MCHP - Microchip Technology: The Quiet Giant With Steady Cash Flow

2023-08-17 03:43:02 ET

Summary

- Microchip Technology is a global leading supplier in microcontrollers (MCUs) used in various home appliances and gadgets resulting in 131 consecutive quarters of Non-GAAP profitability.

- The company has sparked growth through strategic balance sheet management to fund mergers & acquisitions and consistent research & development into new projects.

- MCHP stock is trading at a low valuation and has the potential for multiple expansion, but analyst low growth estimates may mean a lower P/E for longer.

Investment Thesis

Microchip Technology ( MCHP ) is one of the world's leading suppliers in microcontrollers (MCUs). MCUs are a $20.6 Billion dollar industry expected to grow at an 11% compounded annual growth rate through 2030. MCUs are used in products that need to be able to sense inputs, execute a program, and send an output. They are in tools used in common day gadgets and accessories that people will continue to need.

Microcontrollers are used in familiar products such as automobiles and home appliances. Here are some examples of home appliances in which microcontrollers are used:

- Refrigerators

- Washing machines

- Microwave ovens

- Cordless vacuum cleaners and robot vacuum cleaners

- Hair dryers

- Sphygmomanometer/thermometer

- Lighting devices

- TV remote controls

{kind=link}

Analysts covering Microchip Technology expect low single-digit growth in the coming 3-5 years as demand stabilizes. This is after the company outperformed the past 5-6 quarters due to the global chip shortage. However, management has done a great job diversifying the company through mergers and acquisitions and consistent research and development. This, along with the firm's ability to generate free cash flow under almost any economic scenario, has allowed MCHP to survive and outperform the market.

Microchip Technology is not a flashy tech company like Nvidia ( NVDA ) or other high-flying chip companies. Instead, it is a necessity tech supplier in the semiconductor industry that is a market leader in the MCU segment across the world. Microchip is one of the best-run companies in the world and has been around since 1989. They have 131 consecutive quarters of Non-GAAP profitability and saw record sales, profits, and EPS in Q1 this year. Another reason why MCHP continues to outperform in the long haul.

