MGPI - MGP Ingredients: No Margin Of Safety

Summary

- Investors re-rated $2.1 billion market cap MGP after the 2021 purchase of Luxco, owner of a stable of higher-margin niche market branded spirits, almost doubled annual sales.

- Comparable acquisition-adjusted sales are up about 13%, but gross profit is only up about 10% due to lower margins - still a good result.

- Adjusted 3Q2022 results were flat to 2021 with lower margins due to higher input prices in corn, wheat and natural gas and increased advertising expense.

- The stock ran from the mid-$70s in February 2022 to over $120 in December 2022 before dropping to the current level in the high $90s.

- Based on conservative valuation metrics, the stock is over-valued and should trade a good 20 to 30 points lower to be attractive to value investors.

MGP Ingredients, Inc. (MGPI) is a low-profile producer of distilled spirits sold under its own brands and private labels, industrial alcohol and food ingredients. With a market cap of $2.1 billion as of January 31, 2023, the company has not exactly been a growth story; it just qualifies as a mid-cap (> $2.0 billion market cap per Investopedia ) even though it's been distilling spirits since 1941. After 79 years, however, it's time to re-evaluate the future prospects of MGP as an investment. Hint: The recent strong growth wasn't all from distilling a few extra barrels of spirits, selling more texturized wheat protein or increased COVID-related drinking at home.

Look at the stock price over the past three years.

What's going here?

A Tale of Two MGPs

A more than cursory look reveals two MGPs; one before the $475.0 million purchase of St. Louis-based Luxco, a producer, bottler, importer and marketer of a portfolio of alcoholic beverage brands, and one after.

Before the Luxco purchase, MGP annual sales grew at a 4.4% CAGR from $318.3 million in 2016 to $395.5 million in 2020. Net income grew at a 5.3% CAGR from $31.2 million to $40.3 million over the same period. The average mega-cap consumer staples company would be extremely happy about organic growth at these rates, but with MGP we're talking about a relatively old company growing off a very low base. In other words, pretty good, but nothing amazing.

Sometime in 2020, management decided they needed to do something to re-invigorate the company and build shareholder value a little faster. MGP had produced and sold its own private label brands, but according to the Whiskey Advocate :

And while MGP has made forays into offering its own-brand whiskeys under the Rossville Union rye, George Remus bourbon, and Eight & Sand American whiskey labels, progress has been slow. They're only available in some states and-despite reflecting the high quality turned out by the distillery (Remus Repeal Reserve regularly scores above 90 in the Buying Guide)-aren't nearly as well-known as other brands made on the very same stills.

So, according to the Shareholder Letter in the 2020 MGP Annual Report :

We also spent considerable time during the year evaluating opportunities to increase the long-term value creation for our shareholders by adding products to our portfolio that provide higher margins and more predictable revenue and earnings capability in attractive categories. As a result, in January of 2021 we announced a definitive merger agreement with Luxco, Inc., a branded spirits company with a 60-year history of success. This transaction provides the opportunity to more fully participate in the branded spirits category on a national and international level, and adds meaningful diversification to our overall business. We believe this transaction will allow for future growth, both organically as we continue to invest in the brands, as well as providing a platform for future acquisition opportunities.

The acquisition materially changed the company. The "old" MGP was gone; in its place, a very different company. Even though Luxco was only included in MGP's financials beginning April 1, 2021, year-end revenue hit $626.7 million with net income of $90.8 million.

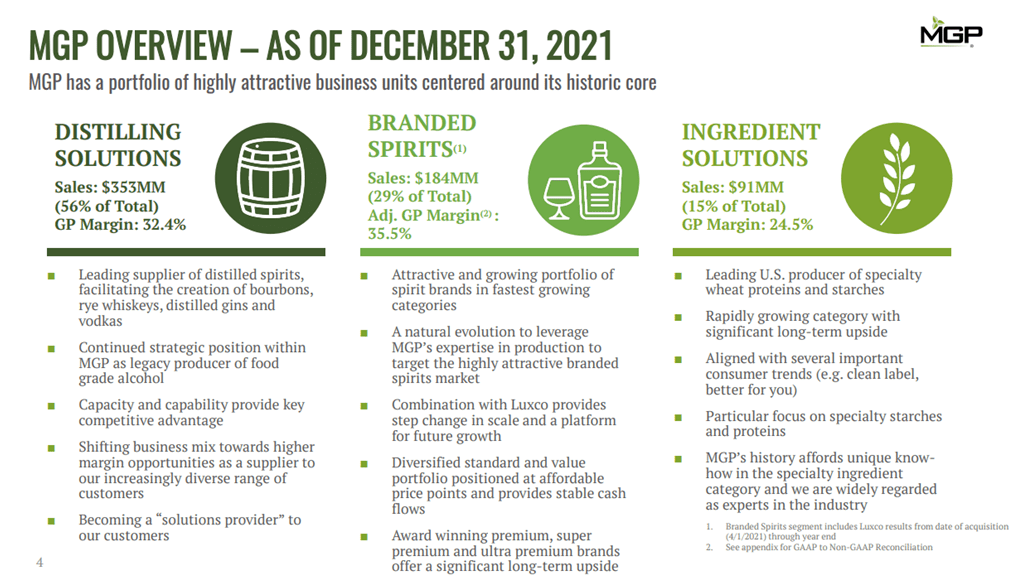

Management described the "new" MGP in the following slide from the third quarter 2022 Investor Presentation :

