MTD - Mettler-Toledo: Weak Chinese Pharma And Biopharma Continues To FY24

2023-11-11 05:06:13 ET

Summary

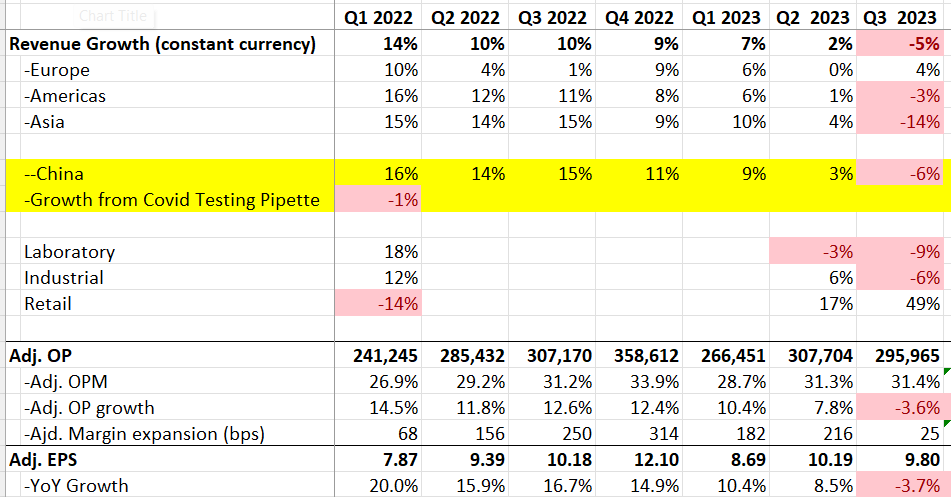

- Mettler-Toledo's Q3 results showed a 5% decrease in revenue and a 3.7% decline in adjusted EPS, largely due to weak performance in China.

- The decline in China is attributed to the impact of the pandemic on the pharmaceutical and biopharma industry, as well as an anti-corruption campaign in the healthcare sector.

- The company expects the slowdown in China to continue in the first half of FY24, with no growth in revenue and a decline in adjusted EPS projected for the year.

I called out the near-term risk of China's deterioration for Mettler-Toledo ( MTD ) in my introductory article back in September. Mettler-Toledo posted a very weak Q3 FY23 result on November 9th, with a -5% decrease in revenue on a constant currency basis and a -3.7% decline in adjusted EPS year over year. I believe the Chinese operation will continue to be weak in FY24, and I maintain the "Sell" rating with the revised fair value of $805.

Quarterly Review and Outlook

In Q3 FY23, their revenue and operating profit declined by 5% and 3.6% year over year, respectively. China operations' revenue dropped by 6% in constant currency, marking the first time it has experienced a decline in recent quarters. The business in China is crucial for Mettler-Toledo's growth, representing 22% of group revenue and 35% of group profits.

{kind=link}

China's decline is inevitable, as I analyzed in my initiation article. I believe the key reasons are as follows. Firstly, the pharmaceutical and biopharma industry in China has been impacted by the pandemic, leading to weak capital investments due to the overall economic downturn in the country. China's zero-covid policy has contributed to a substantial decline in its economy during the pandemic period. Secondly, the Chinese government initiated an anti-corruption campaign in the healthcare industry, targeting hospitals and pharmaceutical companies. These investigations have led to the suspension of many hospital operations, including surgeries. According to the Council on Foreign Relations , as of July 31, 2023, investigations were launched against over 155 hospital chiefs, more than doubling the total from the previous year. Lastly, the pharmaceutical and biopharma industry in Western countries is also experiencing a significant slowdown due to inventory destocking. Some multinational companies in this sector have operations in China, contributing to the adverse impact on China's growth.

In the earnings call , their management expects the slowdown in China to persist in the first half of FY24 but anticipates a moderation in the second half due to a weak comparable. They provided guidance for both FY23 and FY24.

For the full year of FY23, they expect local currency sales to decline by approximately 1%, a downward revision from the previous forecast of 0-1% growth. Free cash flow for the year is now expected to be approximately $875 million, with the total share repurchase estimated to be $900 million in FY23.

As for the FY24 guidance, they anticipate no growth in revenue on a constant currency basis, and adjusted EPS is projected to grow by 2-4% on a constant currency basis. The free cash flow is forecasted to be $850 million in FY24, reflecting a 2.8% decline compared to FY23's guidance. They plan to deploy $850 million in cash for share repurchases in FY24.

Overall, the guidance is notably weak, assuming the continued weakness of their China operations and anticipating challenges in the global pharma and biopharma industry growth. Additionally, in my view, the weak Chinese economy is attributed to both weak domestic consumption and sluggish export and manufacturing growth driven by the global economic slowdown. Therefore, I believe China's weakness could persist for an extended period, beyond just the first half of FY24.

