QQQ - Micron Technology Stock: Q3 Earnings Should Be Ignored By Investors

2023-06-21 12:00:42 ET

Summary

- Micron is a business with deeply cyclical earnings, and this down cycle is particularly deep.

- It's important to embrace this volatility, only buy when the stock price is very low, and be prepared for it to fall further, while still aiming for big returns.

- The biggest lesson for investors is that nobody knows what earnings will do in any given quarter, but the cycle will eventually turn up within 2-5 years.

- I have found a medium-term strategy works best for investors with these kinds of deeply cyclical stocks.

Introduction

Since I have an unusual investment approach for stocks like Micron ( MU ), I like to begin my articles by reviewing the results of my previous public articles with the hope they might add a little validity to my overall investment process. I've written about and purchased Micron stock twice in the past five years. Both times, I shared the price at which I was prepared to buy Micron in articles before the price actually fell to those levels. Those articles can all be found on my Seeking Alpha profile page, but I will link to a few of them in this article as well for quick reference. My first "buy article" on Micron was titled " I'm Buying Micron (Even If It's Not Different This Time) ", published on October 25th, 2018. I would hold that position for about 14 months until December 31st, 2019 when I sold and published the article " Profiting From Micron's Cycles: A Case Study ". Here are the returns in between the publication of those two articles.

I did really well with that investment and roughly doubled the returns of both the S&P 500 ( SPY ) and Invesco ( QQQ ) over the same time period.

During the March 2020 sell-off, I was expecting a deep recession so I didn't buy Micron during that decline, but I did cover the stock again last fall when I purchased both it and Advanced Micro Devices ( AMD ). I more or less used the same process I used in 2018, and several of those lessons can be found in my buy article " 6 Lessons For Micron, AMD, And Nvidia Investors ". (Unfortunately, Nvidia never hit my buy price. You can't win them all, I guess.) I'm still holding my Micron position and this is how it has performed since last fall's article.

In nine months, it has returned about 35%. Significantly more than the S&P 500, and slightly more than even the red-hot QQQ. So, we are on a pretty good track right now. Importantly, with this Micron position, my goal is a 100% return within five years (though usually, 2-3 years is the more typical time frame this strategy takes to play out).

If we put the two Micron purchases together, they've returned about 100%, and I had a 2.75-year period when I was out of the stock and I was able to take that money and invest it in something else with better return potential (which is what I did). In order for a buy-and-hold investor to have done similarly well with the stock, they would have had to purchase it back in late-2018 to mid-2019 or earlier than mid-2017 and then held it through today. So, I've done very well with Micron stock over the years with this strategy.

Accept Both What We Know And What We Don't Know

There is a tendency when it comes to deeply cyclical businesses like Micron for investors to do two things. The first is to assume that the business is no longer cyclical (or to be unaware of its cyclical nature altogether). And the second is to think that if one just does enough homework, one can accurately predict short-term earnings and stock price movements. I'm going to address the former issue first.

