MVST - Microvast: Different Risks Loom Large Around The Company

2023-12-08 14:31:11 ET

Summary

- Microvast Holdings is a battery technology company that specializes in designing, developing, and producing battery components and systems, focusing mainly on electric commercial vehicles and utility-scale energy storage systems.

- The company is based in Stafford, Texas with manufacturing facilities in the United States, China, and Germany.

- Despite Microvast's considerable growth prospects, the company encounters risks related to execution, financial performance, raw material expenses, and its dependency on China.

- Microvast has experienced a significant decline in stock value in the last several years, but I see no concrete reason to buy this stock now.

- Losses continue to be high, and there is a significant negative trend in operating cash flow.

Microvast Holdings, Inc. ( MVST ) operates as a battery technology company specializing in commercial electric vehicles (EVs) and energy storage systems. The company distinguishes itself through a vertically integrated manufacturing model and a commitment to robust research and development.

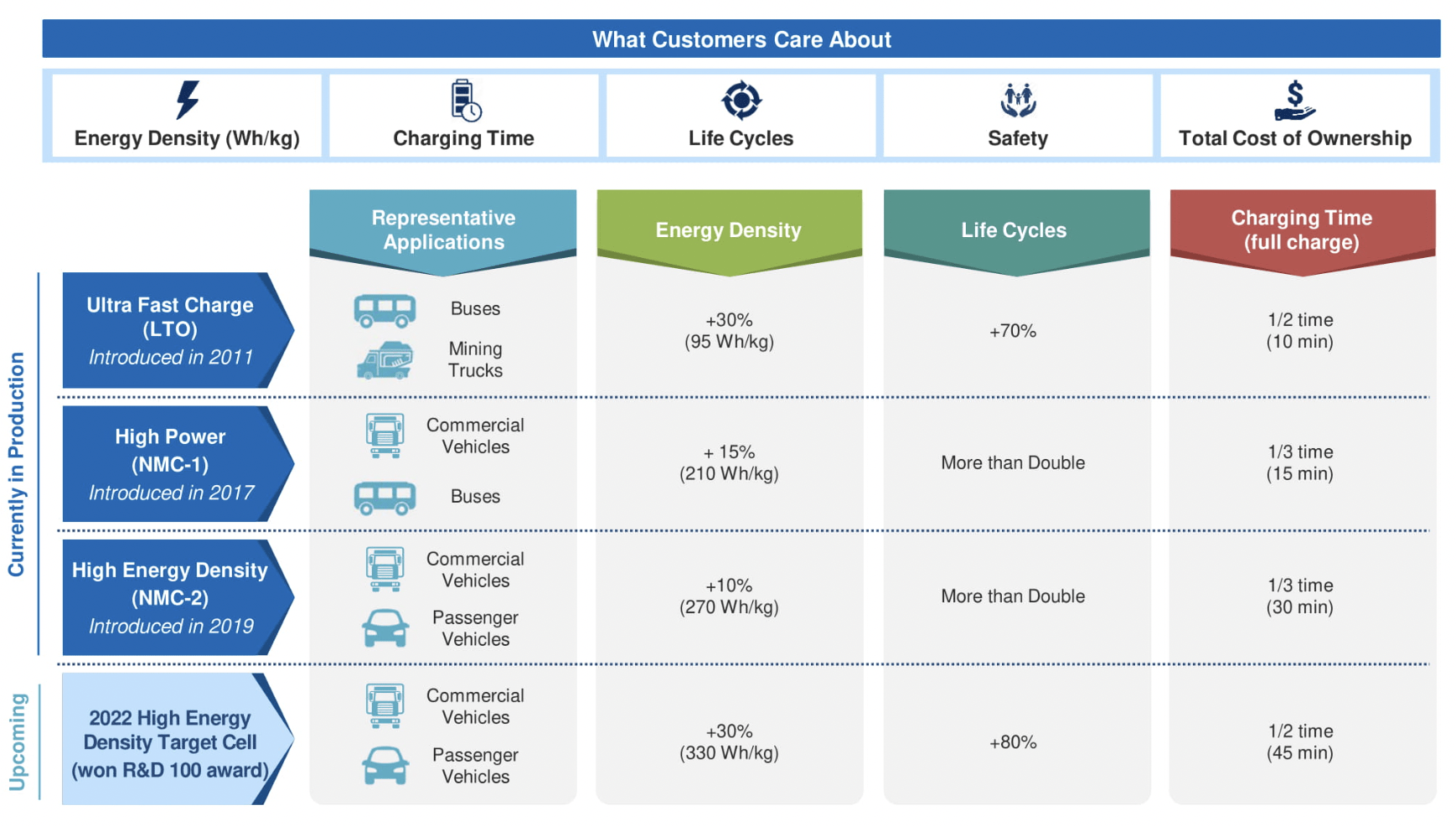

Microvast has successfully engineered battery solutions with notable features, including rapid charging capabilities, extended battery lifespan, and enhanced safety measures.

{kind=link}

Investment t hesis

While Microvast is currently witnessing an increase in demand, especially for its newly introduced 53.5Ah battery cell in 2022, it is important to acknowledge the significant risks associated with the company. This analysis will delve into the challenges Microvast faces in terms of execution, financial stability, raw material expenditures, and its dependence on China.

Despite the already significant decline in Microvast's stock value over the past few years, my investment rating for the company's stock is still a Sell . This stance is rooted in the fact that Microvast has yet to achieve profitability, and the question remains when will it be. The company is grappling with heightened competition in the EV battery market as well as facing potential additional financing, hence it lacks a compelling reason to buy or hold the stock.

With losses continuing to mount, another concern is the negative trend in operating cash flow that exacerbates the overall financial outlook. The combination of these factors underscores the risks and undermines Microvast Holdings as a viable investment option.

{kind=link}

How is the company doing?

