MVSTW - Microvast: The Management Is Selling And So Should You

2023-10-18 21:16:00 ET

Summary

- Microvast Holdings has experienced a significant decline in stock value and lacks revolutionary technology or cost/size leadership in the EV battery sector.

- The company's financials have been volatile, with moderate growth and a high level of capital expenditure.

- Microvast faces increasing competition in the EV battery market and lacks technological innovation compared to its competitors.

Continuing in my analysis of companies involved in the lithium battery world, I have chosen to study Microvast Holdings ( MVST ) this time around. This is a small company headquartered in Colorado, specializing in designing and producing batteries for two main applications: heavy EVs (trucks and buses) and energy battery storage ((ESS)).

Since its debut on NASDAQ, Microvast shares have lost over 80% of their value. In this analysis, I aim to answer a question: Is this a golden opportunity to buy at a very low valuation, or is the downtrend set to continue over the coming years?

In my opinion, it's not a good company to invest in, as it lacks at least one of the two critical factors to succeed in the long term in the EV battery sector: it neither has revolutionary technology, nor is it a cost or size leader in production. Despite a significant increase in the backlog over recent quarters, I believe it's better to sell the stock and invest elsewhere. Debt is not an issue, with only $5.3 million due before December 31, 2025. It's also worth noting that a few weeks ago, a manager of the company sold over 300,000 shares .

Contrary to what I suggested in my FREYR analysis , where I even proposed a short sell, in this case, I'll limit myself to saying that there are better companies for our capital. For instance, I recently revisited my analysis of Solid Power and believe it to be a much more intriguing small-cap within the same sector, with huge potential for an asymmetric bet.

Microvast: Business Model

All of Microvast's batteries are designed in Colorado. Production takes place in centers located in China (Huzhou), Europe (Berlin), and the United States. Operations in the USA are split between ESS system assembly in Windsor, Colorado, and battery production in Clarksville, Tennessee. The Clarksville center is not yet ready, but it is expected to start limited production in Q4 and then become fully operational by 2024.

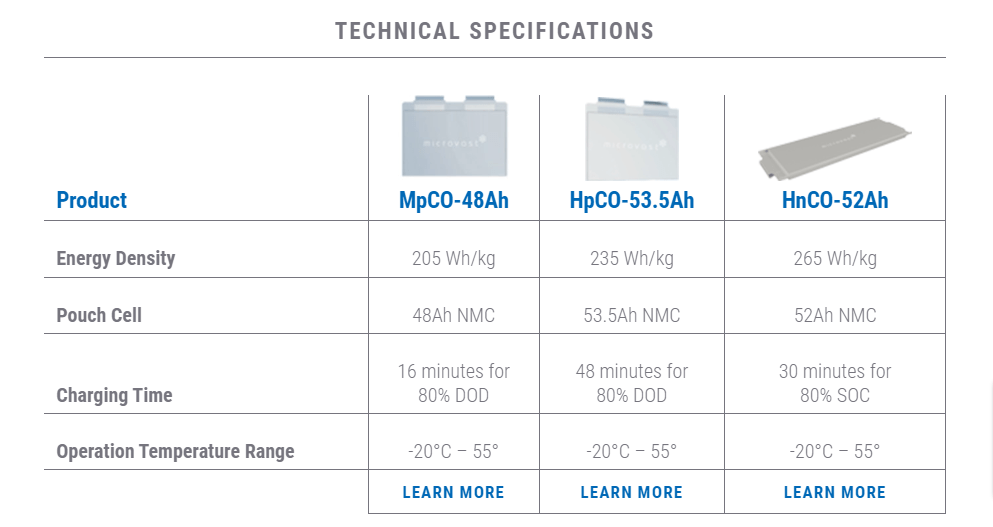

Over time, Microvast began producing various batteries, with its first successful models emerging in 2020. Currently, however, 80% of the backlog concerns the latest 53.5 amp model. Quoting from the recent 10-K report :

Our most recent innovation is our high-energy nickel manganese cobalt (“NMC”) 53.5 ampere-hour battery cell (the “53.5Ah”), whose performance characteristics make it an ideal solution for commercial vehicle and ESS applications.. [...] We expect the 53.5Ah cell to be our dominant revenue driver for this next phase of our growth.

In addition to producing battery cells, Microvast can also assemble battery modules and packs. The battery packs can be customized according to needs: in the US, they are primarily required for battery storage operations, while in Europe, demand mainly comes from heavy vehicle manufacturers.

