QRVO - Microchip: Filtering Out The AI Hype

2023-07-24 12:01:35 ET

Summary

- The stock prices of Nvidia and Microchip Technology have shown some correlation, with the latter benefiting from the popularization of Generative AI tools like ChatGPT.

- The use of Generative AI is expected to result in productivity gains of 24% in the 2022-2040 period, according to a report by a research firm.

- Using joint-demand economics, there are also additional sales opportunities for Microchip's Data Center and Computing segment.

- However, before digesting these prospects, it is important to filter out the hype or providing a picture of what is realistically achievable, for a much-hyped chip industry.

- A more precise idea of potential gains and the effects of the latest geopolitical spat between the U.S. and China can be obtained during next quarter's earnings call.

It's easy to understand why people think of hype when you see the high degree of correlation between the stock price actions of Nvidia ( NVDA ) and Microchip Technology ( MCHP ) since May 24 of this year.

At that time, the AI chip company had announced orders which were more than 50% over analysts' expectations thereby justifying the stock's upside, but, it is a different story for Microchip which seems to have benefited more as a chip play and optimism by investment firm Truist . Consequently, with the first-quarter 2024 (Q1-2024) earnings expected on August 3 , this thesis aims to uncover the truth, and, understand exactly how the micro-controller company could benefit from the popularization of Generative AI tools like ChatGPT.

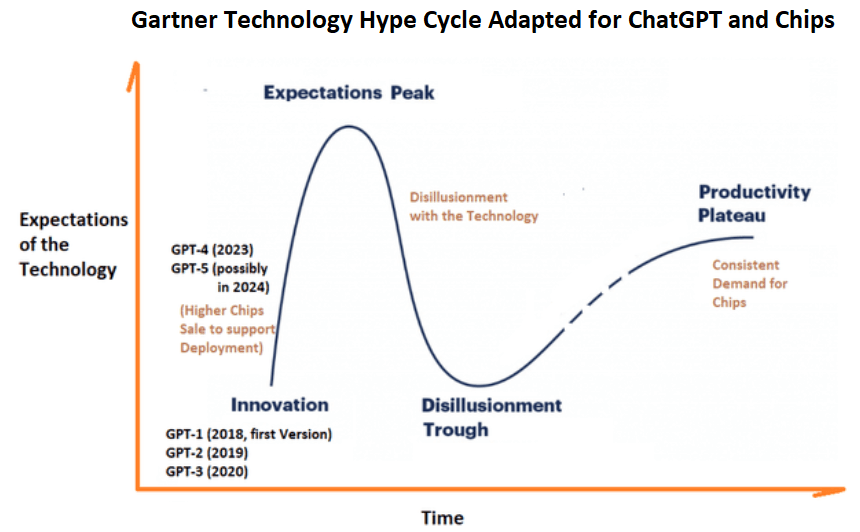

First, to address the hype problem, or provide a picture of what is realistically achievable in an industry where prospects have been blown out of proportion, the obvious way to start is with the Gartner Technology Hype Cycle.

Viewing ChatGPT Through the Tech Hype Cycle

As illustrated below, this graphical representation was designed by researchers at the IT firm Gartner to understand the evolution of tech innovations and I have adapted it for ChatGPT. This Chat-based app for generating intelligent reports was developed by software company OpenAI and makes use of Generative AI algorithms that need Nvidia's H100 advanced GPUs to work. This explains its higher chip sales to support the deployment of the app.

Chart built using data from TechTarget (www.techtarget.com)

{kind=link}

As seen above, the innovation phase started with the development of the first version (GPT-1) in 2018 and, currently, with the fourth version (GPT-4), we are rapidly moving at the experimentation and adoption stage with the 100 million MAUs (monthly active users) mark reached just three months after launch. Logically, after such a level of enthusiasm building up over such a short period, expectations levels are likely to peak as with most technologies, and eventually, many will get disillusioned as per Gartner's experience. Then later, after a relatively longer period, a "plateau of productivity" will be reached which is synonymous with more consistency.

I further support the achievement of productivity status for Generative AI through research by McKinsey .

Thus, in its report dated June 14, the research firm states that this flavor of artificial intelligence, by itself, should engender productivity gains of 24%, on top of what is expected for the 2022-2040 period. This is a lot, and, by putting a concrete figure as to the potential benefits, this thesis shows that amid all the debate around its usefulness, Generative AI cannot be treated as hype in my view.

Now, the next step is to show the relationship between Microchip's mixed signal microcontrollers and ChatGPT, and to this end, I borrow the concept of "joint demand" from economics.

