MFD - MFD: A Nice Infrastructure CEF With International Exposure

2023-08-18 14:22:52 ET

Summary

- Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund offers a high yield of 10.44% and is trading below its intrinsic value.

- The MFD closed-end fund invests in companies involved in infrastructure and utilities assets, providing stable cash flows and attractive yields.

- The fund is well-diversified internationally, reducing investors' exposure to the United States and offering a potential source of income.

- The fund appears able to sustain its current distribution, as it is fully covered with net investment income and net realized gains.

- The fund historically underperforms a comparable index fund, which is a disappointment.

For many years now, utilities, infrastructure companies, midstream firms, and similar entities have been among the favorite investments of anyone seeking a high level of income from their portfolios. This makes sense as these companies all tend to enjoy remarkably stable cash flows due to the fact that they provide a product that is necessary for modern society to function. In addition, all of them tend to be capital-intensive businesses with relatively slow growth, so they pay out a large proportion of their cash flows to their investors in order to provide an acceptable return that is competitive with many other things in the market.

Unfortunately, there are a few downsides to these companies. One of the most obvious of these is that they tend to not be particularly well-followed by many investors or the financial media. As such, it can be difficult to obtain the information that we would really like to have to conduct research about it. It can also be difficult to even find some of these companies unless we run very specific stock screens. In the case of midstream companies, some of them are structured as master limited partnerships, which can cause tax headaches for American investors that might want to include them in a retirement account. Finally, we also have to contend with the difficulty of putting together a diversified portfolio of these companies, which is a lot of work considering the above problems.

One solution to all of these problems is to purchase shares of a closed-end fund that specializes in investing in infrastructure companies. These funds offer a number of advantages over familiar open-ended or exchange-traded funds. In particular, a closed-end fund, also known as a CEF, is able to employ certain strategies that have the effect of boosting its yield well beyond that of any of the underlying assets. When we consider that many infrastructure companies have very high yields to begin with, we can see how this could very easily result in a very appealing investment for anyone that is seeking a high level of income.

In this article, we will discuss the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund (MFD), which is one closed-end fund that can be used by any investor looking to easily include a diversified portfolio of infrastructure assets in their income-focused portfolio. The fund offers a 10.44% yield at its current price, which should prove quite attractive to anyone that is interested in income as it is well above nearly everything else currently trading in the market. In addition, the fund is currently trading for well below its intrinsic value, so it appears to be at a very good price right now. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund has the objective of providing its investors with a high level of total return. This makes a lot of sense considering that this fund primarily invests in common equity. As we can see here, 53.93% of the fund's portfolio is currently invested in common stock:

CEF Connect

We do see though that it has high allocations to both cash and bond. Indeed, that is one of the highest cash allocations that I have ever seen a closed-end fund possess. This is somewhat disappointing as cash tends to offer a much lower yield than either common stock or bonds. However, this statement may be less true today than it was in the past. As of right now, it is not particularly difficult to get a 5% yield from a money market fund. That is actually well above the 4.264% yield of ten-year Treasuries right now. It is also above the 2.68% yield of the U.S. Utilities Index (IDU). Thus, the cash position may not be as big a drag on the portfolio's ability to generate income as it would have been eighteen months ago when money market yields were much lower. With that said though, it does seem likely that bonds issued by infrastructure companies are probably going to have a yield above 5%, and common equity issued by midstream companies and partnerships certainly does. Thus, the 24.17% allocation to cash is hopefully going to be a temporary condition while the fund's managers look for a better place to deploy it. However, it is not as urgent that the fund, which is presumably trying to maximize its returns, unload it quickly as it was when rates were at 0%.

As the name of the fund implies, the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund seeks to achieve its objective by investing in companies that own electric, natural gas, water, and similar utility infrastructure as well as things such as toll roads, airlines, cellular providers, telecommunications companies, and similar entities. Basically, these are the companies whose products and services allow modern society to function, despite the fact that many of them are companies that are frequently taken for granted. The webpage describes the fund's overall strategy thusly:

"Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund is a diversified, closed-end management investment company. The fund seeks to provide a high level of current return consisting of dividends, interest, and other similar income while attempting to preserve capital. The fund seeks to achieve its investment objective by investing predominately in the securities of companies of companies that are involved in the management, ownership, and/or operation of infrastructure and utilities assets, and are expected to offer reasonably predictable income and attractive yields. The fund also invests in senior secured loans generally considered to be high-yield securities."