In 2022, Microvast reported a loss of $158.2 million and foresees staying in a negative cash flow position throughout 2023. These financial challenges stem from substantial investments in research and development, along with significant capital spending. Microvast's financial strategy raises concerns, as the company appears poised to rely on additional debt to fuel its expansion plans, seeking to avoid undue equity dilution. This approach necessitates careful monitoring, as an over-reliance on debt can pose risks to the company's overall financial health.

Execution risk also looms large over Microvast's operations. The successful introduction of new capacity, scaling up production, adhering to delivery schedules, and managing expenses are critical aspects that investors need to keep a close view on. Delays or changes in the company's decisions are not uncommon , so it would add an extra layer of risks to the company.

Furthermore, Microvast's revenue is significantly derived from China, exposing the company to regulatory risks tied to its manufacturing operations and partnerships within the country. The escalating geopolitical tensions between the U.S. and China introduce an additional layer of uncertainty. Potential U.S. restrictions on exporting specific battery technologies to China could impact Microvast's operations, underscoring the importance of closely monitoring regulatory developments and their potential implications on the company's market presence.

The most concerning risk of all

J Capital Research USA LLC, a U.S.-registered company, recently published a report to fairly and correctly address some of Microvast's public statements. Contrary to the chairman's claim of having 2,500 employees at the Huzhou, China plant, J Capital's on-site investigation revealed a workforce significantly smaller. The report, supported by images, videos, and interviews, suggests that the Huzhou factory operates at reduced capacity, raising questions about transparency and whether Microvast's management is withholding information from the public and shareholders. A photo available on their site taken post a Chinese holiday shows minimal activity, prompting concerns about potential issues within Microvast.

Furthermore, J Capital Research highlights a shift in perception among Chinese battery engineers. While in 2017, Chinese bus and truck companies were open to adopting MVST batteries, the recent report indicates a change. Chinese battery engineers no longer see Microvast Holdings as a competitive force in the industry, citing a lack of groundbreaking technology and leadership in production size or cost-critical elements for long-term success in the electric vehicle battery sector. These findings underscore potential challenges for Microvast and call into question its standing within the rapidly evolving electric vehicle market.

