MMLP - Midstream Weekly Recap: Another Big Week With Gains Across The Board

Summary

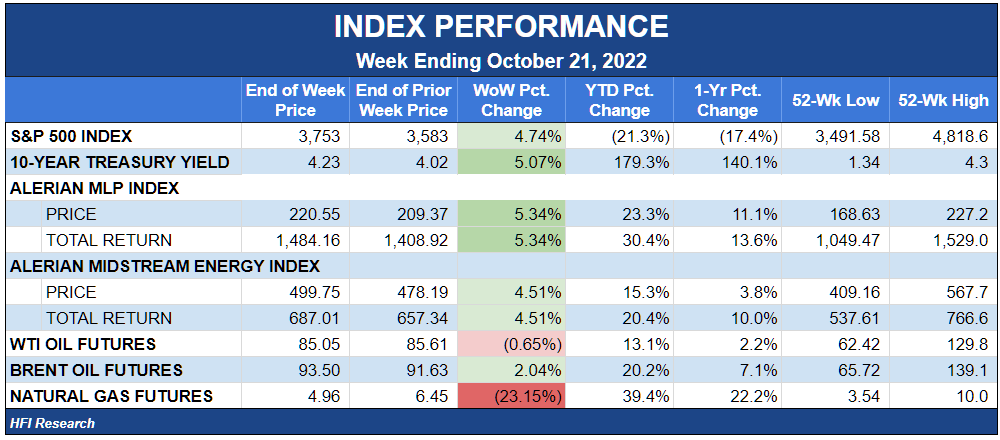

- Midstream equities outperformed the S&P 500 despite rising interest rates and falling WTI and natural gas prices.

- Kinder Morgan kicked off earnings season with a miss.

- Dividend increases continue to roll in.

Midstream Sector Performance

Midstream finished the week up 5.3%, beating the S&P 500 by 0.6%. Once again, the sector bucked the trend of higher interest rates, as the ten-year Treasury rose 5.1%.

{kind=link}

We continue to believe the sector's cheap equity valuations have supported its equity prices. This is likely to continue unless midstream equities continue to rally and/or interest rates move higher from here. At some point, even the most discounted stocks will feel downward pressure from rising interest rates, regardless of their income yield. Alternatively, a sustained drop in interest rates from current levels is likely to provide a bullish tailwind.

Midstream equities also shook off declining WTI and natural gas prices along with the XOP and XLE. We believe investors are getting more comfortable with the oil and gas sector's capital discipline and bullish longer-term prospects amid a structural supply deficit.

