MCHP - Microchip Technology: Not The Time To Turn Bullish Yet

2023-12-01 01:52:18 ET

Summary

- Microchip Technology's near-term performance is expected to be weak.

- The company's 2Q24 results showed a decline in revenue across all major product lines.

- Management's guidance for 3Q24 and 4Q24 indicates continued weakness and potential further decline.

Summary

Readers may find my previous coverage via this link . My previous rating (published in early October 2023) was a hold as I believed Microchip Technology ( MCHP ) would see a very weak near-term performance, which will certainly impact the share price sentiment. I am reiterating my neutral rating for MCHP, as it has become very clear that the near-term weakness is going to persist into 4Q24. There is little reason for me to turn bullish at this point. The right strategy here is to wait for 3Q24 to end and for management to give insights about FY25.

Financials/Valuation

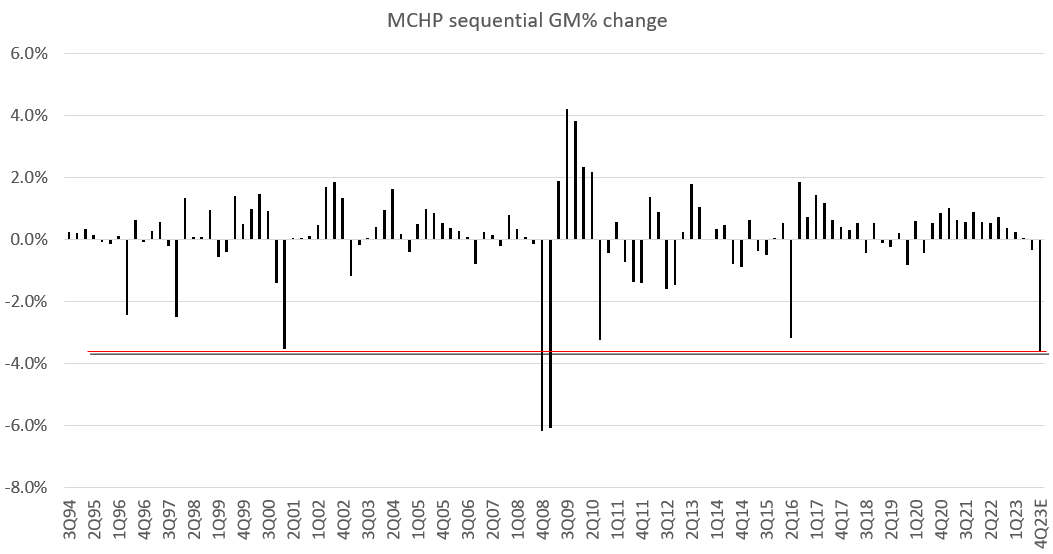

MCHP posted 2Q24 revenue of $2.254 billion, which was a 1.5% decline sequentially and an 8.7% gain annually. Relative to the past year, MCHP y/y growth has decelerated by a big bunch. In FY23, y/y growth trended above 20% against a very strong FY22 growth rate of 20-30% range. The strong growth momentum has slowed down starting 1Q24 (16.6%). The sequential decline was broad-based across all major product lines. By product, MCU posted revenue of $1.29 billion, Analogue posted revenue of $683 million, and FPGA and LMO collectively posted revenue of $280 million. Non-GAAP gross margin came in at 68.1%, which was impacted by lower utilization in the front-end and back-end. That said, adj. EPS did come in line at $1.62.

Based on author's own math

Based on my revised outlook on the business after the 2Q24 results and management guidance, I see a 6% downside to MCHP stock. I now expect MCHP revenue to decline by 5% in FY24, reflecting the sequential decline in 3Q24 (17.5% seq decline) and 4Q24 (10% seq decline). I also expect the net margin to come in lower as the gross margin erodes further. I note here that the net margin could be much lower if pricing starts to become a negative headwind as well. Looking at MCHP's current forward PE multiple of 16.6x implies that the market is anticipating some form of recovery in FY25. However, for my model, I am attaching at a 15x multiple (MCHP through-cycle multiple). All these assumptions led to my price target of $77.63.