{kind=link}

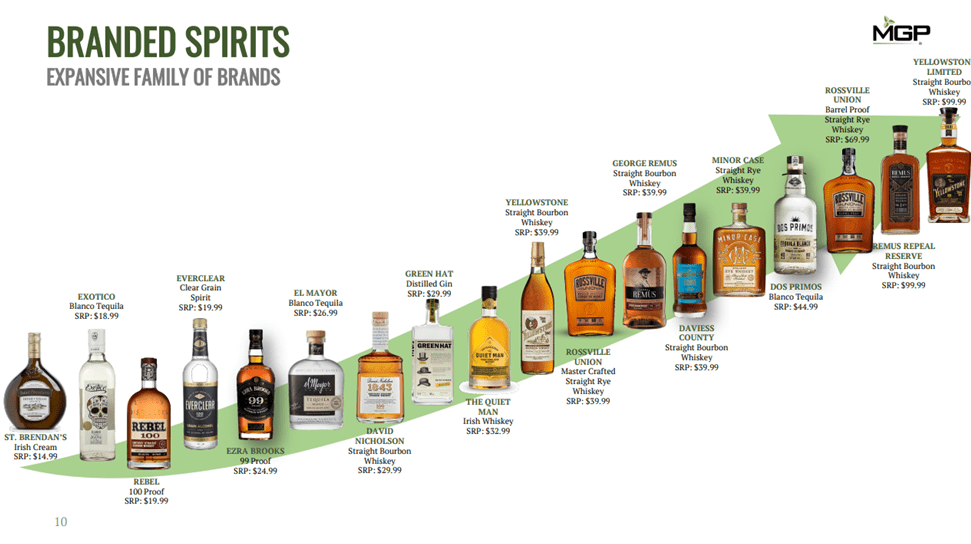

A key element of the Luxco acquisition was the expansion of MGP's higher margin Branded Spirits portfolio - note the estimated 35.5% adjusted gross profit margin in the slide above. However, post-acquisition, MGP's adjusted gross profit margin for Branded Spirits actually declined from 52.7% in 2020. The key difference is that the Luxco acquisition added scale - including mid-priced and value brands while MGP had previously concentrated on the premium segment. MGP sacrificed margin for volume as sales in the segment increased from $2.2 million to $65.2 million in 2021. After the acquisition, here are a few of the company's brands at various price points:

{kind=link}

Although a number of MGP's whiskeys (the majority of branded sales) score well with Whiskey Advocate - notably the reserve editions of Yellowstone, Remus, Rossville and Rebel - most are still niche products that are not as well-known as the competition.

Let's take a closer look at 2022's numbers and see what we can learn.

MGP IS Different, But Is It Better?

Year-over-year comparisons between 2022 and 2021 overstate growth since Luxco was not consolidated with MGP for the first quarter of 2021. Nevertheless, YTD September 30, 2022 sales of $591.4 million were up $131.5 million or 28.6% over $459.9 million in 2021. Net income was up $27.2 million or 45.9% over the same period. Obviously, we can't just accept these numbers as organic growth and move on.

Instead, let's perform an ad hoc, custom analysis and combine 2Q2022 with 3Q2022 for comparison with the combined comparable quarters in 2021.

