its market into three segments:

1. Lab (54% of Q3 sales): MTD offers a wide variety of precision laboratory instruments for sample preparation, synthesis, analytical benchtop, material characterization, and in-line measurement.

2. Industrial (39%): The company provides numerous industrial weighing instruments and related terminals, offering dedicated software solutions for the pharmaceutical, chemical, food, discrete manufacturing, and other industries. Additionally, MTD offers metal detection, X-ray, checkweighing, and other end-of-line product inspection systems used in production and packaging.

3. Food Retail (7%): MTD sells networked scales and software that can integrate backroom, counter, self-service, and checkout functions. It can also incorporate fresh goods item data into a supermarket’s overall food item and inventory management system. MTD offers stand-alone scales for basic counter weighing and pricing, price finding, and printing.

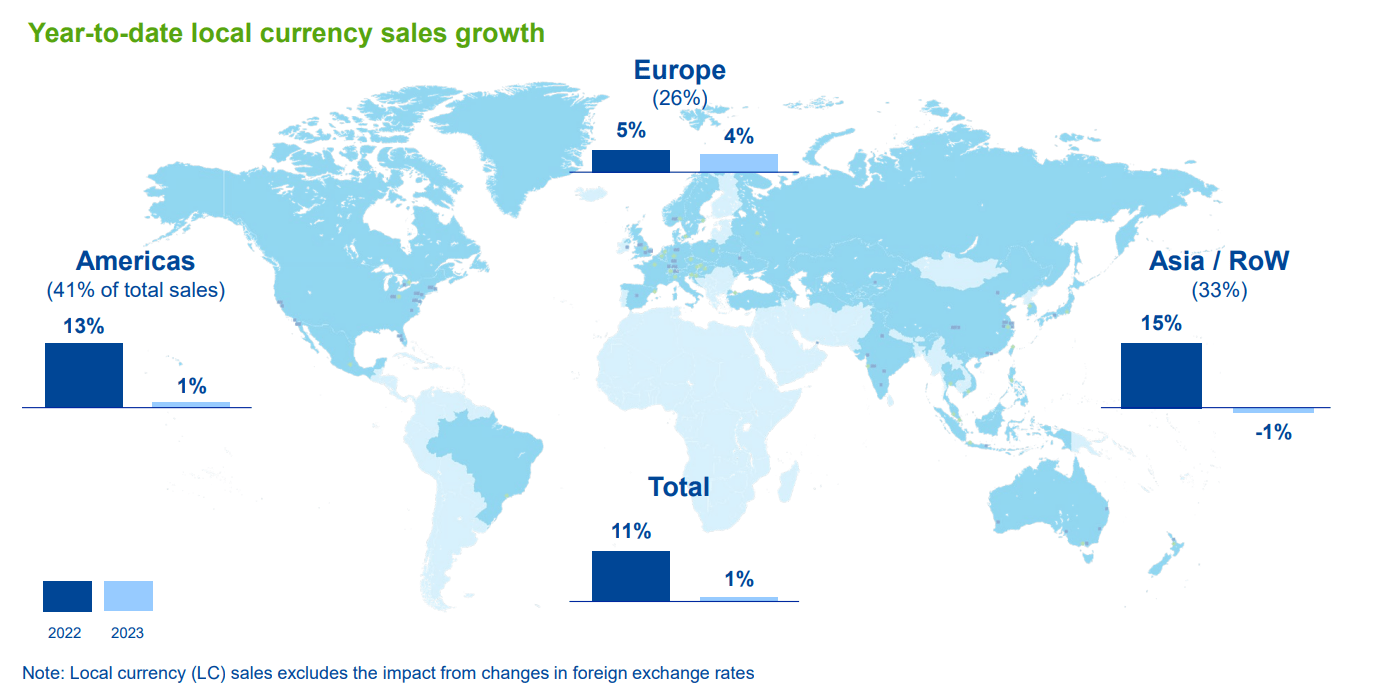

The business is well-diversified among regions and not dependent on a single customer, as no customer contributes more than 1% of sales. In Q3, net sales were derived from Europe (26%), North and South America (41%), and Asia and other countries (33%). The business has a significant presence in China, which notably impacted growth last year and is projected to continue with sales decreasing at a high single-digit rate in 2024.

{kind=link}

Another aspect contributing to the company's competitive advantage, as believed by management, is the service business, which accounts for 23% of revenues. This aspect is important because it creates customer relationships. MTD maintains geographically focused market organizations around the world that are responsible for all aspects of sales and service. These market organizations are customer-focused, with an emphasis on building and maintaining value-added relationships with customers in the target market segments.

