ATVI - Microsoft Corporation Goes Beast Mode (Rating Downgrade)

2023-05-07 12:00:00 ET

Summary

- Microsoft Corporation reported stellar fiscal Q3 earnings results last week.

- The growth of Microsoft’s core and cloud businesses along with the rise in popularity of its AI products could help the company outpace its competitors.

- Even though there are some regulatory and macroeconomic challenges that Microsoft would face, the company’s stock nevertheless remains a decent investment in the current environment.

After the release by Microsoft Corporation ( MSFT ) of its latest earnings report for Q3, it’s safe to say that there’s nothing not to like about the company in its current form. Microsoft’s core business continues to generate record returns, its cloud solutions once again gained new customers, and its flagship AI products are already disrupting the tech industry and could help the company create additional shareholder value for years to come. Therefore, even though there are several challenges and risks that Microsoft is likely to face in the foreseeable future, the latest earnings results show that the company nevertheless remains a decent investment among its Big Tech peers. Microsoft has all the chances to continue to reward its shareholders in the coming years.

Microsoft Continues To Deliver

Last week, Microsoft revealed a stellar earnings report for Q3 which showed that its business generated $52.86 billion in revenues, up 7% Y/Y and above the consensus by $1.85 billion, while its non-GAAP EPS came at $2.45 and also above the consensus by $0.22. Such a great performance helped Microsoft’s stock to reach new 52-week highs at which the business’s shares trade to this day. There are reasons to believe that the momentum won’t fade away anytime soon.

One of the most important things that needed to be highlighted is the fact that Microsoft’s core productivity and processes business managed to grow at a double-digit rate and generated $17.5 billion in revenues, up 11% Y/Y, despite all of the macroeconomic challenges that had a negative impact on its Big Tech peers. On top of that, the company has also managed to increase its Microsoft 365 Consumer subscriber count to 65.4 million, up from 58.4 million a year ago. At the same time, its social media LinkedIn experienced another quarter of record engagement as its revenue and sessions were up 8% and 15%, respectively.

All of this shows that Microsoft continues to be resilient to the ongoing global uncertainty, and it’s one of the main reasons why its stock is currently one of the best-performing stocks of the S&P 500 Index (SP500). Even though enterprises are cutting costs and laying off people, Microsoft is able to capture more market share in the cloud industry in such an environment thanks to the increase of new customers which helped its cloud business to generate $22.1 billion in revenues in Q3, up 16% Y/Y. As the cloud market becomes a $237 billion opportunity, Microsoft has all the chances to become one of the biggest beneficiaries of the forecasted increased demand for cloud solutions in the following years, especially since its closest rival Amazon.com, Inc. ( AMZN ), lost market share in the March quarter .

Last but not least, Microsoft’s major leap forward in the AI field thanks to being one of the major backers of OpenAI’s ChatGPT chatbot has all the chances to help the company gain a greater market share in the digital advertising field. Even though it’s unlikely that Alphabet Inc. ( GOOG , GOOGL ) aka Google will be dethroned from its dominant position in the digital advertising business anytime soon, there’s nevertheless a possibility that if Microsoft continues to be the leader in the AI field, then it has all the chances to disrupt the operations of its biggest competitor in the long run. The company has already been testing ads within its Bing AI-powered chatbot, which could help its digital advertising business create new growth opportunities. As such, it’s safe to say that there’s nothing not to like about Microsoft, which so far has been performing significantly better than a lot of other companies in the current environment, and there are reasons to believe that it would continue to exceed expectations in the following quarters.

What’s Next For Microsoft’s Shares?

