MVST - Microvast: Vast Upside With Vast Risks

2023-08-06 00:24:01 ET

Summary

- Microvast is a relatively young company still burning cash, but I see many positive trends in the financial performance.

- Despite negative free cash flow, the balance sheet is solid enough to fuel further growth and business expansion.

- Despite the significant risks inherent to investing in Microvast, I believe that the massive upside potential outweighs all risks and uncertainties.

Investment thesis

Microvast ( MVST ) trades almost ten times cheaper than the all-time high. The stock suffered a massive selloff, starting in February 2021 and bottoming in December 2022. MVST demonstrated an impressive year-to-date rally this year, and my valuation analysis suggests that the stock is still massively undervalued. But there is no reward without risk, and the risks of investing in the stock are also massive. But I think that the upside potential outweighs the risks. I like MVST's improving financial performance and strong revenue growth momentum amid the uncertain environment. The management has a long-term view and allocates substantial resources to innovation and production expansion. MVST is a long-term play with a multiple years horizon and potential deep drawdowns, but I am adding the stock to my long-term portfolio.

Company information

Microvast Holdings is a battery technology company involved in designing, developing, and manufacturing battery components and systems primarily for electric commercial vehicles and utility-scale energy storage systems.

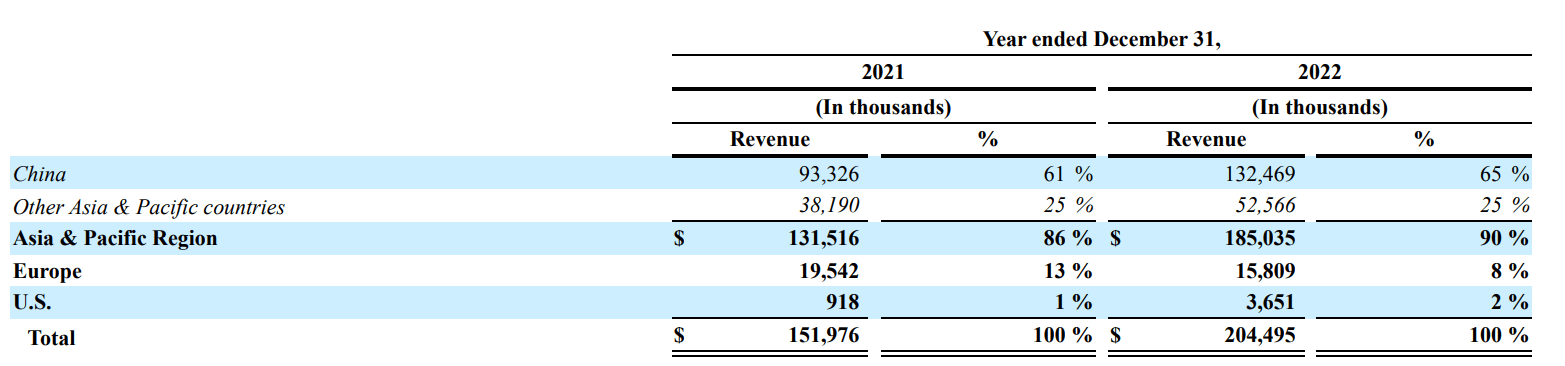

The company's fiscal year ends on December 31. According to the latest 10-K report , the company generated about two-thirds of its sales in China during FY 2022.

{kind=link}

Financials

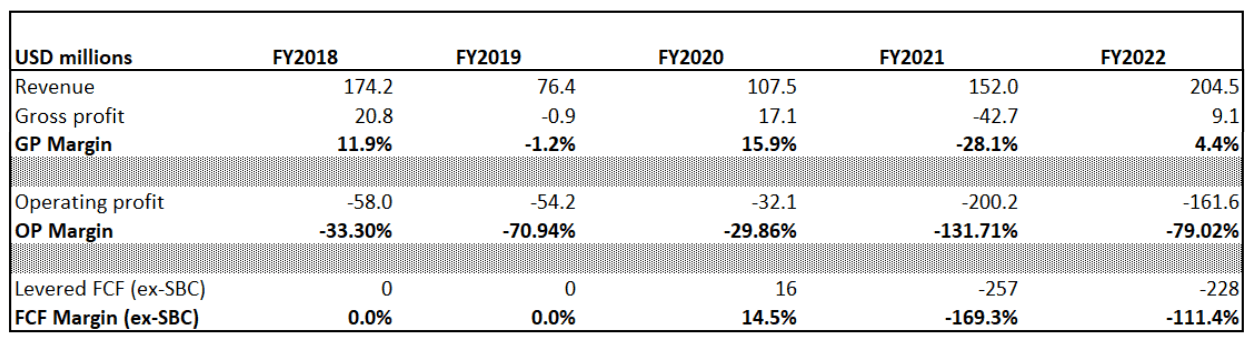

Microvast went public in 2021 , so we have a limited track record of the company's financial performance. The operating and free cash flow [FCF] margins are still negative, and the gross margin is still razor-thin. Since FY 2019, the top line demonstrated impressive growth and more than doubled.