We have one of the largest and broadest global sales and service organizations among precision instrument manufacturers we compete against... This field organization has the capability to provide service and support to our customers and distributors in major markets across the globe. This is important because our customers increasingly seek to do business with a consistent global approach.

we believe service is a key part of our solution offering and helps significantly in customer retention. The close relationships and frequent contact with our large customer base allow us to be the trusted advisor of our customers, which provides us with high-quality sales opportunities as well as innovative product and application ideas.

MTD typically allocates 5% of revenues to research and development (R&D) and is considered an innovation leader. MTD has a good reputation dating back more than 70 years, which is something that, even if a competitor desires, cannot be easily replaced. The competitive advantages that management believes they have are well described here :

advantages include our worldwide market leadership positions; our global brand and reputation; our track record of technological innovation; our comprehensive, high-quality solution offering; our global sales and service offering; our large installed base of instruments; and the diversification of our revenue base by geographic region, product range, application, and customer.

They can back all of these claims with numbers, as we will see further. I am not alone in the claim that MTD has a pretty wide moat; this is what Terry Smith wrote about MTD in the recent shareholders' letter :

Mettler-Toledo suffered from a downturn in demand for laboratory equipment post the pandemic, demand falling in China and a tighter funding market for biotech companies. However, we have no 3 concerns about their longer-term prospects and our holding in Mettler-Toledo, in particular, is small and we may be able to use share price weakness to acquire more.

MTD is also on the wide moat list of the great Michael Mauboussin from Morgan Stanley.

Numbers

In the past decade, MTD has more than doubled the S&P return, despite not being classified as a growth stock. However, what can you expect from a company whose customers come from diverse industries such as cosmetics, medicine, retail, and industrial, all of which are growing industries? As these sectors expand globally, they will continue to purchase MTD instruments to increase their production.

Another crucial factor, in my view, regarding MTD is its linear growth in both earnings and revenue. While it may not be recession-proof, as evident in the past year and the following year with decreasing growth, in the long term, it consistently keeps growing and increasing its margins with pricing power.

Significantly, most of the EPS growth comes from two factors: margin improvement, indicating substantial pricing power, and share buybacks, reducing the share count by about 2% annually, possibly more now given the decline in the stock.

Here is what the CFO said in the Q3 earnings call :

pricing continues to do very well this year. It came in about 4.5% or so for the third quarter, we'll probably be down a little bit from that level in the fourth quarter, probably in the 4% kind of a range. But then, when we kind of like think about next year, we're probably more in the 2% range, probably more -- in a more normalized environment for next year.

It seems like MTD has significant operating leverage, as its EBIT margin has shown a 5% CAGR in the last 5 years. We can assume that in the long term, with the anticipated 5-6% top-line growth, we will see the margins growing as well.

These high and growing margins contribute well to one of the most important indicator, in my view, for long-term success, which is a high and growing Return on Capital. ROCE for MTD has grown at a 10% CAGR in the last five years, and ROIC at a 5% CAGR, both creating a significant spread above the Weighted Average Cost of Capital. A study by Michael Mauboussin shows that a high and growing spread between a company's ROIC and its WACC is a common trait among winners.

In terms of solvency, it seems like MTD has a lot of debt, but it is not a problem in my view. More than 50% of the debt is maturing after 2033 and with low interest. Apart from that, a current ratio of 1.1 and an Altman Z score of 9 indicate a well-balanced and efficient balance sheet.

Q3 and Outlook

So, last week, MTD reported an update before Q3 earnings regarding their sales. Due to shipping delays, the guidance for Q3 is not relevant.

sales and Adjusted EPS for the fourth quarter of 2023 will be below its previously-issued guidance due to unexpected shipping delays with a new external European logistics service provider, which the Company expects to largely recover in the first quarter of 2024.

For the fourth quarter ended December 31, 2023, the Company estimates, based upon preliminary information, that reported sales declined approximately 12% and local currency sales declined approximately 13% as currency increased sales growth by approximately 1%. This compares with previous fourth quarter local currency sales decline guidance of approximately 7% to 8%.

It is not too much of a concern for us as it involves external factors. The management did well to announce it before earnings to avoid causing unnecessary worry during the earnings call.

Apart from that, let's talk about last year. After emerging from the COVID research burst, it seems like there was a severe slowdown in China and slower growth in the rest of the world, following the strong growth in the last two years. This makes the growth for 2023 flatten as well as in 2024.

As we look to the remainder of 2023, we expect market conditions to remain weak, especially in China. And based on market conditions as of today, we would expect these headwinds to persist into next year.

we expect a normalization in activity in 2024 and the long-term outlook remains strong as innovation pipelines remain full of novel drugs and therapies to be brought to the market.