{kind=link}

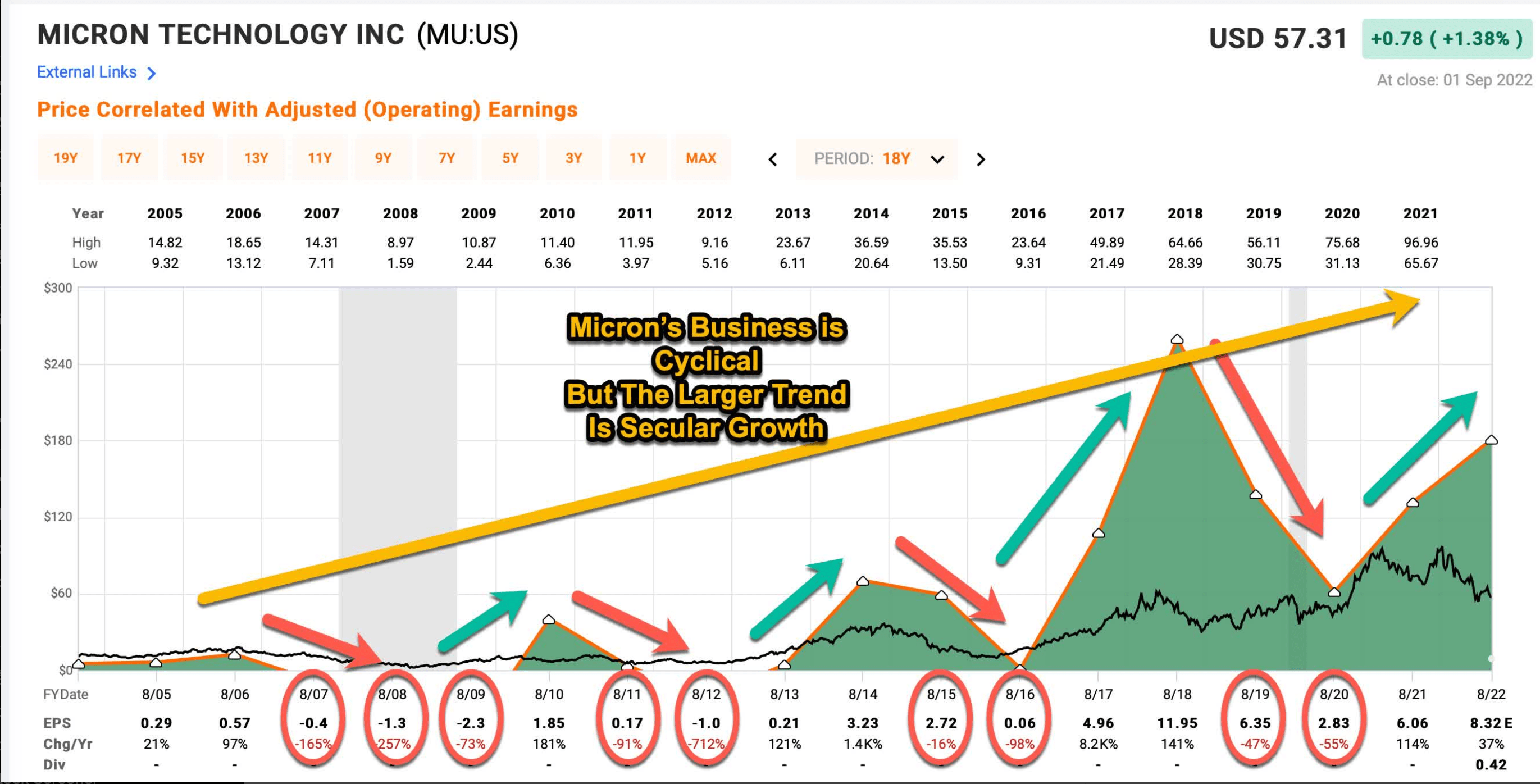

Above is a copy of a FAST Graph I used in one of my Micron articles last fall where I shared the price I would likely start buying the stock. The dark green shaded area represents Micron's historical earnings per share. I consider earnings drawdowns that are deeper than -50%, which also later recover in a timely manner, to be deeply cyclical. If there is a trend of higher earnings peaks and higher price peaks over various cycles, that is a sign of a high-quality deep cyclical I would be interested in buying if the price was right. (If the earnings and price do not have a history of recovering in a timely manner, then I simply avoid those stocks because cyclical businesses can be very dangerous if they don't recover.) Also worth noting, is that at this time, Micron also had a history of earnings troughs making higher highs, which indicates an underlying secular growth trend. On one hand, this secular growth trend makes it easier to buy such a volatile stock during down cycles because it's a sign of a strong business. On the other hand, it means that sometimes my "buy prices" don't get hit because investors are more willing to pay higher prices. (This is why I wasn't able to buy Nvidia at the price I wanted last fall.)