Admittedly, this description is not as descriptive as I would like it to be. In particular, the fund does not state what exactly it considers to be a utility or infrastructure company. However, a look at the sectors that are represented in the portfolio answers this question quite well. Here they are:

Macquarie/First Trust

This is largely the definition that I gave preceding the quote. However, there are a few things on here that are quite surprising. For example, it is difficult to see how an aerospace company, a defense contractor, or a media company could possibly be considered "infrastructure." However, these firms account for only a relatively small portion of the fund's portfolio. We can clearly see that electric and gas utilities, telecommunications companies, and midstream companies are the heaviest-weighted sectors here. That, along with toll roads, railroads, and telecommunications companies are pretty much what we would expect to find in an infrastructure fund like this one.

One of the defining characteristics of utility and infrastructure companies is that they tend to enjoy remarkably consistent cash flows and revenues regardless of the conditions in the broader economy. This comes from the fact that their services are considered to be necessities by most people that live in modern society. For example, all of us have become dependent on always having electric service, running water, and heat in our homes and businesses. The same thing largely applies to telecommunications services, as having access to the Internet has become almost essential to most people. As such, they will normally prioritize paying their utility and telecommunications bills ahead of discretionary expenses during periods in which money gets tight.

As I pointed out in a recent blog post , money has been getting very tight for many average American households due to the rapidly rising cost of living brought on by a multi-decade-high rate of inflation. Businesses that should weather this environment largely unscathed are quite useful to include in a portfolio in such an environment.

Midstream companies have similar cash flow stability. This is because their business model is based on long-term contracts with their customers. Under these contracts, a midstream company transports crude oil, natural gas, and other hydrocarbon products on behalf of its customers. In exchange, the customers pay the midstream provider a fee that is based on the volume of resources that are transported, not on their value. This provides the midstream company with a great deal of insulation against fluctuations in energy prices, which can be quite volatile. These contracts also typically specify a minimum volume of resources that must be transported through the midstream company's infrastructure or paid for anyway. This protects the midstream company against production declines that might accompany a fall in energy prices. The minimum volume commitment also provides the midstream company with a certain minimum level of cash flow, which it can use to support its distribution.

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort to discussing utilities, midstream companies, and various other infrastructure companies over the years. As such, the largest positions in the portfolio will probably be familiar to most readers. Here they are:

Macquarie/First Trust

We see a few utilities here that I have discussed, including National Grid (NGG), Sempra Energy (SRE), and Eversource Energy (ES). We also see Enbridge (ENB) and TC Energy (TRP), which are two of the largest midstream companies in North America. Interestingly though, we do not see any of the large midstream partnerships like MPLX LP (MPLX) that could be better investments than some of these companies. In fact, the only master limited partnership in the portfolio as of May 31, 2023, was Enterprise Products Partners L.P. (EPD). The fund might be avoiding these assets for regulatory reasons, as I can find no evidence that this fund is structured as a corporation. That structure would be necessary if it wishes to include master limited partnerships to any significant degree.

One of the nice things here, though, is that the fund is fairly well-diversified internationally. We expect this from a Macquarie fund as Macquarie itself is an Australian company and it is well-known for its infrastructure funds that focus heavily on assets outside of the United States. As of right now, only 40.30% of the fund's assets are invested in American companies:

Macquarie/First Trust

This is something that is very nice to see. As I have pointed out in numerous previous articles, most American investors are far too heavily exposed to the United States. This is partly because American markets have outperformed most foreign ones over the past decade, but it represents a very big risk. This is because most Americans receive a substantial portion of their income from Social Security or a job in the United States. If their assets are also nearly all in the United States, as is the case with most Americans, then any sort of domestic economic or political problem could wipe out their incomes and assets. An investor that is well diversified internationally can reduce their risks of adverse consequences from domestic problems. This fund appears to be one way to achieve that diversification as it overweighs foreign assets so its inclusion in a portfolio will reduce an investor's domestic exposure across the whole portfolio.