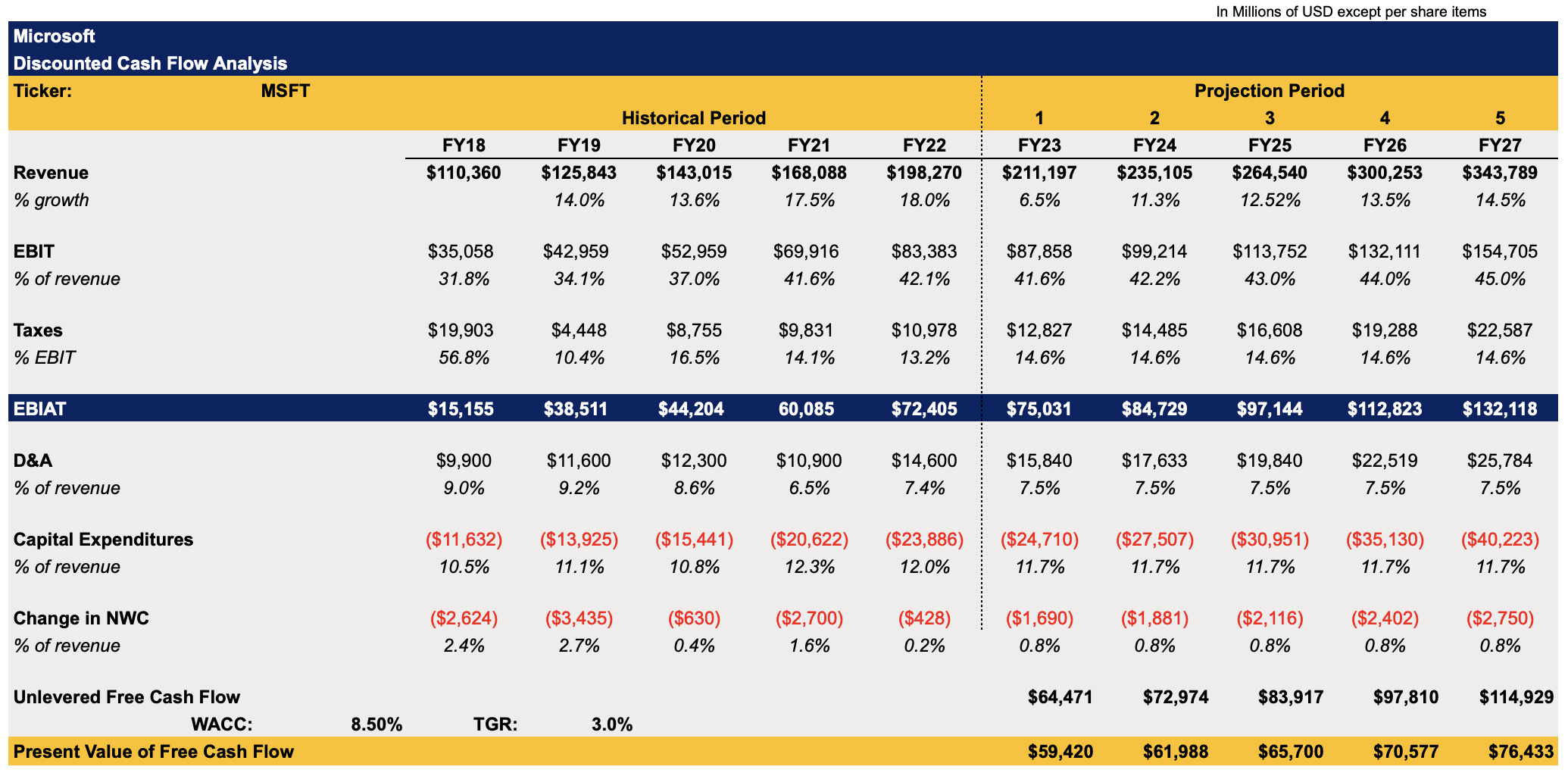

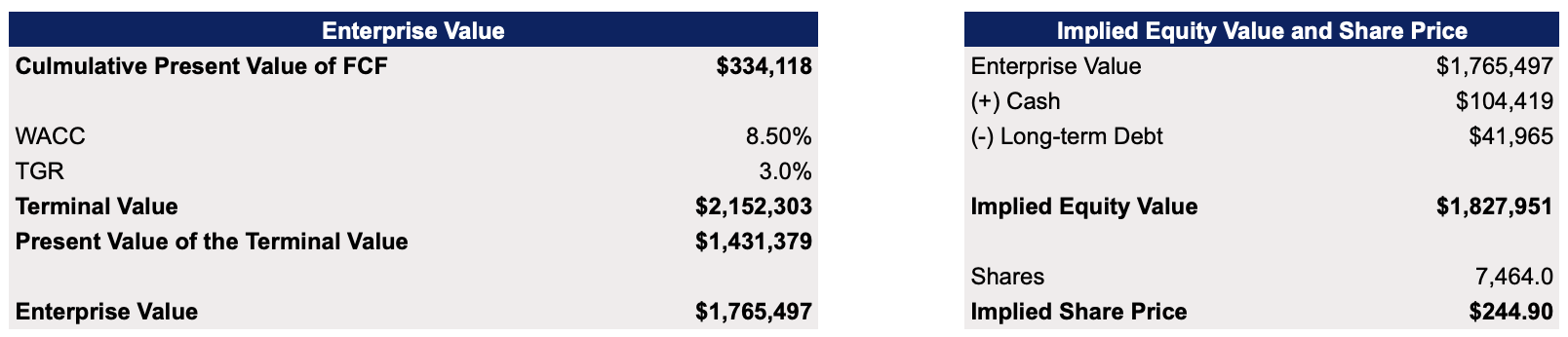

With all of that in mind, it makes sense to update Microsoft’s discounted cash flow ("DCF") model, which in early March showed the company’s fair value to be $241.35 per share. Thanks to the great performance in Q3, the street became more optimistic about the company’s growth prospects for the following years and increased their revenue and EBIT growth expectations for the those years. These changes are reflected in the updated model below. Even though Microsoft’s management noted how commercial bookings are expected to be relatively flat in Q4, the company should nevertheless be able to improve its Y/Y sales this year despite all the macroeconomic challenges and is likely to continue to accelerate the pace of growth in the future thanks to various opportunities that were explained above. All the other metrics in the updated model mostly have been unchanged.

Microsoft's DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

{kind=link}

The updated model shows Microsoft’s fair value to be $244.90 per share, which is an increase from the previous valuation calculations but also significantly below Microsoft’s current market price.

Microsoft's DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

{kind=link}

While it might seem that Microsoft’s stock might not be worth owning at the current levels, the reality is that the company is currently leading in AI development among its Big Tech peers. If it’s able to extend its lead and continue to outpace others, then the business might exceed all the growth expectations. In such a scenario, Microsoft’s shares could continue to keep momentum and further appreciate, as is happening with another AI name, Nvidia Corporation ( NVDA ). It also trades greatly above its fair value, but the AI hype train keeps the momentum going. Considering this, there’s still a case to be made that Microsoft could continue to create additional shareholder value, but the margin of safety of owning its shares at the current levels is nevertheless thin in comparison to a few weeks ago.

There Are Still Reasons To Be Cautious