Microchips is a Joint Winner with Nvidia for AI

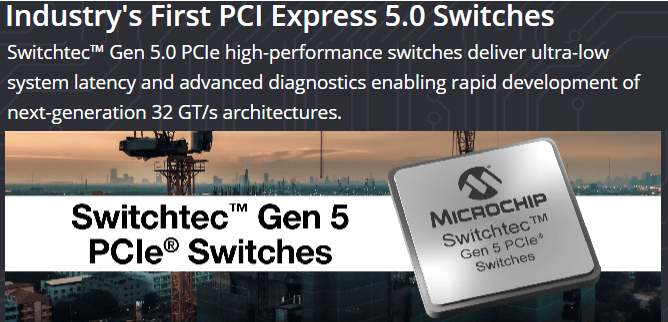

First, Nvidia's chips even if they are the world's most advanced GPU chips cannot operate in isolation, as they have to be inserted in servers containing memory chips and other accessories. Then to connect to storage devices within data centers, PCI switches are needed, not just any piece of hardware that engineers can lay their hands upon, but, only the most advanced ones produced by the likes of Microchip, namely the Switchtec which offers the industry's highest data transfer rate of 32 GT/s.

Microchip Switchtec Gen 5 PCI (www.microchip.com)

{kind=link}

In other words, to deliver the highest performing AI applications, you need both the best GPUs and switches, synonymous with joint demand, or demand for one product leading to request for the other. To obtain confirmation of Microchip's product being appropriately positioned, CEO Ganesh Moorthy talking during the fourth quarter's (Q4-2023) earnings call, "We are getting tailwind from the AI servers and we are represented in those. Many of our PCI switches are an analytical part of that".

Now, that was on May 4, or twenty days before Nvidia announced its sky-high revenue guidance of $11 billion compared to the $7.11 billion analysts were expecting, or a difference of $3.89 billion, all based on the uptake of Generative AI.

Valuing the Opportunities

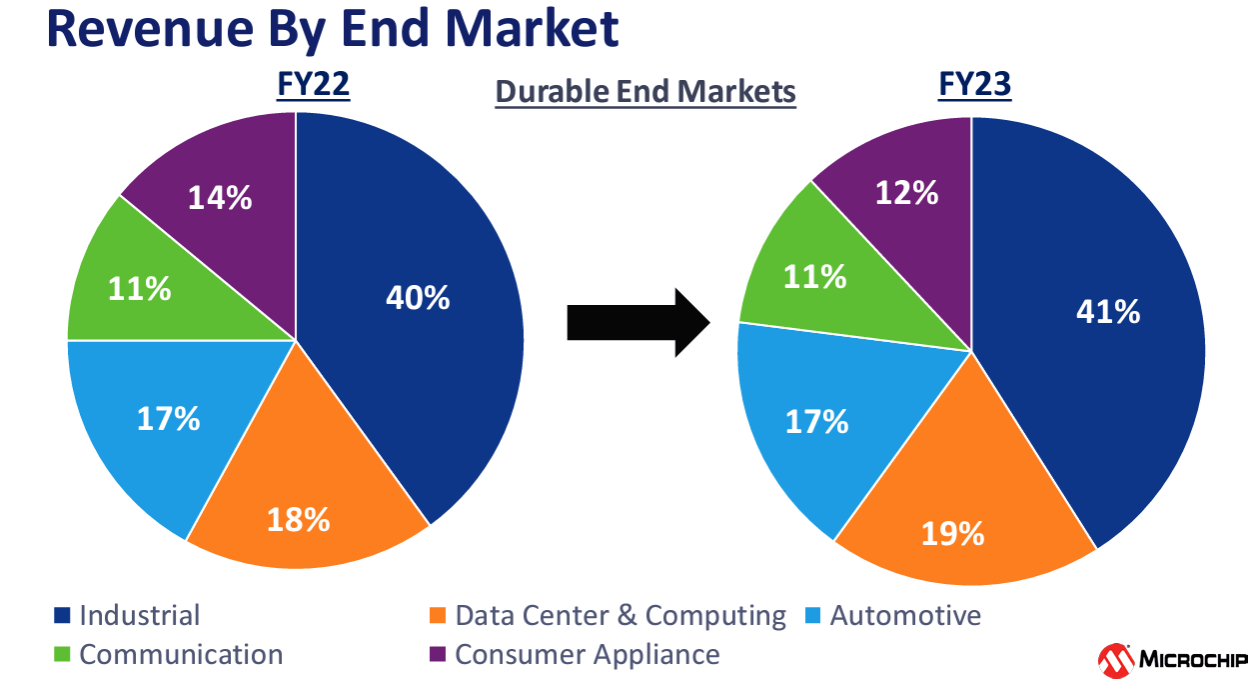

For Microchips, the related sales opportunities should manifest themselves in the Data Center and End User end market , which as shaded in blue below has been resilient despite weakness in demand for the semiconductor industry, with its share of revenue increasing by 1% (18% to 19%) from FY-2022 to FY-2023.