One of the big problems with actively managed funds is that they frequently underperform comparable index funds. The primary reason for this is that actively managed funds have much higher expenses than funds that simply mechanically buy every stock in an index. This fund is certainly no exception to the rule, as its expense ratio is 2.66% compared to 0.41% for the iShares Global Infrastructure ETF (IGF). The Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund has also underperformed the index fund over time. This chart shows the ten-year total return of both assets:

{kind=link}

As we can see, the index fund has substantially outperformed the closed-end fund over the ten-year period. However, it is important to keep in mind that this performance comparison assumes that all of the distributions paid by both funds were fully reinvested. Many income-seeking investors will not do that, and the closed-end fund has a substantially higher yield than the index fund. As of the time of writing, the index fund only yields 2.65% compared to 10.44% of the closed-end fund. Thus, the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund might still appeal to some investors that are seeking income, despite the lower total return.

Leverage

In the introduction to this article, I stated that closed-end funds have the ability to employ certain strategies that can boost their effective yields well beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund is borrowing money and using those borrowed monies to purchase common equity and fixed-income securities that are issued by infrastructure companies. As long as the purchased securities deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective return of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, so that will usually be the case. It is important to note though that this strategy is not as effective at boosting returns today with rates at 6% as it was eighteen months ago when rates were at 0%. This is because the difference between the interest rate that the fund has to pay on the borrowed money and the return that it can receive from the purchased assets is much narrower than it once was.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt because that would expose us to too much risk. I generally do not like a fund's leverage to exceed a third as a percentage of its assets for this reason. Fortunately, this fund is currently satisfying that requirement. As of the time of writing, the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund has levered assets comprising 27.22% of the portfolio. Thus, it appears that this fund is striking a reasonable balance between risk and reward. We should not have to worry too much about the fund's debt today.

Distribution Analysis

As mentioned earlier in this article, one of the reasons why investors purchase utilities and similar companies is that they tend to have fairly high dividend yields. This comes from the simple fact that they are in capital-intensive businesses with relatively low growth and limited internal investment opportunities. As such, they pay out a relatively high proportion of their cash flows to their investors in order to provide a reasonable return. The market tends to not assign particularly high multiples to these companies due to their growth, so the dividends and distributions end up being a substantial percentage of their share prices. The Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund purchases shares of these companies and then applies a layer of leverage to boost the effective yield of its portfolio. As is the case with all closed-end funds, it then pays out a significant portion of its investment profits to its shareholders in the form of distributions.