Since Microsoft’s stock doesn’t have a lot of margin of safety at the current levels, even though its shares could retain their momentum and appreciate further, there’s nevertheless a risk that a potential recession along with the AI hype train going off the rails could kill the growth story in the short-term. Under such a scenario, there’s a possibility that despite all the growth opportunities, the general market fear could prevail and Microsoft’s shares could depreciate to more suitable levels.

On top of that, Microsoft has recently faced another roadblock in its quest to purchase Activision Blizzard, Inc. ( ATVI ). Last week, the UK regulator decided to block the deal citing competition concerns in the cloud gaming field. The problem with such a decision is that cloud gaming is still in its infancy and it’s unlikely that it will play an important role in the overall gaming industry anytime soon.

While the global gaming market was worth $184.4 billion in 2022, the cloud gaming market accounted for only $2.4 billion of that market. That’s one of the main reasons why Microsoft is planning to appeal the decision and has a chance to win such an appeal in the foreseeable future. However, there’s still a risk that if the deal is not completed by July 18, then Microsoft would be required to pay $3 billion in breakup fees to Activision, and this is something that investors need to keep in mind.

Last but not least, there’s also a risk that the upcoming AI regulations could slow down AI development. This could lead to a decrease in monetizable opportunities and make it harder for Microsoft to capture additional market share in the digital advertising industry from Google.

The Bottom Line

While there are certainly reasons to be cautious about some aspects of Microsoft Corporation’s business in the coming months, there’s nevertheless an indication that the company has everything going for it to continue to generate aggressive returns and create additional shareholder value at the same time. As such, I would argue that if Microsoft Corporation management continues to scale the company’s core and cloud businesses while its AI products continue to attract new users, then Microsoft would be able to outpace the competition. This would make its stock an attractive investment in the long run. However, the lack of the margin of safety along with the increase of macro risks could nevertheless kill the momentum and force a depreciation of Microsoft Corporation shares in the short to near term.

For further details see:

Microsoft Corporation Goes Beast Mode (Rating Downgrade)