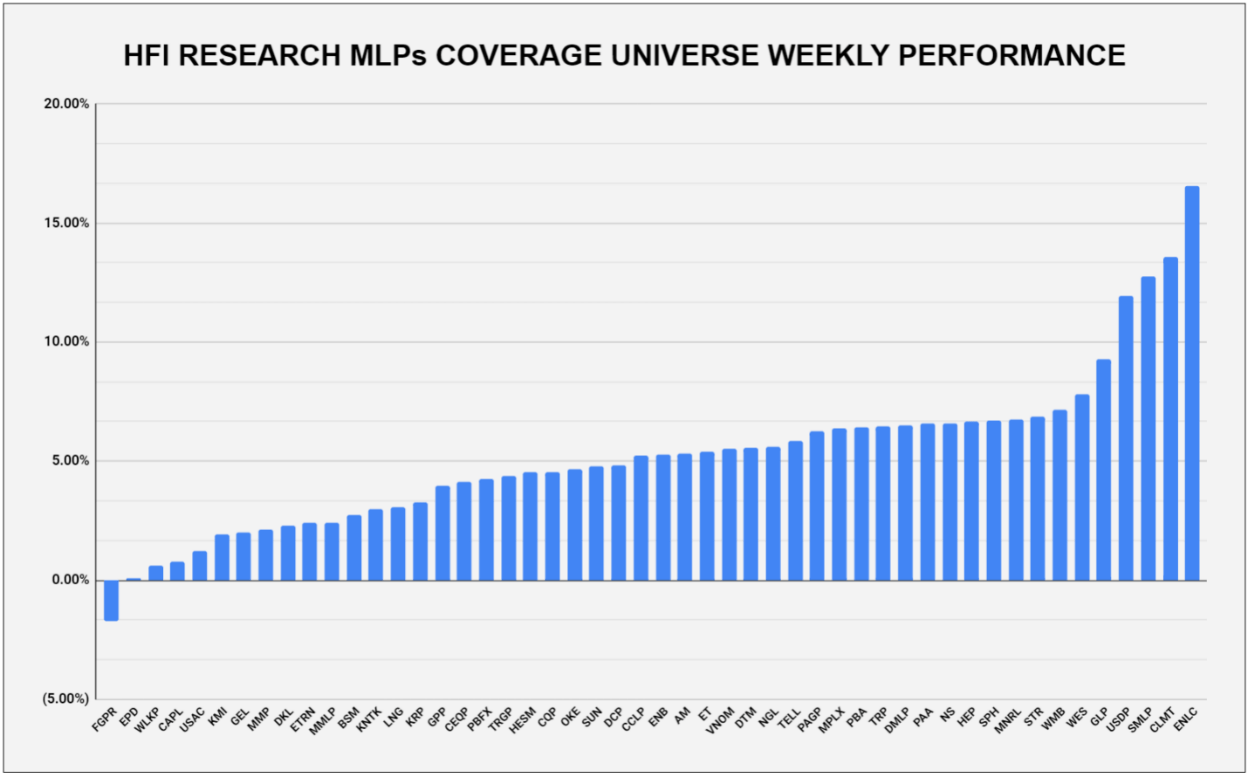

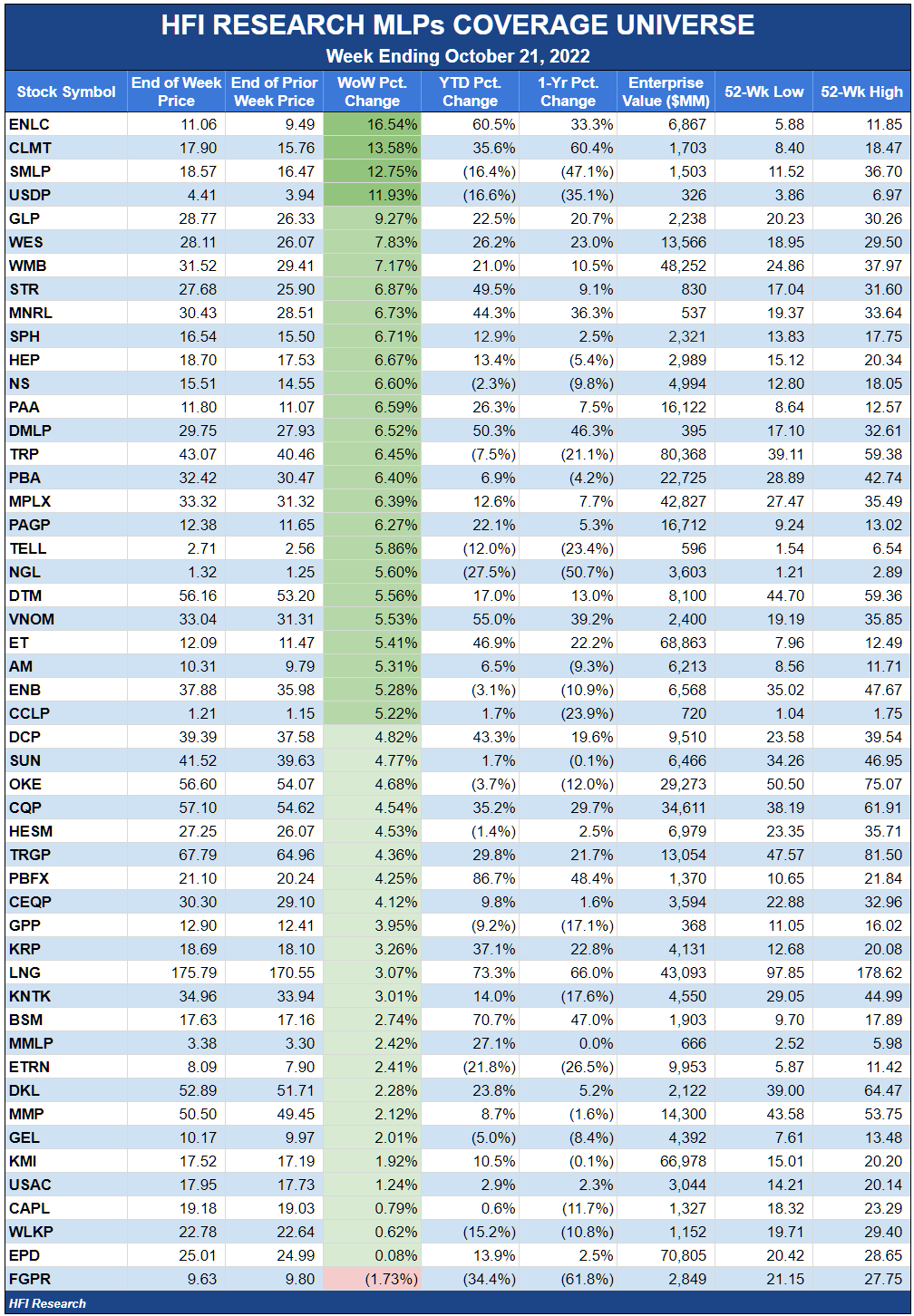

Our coverage universe was green across the board during the week. Only one equity was negative on the week; namely, Ferrellgas Partners (FGPR), for which we don't provide a value range or price target due to its risk of permanent loss to unitholders.