Company Presentation (static.seekingalpha.com)

{kind=link}

For an estimate of potential opportunities, while waiting for management's guidance during the upcoming earnings call, in the eventuality Microchips just manages to ink more switch-related sales contracts for an amount of $38.9 million, (which represents only one-hundredth times the $3.89 billion to be harvested by Nvidia), the Data Center segment would generate $1.636 billion in FY-2024, on top of what was expected at the end of Q4-2023. This figure is obtained after adding the $1.596 billion for FY-2023 to $38.9 million and means a growth of 2.4% for the segment, which, by the way, remains a modest target based on only a tiny fraction of Nvidia's outlook, but, considers that it will take time to attain the productivity phase as per Gartner's Hype Cycle.

Hence, to value the company for the medium term, I use the profitability criteria.

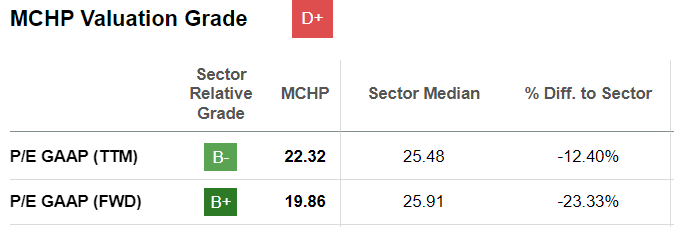

In this respect, as an IDM or integrated device manufacturing play, Microchip scores better with gross margins of 67.52% compared to only 53.31% for Nvidia which has to bear higher costs of revenues involved in outsourcing chip production to Taiwan Semiconductors Company ( TSM ). However, despite this higher profitability, Microchip remains undervalued when looking at the Forward Price-to-Sales multiple of 19.86x which is below the sector median by 23%. Adjusting accordingly, I obtain a target of $110.62 (89.72 x 1.233) based on a share price of $89.72.

{kind=link}

Now, this share price is also justified when looking at the competition and the latest move by China to curb the export of certain chip-making metals.

Competitors and Geopolitical Risks

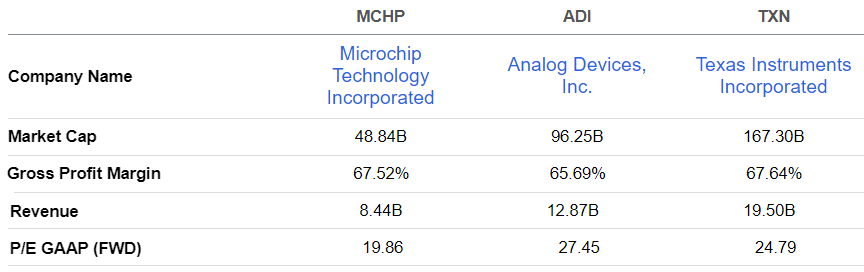

Two competitors (especially for analog chips) are Analog Devices ( ADI ) and Texas Instruments ( TXN ), which despite benefiting from much higher revenue levels to spread their fixed costs on, deliver around the same gross margins as Microchips as tabled below. This means it has a better production proficiency, but remains undervalued based on earnings metrics. This again justifies the higher target of $110-$111.

Comparing with peers (seekingalpha.com)

{kind=link}

Talking risks, there is also uncertainty caused by geographical exposure to the rest of the world (non-U.S) which accounted for about 78% of revenues in fiscal 2023 including 21% for China alone. Now the East Asian giant retained its spot as the world's premier semiconductor market in 2022 as per the Semiconductor Industry Association, which means that strength in the Chinese market is key to being a global player for Microchip.

However, this strength comes at a cost as due to problems impacting the post-Covid recovery of that country, there could be demand headwinds for Microchip's chips, exacerbated to some extent by uncertainty caused by the world's second-largest economy possibly restricting chip-making metals to reach America. In this connection, as I had explained in a recent thesis , these restrictions cover Gallium and Germanium with companies like Analog Devices, Qorvo ( QRVO ), and others likely to see headwinds, not Microchip which is more specialized in SiC or silicon carbide. On the contrary, since SiC can become an alternative for Gallium-based compounds in certain high-voltage applications, Microchip could benefit from Chinese restrictions. For this matter, it already plans to expand existing wafer production in the United States under a multi-year $800 million investment in capacity, which is aligned with the CHIPS Act.

Adopting caution, with the earnings call only about one week away, some would prefer to wait for a relevant update from the management as to what the company is doing to reduce the impact of geopolitical risks on its topline.

What to look for during Earnings and the AI Potential

In the same breath, given less favorable macros globally than in 2022, and the company having little visibility in end markets, it is crucial to be updated as to what measures are being taken to reduce the inventory which was at a record level in dollar terms at the end of Q4-2023.