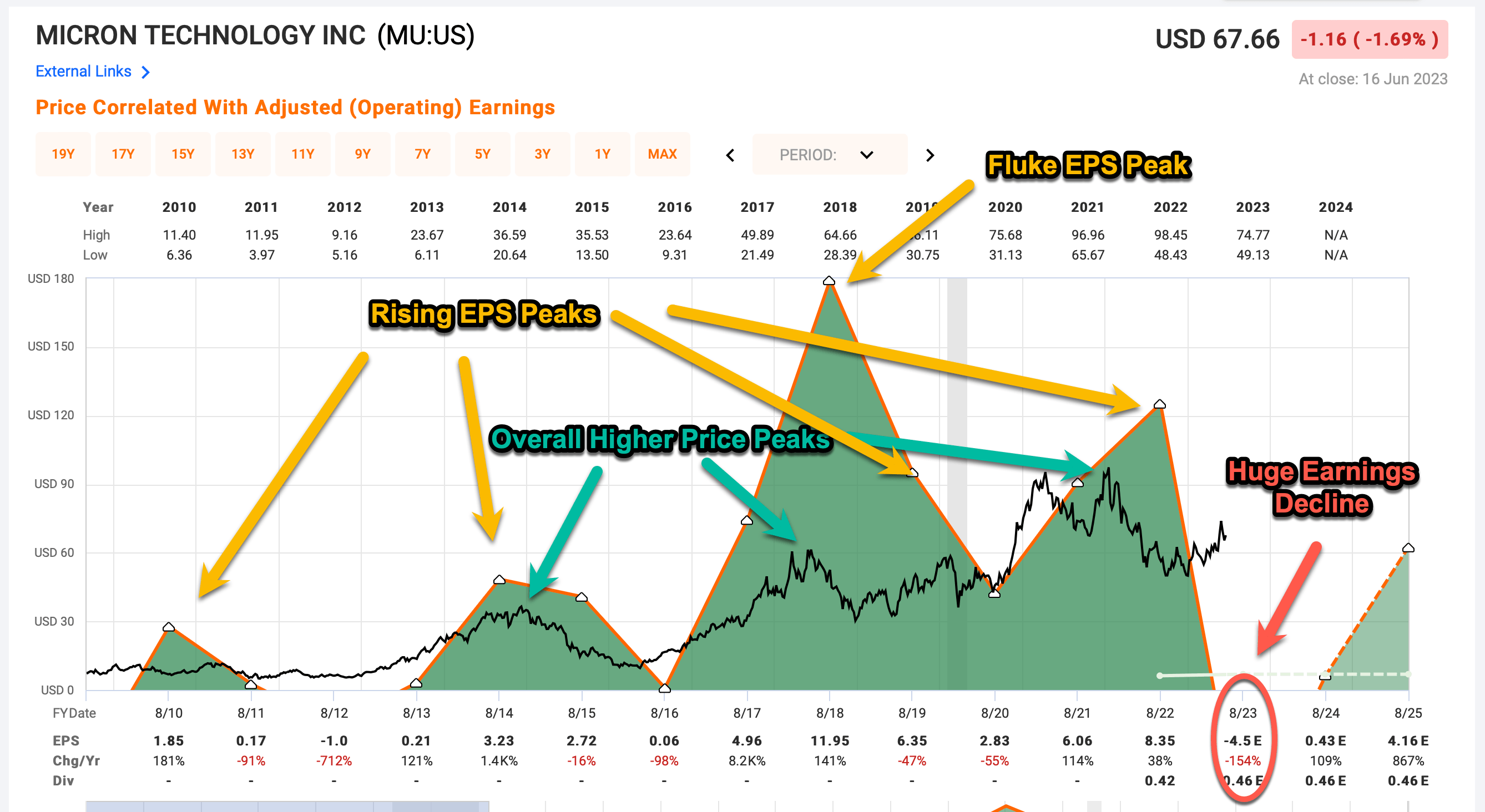

In terms of Micron's expected earnings this year, an interesting change has occurred. The previously very clear pattern of higher trough earnings is likely to end this year.

