MSBI - Midland States Bancorp: Attractively Valued With A Positive Topline Outlook

Summary

- The management’s strategies and some economic factors will reduce the pace of loan growth this year.

- The margin will likely grow once the up-rate cycle is over.

- Provisioning charges for expected loan losses will likely remain above average this year as the reserves appear insufficient for upcoming economic headwinds.

- The December 2023 target price suggests a high upside from the current market price. Further, MSBI is offering a high dividend yield for a bank holding company.

Although the loan growth of Midland States Bancorp, Inc. (MSBI) will most probably decelerate this year, it will likely remain positive, which will boost earnings. Further, earnings will receive support from margin expansion towards the end of this year. On the other hand, provisioning for loan losses will likely remain above average, which will hurt the bottom line. Overall, I'm expecting Midland States Bancorp to report earnings of $3.67 per share for 2023. Compared to my last report on the company, I've slightly reduced my earnings estimate mostly because I've decreased my loan growth estimate for the year. The year-end target price suggests a high upside from the current market price. Therefore, I'm maintaining a buy rating on Midland States Bancorp.

Significant Decline in Loan Growth Likely

Midland State Bancorp's loan growth slowed down to 1.7% in the fourth quarter from 7.0% in the third quarter of 2022. A further slowdown is likely due to the management's policy of preferring pricing over volume. As mentioned in the earnings presentation , the management wants to focus on profitability while maintaining a conservative approach to new loan production. Further, the exit from the GreenSky program will hurt the origination of consumer loans. GreenSky is a third-party servicer that Midland partnered with for national and regional home improvement loans.

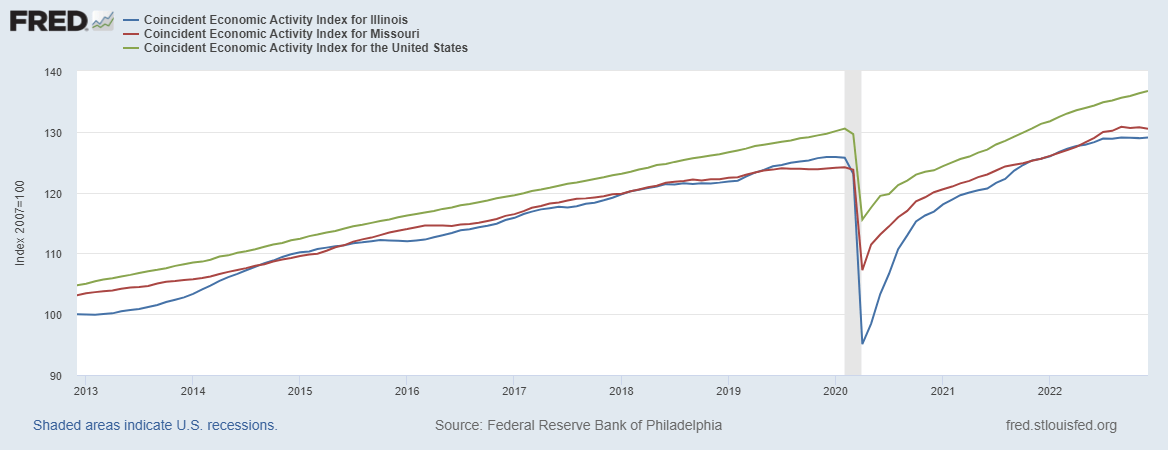

A majority of Midland's loan portfolio comprises commercial and commercial real estate loans. Within these sub-portfolios, the sectors of skilled nursing, retail, and rental and leasing are heavyweights. Further, the company mostly operates in the states of Illinois and Missouri. Considering these characteristics, I believe the unemployment rates and economic activity indices of Illinois and Missouri are appropriate indicators of loan growth in the near term. As shown below, the economic activity indices for both states are currently showing flatter trends than the national average.

{kind=link}

The unemployment rate is giving a mixed picture. Illinois has one of the worst unemployment rates in the country, while Missouri has one of the best, according to official sources . Nevertheless, the labor markets of both states are at remarkable levels compared to their respective histories.

Considering these factors, I'm expecting the loan portfolio to grow by 6% in 2023. In my last report on the company, I projected a loan growth of 8% for the year. I've reduced my loan growth estimate as my outlook is bleaker than before.

Meanwhile, I'm expecting deposits to grow in line with loans. The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| Net interest income |

| 180 |

| 190 |

| 199 |

| 208 |

| 246 |

| 268 |

| Provision for loan losses |

| 9 |

| 17 |

| 43 |

| 3 |

| 20 |

| 26 |

| Non-interest income |

| 72 |

| 75 |

| 61 |

| 70 |

| 80 |

| 68 |

| Non-interest expense |

| 192 |

| 176 |

| 185 |

| 175 |

| 176 |

| 185 |

| Net income - Common Sh. |

| 39 |

| 55 |

| 22 |

| 80 |

| 95 |

| 83 |

| EPS - Diluted ($) |

| 1.66 |

| 2.26 |

| 0.96 |

| 3.57 |

| 4.23 |

| 3.67 |

| Source: SEC Filings, Earnings Releases, Author's Estimates(In USD million unless otherwise specified) |

In my last report on Midland States Bancorp, I estimated earnings of $3.85 per share for 2023. I've reduced my earnings estimate mostly because I've slashed my loan growth estimate for the year.

My estimates are based on certain macroeconomic assumptions that may not come to fruition. Therefore, actual earnings can differ materially from my estimates.

MSBI is Currently Trading at a Large Discount to its Target Price

Midland States Bancorp is offering a dividend yield of 4.4% at the current quarterly dividend rate of $0.30 per share. The earnings and dividend estimates suggest a payout ratio of 33% for 2023, which is below the five-year average of 42%. Therefore, the dividend payout appears secure. Midland usually increases its dividend only once a year, so another dividend hike is unlikely in the year ahead.

I'm using the historical price-to-tangible book ("P/TB") and price-to-earnings ("P/E") multiples to value Midland States Bancorp. The stock has traded at an average P/TB ratio of 1.14 in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| TBVPS - Dec 2023 ($) |

| 26.9 |

| 26.9 |

| 26.9 |

| 26.9 |

| 26.9 |

| Target Price ($) |

| 28.0 |

| 29.3 |

| 30.7 |

| 32.0 |

| 33.4 |

| Market Price ($) |

| 26.2 |

| 26.2 |

| 26.2 |

| 26.2 |

| 26.2 |

| Upside/(Downside) |

| 6.7% |

| 11.9% |

| 17.0% |

| 22.1% |

| 27.3% |

| Source: Author's Estimates |

Excluding the outlier in 2020, the stock has traded at an average P/E ratio of around 8.3x in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| T. Average |

| EPS 2023 ($) |

| 3.67 |

| 3.67 |

| 3.67 |

| 3.67 |

| 3.67 |

| Target Price ($) |

| 23.1 |

| 26.8 |

| 30.5 |

| 34.1 |

| 37.8 |

| Market Price ($) |

| 26.2 |

| 26.2 |

| 26.2 |

| 26.2 |

| 26.2 |

| Upside/(Downside) |

| (11.8)% |

| 2.1% |

| 16.1% |

| 30.1% |

| 44.1% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $30.6 , which implies a 16.6% upside from the current market price. Adding the forward dividend yield gives a total expected return of 21.1%. Hence, I'm maintaining a buy rating on Midland States Bancorp.

For further details see:

Midland States Bancorp: Attractively Valued With A Positive Topline Outlook