A Look at the Financials

Below are the main figures related to Microvast's income statement over the past few years (data in $ million, source: Seeking Alpha):

| Dec 2018 |

| Dec 2019 |

| Dec 2020 |

| Dec 2021 |

| Dec 2022 |

| TTM |

| Revenues |

| 174.2 |

| 76.4 |

| 107.5 |

| 152 |

| 204.5 |

| 225.3 |

| YoY Growth |

| -56.1% |

| 40.7% |

| 41.4% |

| 34.5% |

| 10.2% |

| Gross Profit |

| 20.8 |

| -0.2 |

| 17.1 |

| -42.7 |

| 9.1 |

| 20.5 |

| Gross Profit Margin |

| 11.9% |

| -0.3% |

| 15.9% |

| -28.1% |

| 4.4% |

| 9.1% |

| Operating Income |

| -58 |

| -54.2 |

| -32.1 |

| -200.2 |

| -161.6 |

| -131.6 |

| Net Income |

| -54.9 |

| -57.5 |

| -33.6 |

| -206.5 |

| -158.2 |

| -125.9 |

As one can see, revenues and margins have been on a roller coaster for the past 5 years. Depending on market conditions, a battery was more or less in demand, and a facility could benefit from tax incentives or not. 2023 has been another year of very moderate growth so far, but a new boom is expected next year: as of June 30, 2023, Microvast's backlog was 600+% higher than that of June 30, 2022, standing at 675 million dollars.

The volatility in revenue and margins comes precisely from the product mix. At this particular historical moment, the 53.5-amp battery has enjoyed great commercial success, and Microvast manages to sell it with good margins. Almost all of the backlog depends on this single product which, like every other battery in the market, will face increasing competition in the coming months.

Let's now turn to the data on financial solidity:

| Dec 2019 |

| Dec 2020 |

| Dec 2021 |

| Dec 2022 |

| Last Report |

| Cash & Equivalents |

| 29.5 |

| 22.2 |

| 482 |

| 257.4 |

| 168.3 |

| Total debt |

| 150.2 |

| 151 |

| 147.4 |

| 175 |

| 164.1 |

| CapEx ((TTM)) |

| -20.3 |

| -18.6 |

| -87.9 |

| -150.9 |

| -176.6 |

As can be seen, the company has essentially used the proceeds from its stock market listing to finance its capital expenditure. Most of the funds were used to expand the production facility in Colorado, so as to assemble the ESS units there and take advantage of the tax incentives of section 45x of the IRA, and to build the new plant in Tennessee.

Valuation

Here is a table showing the most relevant valuation multiples for Microvast, compared to other battery producers. Most of the competitors are in one of two situations: they are either small/micro-cap companies in a pre-revenue stage, or big consolidated manufacturers. Since it would be of little value to compare the multiples of pre-revenue companies, for my comparison I opted for the big manufacturers.

| Microvast |

| LG Energy Solution |

| SK Innovation |

| Samsung SDI |

| Prices/Sales |

| 2.28 |

| 3.84 |

| 0.17 |

| 1.56 |

| Price/Book |

| 0.89 |

| 6.46 |

| 0.65 |

| 1.99 |

| Debt/Asset |

| 0.16 |

| 0.22 |

| 0.41 |

| 0.18 |

| Gross margin % |

| 15.29 |

| 14.48 |

| 3.31 |

| 17.26 |

| EBITDA margin % |

| -28.81% |

| 10.29 |

| 1.24 |

| 15.06 |

I could not use the P/E ratio, since Microvast is still unprofitable. Judging by the data, I would much rather on Samsung SDI than Microvast. Also, we should not forget that gross margins for Microvast have been very volatile in the past while Samsung have kept theirs very steady in a 17-21% range.

Microvast's Technological Challenge

The EV battery market shares many similarities with the traditional battery and semiconductor markets. In the initial market expansion phase, there is a huge demand for companies focusing on R&D and OEM manufacturers. Gradually, technological and production leaders consolidate, leading to a handful of major companies dominating the market: TSMC, Intel, AMD, Duracell, and so on.

We are still in the first phase of the market's expansion, where many downstream companies in the supply chain need to secure any available quality battery to keep up with vehicle production rates. Having slightly below-average technology and slightly above-average prices is still enough to generate large industrial orders. This is true for electric cars and even more so for heavy vehicles, where all major manufacturers have simultaneously embarked on their race to electrification in the past two years.

Given that Microvast's annual revenue is less than half a billion dollars, the chances of it becoming a volume production leader are extremely slim. At this point, comparing its production volumes to giants like CATL, LG, SK Innovation, BYD, or Tesla is irrelevant. The other competitive front, technology, is also where I have serious reservations.

{kind=link}

Is the 53.5 Amp/h battery really that innovative?

As mentioned, the 53.5 ampere/hour battery is Microvast's flagship product. It's quite telling that they use this uncommon metric to identify their product, given that the EV industry has been shifting more towards Wh and Wh/kg. Here's a brief refresher of high school physics lessons:

- Amperes measure how much current flows in a battery in a second;

- Ampere/hours measure how much electric current the battery can provide in an hour. Without knowing the battery's operating voltage, it's not a very indicative measure because it doesn't allow us to know its actual power;

- Watts measure the amount of power provided by the battery. This is a valuable indicator of an EV battery's performance, much like horsepower is for an internal combustion engine;

- Watt/h expresses the total amount of power the battery can supply in an hour.

A 53.5 ampere/hour battery isn't particularly special. For three years now, Samsung SDI has been selling batteries for heavy vehicles with capacities of 60 ampere/hour and even 94 ampere/hour .

