MCHP - Microchip: Solid Company For The Long-Term But I'll Wait For Earnings To Decide

2023-10-27 13:01:09 ET

Summary

- Microchip Technology Incorporated has seen improvements in its financial metrics and is trading at fair value.

- The company has manageable debt and is at no risk of insolvency.

- Microchip Technology has a strong competitive advantage and has been leading its competitors in terms of efficiency and profitability.

- I will be waiting to initiate a position until after earnings.

Investment Thesis

Microchip Technology Incorporated ( MCHP ) is going to report Q2 earnings soon, so I decided to look into the company's financial health over the long run to see if it is a good time to put some cash into it. The company has seen a lot of improvements in all of the financial metrics I've covered, however, I would like to wait until after the earnings so the volatility comes down, and if the long-term thesis is still intact and the company comes down on a bad report, I think this would present a good entry point as the company is trading at a fair value currently.

Financials

As of Q1 '24 , the company had $271m in cash against around $4.6B in long-term debt, which was reduced from a quarter ago by around $400m. I like seeing this initiative from companies. A lot of investors tend to avoid companies with excessive debt when it comes to investing in a stock. I don't think there's anything wrong with leverage when it is manageable, and in the case of MCHP, it is very manageable. The company's latest interest coverage ratio stood at around 19x, while historically it's been worse in prior years. This ratio means that the company's EBIT can cover annual interest expense on debt 19 times over. For reference, many analysts consider 2x to be healthy, however, I consider 5x to be optimal as I like to be more conservative. So, it's safe to say the company is at no risk of insolvency.

The company's current ratio has been hovering around 1 for a while, which is the bare minimum I like to see. I would prefer to see that ratio in the range of 1.5-2.0. As of the latest quarter, it just passed 1 so at least it can cover its short-term obligations right now, so I don't think it has any liquidity issues.

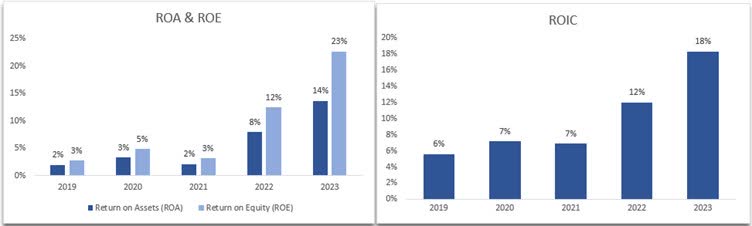

In terms of profitability and efficiency, the company's ROA, ROE, and ROIC have been experiencing an impressive uptrend in the last few years, driven by the company's ability to become more efficient as I can see that the increase in sales did not lead to the same increase in COGS and operating expenses, which led to dramatic operating margin expansion. This tells me that the company is able to utilize its factories to a fuller extent without having to increase costs, thus improving efficiency.

Profitability and Efficiency metrics (Author)

{kind=link}

Furthermore, the company's ROIC is much higher than its weighted average cost of capital of around 11%, which is also quite high because of the company's high beta. It looks like the company is a value creator and not a destroyer.

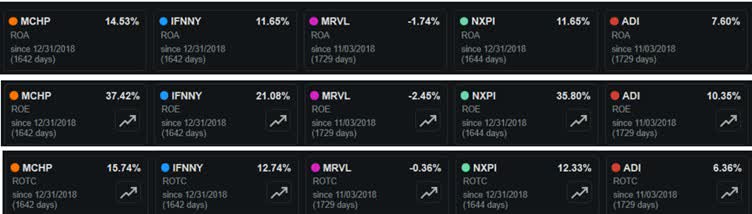

If we compare the company to its competition on the same metrics (ROTC is slightly different from ROIC, but Seeking Alpha doesn't have that metric, both measure efficiency), we can see that MCHP is leading the pack, which tells me that the company has a decent competitive advantage and a strong moat.