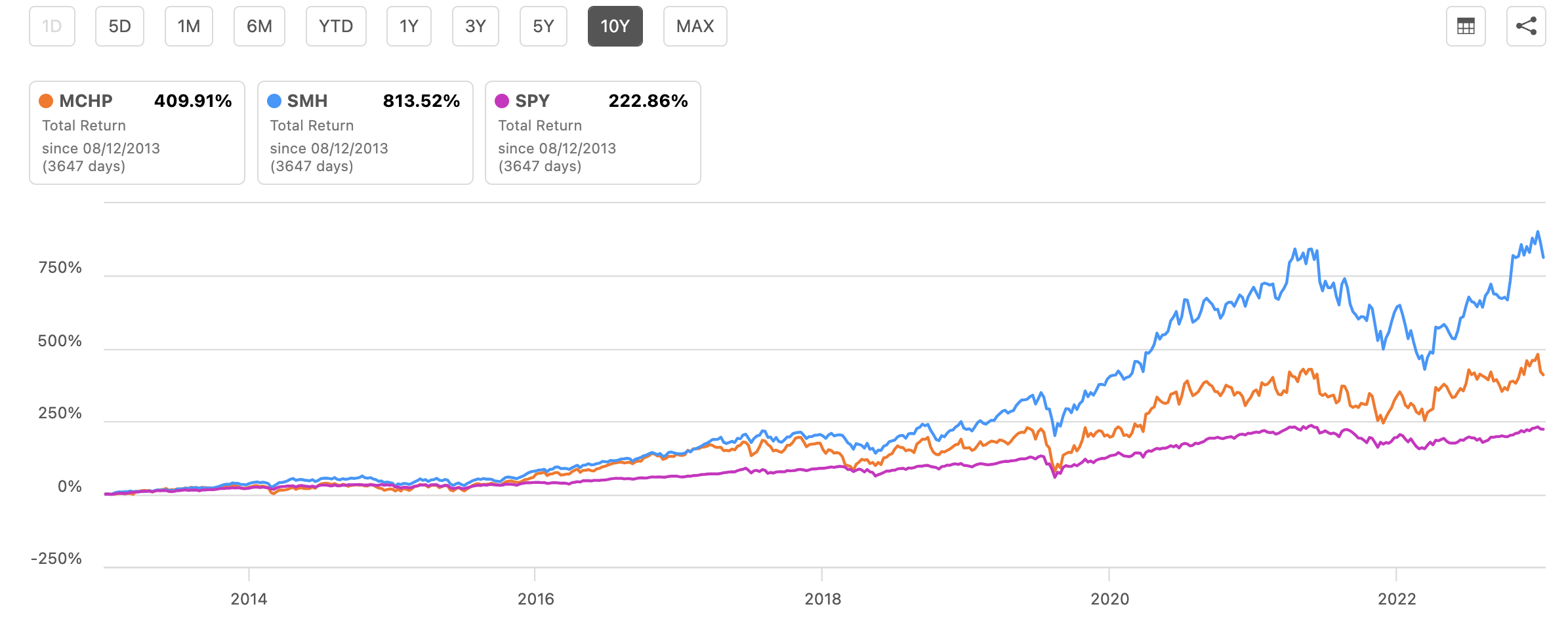

{kind=link}

MCHP 10yr Total Return comparison .vs. Industry & Market (Seeking Alpha)

MCHP has increased its dividend for 19 consecutive years and paid a dividend for 84 consecutive quarters, soon achieving dividend aristocrat status (25 years). They have a low payout ratio of 31.3%, a 13.5% 5-year dividend growth rate, and a solid 7.4% FCF yield. I believe that as more electronic devices become "smarter" and connected to the internet (Internet of Things), Microchip's MCUs and analog chips will see steady increasing demand.

MCHP is trading at a price-to-earnings ratio of 13.3x, which is below the five-year average of 15.3x and well below the industry median. MCHP is simply a value stock. Analysts expect low single-digit sales and earnings per share growth in the next 3 years. The valuation is trading on the lower end with upside room given their control over margin expansion and utilizing its balance sheet. My calculations see the stock trading slightly below fair value, but ultimately I believe MCHP is a hold for investors as a reliable long-term chip play with its customers' needs going nowhere.

