MLR - Miller Industries: Elevated Working Capital Needs Suggest More Share-Price Consolidation

2023-10-09 13:13:35 ET

Summary

- Miller Industries has experienced significant earnings growth over the past four quarters, with a 50% increase in top-line sales and an $11.2 million improvement in net profit.

- The company's debt position has increased, and its inventory levels are at the highest they have been in quite some time, which could pose risks in a volatile market.

- Miller's cash-flow generation has been impacted by working capital commitments, and its price-to-free cash flow ratio indicates that it is not cheap from a valuation perspective.

Intro

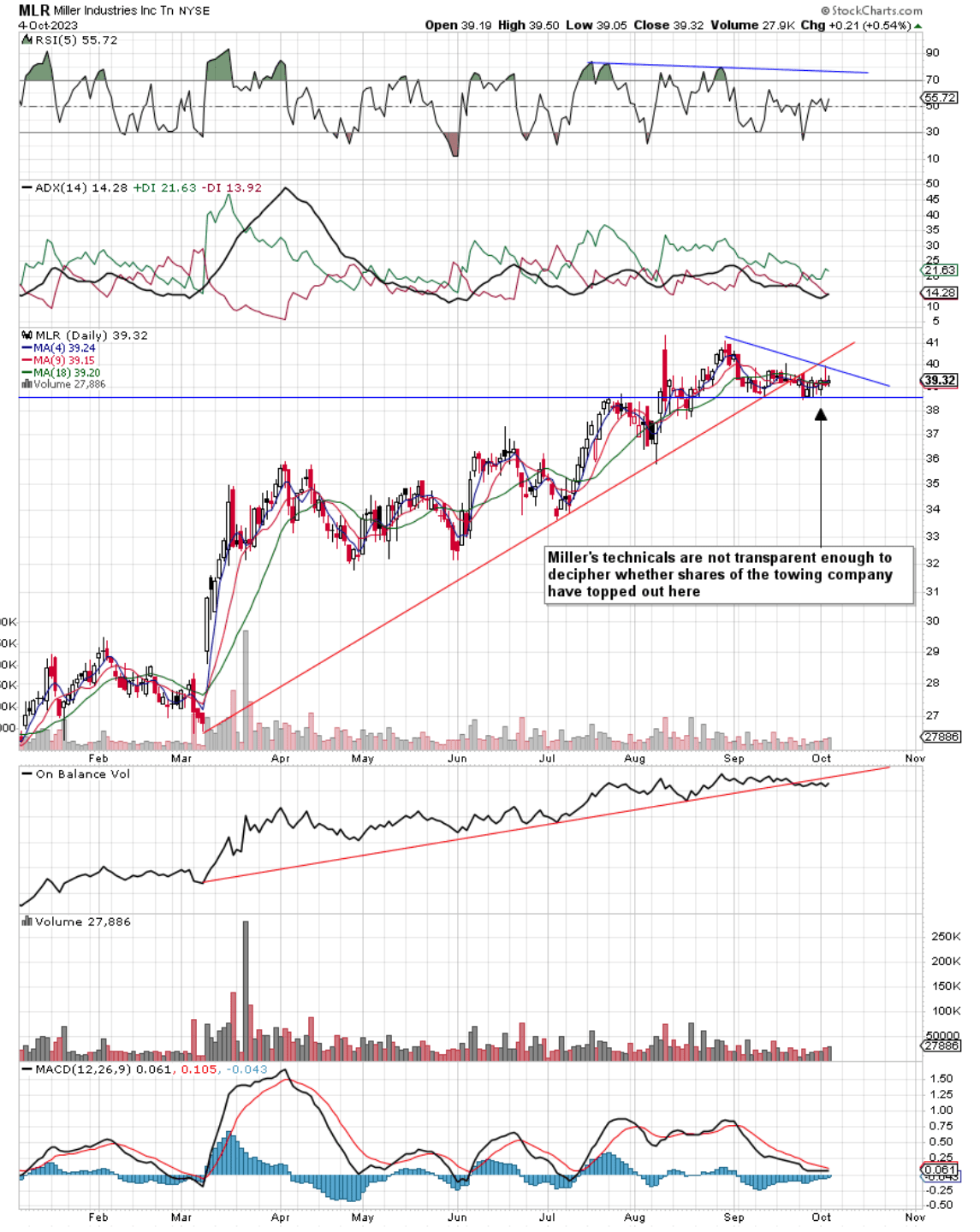

We wrote about Miller Industries, Inc. ( MLR ) back in September of last year when we pointed to a potential violent rally in the share price once shares bottomed in earnest. Although we recommended that investors wait until a firm bottom was confirmed, sequential quarterly trends (concerning margins) were finally beginning to improve. That technical bottom came approximately two weeks after our September'2022 commentary at roughly $21 a share. Since then shares almost doubled over eleven months arriving at almost $41 a share by August of this year. Over the past 6 weeks or so, however, we have seen shares consolidate so the key question now is whether Miller's gains over the past 12 months can continue in earnest.