Profitability and efficiency vs competition (Seeking Alpha)

{kind=link}

I would be willing to pay a premium for such a quality company and it usually trades at a premium also, however, it seems like the company is trading at recent lows in terms of P/E ratio. This doesn't surprise me because of the negativity in the semiconductor sector, which was plagued by inventory buildups and high prices due to inflation, which brought negative sentiment. Many companies in the semiconductor sector have experienced this and many are seeing the bottoms set in and the demand pick back up sometime in early '24.

PE ratio (Seeking Alpha)

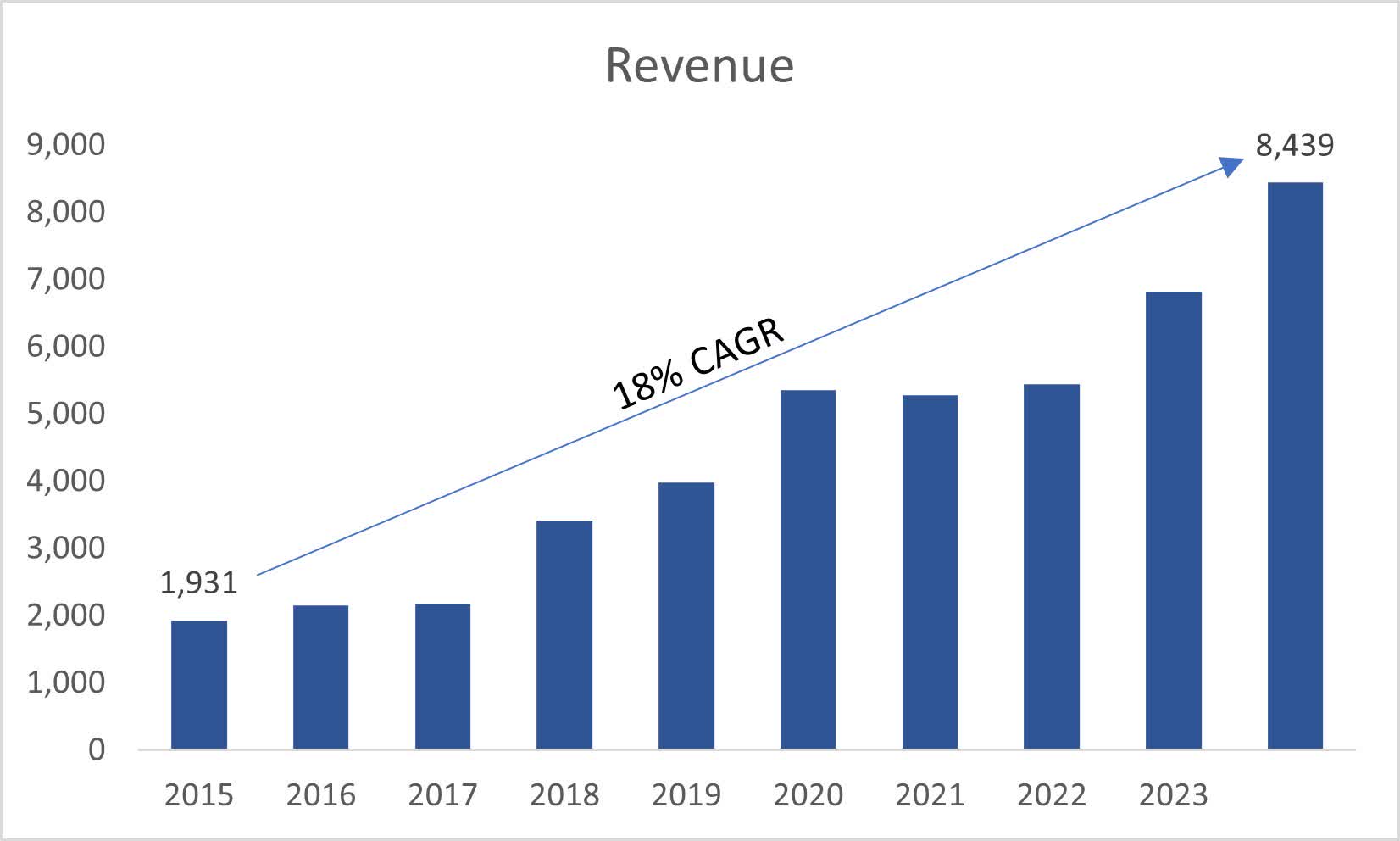

In terms of revenues, the company's been performing quite well over the years, so it is rather surprising to see that analysts are estimating very poor performance going forward. I can understand the company's poor performance for FY24 since the management guided around up 1% to down 3% sequentially due to the mentioned reasons in the semiconductor segment, but I don't think it is very easy to assume underperformance going forward because many other companies in the industry are seeing a rebound coming over the next half a year to a year.

Revenue (Author) Revenue Estimates of analysts (Seeking Alpha)