{kind=link}

I know there are a lot of arrows in the graph above, but I want to point out how wonderful things were going for Micron over the past 10-15 years or so. They had a fluky high EPS year in 2018, probably due to corporate tax cuts, but putting that year aside the overall trend was of a deeply cyclical business in a clear secular growth trend. Until we get to this year when earnings are totally crashing.

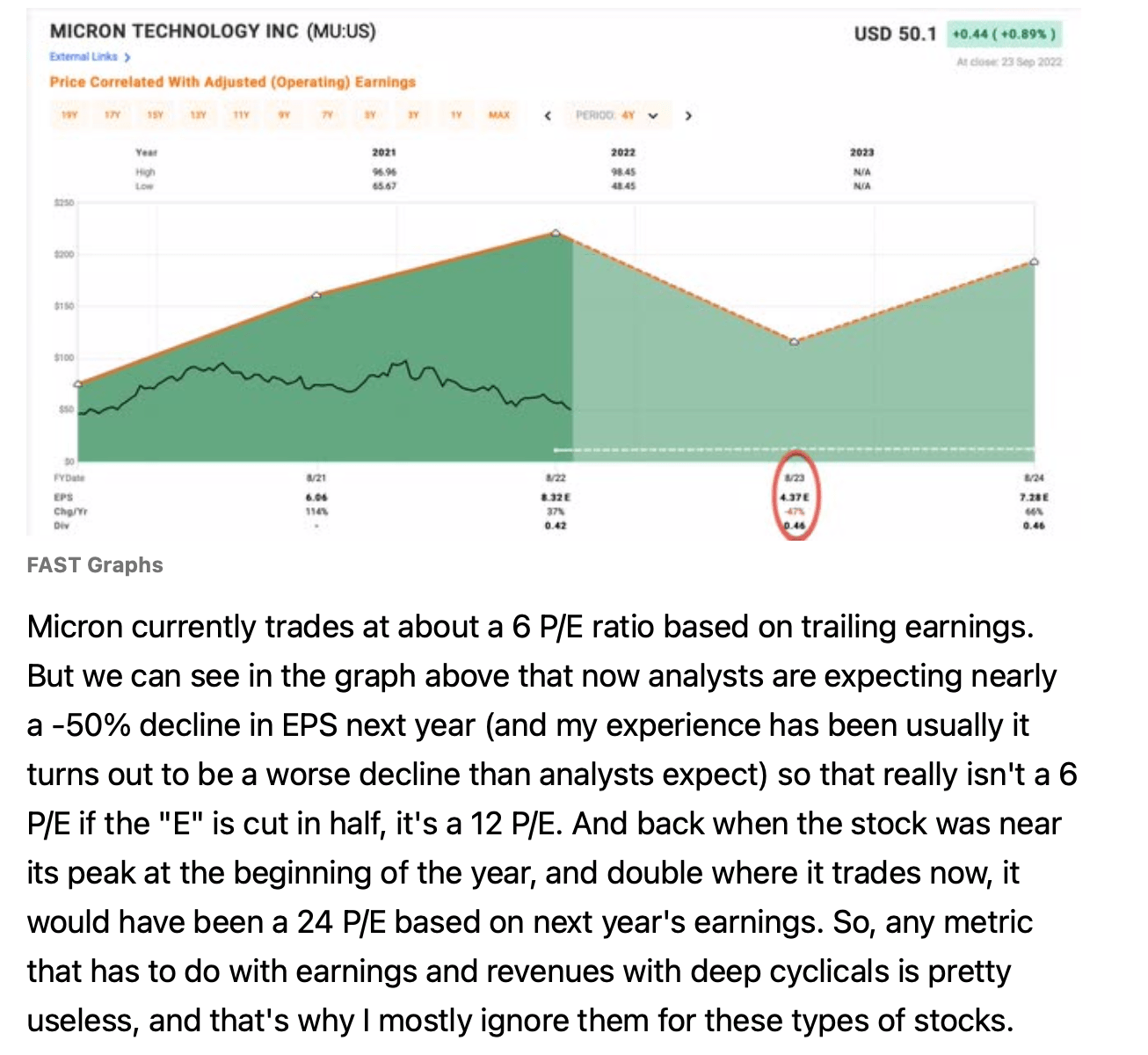

Before I move on, I want to share a graphic and quote from my last Micron article where were see what analysts' earnings estimates were for 2023, just nine months ago.