FCF & Balance Sheet Management

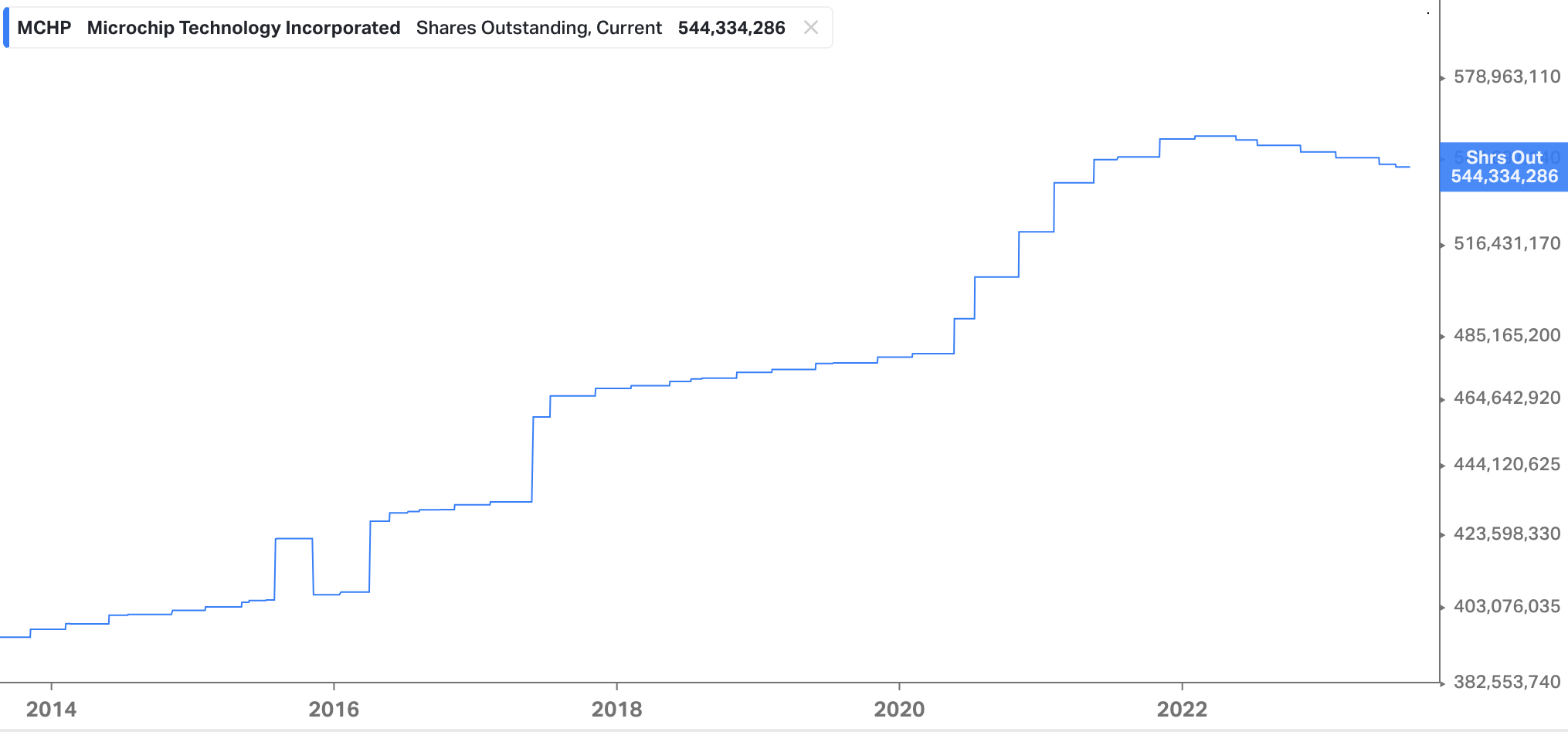

Microchip Technology's shares outstanding have increased by over 37.9% in the past 10 years. The company has constantly issued more shares over the years to help fund acquisitions and research and development. MCHP has had 18 acquisitions in its history, and its two biggest have come in the last 10 years: Microsemi ($10 billion in 2018) and Atmel ($3.5 billion in 2016). Management has started to address the rising share count problem by buying back approximately $1.5 Billion as of Q1 earnings which is part of their $4 billion buyback program.

{kind=link}

MCHP Shares Outstanding (Koyfin)

M&A has been a key driver of growth and shareholder return for Microchip Technology in the past. I would expect that trend to continue in the future, given the company's strong cash flow and track record of successful M&A. Morningstar Analysts highly rate MCHP's acquisitions of Atmel and Microsemi, saying that:

Apart from a robust portfolio, the acquisition will expand Microchip's total addressable markets. Strong demand for Microsemi's solutions in Data Center, Communications, Defense & Aerospace markets bodes well for Microchip in the long haul.