{kind=link}

Kinder Morgan Kicks Off Earnings Season

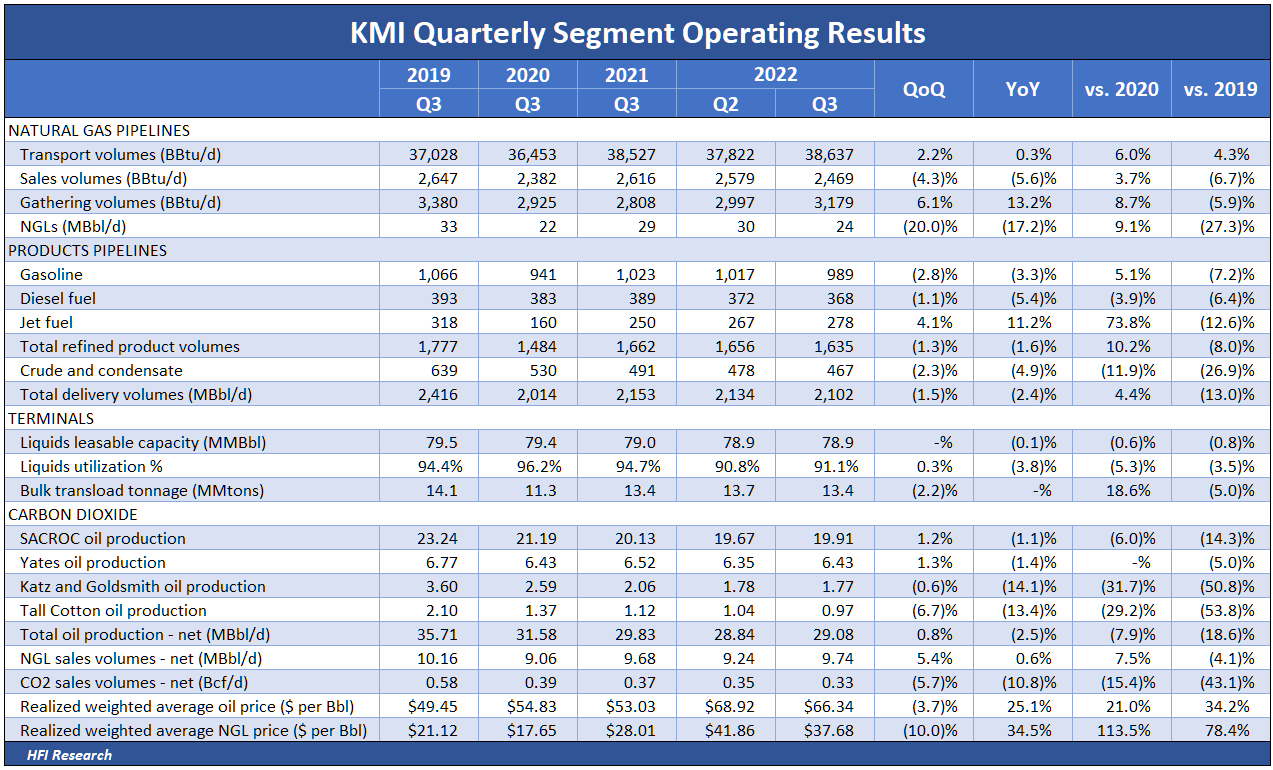

Kinder Morgan ( KMI ) kicked off earnings season with a whimper. The market had expected KMI's third-quarter Adjusted EBITDA of $1.83 billion, while the company reported $1.77 billion, missing expectations by 3.3%.

KMI's throughput volumes were tepid in the third quarter. The main bright spot was KMI's natural gas gathering volumes, which were up 13% year-over-year due to increasing production activity on its Haynesville acreage. Natural gas transport volumes were only up 0.3% from year-ago levels but would have been higher if Freeport LNG had been operational. Natural gas deliveries to power plants grew 11%, preventing a year-over-year decline in volumes.

In KMI's refined products pipeline segment, volumes fell due to slowing domestic demand, though jet fuel demand staged an impressive 11% year-over-year increase. In KMI's crude oil pipelines, declining Eagle Ford volumes caused volumes to fall 5% from the previous year.

KMI's third-quarter volume performance can be seen in the following chart. Overall, the performance doesn't inspire much long-term confidence. Natural gas transportation and gathering are likely to continue to weigh most heavily in future results, so KMI's stock is likely to be sensitive to factors that affect those variables.

{kind=link}

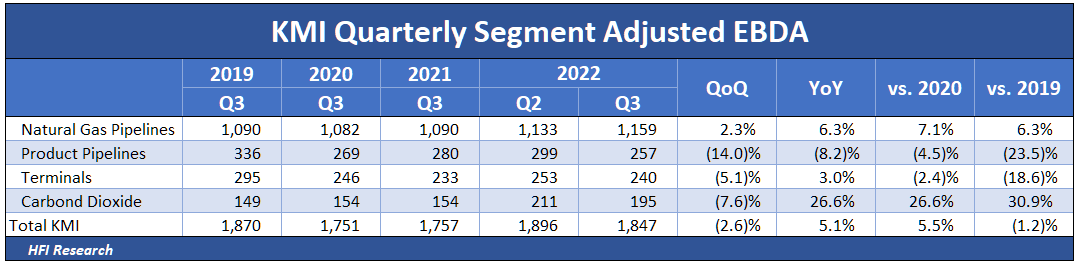

Financial performance during the third quarter was also disappointing, though management continues to expect 2022 Adjusted EBITDA to track 4% to 5% above 2021 figures. This is below management's previous guidance of 5%. During the quarter, KMI repurchased $90 million of shares. Year-to-date, it has repurchased 21.7 million shares for $368 million at an average price of $16.94. Management intends to continue opportunistic repurchases going forward.

{kind=link}

Management signaled it would return to pursuing growth projects once KMI's leverage has been brought down to its target. Large and profitable growth projects will be necessary to bolster the company's financial performance. We expect projects in renewable natural gas to be management's highest priority.

We view KMI's operations as sort of a melting ice cube absent new hydrocarbon-based growth investments. It's too early to gauge returns from its non-hydrocarbon initiatives. KMI's massive system has little room to grow outside of gathering and processing and Permian egress, so much of its financial performance will be driven by rate increases on its natural gas and liquids transportation pipelines, which came in below the rate of inflation in the third quarter. We rate KMI as a Hold and believe there are more attractive investment alternatives among midstream equities.

MLPs Stand Out

MLPs were strong during the week. The top-performing MLP was our holding, Calumet Specialty Products Partners ( CLMT ), which rose 13.6% on no news. Summit Midstream Partners ( SMLP ) was the second best performer, up 12.8% on the week after announcing an acquisition that would de-lever its balance sheet, as we profiled here . Liquids-weighted names were also among the big gainers. Our holding, Western Midstream Partners ( WES ), as well as NuStar Energy ( NS ) and Global Partners ( GLP ), all traded more than 6.5% higher.