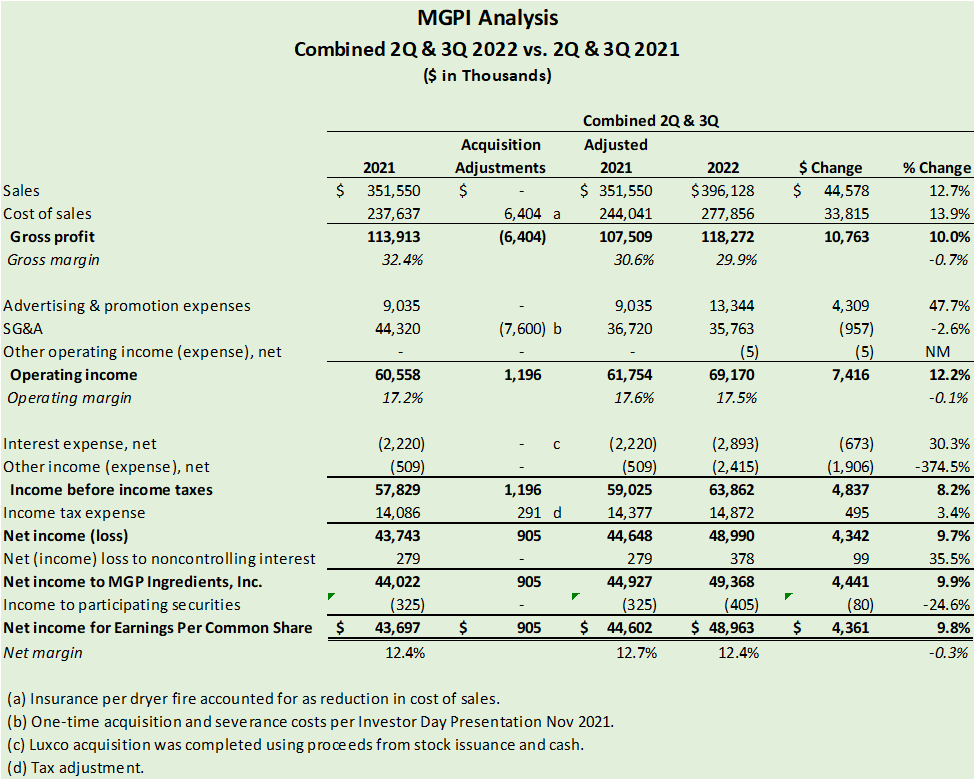

{kind=link}

The adjusted results for the comparable second and third quarters of 2022 vs. 2021 generally support the idea that the Luxco acquisition reduced margins in return for accelerated growth and scale, but the spike in MGP's primary inputs, corn, wheat and natural gas, certainly added to the squeeze:

- Sales increased $44.6 million or 12.7%.

- Gross profit increased $10.8 million or 10.0%, but the gross margin slipped from 30.6% to 29.9%.

- Operating income increased $7.4 million or 12.2%, but the operating margin declined very slightly to 17.5%.

- The net margin declined from 12.7% to 12.4%.

- Finally note the 47.7% increase in advertising. Building volume in a liquor brand requires a very large investment in advertising and marketing. For example, consider Diageo's ( DEO ) ubiquitous Captain Morgan commercials.

If we tighten the focus to the third quarter of 2022, the story becomes a bit more nuanced. We can see the increasing impact of commodity prices, principally corn, wheat and natural gas, on MGP's earnings - and that sales growth has not come from where management might have planned.

{kind=link}

MGP, per the 3Q2022 10-Q , purchases "grain, wheat flour, and natural gas, respectively, for delivery from one to 24 months into the future at negotiated prices." The company, however, does not hedge commodity costs beyond these futures contracts. As a result, the 3.0% decline in gross margin to 29.4% probably at least partly resulted from the spike in corn, wheat and natural gas prices due to the Ukraine war.

Surprisingly, the strong sales increases are not coming from the Branded Spirits segment acquired with Luxco - at least through YTD 3Q2022:

- Sales increased $24.5 million or 13.9%, but not as might have been expected. Sales were up just 2.0% in the Branded Spirits segment, while sales were up 19.0% in the legacy Distilling Solutions segment and 24.0% in the Ingredient Solutions segment.

- Operating income (adjusted for a small amount of acquisition expenses) was up just $686,000 and the operating margin fell to 16.8% due to a $1.6 million or 28.5% increase in advertising.

- The adjusted net margin declined from 13.5% to 11.7%, with adjusted net income available to common shareholders actually declining $303,00 to $23.6 million.

It's too early for the final verdict on the Luxco deal, but there are valid questions. MGP's organic growth YTD 3Q 2022 seems to have come from its legacy business segments. There was an initial "pop" in Branded Spirits - 44.0% unadjusted growth YTD 3Q2022 compared to the prior year which was lacking Luxco until after April 1 - essentially an unsound comparison. It appears - with the information we have at this time - that MGP bought slower-growing sales in Branded Spirits while its legacy business has supplied the 13% to 14% topline sales growth we see in our analyses. Not what we would have expected.

Family Connections

MGP was founded in 1941 by Cloud L. Cray, Sr. as a grain distillery operating in Atchison, Kansas, and Lawrenceburg, Indiana. Members of the founding family and relatives maintain a fairly tight degree of control over the company. MGP has a class of preferred stock, but it is held, according to the MGP website , "by members of the Cray family and/or their designees" and is apparently not registered with the SEC. The preferred stockholders are entitled to elect five of the company's nine directors. Further, only preferred stockholders are entitled to vote on mergers, dissolutions, leases, exchanges or sales of substantially all of the company's assets or amendments to the articles of incorporation, unless the vote would change the amounts outstanding or rights of the common or preferred stock.

