SSNLF - Micron: Korean Memory Competitors Are Just Too Formidable

2024-01-17 00:57:26 ET

Summary

- Micron reported strong performance in its DRAM segment in its December 2023 earnings call, with sales reaching $3.4 billion, surpassing expectations.

- Korean memory manufacturers Samsung and SK hynix provided preliminary Q4 sales guidance in early 2024, with both companies experiencing robust earnings and momentum in 2024.

- South Korean competitors SK hynix and Samsung Electronics continue to outperform Micron in the DRAM sector in this comparative analysis.

- SK hynix stands out as the sole global mass-producer of HBM3, but limited HBM capacity is enabling Micron and Samsung to gain exposure.

Micron's Recent Earnings Call and Guidance

Micron DRAM Results

Micron ( MU ) reported FYQ1 2024 earnings conference call on December 20, 2023. The company reported robust performance in its DRAM segment, with sales reaching $3.4 billion, surpassing Street expectations by 7%. This marked a significant increase of 24% QoQ and 21% YoY. The majority of these sales were attributed to 1? nm and 1Þ nm in the DRAM category. Micron is on track for volume production and anticipates the introduction of 1Ý nm DRAM utilizing Extreme Ultraviolet (EUV) technology in CY25.

Samsung and Sk hynix Q4 Preliminary DRAM Data

In a comparison between actual MU DRAM data and its competitive Korean memory manufacturers, Samsung Electronics ( OTCPK:SSNLF ) and SK hynix ( OTC:HXSCL ) in early January 2024 provided preliminary Q4 sales guidance prior to their actual Q4 2023 earnings calls.

In the fourth quarter, Samsung reported DRAM bit growth of 29% and ASP increase of 12% on mobile DRAM restocking purchases by Chinese smartphone manufacturers.

Samsung's DRAM business is anticipated to experience robust earnings and momentum in 2024, driven by price increases and the ongoing qualification testing for HBM3/HBM3E chips.

For preliminary Q4 2023, hynix projects a decline in their bit shipments from +20% to +10%. Looking ahead to 2024, hynix anticipates high-teens percent year-on-year bit growth. The company observes the AI-driven HBM market expected to grow between 60% and 80% over the next five years, potentially at an accelerated pace, trending to represent a mid/high-teens percent share of the overall market.