Among the worst performers was our holding Enterprise Products Partners ( EPD ), which fell after receiving a downgrade from Tudor Pickering. Tudor downgraded EPD from Buy to Hold with a $29 price target. Its caution stems from weakening global petrochemical fundamentals. We voiced similar concerns over the past few weeks, though we remain bullish due to our longer-term outlook, attractive returns from EPD's non-petrochemical segments, and the income safety that exists in EPD units.

Among corporations, our holding, EnLink Midstream ( ENLC ), was the biggest gainer on no news. Last week, ENLC announced its participation in a carbon capture project with Exxon Mobil ( XOM ) and CF Industries ( CF ), though we doubt the news was behind this week's rally.

Williams ( WMB ) was the next-best performing corporation, up 7.2%. The gain is surprising in light of the 23.2% decline in natural gas prices during the week. WMB signed a deal to extend its reach into clean hydrogen, as discussed further below, though we don't believe the announcement had an impact on WMB's stock. Sitio Royalties ( STR ) was the third-best performer, up 6.9%. STR stock is up 15.3% since we recommended it on October 4.

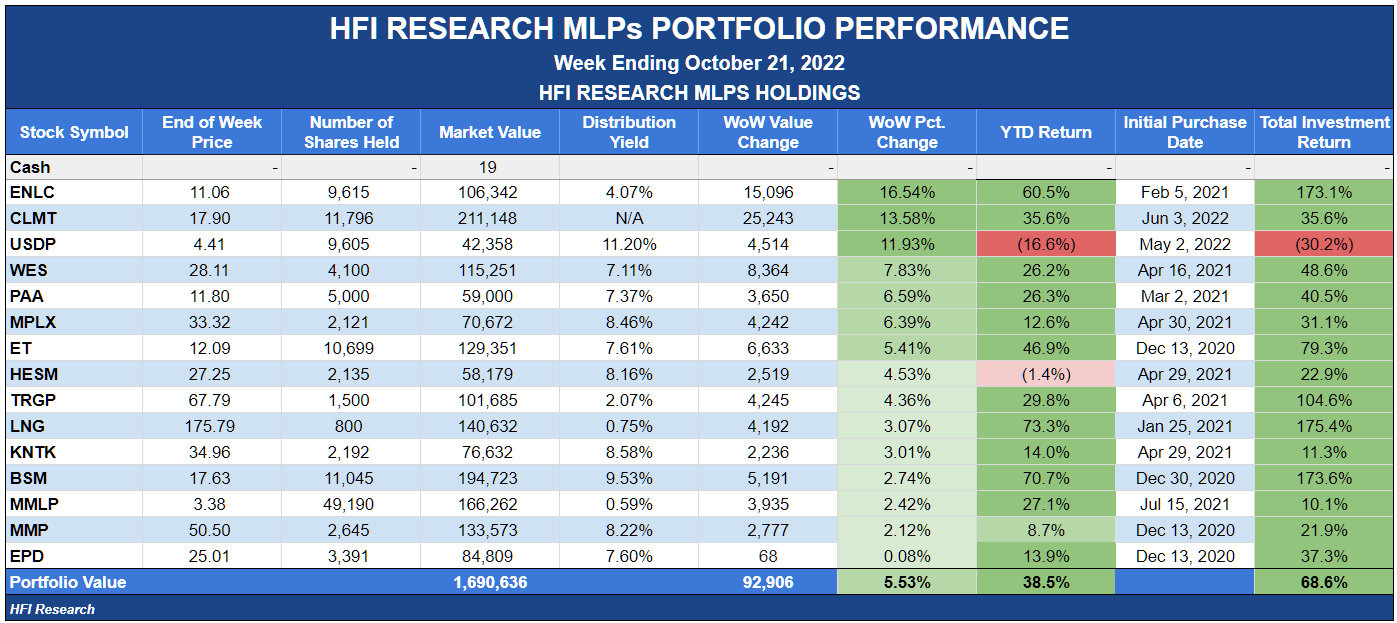

Weekly HFI Research MLPs Portfolio Recap

Our portfolio outperformed its benchmark, the Alerian MLP Index, by 0.2% during the week.