Comments

MCHP 2Q24 results continue to show that they are facing a hard time. In fact, the near-term revenue outlook seems to be worse than I expected, and the weakness is across the board. With the exception of A&D, all regions and end markets are experiencing softness as customers react to business uncertainty. I believe the uncertainty is largely driven by the weak macroeconomic situation, which I don't see improving anytime soon. Rates are still high, and with US employment still very strong, there is little reason for the Fed to cut rates. Underlying operating metrics also point to upcoming periods of softness. Lead times for MCHP, for example, were 13 weeks at the end of 2Q24, down from 52 weeks when the year began. It would appear that MCHP is running at a high efficiency rate, and bulls would say that everything else being equal, normal lead times will let Microchip know which of their products are selling well since buyers aren't enticed to buy more than they need. However, the reduction in lead times is due to a lack of demand, and with a lower level of bookings, it also means that MCHP has reduced visibility into the timing of growth recovery.

However, the significant reduction in lead times is also resulting in lower bookings and reduced near-term visibility. Source: 2Q24 earnings

The magnitude of near-term weakness can also be seen from management's weak 3Q24 guide, which reflects continued broad-based weakness and customer inventory adjustments. To be more precise, revenue for 3Q24 was projected to be $1.86 billion, reflecting a 17.5% sequential decline and a 14% annual decline at the midpoint. I note that this guide is way below the consensus pre-results estimate of $2.11 billion. Importantly, management expects headwinds to persist into the 4Q24 and has signalled the potential for further sequential decline. Making things worse, not only is revenue expected to see a major decline, but gross margin is also expected to erode more than previously expected. Management guided the 3Q24 gross margin to 64.5% at the midpoint, which is a staggering 360-bps decline sequentially. To put things into perspective, aside from the subprime crisis, this decline is the worst in MCHP's operating history as a public company. Management also mentioned that pricing remains stable and that a decline in volume was the key contributor to its weak December quarter revenue outlook. What this tells me is that there is room for gross margin to further erode sequentially if the business environment turns for the worse, as pricing decline was not embedded into the guide.

{kind=link}

What was encouraging in the quarter was that management made progress in reducing its debt. It has now repaid $6.7 billion in debt since the closing of its Microsemi acquisition in 2Q18. As of 2Q24, MCHP has a net debt position of ~$5.81 billion, or 1.33x LTM EBITDA, a decline from ~1.8x last year. In the event of an extended period of decline, it is less likely that MCHP will need to raise capital from the public or debt market, as it should to service this level of debt comfortably.

That said, I think it is very clear that the near-term weakness is going to be very weak, much worse than I previously expected, so I do not see any reason for any investors to buy the stock now. I think the best move here is to wait until 3Q24 is past and monitor the demand situation when management gives further comments about 4Q24. Remember that management visibility into demand is low, so I would not take any medium- to long-term guide seriously yet.

Risks

Upside risk here could be that MCHP sees a recovery faster than what the market and I expect. Given that management already set the expectations that growth is going to see strong sequential decline over the next 2 quarters, any signs of growth will cause a major reset in expectations. This will probably cause the market to be more bullish as it could be a signal of a new upcycle.

Conclusion

It is clear that MCHP faces persistent near-term challenges which reinforces my neutral rating. The company's recent 2Q24 results exhibited broad-based revenue declines across major product lines, with weakened margins influenced by lower utilization. Management's bleak 3Q24 guidance, projecting significant sequential declines in revenue and gross margin, further emphasizes the challenging landscape ahead. While debt reduction is positive, the worsening near-term outlook suggests a wait-and-watch approach until clearer demand signals emerge post-3Q24.

For further details see:

Microchip Technology: Not The Time To Turn Bullish Yet