Comparative DRAM Metrics

DRAM Revenues

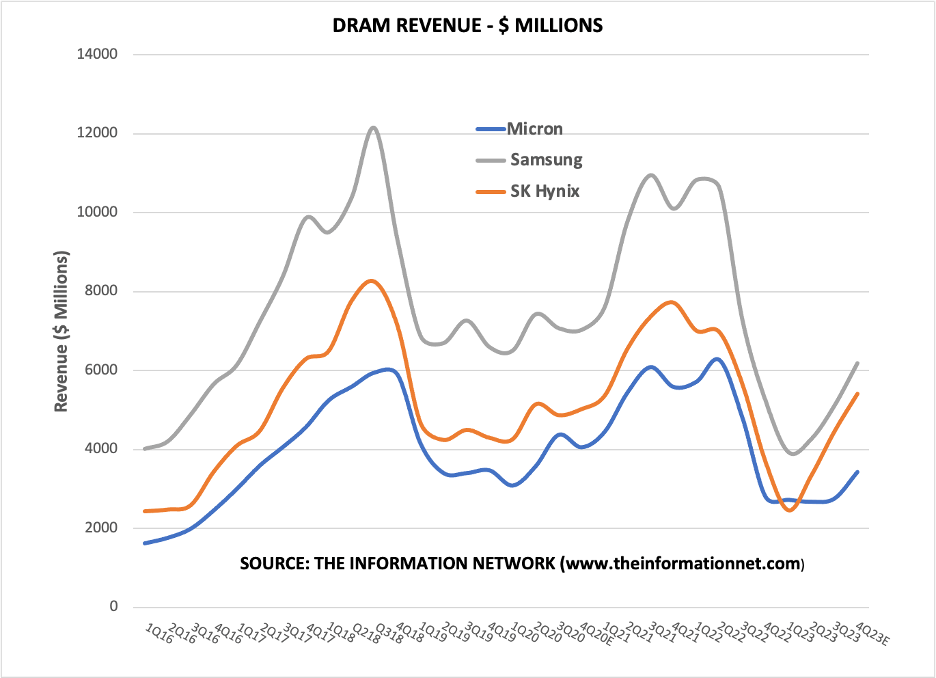

Chart 1 shows DRAM revenue for the period Q1 2016 through Q3 2023 (Micron's fiscal Q4 2023) and further estimated to Q4 2023 for Samsung and hynix, based on these company's guidance.

Micron's DRAM revenue growth of just 3% was significantly lower than that of competitors. The fact that HBM is priced at 7x those of standard DRAMs, and Micron shows minimal ramp in DRAM revenue indicating the company's minimal acceptance to customers.

Importantly, SK hynix, with a dominating share of the HBM market, shows strong revenue growth that started in Q2 2023 and should continue through Q4 2023.

Revenue growth between Q1 2023 and Q4 2023 are:

- 120.2% for SK hynix

- 57.3% for Samsung

- 25.9% for Micron

It is noteworthy that DRAM revenues from SK hynix are now about 70% of peak revenues before the recent 2022 memory downturn. In contrast, revenues from Samsung and Micron are now just 56% of peak revenues.

{kind=link}

Chart 1

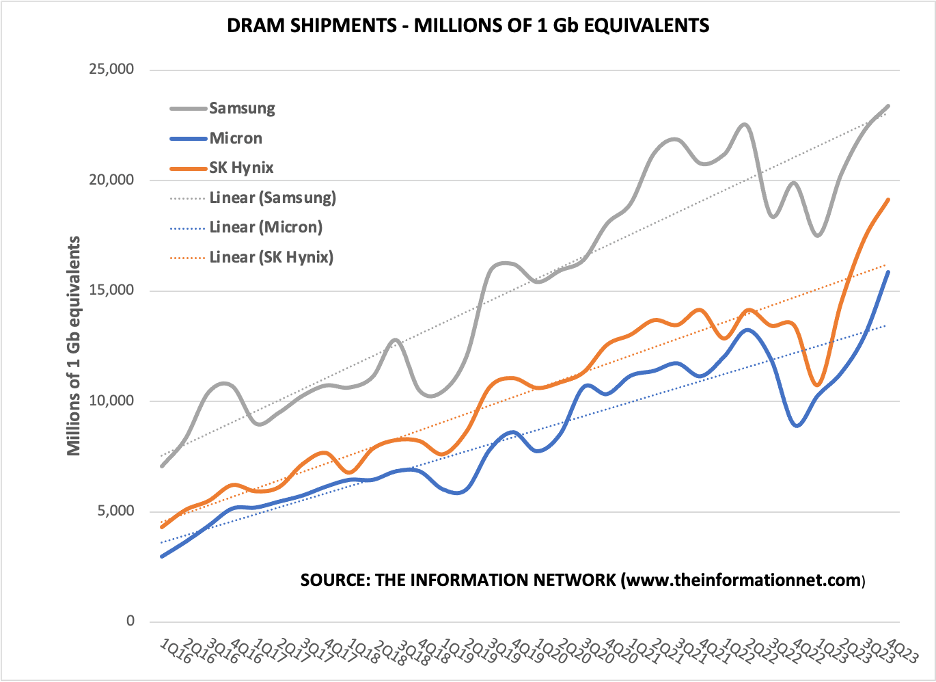

DRAM Shipments

Chart 2 illustrates DRAM bit shipments by company, highlighting the dotted trendlines. It is evident that Samsung previously held a substantial lead in the sector. However, in recent quarters, there has been a noticeable loss of market share to SK hynix, possibly linked to SK hynix's dominance in the High HBM market.