{kind=link}

Analysts were expecting $4.37 per share for 2023 just nine months ago. As I pointed out, these sorts of earnings declines are almost always worse than what analysts expect. In this case, they were massively off, and now are expected to be negative -$4.50 per share and we are already two quarters into the fiscal year. Some of the negativity is certainly due to China's new regulations , but not most of it.

These analysts are paid lots of money to predict Micron's earnings and 29 of them were covering the stock. Historically they are correct 50% of the time, the same as a coin flip. So, if a bunch of highly-paid and specialized analysts can be this wrong, it's wise to show some humility when it comes to predicting short-term earnings. Notice, that when I bought Micron, I didn't pretend to know where earnings would bottom. I suspected analysts were too optimistic, but the honest answer during the down cycle of a deeply cyclical business, if someone asks what earnings are likely to do, is to admit we don't really know over the short term.

So, What Do We Know?

The main thing we know is that earnings are not very useful when trying to predict the future stock price of a deeply cyclical business like Micron. I would add that now, no matter what earnings come in at this report, if we are willing to stretch our time horizon out to 3-5 years from now, it's highly likely at that time earnings will be both positive and also higher than, say, $6.00 per share, which is around where they were pre-pandemic. And, we also know the last time earnings were around that level, the stock price peaked at roughly around $100 per share.

Making these reasonable medium-term assumptions based on Micron's history of recovering from downcycles can guide our entry into the stock at a price that is acceptable to us. Personally, I aim for higher-than-average returns when picking individual stocks. And, sometimes I'm wrong (about 20% of the time using this strategy I take a significant loss). So typically with a deeply cyclical business and stock like Micron, my base-case assumption is that even if a downcycle turns out to be pretty big (as in a recession case), I aim for a 100% return within five years. This works out to about a 15% CAGR if it indeed takes five years for the stock to recover its old highs. If it takes less time, that CAGR goes higher. (My average CAGR of my two Micron purchases right now is about 35%, but so far I haven't had to hold the stock through a recession, yet.) In order to meet my return goals, I basically need to buy the stock when it is about -50% off its highs, which is what I did last fall.

A person with return goals that are lower than mine certainly might have been happy to pay more for the stock. That's perfectly fine. However, there is another factor to consider, and that is how much downside a person can tolerate before they question their thesis, panic, and sell. Micron stock has a history of very deep price drawdowns, as I share in the table below.

| ~Year |

| ~Time Until Bottom |

| ~Duration |

| ~Depth |

| 1984 |

| 1 year |

| 9 years |

| -89% |

| 1986* |

| 6 months |

| 18 months |

| -79% |

| 1988 |

| 6 months |

| 1 year |

| -42% |

| 1989 |

| 18 months |

| 4 years |

| -71% |

| 1995 |

| 1 year |

| 4.5 years |

| -80% |

| 2000 |

| 2.5 years |

| 18 years+ |

| -92% |

| 2004* |

| 1 year |

| 2 years |

| -47% |

| 2006 |

| 1.5 years |

| 7 years |

| -90% |

| 2014 |

| 1 year |

| 3 years |

| -73% |

| 2018 |

| 6 months |

| 2 years |

| -53% |

| 2022 |

| ? |

| ? |

| -50%? |

In 2014, even without an economic recession, the stock fell more than -70%. In previous recessions, Micron has fallen -90% off its highs. Even buying the stock at -50% off its highs as I did, if it were to go on to fall -90%, means I would have to suffer a -80% drawdown in my position. (Imagine a $100 stock that you buy at $50, falling to $10. That's a -80% decline for those buying at $50.) You can only imagine what it would feel like for investors who bought the stock when it was less than -50% off its highs.