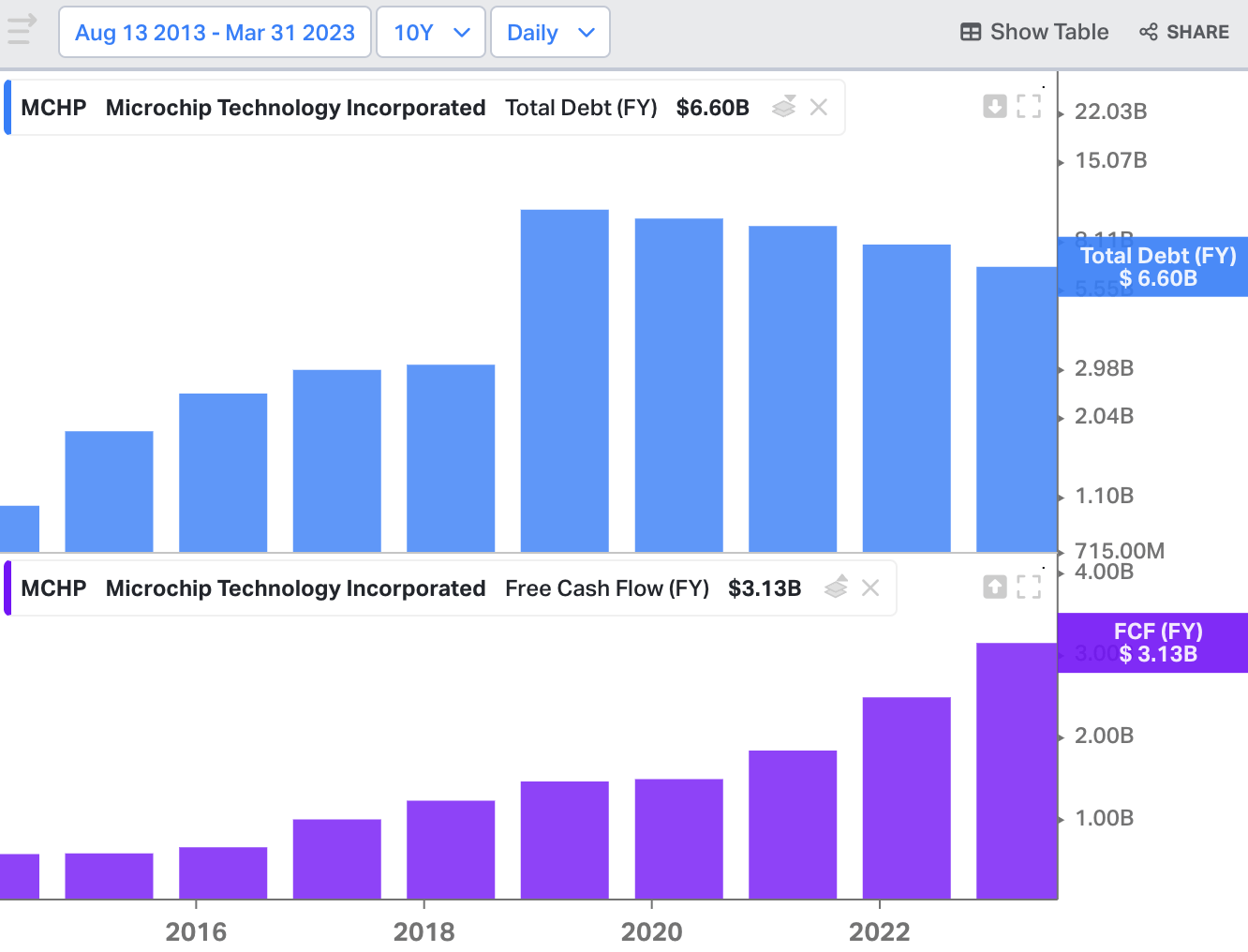

Microchip Technology's share dilution helped the company raise money to pay off debt it took on to finance the acquisition of Microsemi and continue internal investment for growth. MCHP's total debt jumped to a new all-time high in 2018, from $3 billion to $11.3 billion, to help pay for their acquisition. The company now has 20 consecutive quarters of debt pay down and now has debt down to just above $6 billion.

Last fiscal year, MCHP had $3.6 billion in cash from operations and has $3.2 billion in FCF currently. The company consistently generates cash, which gives management the flexibility to play with the balance sheet and the company's funding. Microchip has generated nearly $10.7 Billion in Adjusted FCF since 2019. MCHP has a steady business model and reliable customers, with high switching cost making it a dependable stock to hold.

{kind=link}

MCHP Total debt & FCF (Koyfin)

The last thing I want to note about the company's balance sheet and cash flow is management's ambitious goal to accelerate cash returns targeting 100% of FCF in roughly 6 quarters. They also want to increase capital returned to shareholders to 50% of Adj. FCF, rising to 100% of Adj. FCF as net leverage drops to ? 1.5X. Management has a plan in place, Microchip 3.0, for sustained revenue growth and margin expansion to help continue to return capital to loyal shareholders.

Valuations & Price Targets

As I mentioned before, MCHP is trading at a relatively low valuation compared to its historical average. It currently sits at a price-to-earnings ratio of 13.3x, while its P/E range over the past 10 years has been between 15-18x. The 5-year average P/E ratio is 15.3x. This indicates that there is room for the stock price to go higher due to multiple expansion. However, it is hard to argue that the valuation is not fair given the company's low growth estimates. The street consensus average has sales increasing 3.3% this year, 0.55% the following year, and 5.3% the year after that. EPS growth is slightly better, but ultimately to see the stock price go past $90, we may need improved guidance.

Enterprise value to sales (EV/S) tells a different story to me. MCHP's EV/S of 5.7x is below its 5-year average, but well above the industry median . I believe that the stock could see more downside due to this inflated EV/S number and the lack of sales growth ahead. I have reflected this in my price target scenario table below, where I calculated MCHP to be trading at an 8.3% discount from fair value with a 1.9x risk-to-reward (R/R). Morningstar analyst rate fair value at a P/E of 15x, or $90 per share.

The stock has pulled back 7.5% in the past month, along with the cool-off of other semiconductor stocks. I believe that the stock is a hold in the $80s, but would be a buy if it continued to fall below $79 per share. At that point, the R/R would be increased over our 3x target, and price appreciation paired with dividend growth should give market outperformance returns to shareholders over the next 5-10 years.