{kind=link}

{kind=link}

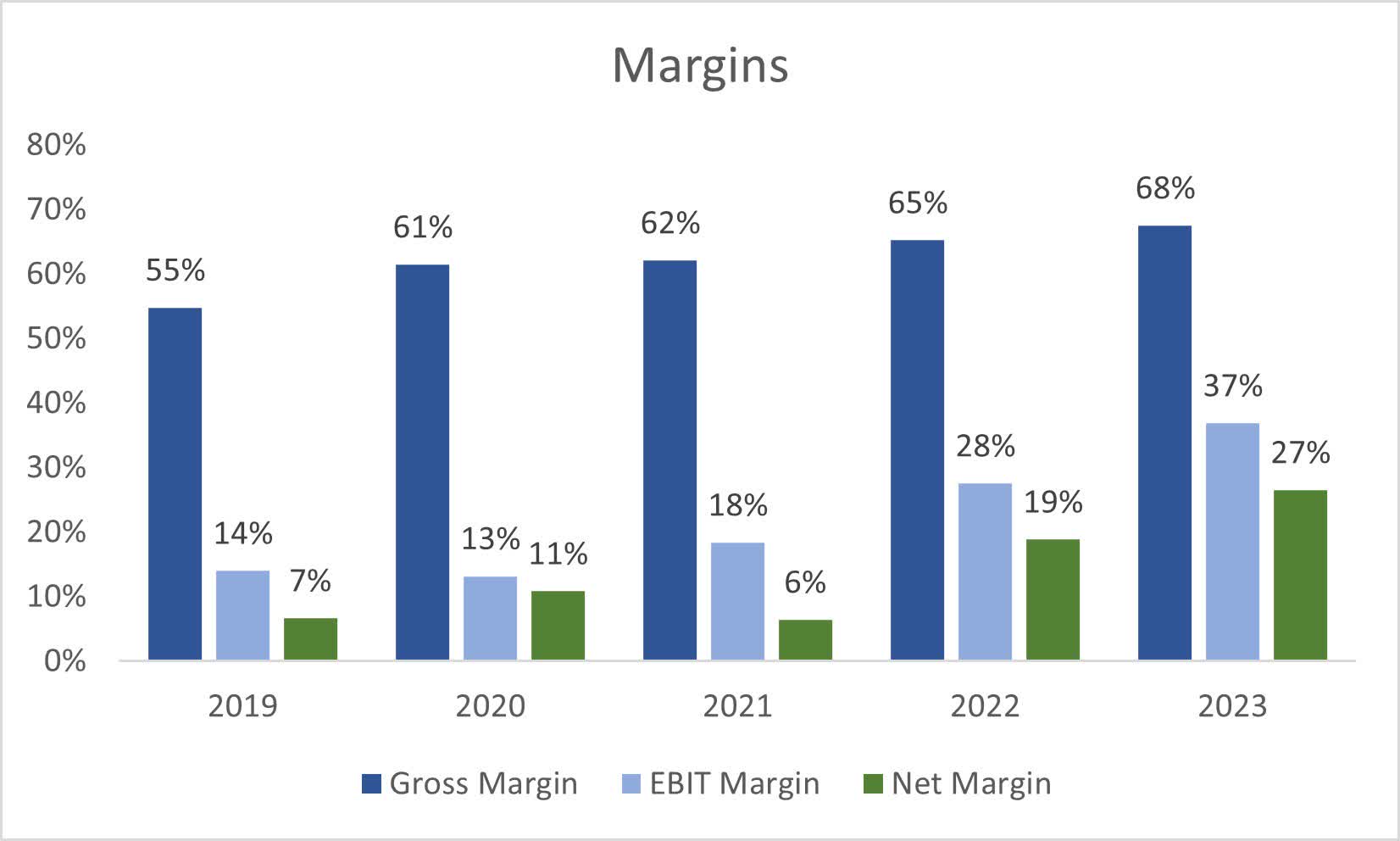

In terms of margins, I see nothing but a positive trend here also, just like in previous financial metrics mentioned. The company is able to improve its efficiency year after year, and not by just a couple of points either. These are substantial improvements over the last few years, and as I mentioned earlier, the company benefited from much higher sales that did not proportionally increase the company's costs.

{kind=link}

Overall, I see a company that has improved drastically over the years, is leading the pack of the competitors mentioned above, and has a strong competitive edge and a decent moat. The company's efficiency and profitability have improved dramatically since FY21. I am curious to see how next year's margins will develop. I have to commend the management for how the company has developed over the last couple of years.

Valuation

As I mentioned I was very surprised with the analysts' estimates of revenues over the next couple of years. The next year is easier to calculate since it's not far off now and the management provides guidance on the outlook, so I understand the low numbers there. However, I read from many other semiconductor companies that the demand will pick back up next year, so I can see these revenue estimates changing over the next year and reflecting a different, more positive outcome. So, I decided to go with what I think are conservative, yet reasonable estimates for my three scenario assumptions. Below you will see estimates for base, conservative, and optimistic scenarios.

{kind=link}

In terms of margins and EPS, I decided here to be a little more conservative than what the analysts are estimating. This way I'll get a little extra margin of safety and that never hurts.

{kind=link}

Analysts EPS estimates (Author)

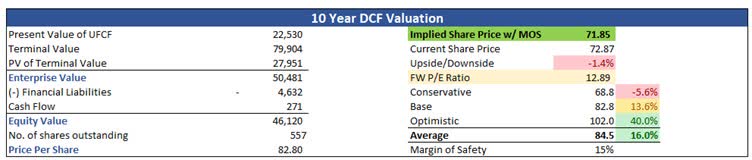

For the discount rate for the DCF, I went with the company's weighted average cost of capital, or the WACC, which ended up being around 11%. I decided to go with a 3% terminal growth rate also.