In fact, from delving through Miller's trends both on the cash-flow statement as well as the balance sheet, we would be conservative with a Hold rating at this juncture. The reason is that liquidity conditions continue to remain tight (high inventory number) which is affecting strong cash-flow generation. Furthermore, from a free-cash-flow basis, shares are by no means cheap as we discover below.

Miller Industries Daily Technicals (Stockcharts.com)

{kind=link}

Q2 Earnings Strength

As always, what drives a company's share price is essentially its earnings growth and Miller has enjoyed this trend in spades particularly over the past four quarters. Given how low shares had stooped to late last year (under-average valuation), Miller enjoyed the perfect setup as supply chain conditions began to significantly ease.

Taking the above into account with the company's strong backlog, Miller reported more than $300 million in top-line sales in Q2 which was almost a 50% increase over the same period of 12 months prior. A much higher gross margin print of 13%+ resulted from production improvements and easily compensated for higher interest expense (due to debt used on the Southern Hydraulic Cylinder purchase) and higher SG&A costs (due to rising revenues & an altered executive compensation program). As a result, net profit for the quarter came in at $14.9 million which was a whopping $11.2 million improvement over the same quarter of 12 months prior.

However, given that the CEO only gave top-line guidance for fiscal 2023 ($1+ billion) and that earnings contain non-cash items, let's delve into Miller's recent cash-flow & balance sheet trends from a cash-flow perspective to see if the company has enough firepower to keep this earnings growth elevated.

Balance Sheet Trends

Concerning Miller's debt position, the company reported $60 million of long-term debt at the end of Q2. Although this number is quite small compared to the company's equity ($315+ million), it has risen by $20 million compared to Q2 last year and $15 million sequentially. Management stated on the recent earnings call that its objective is to bring down leverage over time as Miller just six quarters ago (Q4-2021) was a zero-debt company. However, wanting to do something as well as being able to do something are two entirely different things & here is where market conditions will come into play in a big way.

For example, apart from debt reduction, holding inventory is another top priority for the company. This is understandable as the backlog remains near record levels and demand remains strong. Miller's inventory came in at $167.5 million at the end of Q2 which is the highest it has been in quite some time. From a supply-chain point of view, the risk here is that if trading conditions were to 'lock up to an extent once more (in terms of product procurement), Miller would have no choice but to hold more inventory than it would normally.

Cash-Flow Trends & Valuation

Suffice it to say, more working capital commitments are having an impact on cash-flow generation as we can see from Miller's cash-flow statement. If we compare for example the company's trailing 12-month operating cash-flow number of $18.58 million, we see that it comes in almost 19% lower compared to the company's 5-year average ($22.84 million). A lower operating cash-flow print has ramifications for how much the company can invest going forward & how much free cash flow the company can generate.

To this point, Miller generated approximately $5.9 million of free cash flow over the past four quarters. Therefore, when we divide this number by Miller's present market cap ($449.12 million), we get a trailing price-to-free cash flow ratio of approximately 76. Suffice it to say, from a free cash-flow perspective, Miller Industries is not cheap as the above multiple informs us of how much each dollar of free cash flow costs Miller at present. Remember, free cash flow is the most important metric in investing bar none in that it tells us how aggressive management can be with its growth plans. Furthermore, given the market is always forward-looking, an above-average free cashflow multiple (which we have now in Miller) will not go unnoticed by investors, especially if liquidity remains tight in upcoming quarters.

When it boils down to it, inventory, long-term debt & capex all increased in Q2. If these trends continue, this will simply have to place more pressure on the financials and especially free cash-flow which is the driver of growth over time. Yes, the company's trailing GAAP earnings are cheaper (trailing GAAP multiple of 11.69 compared to a 5-year average multiple of 14.19) but we do not believe there is enough of a discount (due to the reasons discussed above) here to justify taking a long stance at this time. This is why believe a 'Hold' rating for the stock is the best course of action at this present moment in time.

Conclusion

Therefore to sum up, although Miller has had an outstanding 2023 to date where earnings growth has been to the core, higher accounts receivables as well as rising inventory levels may mean Miller Industries will not be able to turn over product (sell) at the same clip as it is doing at present. Let's see what Q3 brings. We look forward to continued coverage.

For further details see:

Miller Industries: Elevated Working Capital Needs Suggest More Share-Price Consolidation