MGDDY - Michelin: Global Leader That Should Keep Rolling

2023-05-23 16:38:05 ET

Summary

- Michelin continues to be a great long-term investment with Q1 2023 sales up 7.4% YoY with the company proving resilient through COVID and the Ukraine conflict.

- As a global industry leader with a great brand, Michelin is highly profitable with ROE of 12.5% and ROIC of 12.4% since 2008.

- The company recently increased the annual dividends to €1.25 per share (an 11% increase) with more room to grow at only a 42% payout ratio.

- Cyclically adjusted investors' ROE points to 10.4% potential long-term shareholder returns at the current price before considering growth.

Michelin ( MGDDY ) is back on my radar to dollar cost average down into as the company continues to perform along the lines of my long-term investment thesis, despite COVID and the Ukraine conflict. The company is currently trading at 9.5x forward P/E and comes with a solid dividend yield of 4.5%. Since I last wrote about Michelin in June 2020 , the company has provided total returns of 36.6%. In Q1 2023 , the company reported strong results with sales up 7.4% and increased the dividend to €1.25 per share (an 11% increase).

Compared to other tire manufacturers, Michelin continues to be my favorite compared to other companies such as Goodyear ( GT ) or Continental ( CTTAY ) due to its strong operations and pricing power of the globally respected Michelin brand. This article will discuss Michelin's strong potential as a long-term investment with 10.5% returns before considering growth.

Updates on Michelin's Results

Like many other European companies, Michelin was hit with the COVID pandemic and now the Ukraine conflict. The company has recovered well from both and in the latest Q1 2023 quarter Michelin reposted a 7.4% increase in revenues to €7.0 billion. The company maintained its full year guidance for 2023 with sales expected to be flat to down 4% with operating cash flows and free cash flows €3.2 and €1.6 billion respectively.

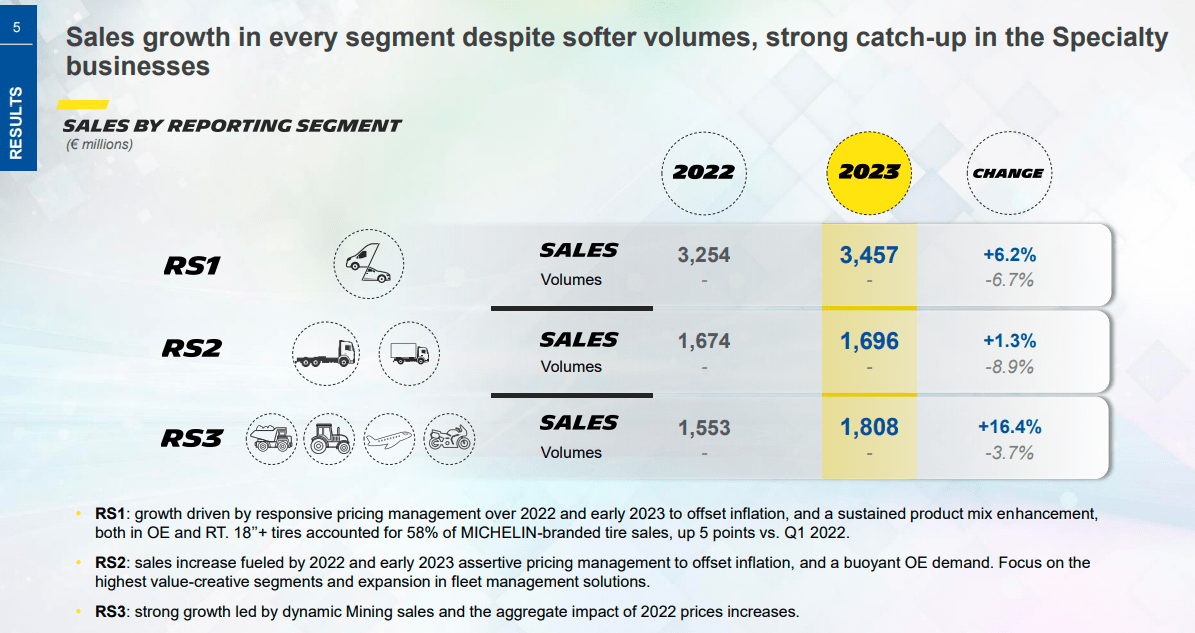

Michelin's results were driven by a 12.3% price-mix effect partially offset by a 6.6% volume decline. The positive price mix effect was driven by growth in the company's high-value segments and strong Mining tire sales (RS3 +16.4%) helping drive the average price-to-volume higher for the quarter. The volume decline was driven by a 25% decrease in Eastern European sales.