{kind=link}

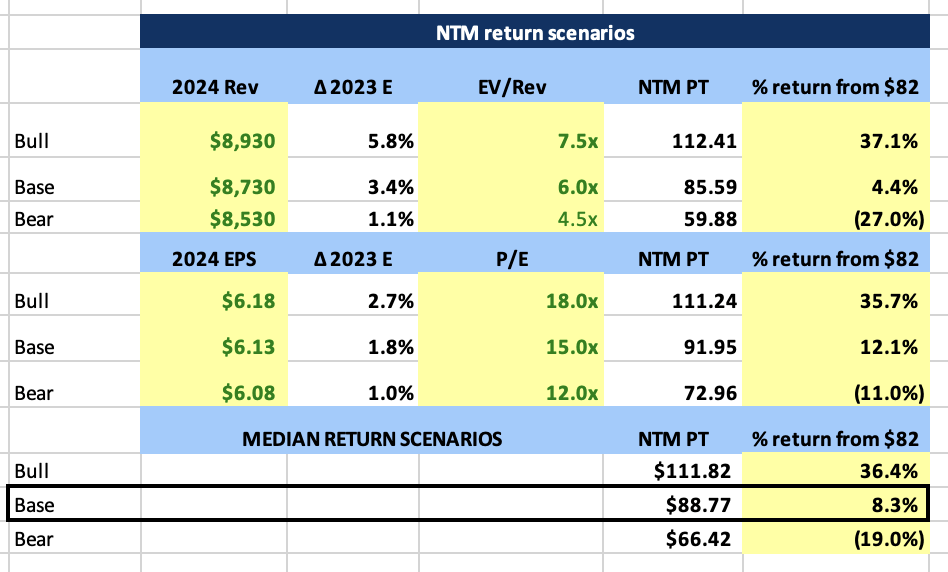

2024 MCHP Price Target Scenario Table (Author Calculations Based on Analyst Estimates From Koyfin Data)

Microchip Technology was trading at fair value a month ago, but has since given up those gains. Headwinds have been showing, and inflation has been sticky, causing a less optimistic outlook. Historically, it has been best to accumulate shares between the $68-$73 range, as that is where the stock tends to bottom and find a rebound point. Sitting at $82 currently leaves room for downside, but over time the company and stock will grow. They are a major supplier for products that have become a necessity in society, and because of that will generate a safe and steady cash flow.