Board members include Karen Seaberg, daughter of founder Cloud Cray and her daughter Lori Mingus. According to the January 27, 2023 Form 13D/A filing Seaberg controls about 14.2% of MGP common stock and, along with Thomas M. Cray, her cousin, 93.4% of MGP preferred stock. Seaberg, who is 74 years old and is undoubtedly estate planning, has been a consistent seller of MGP common stock above $100.00 per share, but she has not sold any of her preferred stock.

Per the April 13, 2022 MGP Proxy Statement the Lux family, relatives of Paul Lux, one of the founders of Luxco, own about 22.8% of MGP common stock. The Lux group has the right to elect two directors to the board as long as they own 15% or more of the company's shares and one director as long as they own between 10.0% and 15.0%.

At this point, there can be no M&A activity or changes to the company's charter without the agreement of the Seaberg/Cray preferred stockholders - and with a combined 37% of the common stock and seven directors between them - other major corporate actions would be difficult as well. While the situation limits corporate flexibility, a presumed benefit is the alignment of the interests of the family groups and shareholders in maximizing shareholder value.

Capital Management and Allocation

MGP has a tradition of conservative capital management . The Luxco acquisition was financed with cash on hand plus borrowing under MGP's existing revolving credit facility. The new credit facility balances were refinanced by the private sale in November 2021 of $201.3 million in 1.875% convertible senior notes due in 2041. There are two other minor debt tranches outstanding that bring total debt to $226.3 million as of the end of 3Q2022. With stable cash flows and 3Q2022 net debt to EBITDA ratio of only 1.3, MGP's "access to capital remains robust" as stated in the 3Q2022 10-Q . The company has $400.0 million in capacity through a flexible credit agreement and approval for an additional $120.0 million in private placement notes. There is plenty of ammo for another acquisition or two.

Management stated the company's capital allocation priorities in the MGP 3Q2022 Investor Presentation.

{kind=link}

MGP is not generous about returning capital to shareholders. Many closely-held companies do not pay significant dividends, for example, see my Seeking Alpha article on Grupo Bimbo. MGP pays a minimal dividend of $0.48 per year, a yield of about 0.49%. The payout ratio hovers around 10.0% even though the dividend has increased at a 24.57% CAGR for the past five years. There is room for dramatic increases, but don't bet on it.

The only stock buybacks completed by MGP are in connection with withholding taxes on employee restricted stock grants.

Valuation

I think MGP is currently over-valued.

According to Seeking Alpha , the average Wall Street analyst price target is $126.57 per share, 29.3% above the closing price of $97.87 per share as of February 1, 2023. With a consensus EPS estimate of $5.05 for 2023, that's a forward PE of 19. Diageo, arguably the best alcoholic drink company in the world, trades at a forward PE of 21, has grown net income at a 5.49% CAGR for the past three years from a huge base and offers a 2.05% dividend. MGP is growing faster - from an immensely smaller base - but it seems that growth is coming from its legacy distilling and ingredients operations, not the 29% of sales associated with Branded Spirits. Should it really trade at a premium to Diageo?

Seeking Alpha's Authors and Quant Ratings both rank MGP as a "Hold" while Wall Street analysts see the stock as a "Strong Buy." Note the "F" for Valuation in the Factor Grades:

Seeking Alpha

Finally, I ran a very simplistic discounted cash flow model for MGP as another reality check. Here are the results:

{kind=link}

A 12.0% growth rate for 5 years is very generous, as is the 16x terminal multiple - the long-term PE of the market per S&P. The 10% discount rate is my personal hurdle rate for stock investments. The result is $59.25 per share, about 40% below the current stock price.

Conclusion

I was interested in MGP as a financially stable, but growing recession-resistant consumer products play, but I ran into a number of concerns:

- Branded Spirits are growing slowly and will require increased advertising, marketing and promotion to grow faster. Diageo spent about 12.0% of sales on these items for fiscal 2022, YTD 3Q2022, MGP spent about 3.2%.

- MGP's products depend on the prices of corn, wheat and natural gas - all of which will continue to be subjected to inflation and/or price shocks for an uncertain amount of time. Margins will be under pressure.

- The Seaberg/Cray and Lux family dynamics are a wild card impacting all corporate decisions.

- The valuation is stretched and the dividend does not provide support for the stock price in a downturn.

It will take time for the Luxco acquisition to prove its worth through growth in the higher margin Branded Spirits segment - the rationale for the deal. In the interim, the legacy segments will be under margin pressure. I see growth slowing, Wall Street becoming disenchanted and the price hitting $60.00 to $70.00 per share as the stock re-rates to a 12 to 14 PE. As a conservative, value-oriented investor with a 3 to 5-year investment horizon, I don't see Seth Klarman's famous "margin of safety" at the current price.

For further details see:

MGP Ingredients: No Margin Of Safety