{kind=link}

The company is still in its early stages of development and incurs significant R&D expenses to expand and improve its offerings to customers. Microvast also spends heavily on selling and marketing expenses to fuel sales growth. The company looks very far from reaching operating profits. It is also crucial that the business scale is relatively small, and there is a potential to expand profitability with the economies of scale effect, but it is a long-term perspective.

Despite having a wide negative FCF margin, the company's balance sheet looks solid, thanks to the cash raised during the IPO. MVST is in a firm net cash position with sound liquidity ratios.

Seeking Alpha

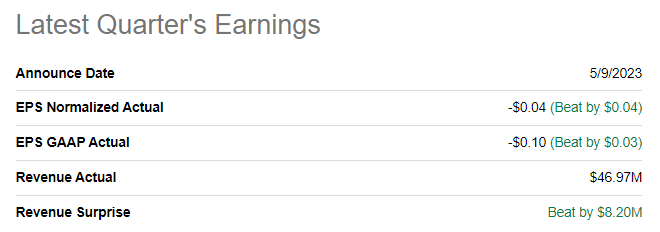

The company released its latest quarterly earnings on May 9, beating consensus estimates on the top and bottom lines. It was the highest-ever Q1 revenue MVST with a 28% YoY growth. The strong revenue momentum was primarily thanks to the strength in Europe.

{kind=link}

The gross margin also demonstrated solid YoY improvement expanding to 10.3% from zero. The improvement was mainly due to production efficiencies and a more favorable product mix. I think that Q1 financials were strong, which is impressive, especially amid the current uncertain macro environment. A very bullish sign is that the management raised its full-year guidance and now expects annual revenue growth within the 70% to 80% range compared to the previous estimate for revenue growth between 65% to 75%. During the latest earnings call , the management reiterated its long-term expansion plans. It emphasized that solid momentum in European U.S. sales is expected to remain in the nearest quarters. The upcoming quarter's earnings release is planned on August 7. Quarterly revenue is expected at almost $66 million, which would be MVST's record.

Valuation

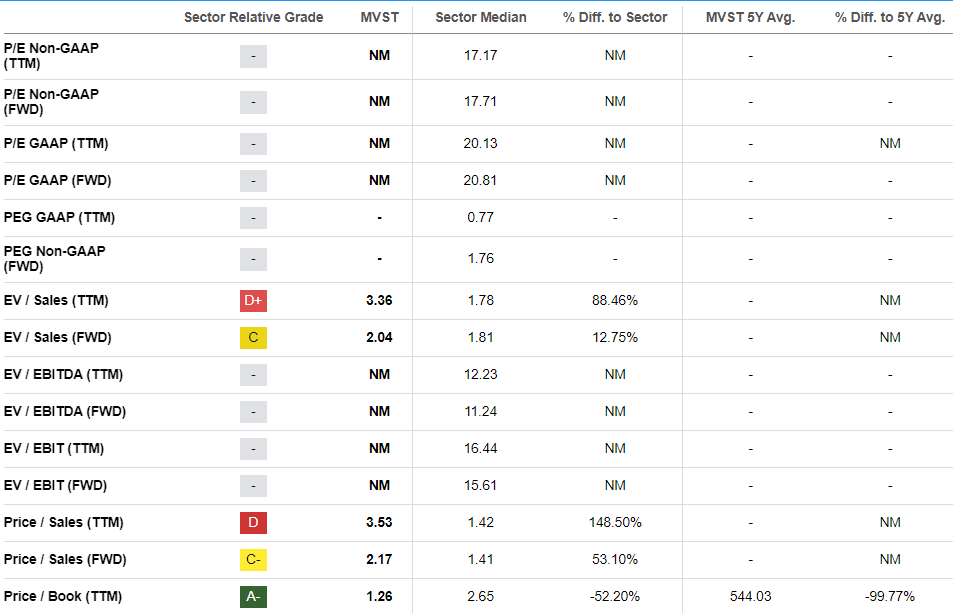

This year, the stock outperformed the broad market with a 64% year-to-date rally. Seeking Alpha Quant assigns the stock a low "D" grade, though few multiples are applicable since most profitability metrics are still negative. The company is in the very early stages of its life cycle. Therefore, multiples analysis might not be the best fit to make conclusions about the valuation.