Michelin Sales Growth by Customer Type (company Q1 2023 investor presentation)

{kind=link}

A Profitable And Growing Business

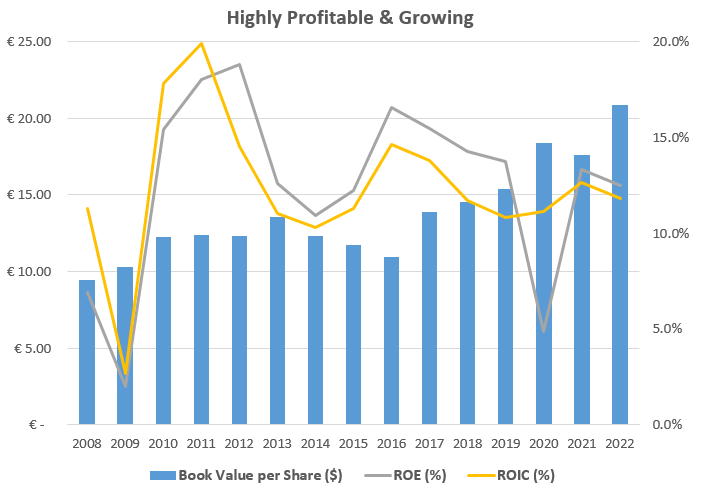

Michelin's strong operations and product portfolio have allowed the company to achieve average return on equity and return on invested capital of 12.5% and 12.4%, respectively, since 2008. While the company is cyclical along with the automotive industry (as witnessed by thin net income margins seen in 2008/2009), this average level of profitability is well above my rule of thumb of 9% ROIC, allowing me to be confident that, in my opinion, the company is able to maintain and continue to increase its intrinsic value over a business cycle. Also notable is that in over a decade the company has not reported a net income loss in any year.

Michelin's Profitability and Book Value Growth (complied by author from company financials)