I actually think this slowdown created an opportunity for long-term shareholders, as nothing has changed in the business's competitive advantages. China will continue to grow in the long term.

While the outlook for China is uncertain in the near-term, the long-term growth opportunity remains significant due to the country's commitment to expanding R&D investment and supporting development of advanced pharma, biopharma, new energy and new material industries. Our business is very well-positioned to capitalize from these growth opportunities and we expect solid growth over the long-term.

As well as the rest of the world, with long-term growth of 5-6%, driven by continued growth in R&D spending by the customers.

opportunity to capture market share in a few account for an underlying market growth over the mid and long term in the range of 4% to maybe 4.5%. We should get to the 6% by taking the market share that we are going after.

On top of the 5-6% top-line growth, we should add 1-2% a year for margin improvement, as well as 2-3% for share count reduction. That brings us to an 8-11% long-term EPS growth rate, and based on past numbers, perhaps even more.

Management & Board

As for executives' compensation, I don't think there is much to write about; it is pretty standard for a company of this size.

What is worth mentioning is the Chairman of the Board, the former CEO Robert Spoerry, holds about 1.2% of the company. This gives him good skin in the game, in contrast to the relatively new CEO who does not hold a significant number of shares.

Also, back in November, a director at MTD purchased more than 300 shares, a good indicator looking forward, in my view.

Risks

The risks I see include a significant portion of revenue derived from China. The instability in its economy over the last few years, along with increasing tensions with the US, makes me uncomfortable.

Another risk is a global recession, as seen in China; MTD is affected by such situations, and a slowdown in R&D spending could decrease revenues. Consequently, due to operating leverage, the margins could also decrease.

Additionally, another risk I see is valuation. MTD is not a cheap stock at all, and some investors may be hesitant to buy into 10% growth at 30 times earnings.

Valuation & Conclusions

MTD is currently trading significantly below its multiples' averages, mainly due to the slow growth it is currently experiencing. However, taking a long-term perspective, we could anticipate the growth to accelerate. In such a case, we might have the opportunity to invest in a long-term compounder at a favorable multiple. Nevertheless, purchasing a business at a 30 times multiple is advisable only if you plan to hold it for the long term, say, 5 years and beyond, allowing the compound effect to take place. Looking at the PEG ratio, assuming a long-term 12% EPS growth, we arrive at a PEG of 2.5, which is below the average of almost 3.