Financials

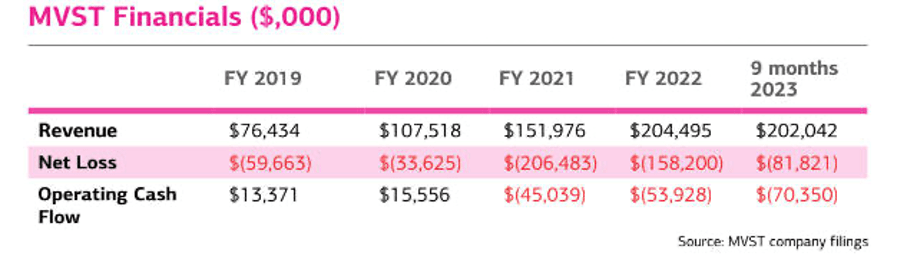

The provided image illustrates Microvast's income statement figures over the past few fiscal years. Notably, revenues and margins show a fluctuating pattern without clear consistency. Despite being in the initial stages of growth, Microvast reports negative net income, attributed to substantial investments in research and development to enhance its product offerings.

Seeking Alpha

While Microvast dedicates significant funds to sales and marketing for sales expansion, concern arises regarding its cash burn rate in previous years, posing potential challenges. On a positive note, the third quarter of the 2023 fiscal year showcased a robust performance, with $80.1 million in revenue, reflecting a noteworthy 107% surge from Q3 2022. This growth is driven by heightened demand for commercial vehicles in the European and Asia Pacific markets, aligning with increased production rates by original equipment manufacturers (OEMs).

Despite this revenue growth, profitability remains in negative territory. In Q3 2023, the GAAP net loss improved to $26.2 million from $36.5 million in Q3 2022. However, on a year-to-date basis, the adjusted net loss was $30.2 million, a decrease from $61.4 million in the corresponding nine-month period of the previous year. Despite the improvements, the overall financial results are perceived as suboptimal for a company in this industry.

Valuation

The company's consistent lack of profitability, combined with the projection that it won't be profitable in the near future, raises skepticism about the wisdom of investing in Microvast stock. Operating in a capital-intensive industry, Microvast's substantial upfront investments, coupled with persistent losses, pose a risk of cash flow problems, hindering the ability to meet financial obligations or invest in necessary improvements.

The current market capitalization of $403 million, at a forward P/E ratio and forward EV/EBITDA ratio of -3.2 and -17.37, almost in line with its industry peer Enovix. However, given Enovix's industry positioning, significant technical and commercialization progress, as well as financial health, both company's valuations would diverge, with MVST dropping further.

As a result, it is to my analysis that the company's valuation will take a dent and drop below the current level, alongside the negative impact on the stock price when the company announces additional equity or debt financing.

The recent sale of over 15% of director holdings in September, followed by another million shares in November, likely contributes to concerns about the company's potential over-valuation. The fact that even the management is divesting from the company at the current price level raises questions about the overall confidence in Microvast's valuation.

Conclusion

In conclusion, Microvast Holdings, Inc.'s growth potential is hindered by operational shortcomings, including a lack of operational free cash flow, high manufacturing costs leading to thin margins, and a capital-intensive model requiring substantial upfront investments. The company's persistent lack of profitability, coupled with escalating competition in the EV battery market, raises concerns about potential cash flow problems.

The current economic backdrop of inflation and high interest rates further diminishes the appeal of investing in Microvast stock. Adding to the skepticism, the recent substantial sale of shares by director Zheng Yanzhuan raises red flags for existing shareholders, making it advisable to exercise caution and refrain from investment in Microvast at this time.

For further details see:

Microvast: Different Risks Loom Large Around The Company