On the other hand, Micron's performance has notably lagged behind its competitors, reflecting a lower market share compared to industry counterparts. HBM is priced at 7x those of standard DRAMs, and Micron has shown minimal ramp in DRAM revenue indicates the company's minimal acceptance to customers.

Bit shipment growth between Q1 2023 and Q4 2023 are:

- 78.2% for SK hynix

- 64.3% for Samsung

- 54.3% for Micron

It is noteworthy that bit shipments from all three companies have now exceeded shipments prior to the recent memory downturn in 2022.

{kind=link}

Chart 2

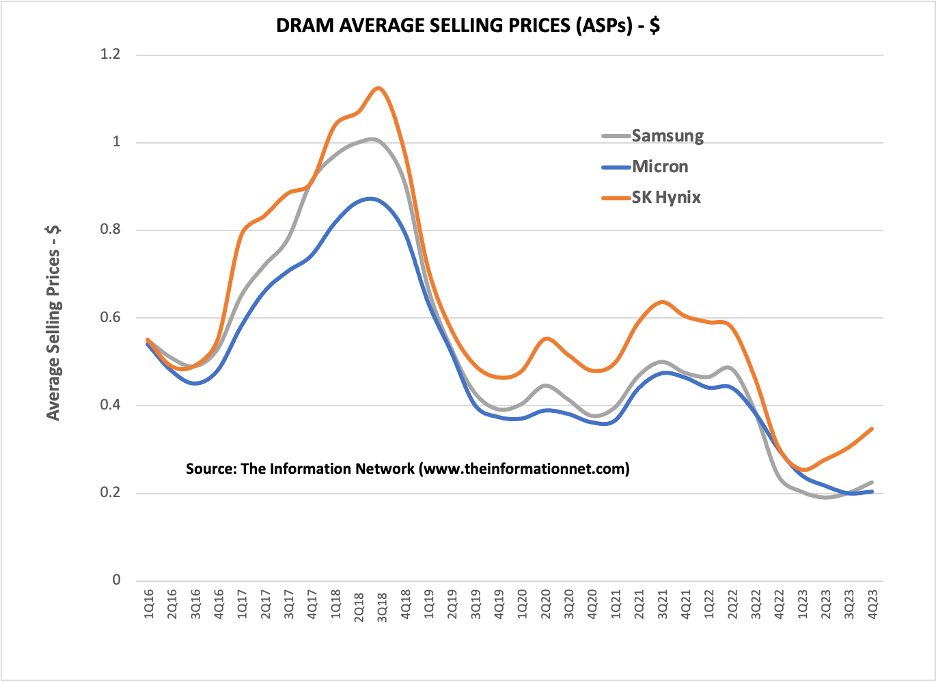

DRAM ASP

Chart 3 shows DRAM ASP data for the three companies. Micron shows little improvement in ASPs over the past year because (1) it still hasn't moved to EUV lithography and (2) it has no HBM market.

For Samsung and SK hynix, the opposite is true, and we can see improvements in ASPs, particularly for the latter, with strong HBM exposure.

ASP growth between Q1 2023 and Q4 2023 are:

- 36.7% for SK hynix

- 10.5% for Samsung

- -15.5% for Micron

{kind=link}

Chart 3

Competition Heating up With HBM as Capacity Fills

Micron positions its HBM3 Gen2 as a significant advancement, boasting a 50% improvement over base HBM3 chips from competitors Samsung Electronics and SK hynix. Micron's offering also provides 50% more memory density than the HBM3 Gen2, also known as HBM3E, introduced by rivals. The company anticipates a 15% performance boost compared to the 8 GT/second target set for SK hynix's HBM3E memory.

Samsung and SK hynix are planning to release samples of their HBM3E in the first quarter of the upcoming year, with volume production scheduled for the second half of 2024. SK hynix aims to commence mass production of the fifth-generation HBM3E in the first half of the next year and the sixth-generation HBM4 in 2026. Samsung is set to ship HBM3 and fifth-generation HBM3P starting in the fourth quarter of the current year, with no official announcement regarding the release date for HBM4.