{kind=link}

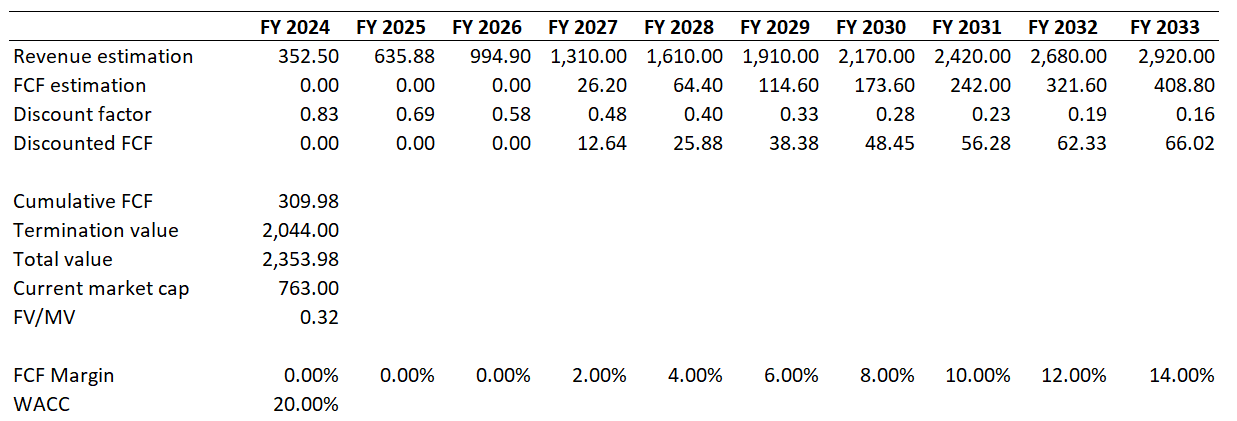

Consensus earnings estimates forecast a very rapid revenue growth over the next decade. The expected CAGR is above 26%, and it is a very aggressive assumption. But I will use it for my base case scenario and then simulate the one with more moderate revenue growth. I expect the FCF to turn positive after the company surpasses one billion dollars in sales, which is expected in FY 2027. For the years beyond, I expect the FCF margin to expand by two percentage points yearly. Since the level of uncertainty is massive, I incorporate a twenty percent WACC.

{kind=link}

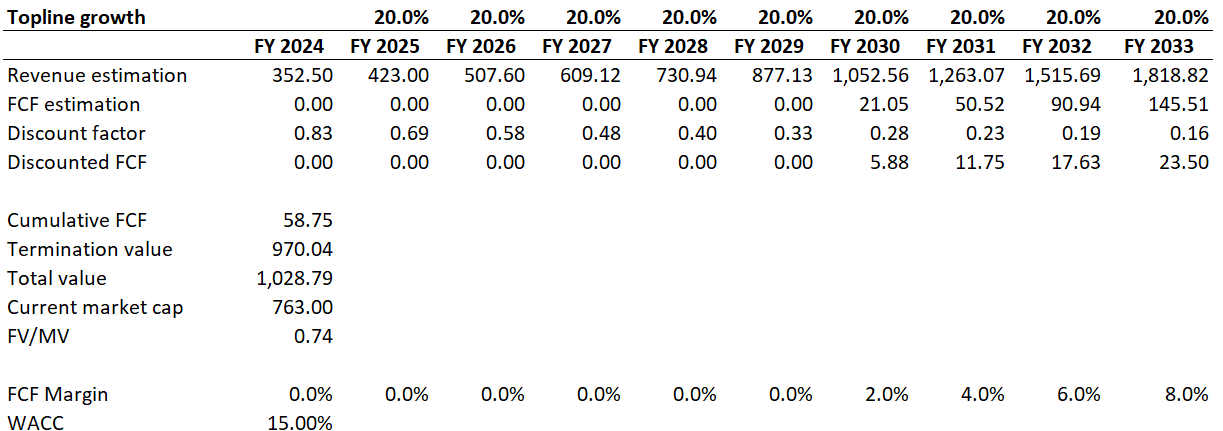

As you see, the stock is about three times undervalued. But expectations are very aggressive, and I would like to simulate a more moderate scenario. For the second scenario, I take a 20% revenue CAGR, and under this assumption, revenue is expected to surpass one billion only in FY 2030. The FCF margin assumptions I use for the second scenario will also change accordingly. Since this scenario is more conservative, I use a lower WACC of 15%.

{kind=link}

The stock still looks very attractively valued under more conservative revenue growth and FCF margin assumptions. But, potential investors should not forget that it is a long-term play because the company is very far from generating positive FCFs.

Risks to consider

MVST is a growth company in the early stages of its development. The company is still losing money and is not expected to break even in the next few years. That said, investing in the stock is very risky, and a high level of volatility is inherent to stocks like this. MVST currently trades about ten times lower than its all-time highs, and investors should be ready to bear a massive risk if they want to bet on the company.

The company generates about 98% of sales outside the U.S., meaning vast foreign exchange risks. Earnings can be significantly adversely affected in case of unfavorable fluctuations in the forex market. It is also crucial to point out that the risk related to China is also massive. The company's largest manufacturing facility is located in China, and sales in this country comprise about two-thirds of the total. Potential escalation in geopolitical tensions between the U.S. and China will likely disrupt the company's operations and earnings.

In FY 2022, MVST's top five customers contributed approximately 36% of the total sales. That said, the concentration risk is high for the company. The overreliance on large customers makes the company's earnings vulnerable to customers' financial performance. A high concentration of sales also means less bargaining power in negotiations, which is also not good for MVST.

Bottom line

To sum up, MVST stock is a "Buy" for long-term investors ready to tolerate short-term volatility and even potential deep drawdowns. The very high risks and uncertainties explain a massive discount on the stock price. But I see favorable secular trends for the company related to clean energy, and I consider the management efficient in execution based on the financial performance and capital allocation.

For further details see:

Microvast: Vast Upside With Vast Risks