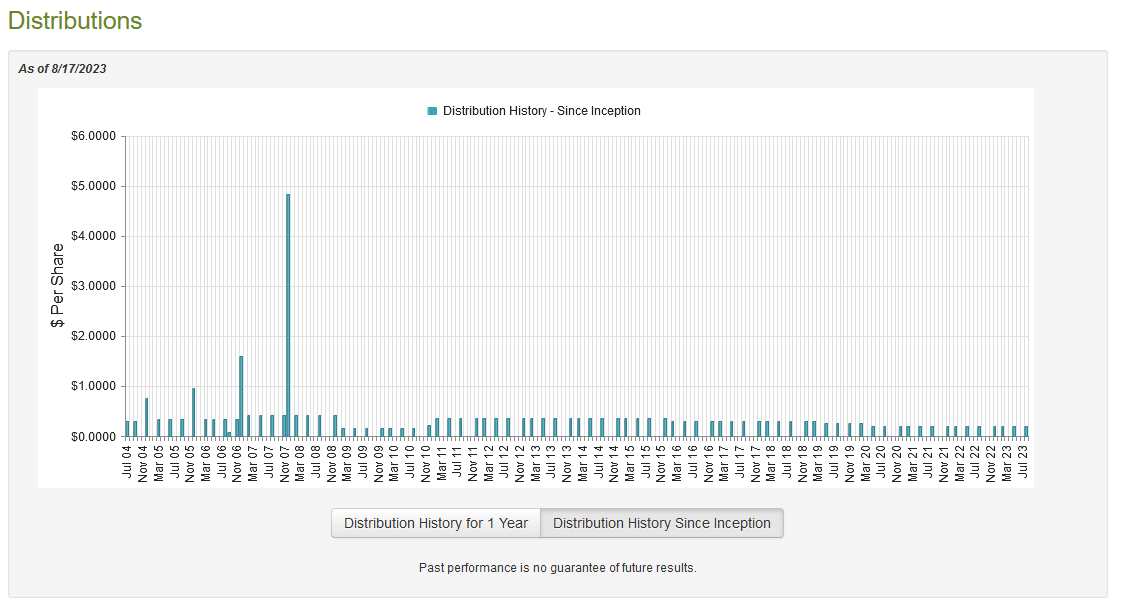

As such, we might assume that this fund would have a very high distribution yield itself. That is certainly the case, as the fund pays a quarterly distribution of $0.20 per share ($0.80 per share annually), which gives it a 10.44% yield at the current price. Unfortunately, the fund has not been especially consistent with its distribution over the years. In fact, it has varied quite a bit:

{kind=link}

This variation in the fund's distribution is almost certainly going to be a bit of a turn-off to those investors that are seeking a stable and secure source of income to pay their bills and finance their lifestyles. However, it is understandable that the fund would have to vary its distribution with time. After all, the fund is basically attempting to pay out its investment profits while keeping its asset base relatively stable. Its investment profits will certainly not be stable over time though, as we have seen two major market crashes over the past fifteen years as well as a few periods of sustained low returns.

Indeed, considering the current valuation of the American stock market and the fact that investors tend to get more conservative as they age, it is quite possible that the market returns over the next decade will be somewhat lower than we saw from 2010 to 2023. It is not sustainable for the fund to pay out more than its actual investment returns since that would drain its asset base and make it more difficult to earn sufficient returns to cover its distribution in future years.

As I have pointed out in numerous previous articles, the fund's past is not necessarily the most important thing for new investors. After all, anyone that buys the fund today will receive the current distribution at the current yield. A new investor will not be negatively impacted by the fund's performance in the past. As such, the most important thing for our purposes today is determining how well the fund can sustain its current distribution.

Fortunately, we have a very recent document that we can consult for that purpose. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is one of the newest financial reports available from any closed-end fund, and it should give us an idea of how well the fund performed over most of the first half of this year. This is something that we can find quite useful as the market this year has generally been stronger than it was over 2022 so the fund may have had some opportunities to earn capital gains.

During the six-month period, the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund received $2,057,865 in dividends along with $1,209,027 in interest from the investments in its portfolio. When we combine this with a small amount of income from other sources, the fund reported a total investment income of $3,294,610 during the six-month period. It paid its expenses out of this amount, which left it with $1,776,822 available for shareholders. As might be expected, that was not enough to cover the $3,418,977 that the fund actually paid out during the period. At first glance, this is something that could be quite concerning as the fund did not have sufficient net investment income to cover its payouts.

However, a fund like this does have other methods that can be employed to obtain the money that it needs to cover its distributions. For example, it might have been able to generate some capital gains that can be paid out to the investors. The fund actually had mixed results here as it reported net realized gains of $1,662,219 but these were more than offset by $3,977,298 net unrealized losses. Overall, the fund's assets declined by $3,957,234 during the period. This is disappointing as it implies that the fund did not manage to cover its distributions. However, the fund's net investment income plus net realized gains totaled $3,439,041, which was enough to fully cover the distribution.

Thus, the unrealized losses were the only real cause of the fund's net asset decline and those are not really a big deal until the fund sells them and locks in the losses. Overall, the distribution is probably safe at the current level, especially if the fund can hold the securities with unrealized losses until they return to positive territory.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a closed-end fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, fortunately, the case right now. As of August 17, 2023 (the most recent date for which data is available as of the time of writing), the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund has a net asset value of $8.62 per share but the shares currently trade for $7.63 each. This gives the fund's shares an 11.48% discount on net asset value at the current price. That is not as attractive as the 12.40% discount that the fund's shares have averaged over the past month, but a double-digit discount is still an attractive price to pay for any fund. As such, the price looks quite reasonable today for anyone that wants this fund.

Conclusion

In conclusion, infrastructure companies and utilities can be quite attractive holdings for any income investor due to their high yields and stable cash flows. The Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund provides an easy way to get exposure to these assets and diversify your portfolio internationally at the same time. The only real problem with the Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income fund is that it underperforms the Global Infrastructure Index, but it has a substantially higher yield and that might make some investors favor this fund over the index.

For further details see:

MFD: A Nice Infrastructure CEF With International Exposure