On top of these estimates, I decided to add another 15% margin of safety to give me that little extra cushion of safety. I feel that 15% is enough because the financials of the company looked great and because my estimates are on the lower end of analysts' estimates. With that said, Microchip's intrinsic value is around $72 a share, which means the company is trading at its fair value in my view.

{kind=link}

Closing Comments and Investor Takeaway

Since the company is very close to reporting its numbers, I decided to give it a hold rating until after the report because of the implied volatility associated with these kinds of things. If the company reports worse numbers than estimated, the company may see its share price come down, which would provide a better entry point for the long-term investor, provided that the numbers that come out are only bad in the short term, and the long-term thesis remains intact.

I will be tuning in to the company's earnings call and will look for any hint on how the sales numbers are progressing going forward and whether the company thinks that the trough of demand has been reached. I believe we will hear a more positive vibe coming from the management regarding the future, which will help me decide whether I should start a position or not. The company is set to report the numbers on the 3rd of November post-market.

I wouldn't be surprised if I heard some declines in efficiency due to the negative sentiment in the industry, which may bring down its share price in the short run. The same goes for the sales numbers. I would be rather surprised if margins not only remained stable but improved while sales came in higher than expected. That may send shares higher, and I would hope not too much because I do like this stock for the long term.

For further details see:

Microchip: Solid Company For The Long-Term But I'll Wait For Earnings To Decide