SK hynix has won the Nvidia contract HBM3 and its Fab M14 is at 100% capacity. HBM capacity will increase at Fab M16. But because of capacity limits, Nvidia will be off-loading excess demand to Samsung and Micron. Also because of limited capacity, Samsung and Micron have enhanced exposure to other AI GPU companies listed in Table 1 above. I estimate Micron's share of the HBM3 market to drop to 2% in 2024.

Further growth of South Korean Competitors

Data in Charts 1-3 are for actual revenues for Micron for the fiscal quarter ending November 30 2023, while those for Samsung and SK hynix are actual revenues for the quarter ending September 30, 2023, and estimated revenues for the quarter ending December 31, 2023.

Data below fill in the missing months between the two Korean companies' actual and estimated metrics.

South Korea Semiconductor Exports

According to South Korean Customs trade data, chip production experienced a remarkable 42% year-on-year increase in November, marking the most substantial surge since the beginning of 2017. Simultaneously, chip shipments soared by 80%, representing the largest increase since the end of 2002. Inventories also witnessed a 36% rise, the smallest increase since February.

These data indicate a rapid recovery in South Korea's crucial chip industry, which has been grappling with a prolonged downturn affecting the economy for over a year. The positive trend serves as an optimistic signal for South Korea's major companies, including Samsung Electronics and SK Hynix. Moreover, it suggests a potential resurgence in demand from the global technology industry, signaling a tentative recovery.

For the month of December, exports recorded a significant YoY increase of 32.6%. well ahead of the export growth rate for chip products, including DRAM and NAND, in November at 19.2%. This figure surpassed the growth rate observed in November, which stood at 12.9%. The notable uptick in chip exports suggests sustained momentum and demand for semiconductor products, contributing to the positive overall growth in exports during this period.

Importantly, China is a key manufacturing hub - accounting for 40% of Samsung's total NAND production capability. It also accounts for 40%-50% of SK Hynix's DRAM chips and 20% of its NAND capacity.

South Korea Semiconductor Equipment Imports

South Korea's trade data for November includes imports of semiconductor capital equipment. Total imports for November were $834 million, remaining flat MoM and experiencing a 40% YoY decline from $1.39 billion.

The 3-month average imports showed a -22% YoY decrease, with October and November combined reflecting a -32% YoY contraction, compared to -13% YoY in 3Q23.

Highlights at a tool-type level include:

- Lithography: November imports for lithography-related equipment were $237 million, showing a -24% YoY decrease.

- Etch: November imports were $126 million, down by -51% YoY.

- Deposition: Imports of deposition equipment were $219 million in November, roughly flat from October and slightly down from $229 million a year ago.

- Inspection: Imports of inspection tools were $180 million in November, up slightly from $178 million in October but down by -28% YoY, compared to +3% YoY in 3Q23.

Investor Takeaway

Entering 2024, the DRAM market anticipates a gradual recovery initiated in the second half of 2023. However, Micron faces ongoing challenges in the HBM segment, competing against SK Hynix, which holds a strong position in HBM chips, providing a favorable outlook for accelerated improvements in both ASP and bit growth compared to Micron and Samsung.

Notably, SK Hynix stands out as the sole global mass-producer of HBM3, securing exclusive supply arrangements with Nvidia ( NVDA ) for the H100 Tensor Core GPU. Predictions indicate a substantial 45% YoY surge in HBM chip sales for SK Hynix in 2023, followed by a notable 40% YoY increase in 2024, posing a significant challenge for Micron.

SK Hynix's continued technological advancements and its established design prowess in HBM technology, along with key partnerships with Nvidia and TSMC, position it for sustained growth in the evolving semiconductor landscape.

While Micron emphasizes the performance gains of its 1?-based HBM3 Gen2 products, SK Hynix's ongoing innovation and partnerships underscore its resilience and competitiveness in the dynamic market. The collaboration with Nvidia and TSMC further strengthens SK Hynix's foothold, signaling potential headwinds for Micron in the evolving landscape of high-performance memory solutions.

For further details see:

Micron: Korean Memory Competitors Are Just Too Formidable