MTD - Mettler-Toledo: Sell Theses Missing Some Key Points

Summary

- Mettler-Toledo continues to catch a strong bid as investors recognize the value proposition on offer.

- This is a selective investment opportunity that requires a deeper analysis beyond the publicly-available GAAP accounting statements.

- We demonstrate that MTD is able to sustainably grow post-tax earnings at 10% with only an 8% reinvestment, leaving 92% as distributable cash flows to shareholders.

- This supports its buyback program that's returned >$1Bn to equity holders over the 12 months to Q3 FY22.

- Net-net, we rate MTD a buy.

Investment summary

We are long-term holders of Mettler-Toledo ( MTD ) and have been beneficiaries of its stewardship in capital management. MTD is a prime example of why it is so essential to rigorously scrutinize all of the moving parts in a company's investment debate. Today's report is a gentle push-back to the recent sell-thesis on MTD, highlighting why we believe the stock to be a strong buy. The short report in question was actually very well written, and made some very compelling reports, providing a balanced but factual set of viewpoints. Other neutral stances on MTD posted on Seeking Alpha also do a fantastic job in presenting the company's publicly-available data. We encourage you to read these publications for the most informed investment reasoning possible. Moreover, previously published short reports in 2019 have proven to turn out to be fruitless.

However, we believe much of the available coverage on MTD misses the investment opportunity, doesn't accurately recognize the future growth in FCFE, misses the direct value MTD creates for equityholders through its buyback stream, and looks only at the publicly-available data from GAAP accounting without a deeper analysis. Consequently, here, I'll run through why we believe MTD is set to continue driving future economic value for equityholders into the years to come. Rate buy.

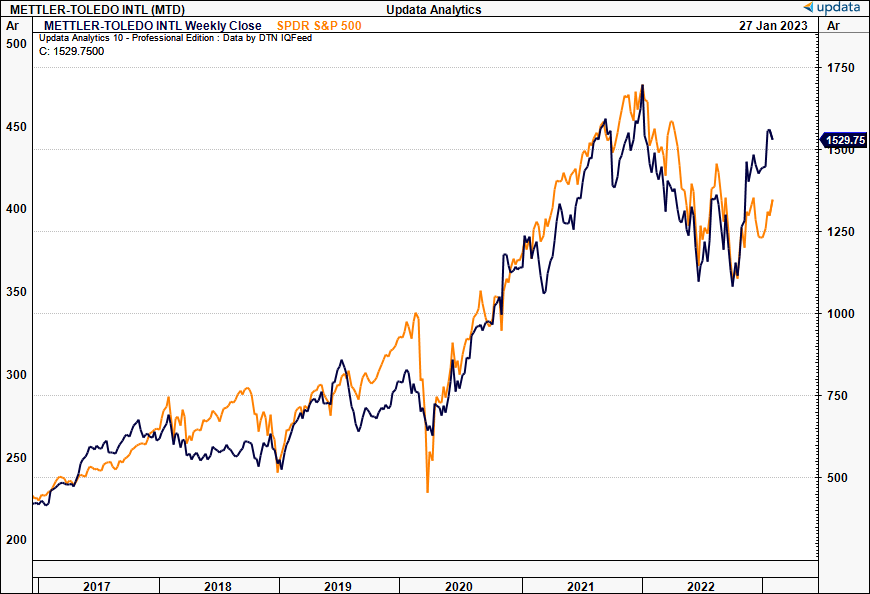

Exhibit 1. MTD 6-year performance against S&P 500, with recent divergence to the upside

{kind=link}

MTD buy thesis, point-by-point

I'll summarize the salient points of our buy thesis in the points below. Note, it's important to realize that there's more to the story to this, including unit economics, the distribution of broad economy's potential outcomes, and central bank tightening policies. Yet, we are holders of MTD based on its strong business model that prioritizes returning capital to shareholders over building out acquisitions.

We've discussed this in our previous publications on MTD, which I've listed here below, in chronological order. I encourage you to read them. See:

With that, our long position is based on the following:

1). Many who are cynical of MTD quote its thin or negative on-balance sheet equity. Yet, a company's valuation, or ability to generate value, has nothing to do with its liabilities exceeding its assets. A company generates corporate and shareholder value when its return on invested capital ("ROIC") exceeds the cost of capital. Warren Buffett labelled this the 'economic moat', but more technically, it is actually a quantifiable measure of competitive advantage. A high ROIC means only a small portion of post-tax earnings is required to fuel high rates of growth, leaving the rest as distributable cash to shareholders. We'd note, here is where the value proposition and alpha opportunity lies for MTD.

2). Note: All of MTD's excess capital is returned to shareholders as buybacks, hence the low/negative equity. It doesn't make acquisitions. Hence, the free cash available to equityholders is miles above what's stated in conventional calculations of FCF that looks at CFFO less CapEx (this calculation also misses a lot of the picture, by estimate). As said, a company generates value for shareholders through a high ROIC, and MTD is absolutely stellar, at 76% for the TTM, on a long-term hurdle rate of ~7-10%.