{kind=link}

There were some notable distribution increases among our holdings. Cheniere Energy ( LNG ) hiked its dividend from $0.33 to $0.395; Black Stone Minerals ( BSM ) increased its distribution from $0.42 to $0.45; and Magellan Midstream Partners ( MMP ) saw an increase from $1.0375 to $1.0475. Each of these companies is among the highest quality names in their respective midstream sub-sector. Their payout increases-and the additional increases we expect in future quarters-speak to the merits of favoring high-quality midstream equities over their lower-quality peers in a long-term, income-focused investment program.

Martin Midstream Partners ( MMLP ), our sole speculative holding, announced a joint venture with Samsung C&T America and Dongjin USA to form DSO Sinochem LLC, which will produce and distribute electronic-level sulfuric acid. MMLP will be the exclusive provider of feedstock to DSO Sinochem's new facility, while its transportation segment, Martin Transport, will provide land transportation services to end-users of the electronic-level sulfuric acid produced by the joint venture.

MMLP plans to invest $20 million for a 10% stake in the venture, funded by borrowings on its revolving credit facility. The company's funding method is probably behind its sulfur terminal sale announced on October 10, which was made to pay down the balance on its revolver.

The new DSO Sinochem venture is expected to enter commercial operations in the first quarter of 2024. MMLP expects its stake to generate $5 to $6 million of distributable cash flow annually, which equates to a 25% to 30% cash return on invested capital. Management reported that electronic-level sulfuric acid demand exceeds supply in the U.S. The high-grade sulfuric acid market has been growing on a global basis, and hopefully, MMLP's investment can earn good returns for many years in the future, irrespective of the ups and downs of oil and gas markets. The deal shows that MMLP management is comfortable in going on offense with its capital, not simply hunkering down in deleveraging mode. No doubt its banks signed off on the deal, which is another positive. Still, we hope this project or any other growth initiative doesn't impede management's efforts to deleverage and refinance its 2024 and 2025 debt maturities.

MMLP's units rose after the announcement through the end of the week, though we don't read anything into the price action, as in our view, it's been nonsensical for MMLP for several weeks. We'd only note that the units traded down on huge volume, then staged a partial recovery once volume normalized. All the moves occurred amid no significant fundamental news for the company outside of its recent asset sale and joint venture, both of which we view as positive.

News of the Week

Oct. 17. Summit Midstream ( SMLP ) announced it was acquiring the Outrigger and Sterling gathering and processing systems in the DJ Basin for $305 million in cash. For details on the deal, which we believe improves the outlook for SMLP units, see our profile here .

Oct. 17 & 18. TC Energy ( TRP ) announced a $29.3 million investment in a renewable natural gas production facility near the Jack Daniel Distillery in Lynchburg, TN. The facility, which will break down certain byproducts in the distilling process into methane, is being developed with 3 Rivers Energy. TRP also announced that it would partner with the Alberta Carbon Grid to evaluate one of the largest areas for safely storing carbon produced from industrial emissions in Alberta. Lastly, TRP was the subject of speculation by analysts this week that it could sell billions of dollars of assets to fund growth projects in Western Canada and Mexico. One analyst pointed to a Keystone Pipeline divestiture as being "ESG-accretive." We'd only consider such a divestiture to be attractive if it was accretive to shareholders, irrespective of its ESG status. We hope management would agree.

Oct. 18. Williams ( WMB ) announced progress on its clean hydrogen commercialization efforts after signing a memorandum of understanding with Daroga Power, a developer of distributed generation energy assets such as hydrogen fuel cells and solar power generation. WMB plans to leverage its nationwide assets to blend, store, and transport clean hydrogen to local and regional markets. The company didn't comment on the deal's expected profitability. We've seen lots of announcements around hydrogen but no results. We'll reserve judgment on these deals until we have a better handle on the returns they generate.

Capital Markets Activity

None.

{kind=link}

For further details see:

Midstream Weekly Recap: Another Big Week With Gains Across The Board