Micron is notably an extreme example. Usually, most deep cyclical stocks aren't this extreme. But I generally try to avoid suffering -50% drawdowns or greater if I can, while still giving myself a reasonable chance to actually buy stock. The main thing, though, is to be mentally prepared for what is a very possible deep drawdown if things don't go well, and not to be surprised by it. It's also important not to double down or triple down too early in this drawdown process. Buying after a -30%, then a -40%, then a -50% drawdown, only to have the price fall an additional -70% off one's cost basis can be crushing. So, as I shared in my previous MU articles, I am prepared to buy more if we experience a really deep drawdown, but I'm not making that second purchase until the price is really deep.

Why investors should ignore Micron's Q3 earnings report

Hopefully, I have shown some evidence here that nobody can predict what MU's earnings will be over the next few quarters. But, given their historical cyclical patterns, even if this turns out to be a bad earnings downturn, usually within five years the earnings and stock price will recover. During the great financial crisis, it took seven years for a peak to new peak recovery. Right now, looking out 2.5 years to 2025, analysts expect $4.28 per share. That seems reasonable to me, and 2026 earnings of $6.00 per share, if there isn't a significant recession, seems reasonable as well. If there is a recession (which is currently my base case), then we should probably push that $6.00 of earnings expectation out to 2027, or maybe even 2028 if the recession is a bad one.

What an investor needs to decide is what sort of returns they are looking for. Below I have provided a table that shares what the returns would be from today if it takes a certain number of years for MU to recover its old high price of $98.45.

| Years Until Recovery |

| Return CAGR |

| 1 |

| +45.55% |

| 2 |

| +20.63% |

| 3 |

| +13.22% |

| 4 |

| +9.83% |

| 5 |

| +7.79% |

If you are in the camp that the US and other major economies will avoid a recession within the next 24 months, then MU looks pretty attractive at its current price. If you think maybe there will be a mild recession but it won't last very long, the current price is borderline for me, with a 13% CAGR expectation. If you think the odds of a recession within the 24 months are pretty high, which would push the recovery time out farther into the future, the returns don't look great if buying at today's price.

Remember, this is just the upside potential. The downside potential I would estimate, given we've had quite a bit of inflation, somewhere between -60% and -70% from today's prices if MU experiences a downcycle similar to what it has experienced during past recessions or deep downcycles. Personally, while I'm still holding my Micron position, I wouldn't buy with new money unless the price was back down near my original buy price of $49.23 per share. I also don't plan to sell until it's up near $100 per share.

Conclusion

It is extremely important as an investor to admit what we don't know. With some businesses, earnings are relatively predictable. Micron is not one of those businesses. And it's possible that even if you get the earnings call correct, the market doesn't care. From the time I bought Micron last fall until today, analysts' earnings expectations were off by around -$9.00 per share to the downside, but guess what the stock price did? It rose more than +30%! Even if a person got the earnings expectations correct, they would have been wrong about the stock price if they had followed those expectations. (And it wasn't just this year's earnings, next year's are now about -40% lower than they were nine months ago.) If you read what I wrote at the time, I expected that earnings would likely miss expectations, but I bought anyway. It doesn't make any logical sense to do that unless one zooms out and looks at the longer-term picture.

No matter what earnings do this quarter, or what guidance is, think about 1) how long might earnings take to get to 2019 or 2021 levels of about $6.00 per share, 2) what sort of returns are you looking for, and 3) how much pain are you willing to suffer while waiting? Answering these questions will help you estimate at what price Micron is a buy for your situation.

For further details see:

Micron Technology Stock: Q3 Earnings Should Be Ignored By Investors