Food Retailing

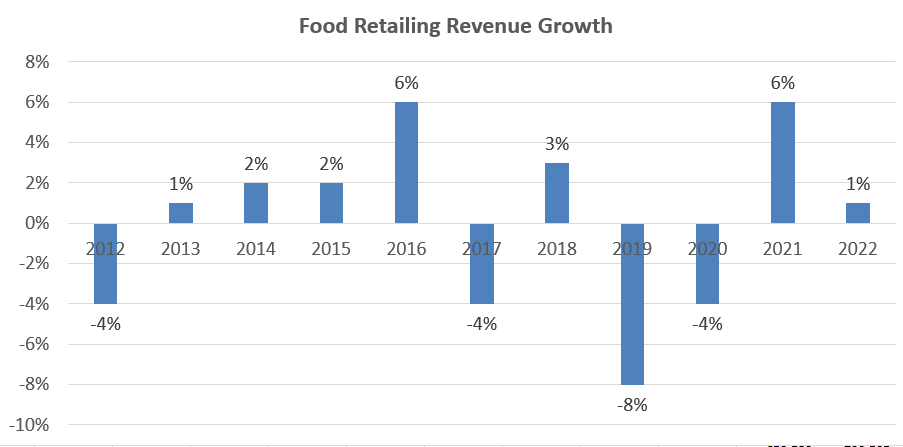

Their food retailing business experienced an unusually high growth rate of 49% in Q3 FY23, a significant departure from its historical trend of almost zero growth on average over the past 10 years. As depicted in the chart below, this exceptional growth in FY23 is anticipated to pose a considerable challenge in FY24 due to tough comparable. During the earnings call, the management attributed this year's growth to the successful penetration of major grocery and club stores. However, they acknowledged the difficulty of maintaining such growth in FY24 and anticipate a modest decline. It's worth noting that food retailing currently represents around 5% of the group's revenue. Despite the recent growth, I consistently believe that this business doesn't align with their overall group strategy, and the business should be divested at some point in the future.

{kind=link}

Valuation Update

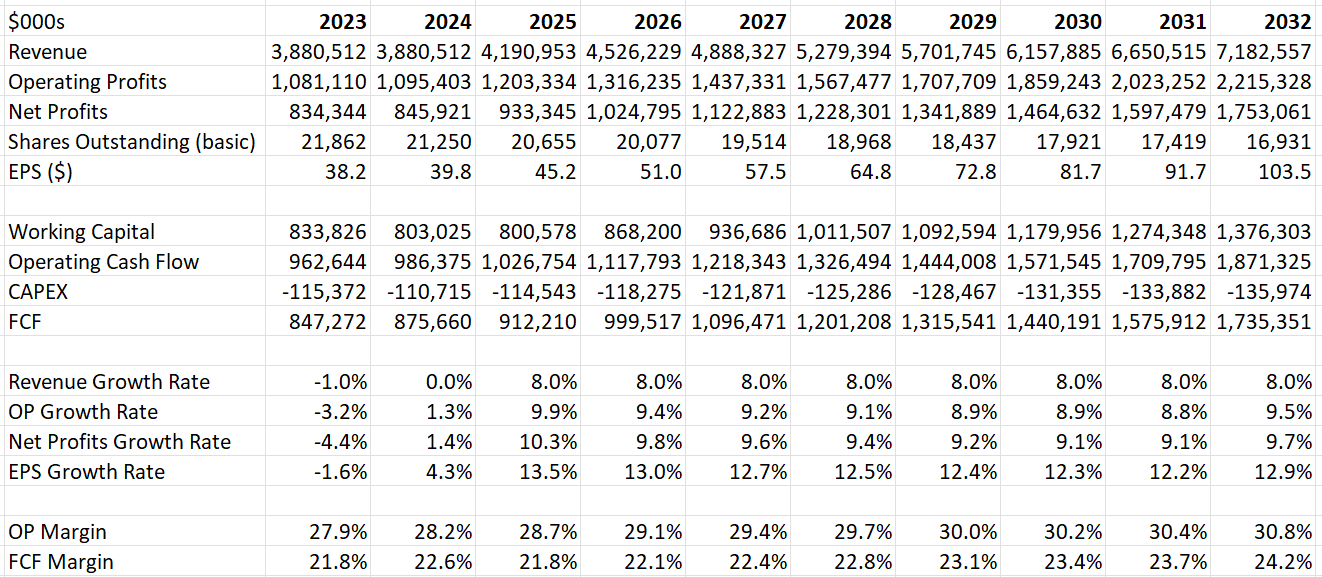

I revised the growth assumptions for FY23 and FY24 to align with their official guidance, which indicates weak growth in both China operations and the global pharma/biopharma industry. I also adjusted the capital spending assumptions for FY23 to align with their guidance. The normalized revenue growth rate of 8% remains intact, as I continue to believe Mettler-Toledo is a high-quality growth company. The 8% revenue growth includes 7% organic revenue growth and 1% acquisition growth.

{kind=link}

The revised fair value of their stock price is projected to be $805, according to my estimate. Consequently, the current stock price is considered overvalued.

Conclusion

Mettler-Toledo delivered a very weak quarterly result and guidance, primarily attributed to weak China growth and a global demand slowdown. I am of the opinion that the China slowdown could persist for an extended period, posing significant growth headwinds for Mettler-Toledo. Given the perceived overvaluation of the stock, I am maintaining the "Sell" rating with a fair price target of $805 per share.

For further details see:

Mettler-Toledo: Weak Chinese Pharma And Biopharma Continues To FY24