{kind=link}

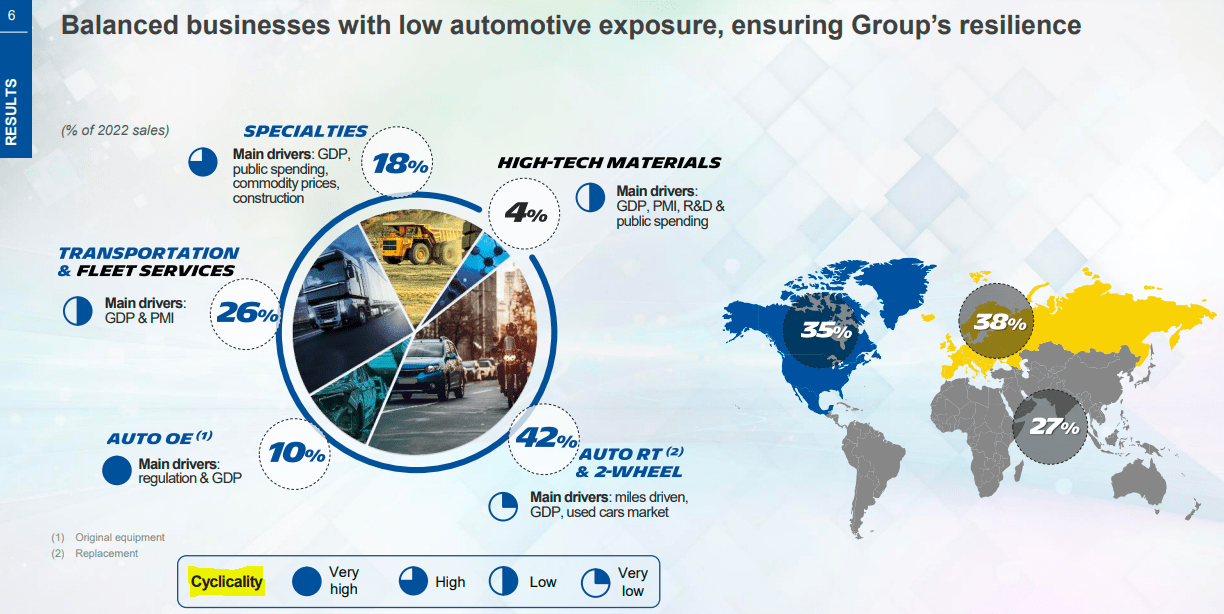

The cyclicality of the company is known and accounted for by management in their financial planning. Michelin is a global giant with a sales breakdown of 38% for Europe, 35% for North America and 27% for the rest of the world as can be seen below. The company breaks down their sales into multiple segments and rates each with a different level of cyclicality. Forecasts across the various sales departments are what builds up to the -4% to flat sales change expected for the full 2023 year mentioned earlier.

Michelin's Sales Mix (company Q1 2023 investor presentation)

{kind=link}

Conservatively Leveraged

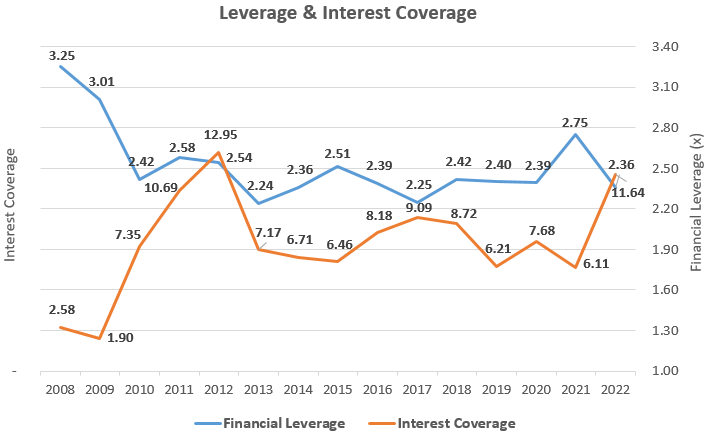

Financial leverage is extra important when considering an investment in a cyclical company. Michelin is conservatively financed with financial leverage currently at 2.39x and their interest coverage ratio a healthy 11.64x. This level of financial leverage is below the 3.25x the company had entering the 2008 recession which makes me feel comfortable that Michelin should be able to handle a potential turn of their business cycle.

Michelin's Leverage and Interest Coverage (complied by author from company financials)

{kind=link}

As outlined in the earlier snapshot from Michelin's Q1 presentation, certain aspects of their business are less cyclical with replacement sales being driven by cumulative miles of tires on the road. Other aspects of the business such as new sales into the OE market are very cyclical as these are new car sales which can be deferred. These diversified sale drivers and healthy leverage ratios make Michelin look well positioned for whatever the economy brings next.

Price Ratios and Potential Returns

I also always like to examine the relationship between average ROE and price-to-book value in what I call the Investors' Adjusted ROE . Investors' Adjusted ROE examines the average ROE over a business cycle and adjusts that ROE for the price investors are currently paying for the company's book value or equity per share. This relationship is especially important for cyclical companies and something I consider similar to Shiller's CAPE ratio but a little simpler to calculate in my opinion.

It examines the average ROE over a business cycle and adjusts that ROE for the price investors are currently paying for the company's book value or equity per share. With Michelin earning an average ROE of 12.5% since 2008 and the shares currently trading at a price to book value of 1.21x when the price is €27.99, this would yield an adjusted ROE of 10.4% for an investor's equity at that €27.99 purchase price, if history repeats itself. This is above the 9% that I like to see and adding a 3% growth rate to represent the company growing alongside GDP could increase this potential total return up to 13.4%.

This €27.99/share price in the calculation is from the company's share price on the Paris stock exchange but the over-the-counter MGDDY found in the U.S. at $15.04 is liquid enough for my retail investing needs with +115,000 share volume on average daily.

Potential Shareholder Returns from Michelin (complied by author from company financials)

Conclusion

The shares of Michelin are looking attractive for me and I will be looking to add to my current position on any market weakness. At only 9.5x forward P/E, long-term investors could be handsomely rewarded if the company repeats its performance over the next business cycle. The company's low financial leverage gives it a strong position to ride out the next business cycle and the 4.5% dividend should provide investors a nice cash flow as they enjoy the growth of this global business.

For further details see:

Michelin: Global Leader That Should Keep Rolling