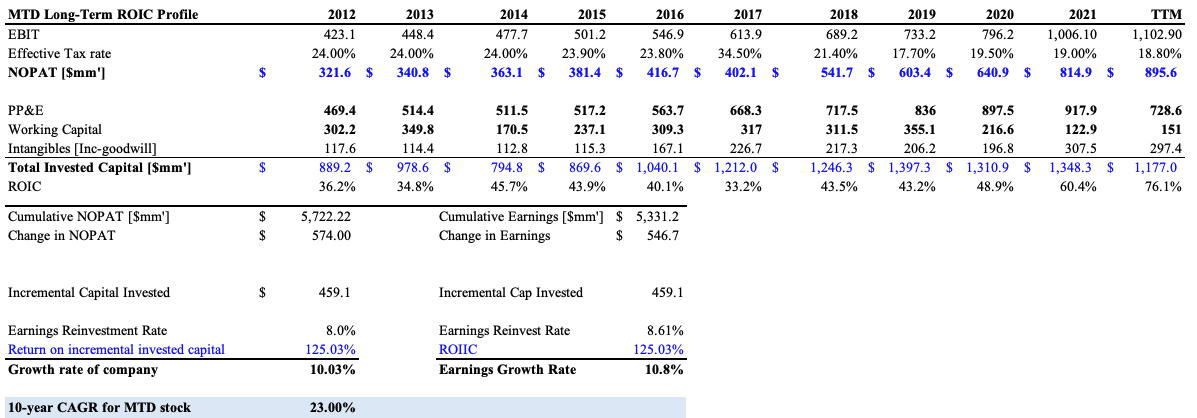

3). Let's break this down for the benefit of our readers. First, MTD generated a cumulative $5.72Bn in NOPAT since 2012 to the trailing 12 months, adding an additional growth of $574mm in NOPAT in that time.

In order to achieve this accumulation and growth in NOPAT, it only had to invest an additional $459mm of capital. That's an astounding 125% in return on incremental invested capital ("ROIIC") over this time. Meaning, the reinvestment rate of post-tax earnings was only 8%, equating to a 10% growth rate of the company per year. This also means 92% of post-tax earnings are distributable to shareholders, in buybacks - a key point that's often overlooked in the negative connotations around MTD's financials.

4). A company can grow at the rate at which it can reinvest, multiplied by its ROIC, and add value if the ROIC is above the cost of capital (see: Damodaran's work , Mckinsey & Co. (2014, 2020), Mauboussin ( 2014 , 2020 , 2022 ), Saber Capital (2016) , Schroders (2021) . Ultimately, this is why MTD can consistently return ~$1Bn in capital each year to shareholders in the form of buybacks - it only needs to reinvest 8% of post-tax net earnings to generate 10% growth, and, as mentioned, this means 92% of residual post-tax earnings is distributable to shareholders via the repurchase/buyback program (Exhibit 2). The economics are the same for its net earnings. The stock has compounded at ~23% per year since FY12, meaning the buyback program has added ~13 percentage points each year in shareholder value, by estimation, evidence of its success to equityholders.

Exhibit 2. MTD only needs to reinvest 8% of post-tax earnings to grow 10% per year, leaving 92% of residual earnings as distributable cash flows to shareholders

{kind=link}

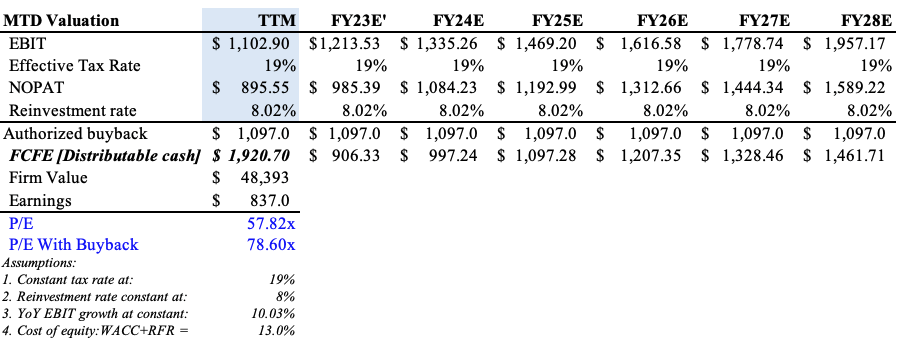

5). The ongoing buybacks also reduce the outstanding share count, reducing available supply, driving the FCFE value per share higher over time as well. Demand and supply mechanics in the marketplace are, therefore, at play too. It's a brilliant strategy, in our best estimation. Based on the above actuals, it can grow at 10% per year sustainably, justifying a 78x P/E (Exhibit 3). Using these numbers with the FCFE, take a discount rate of ~13% to be ultra-conservative - from its current WACC + the current risk-free rate - this still puts MTD at a c.$2,100 per share valuation. Hence, it is substantially undervalued, in our opinion, and will continually grow this valuation as time goes by based on the economics of its buyback program.