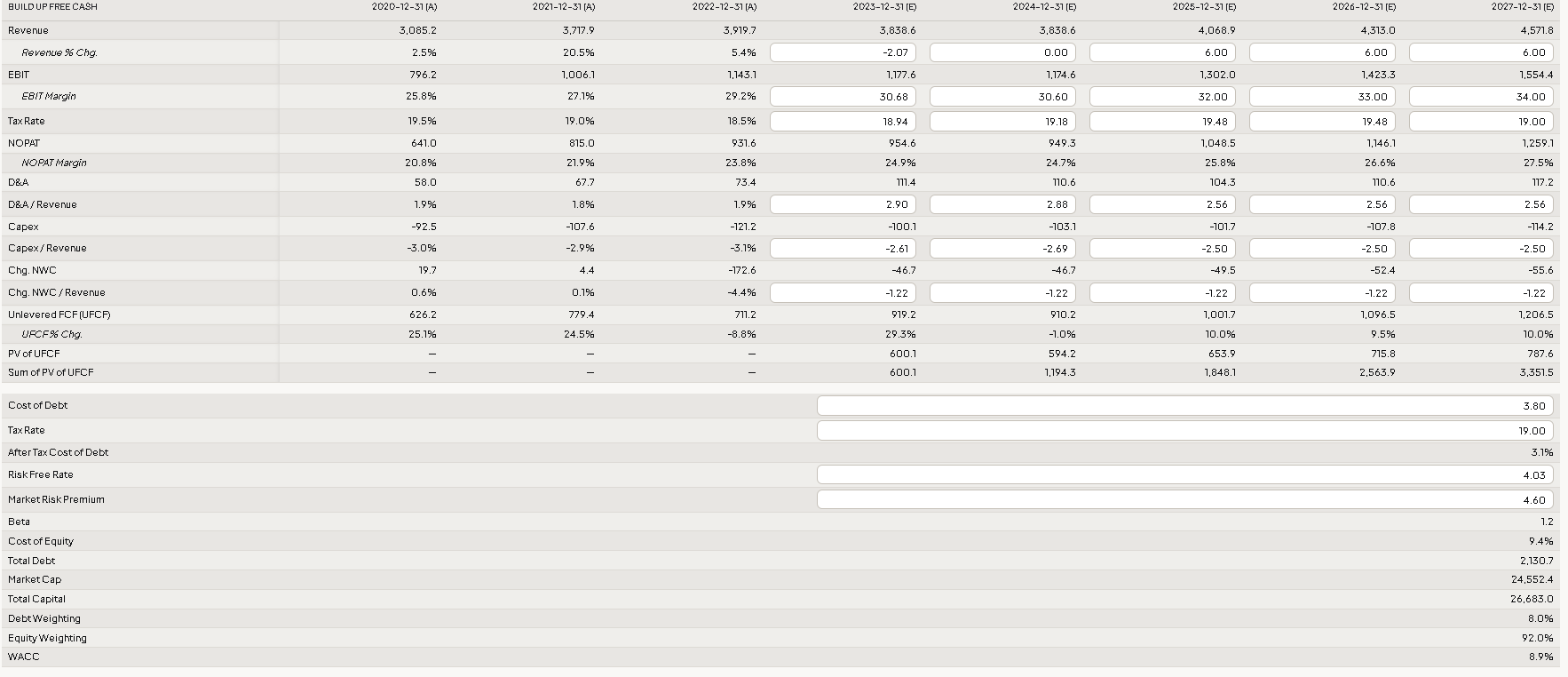

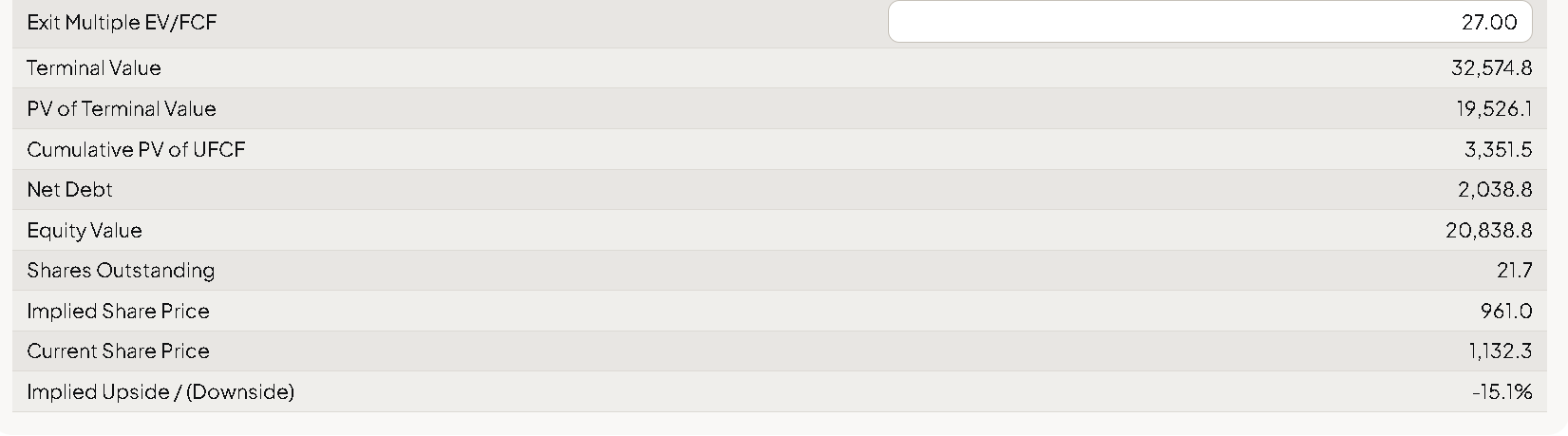

I will also conduct a DCF model, although I don't consider it highly effective for this type of business. DCF models tend to eliminate many top-quality companies, and there are numerous instances of companies beating the market, despite DCF analysis suggesting they were expensive at the time.

In the model, I assume flat 2024 figures for both margin and revenue growth. After that, I project a 6% increase in revenue and a 100 basis points margin expansion per year. The WACC is set at 8.9%. The model suggests the stock is overvalued by 17%. It's important to note that the model does not take into account the meaningful buybacks MTD is executing, which significantly contribute to EPS growth.

{kind=link}

{kind=link}

Considering the risk/reward scenario, in my view, the stock is a buy, but only for those who have the stomach to hold for the long term. This is not a value play; it's a company to hold and enjoy the compounding effect.

I look forward to your comments.

For further details see:

Mettler-Toledo's 2023 Dip Exposes An Opportunity To Acquire This Compounder At A Discount