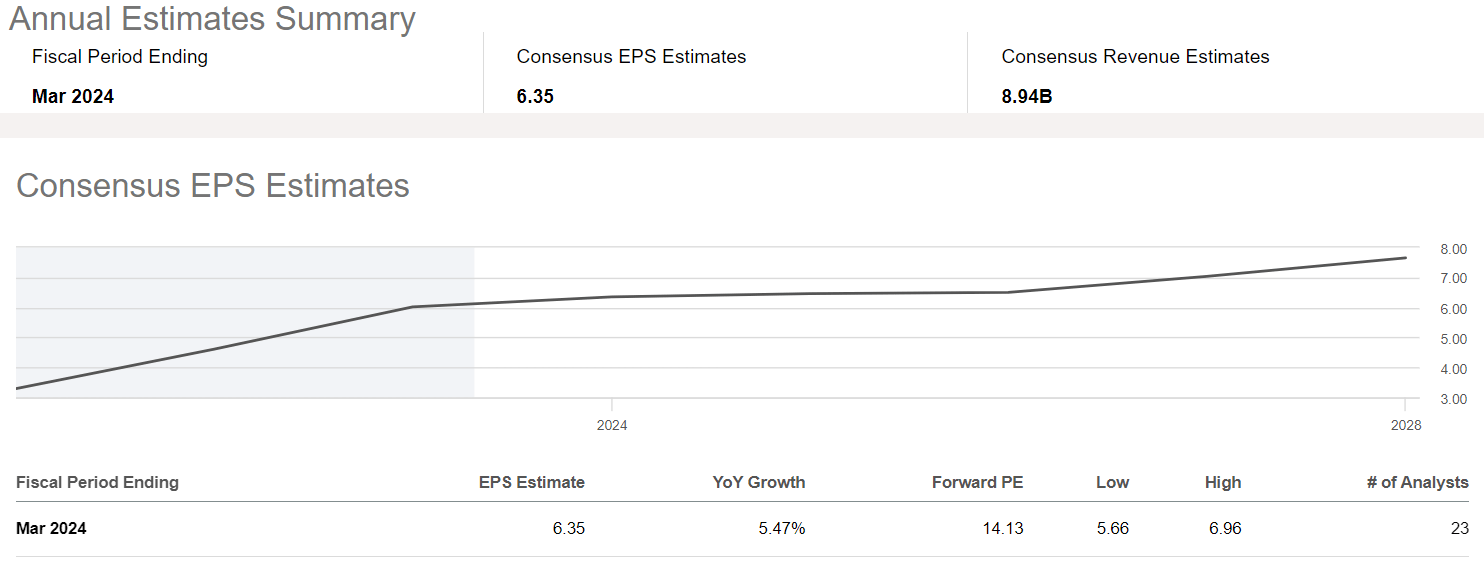

Paying close attention to inventories is also important as it represents cash lying idle, and in the eventuality of Microchip having to liquidate its stocks by selling at a discount, the earnings expectations for FY-2024 currently at $6.35 may need to be revised downwards. In case this happens then my valuations thesis which is based on Microchip's superior profitability going forward may have to be reviewed.

Earnings Estimates (seekingalpha.com)

{kind=link}

However, to mitigate some of those risks, there is AI.

In this respect, investors will note that I have been modest in revenue estimates for the Data Center segment, but noteworthily, with 2.4% AI-led potential growth as mentioned earlier, its weight on total revenues (which are projected at $8.94 billion for FY-2024 as pictured above) would cross the 20% mark next year from 19% in 2023.

To be realistic, there is competition meaning that market share will be split between other players like ADI and Texas Instruments, but these players benefit from the resiliency of IT spending, which, despite the downtrend from 2022, will rise by 4.4% to reach $3.25 trillion in 2023 according to the IDC or International Data Corporation. Furthermore, AI is getting more popular according to McKinsey, which should increase the market size.

Thus, after seeing the advantages of OpenAI's algorithms to deliver both faster and better work output than human beings in certain cases, there is renewed interest in other flavors of AI like Analytics and Recommendation, as, before ChatGPT, it was viewed as a complex field restricted to tech-savvy individuals.

In conclusion, by using the Gartner Hype Cycle to filter out the hype from what is actually realizable through Generative AI, this thesis has shown that Microchip's upside is justified, while also providing a figure as to potential productivity gains. Then, using the principle of joint demand, the actual dollar gains to be made by Microchip through the sale of Datacenter equipment have been identified, and which has been moderated given the competition and the time factor.

Therefore, opportunities are real and a more precise idea can be obtained during the forthcoming earnings call when an updated guidance on FY-2024's revenues is provided, especially for Data Center. Other management updates to scrutinize are the finished goods inventories and whether there are any cancellations or requests for pricing discounts. Finally, given the need to protect SiC's supply chain, there should also be a focus on the raw materials inventory.

Editor's Note: This article was submitted as part of Seeking Alpha's Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Microchip: Filtering Out The AI Hype