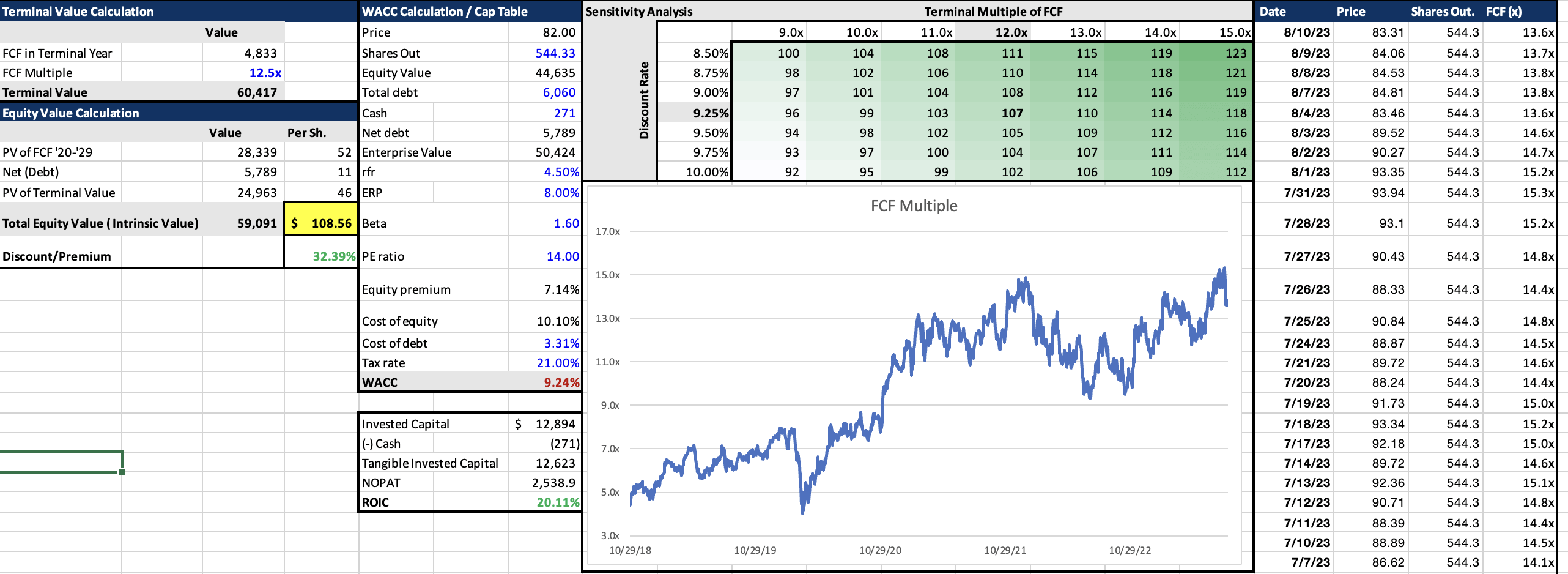

This led me to be able to create a discount cash flow analysis, where I found that the stock was trading at a 32% discount from its mid-term 3-5-year price target of $107 based on the company's current financial standing and estimates. I have shared the sensitivity analysis price target table below, where I use the company's FCF multiple and weighted average cost of capital ((WACC)) to do a what-if analysis. It showed us that once demand picks up and cash keeps coming in, MCHP could move back into the $90s and into the low $100s.

{kind=link}

MCHP DCF Price Target Sensitivity Analysis (Author Calculations)

Last but not least, I looked at the company's enterprise value to EBITDA (EV/EBITDA) valuation and calculated a price target based on the terminal value calculated in my DCF and the company's projected EBITDA and current enterprise valuation. This shows that the stock still belongs in the low $100s in the next few years, given that management continues to execute on its portfolio diversification and balance sheet cleanup plans.

MCHP EV/EBITDA Price Target Estimate (Author Calculations)

Risk

There are a few risks to note with the stock, but none of them in my opinion are reasons not to hold the stock. They are simply catalysts to keep an eye on and could be the reason for certain stock price movements.

The first risk to note is the cyclicality of the semiconductor industry. The semiconductor industry has sharp ups and downs as demand changes with macroeconomic conditions. The company is currently facing headwinds as they exit out of a strong period and enter a slowdown period in demand. However, the constant upgrades in technology lead me to believe that demand will stay low but steady.

The second risk to note is the competitive industry they are in with multiple established and growing players. Margins could see pressure over time with multiple players in an industry, and they have hefty exposure to China, which adds risk. If China forces its companies to not buy from a U.S. supplier, they may switch to a European leader like the Dutch's NXP. This would cause the company to lose billions in sales and dramatically change the company's valuation and price target. Microchip is a global company that needs to consistently provide high-quality products and service to compete against its competitors. Thankfully, their product offerings are relatively sticky with high switching costs for customers and partners, which helps lock in sales and cash flow for the long term.

{kind=link}

Fiscal Year 2024 Q1 Sales Geographic Breakdown (MCHP Investor Relations)

The last risk I want to note is the company's reliance and historical strength on the 8-bit MCU. It is now competing head-to-head against larger firms where it lags advanced technology. Specifically, Microchip faces harder competition in the 16- and 32-bit MCU segment which are more advanced chips being made by Texas Instruments ( TXN ), NXP Semiconductors ( NXPI ), and others. They have been trying to gain steam and catch up but still trail other players. Plus, other firms have now entered the 8-bit MCU industry and have the potential to make just as good if not better products, which could disrupt Microchip's market share. Additionally, revenue growth may suffer if higher-end MCUs are able to displace 8-bit chips as the go-to in certain electronic devices.

Conclusion

Microchip has been around for almost 30 years and continues to innovate and grow. They are a leading semiconductor industry microcontroller (MCU) supplier with reliable customers and a strategic management team. Things have not always looked pretty, but former CEO Steve Sanghi, now executive chair, has done a great job navigating MCHP through the ups and downs. They have industry-leading margins, resulting in steady cash flow to support R&D and M&A to spark growth. MCHP is a textbook value and dividend growth stock that deserves a place in value investors' portfolios.

Investors looking for a safer bet with lower growth and less risk from MCHP's recurring revenue from customers may find this a good play. For someone who works for the company or believes in the products and culture, I suggest looking to buy shares on this dip and to continue to buy if it goes under $80 a share. Just don't expect Nvidia or AMD type semiconductor returns. MCHP is now a value stock that we buy when cheap and trim when expensive, slowly collecting the dividend as we go. MCHP has outperformed the market but with a 1.6x beta, meaning it is 60% more volatile. Although true, it underperforms the SMH semiconductor ETF by a lot. MCHP is an okay hold, but make sure it meets your investment needs.

For further details see:

Microchip Technology: The Quiet Giant With Steady Cash Flow