Exhibit 3. Sustainable growth rate of ~10%, with reinvestment rate of 8%, leaves substantial free cash available to distribute to equityholders. With the buyback program in place, MTD deserves a high multiple

{kind=link}

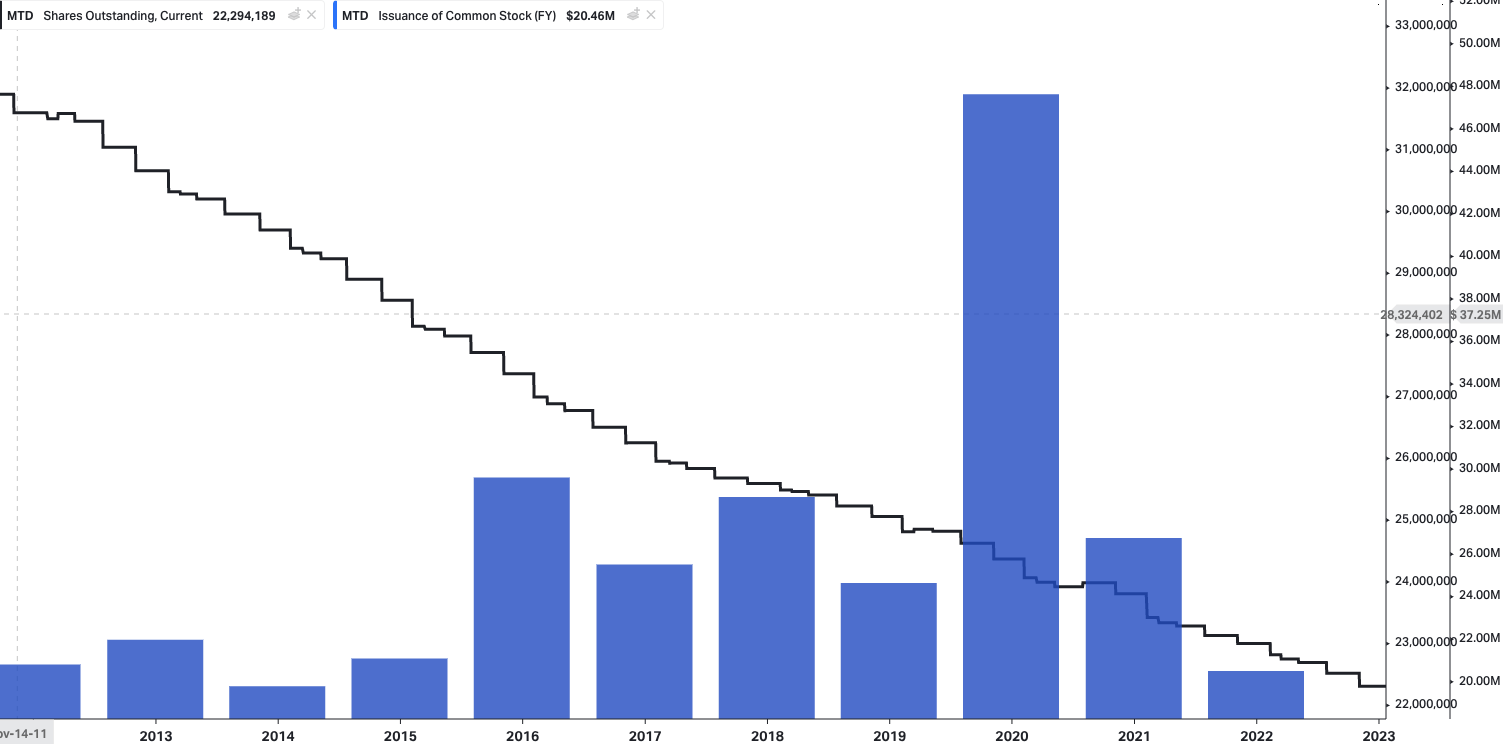

6). Hence, the $1,317/share gain in share price since 2013 and ~$900 per share gain since FY20 is more than justified, in our opinion, and we estimate this trend will continue over the long term. Not to mention, the buyback yield is historically ~7% per annum (we had discussed this at length in our June 2022 report). All whilst the 'balance sheet concerns' remained fully in situ. It would be unwise to short this name, in the best estimation. Instead, we remain long-term holders of the stock, looking to appreciate its buyback over this time.

Exhibit 4. Reduction in share count, versus issuance of common stock

{kind=link}

In short

MTD is a classic example of why it is so essential to understand and analyze the fundamental drivers of growth and shareholder value. This goes beyond the balance sheet or earnings growth, instead linking ROIC, invested capital, and the ability to redistribute free cash to equityholders. MTD's outstanding performance in all 3 of these domains enables it to continuously distribute ~7% of its market cap back in buybacks each period, ~$1Bn in the last 12 months to Q3 FY22. With its FY22 earnings around the corner, we estimate these trends will continue. Rate buy.

For further details see:

Mettler-Toledo: Sell Theses Missing Some Key Points