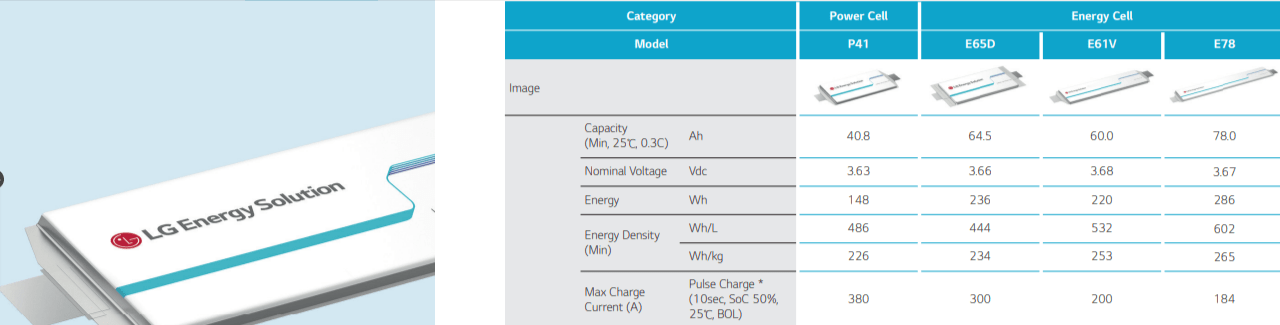

In practical terms, Microvast's technology is not particularly innovative. Its batteries have an energy density of 235 Wh/kilo , while CATL can produce batteries with 330 Wh/kilo , and LG has been offering 60-ampere batteries with an energy density of 253 Wh/kilo for years. Energy density tells us how much power we gain for every extra kilo of batteries we install in our vehicle; it's not particularly relevant for ESS systems, as weight is a less significant variable.

Moreover, Microvast is less efficient than its competitors in battery pack assembly. Once installed in 398 kg battery packs, the system's energy density significantly drops to 180 Wh/kg . This indicates that the battery connection and control system is heavier compared to more efficient competitors like BYD and SK Innovation, in addition to the ones already mentioned.

LG Energy Solution | Product Portfolio

{kind=link}

Clearly, being a technological leader is not essential when there aren't enough batteries on the market, but the situation is changing rapidly:

- Scania and Northvolt are working on an 18,000 square meter facility to produce electric trucks ( source ).

- Daimler and Cummins are developing a battery plant for electric trucks in Indiana, with an investment of $2-3 billion ( source ).

- Lion Electric has just inaugurated a 175,000 square feet facility dedicated to battery production for buses ( source ).

These are just three examples, driven by the fact that it's not easy to find sources related to the activities of Chinese manufacturers. It's easy to imagine that hard work is also being done on the other side of the Pacific to produce batteries for heavy-duty vehicles, further increasing the competition for Microvast.

The Case of Battery Storage

Everything we've said so far can be precisely replicated for battery storage, an extremely competitive market where Tesla is widely establishing itself as a leader in innovation and production. Again, Microvast cannot compete with the production levels of Elon Musk's company; moreover, it does not have disruptive technology capable of conquering the market with its performance.

This is all without considering that we will soon witness the large-scale commercialization of solid-state batteries, a sector in which Microvast has not even announced any ongoing R&D projects. Toyota is ready to launch the first car with SSB in 2025, QuantumScape and Solid Power are ready for large-scale production, and by 2028, SK Innovation will be ready to transition almost entirely to this type of battery. Major announcements of this kind have also come from LG Energy Solution , which should anticipate SK in 2026.

Exactly in line with when Microvast's management predicts the company will start making profits, it's also expected that its technology will become extremely uncompetitive.

Conclusions

Microvast's technology is not particularly advanced, and its production capacity is significantly lower than that of larger competitors, who invest billions for each battery production plant. Consider that the top 10 EV battery manufacturers, at the end of 2022, held a 92% market share . The company has managed to carve out a niche in a less crowded market, taking advantage of the electric truck boom at a time when battery manufacturers are not ready to keep up with demand or offer specialized products.

Over the months, however, this market gap is increasingly being filled by competitors able to benefit from large economies of scale and hundreds of millions of dollars spent annually on research and development. All this while the advent of SSBs is approaching, and Microvast has no ready answer. Given all this, I see no concrete reason to buy the stock today.

Risks and Factors to Consider

My analysis might prove wrong if:

- Microvast effectively introduces a new product line with extremely innovative technology, capable of offering a technological hedge against competitors.

- The company manages to be acquired by one of its major international clients at an appealing price.

- The management finds a new interesting market niche as the heavy-duty vehicle gap closes. eVTOLs or the nautical sector might offer insights.

However, these are all hypotheses I wouldn't be ready to invest in. I believe the company's fundamental problems remain, and there are no significant reasons to keep Microvast shares in the portfolio.

For further details see:

Microvast: The Management Is Selling, And So Should You