MLR - Miller Industries: The Market Is Missing This Operating Leverage Story

2023-07-22 04:26:43 ET

Summary

- I believe the market is ignoring Miller Industries’ upcoming operating leverage story as they are just coming out of a big investment cycle.

- Miller Industries spent $82 million over the course of the past 5 years on modernizing and expanding their capacity. This will lead to sustainably high margins if demand holds up.

- Capex should also decline to around $20 million per year going forward, a significant decline when compared to the $40 million spent in 2022.

- This combination of sustained demand, higher margins, and reduced capex leads me to estimate that Miller Industries shares are worth $55.

- The main risk is economic risk so it is important for investors to keep an eye on incoming economic data.

Even as the stock is up 40%+ year to date, the market seems to be missing the Miller Industries, Inc. (MLR) operating leverage story. Miller Industries has been a solid business in the towing and recovery equipment industry as they have had consistent and profitable growth over a long period of time. I believe that results will improve materially over the next few years as the business begins to reap the benefits of investments made over the last few years and operating leverage becomes apparent.

As this happens the stock will start to screen well as higher margins prove sustainable, capital expenditures drop when compared to 2022, and ROIC increases. The stock should command a more premium earnings multiple when this happens, as investors take notice. Of course, sustained demand must continue for this to happen, but recent evidence makes me believe that there is a good chance this will happen.

In this article I'll provide a general overview of Miller Industries and its past financial results, why the opportunity with Miller Industries currently exists, and what I believe the value of its stock is given recent optimistic commentary from the management team.

Business Overview

Miller Industries primarily manufactures and sells made to order bodies and parts for wreckers and car carriers. Their products are primarily sold through distributors and are installed on truck chassis that are manufactured by third parties. I like this business because it is relatively easy to understand as they don't manufacture a variety of products for a variety of uses; almost all of their business involves products for wreckers, car carriers, and transport trailers.

While they aren't diversified through the industry they operate in, they are diversified through their customer base. In 2022, only one distributor accounted for 11.2% of sales and no other distributor accounted for more than 10%.

Miller Industries' strong relationships with its distributors is a competitive advantage for the business. Most of their distributors have been selling their products for over 10 years, and many of them have been selling their products for 25+ years. This makes Miller Industries entrenched with these customers, and it is likely that these relationships will continue for a long time from here. Additionally, management believes that more than 90% of their distributors only offer products from Miller Industries, despite not having any exclusivity contracts. These strong relationships with a relatively diversified customer base makes Miller's spot in the industry secure.

Past Financial Results

As I mentioned above, Miller Industries has had solid and profitable growth over the past 10 years. Since 2013, revenue has grown at an 8.5% CAGR from $404 million to $848 million, operating income has grown at an 8.4% CGAR from $14 million to $29.6 million, and ROIC has averaged about 12% in that time. Operating income was actually highest in 2019 at $53 million when margins were highest and revenue was similar to what it was in 2022.

Miller's business is more resilient to economic weakness than other businesses in the trucking industry. Commercial Vehicle Group, Inc. ( CVGI ) for example is much more sensitive to changes in GDP. Commercial Vehicle Group manufactures and sells parts for a variety of vehicles, but has a large exposure to the Class 8 heavy-duty truck market, which is very sensitive to changes in GDP. In 2016, U.S. GDP decelerated to 1.7% from 2.7% in 2017. This caused a 20%+ reduction in the production of Class 8 heavy-duty trucks, and the Commercial Vehicle Group's revenue and operating income dropped 20%. Miller Industries does not have this type of sensitivity to changes in GDP.

Notice the large fluctuations in Commercial Vehicle Group's revenue over the past decade.

A look at financial results from 2013-2019 paint a much better picture for Miller Industries. Revenue CAGR in that period was 12.4%, operating income CAGR was 25% and ROIC averaged closer to 15%.

The pandemic is the clear marker of these different numbers. In 2020, demand dropped for their products as the economy shut down and as demand subsequently picked up, supply chain issues led to a drop in margins. Sales are just now back to where they were from before the pandemic, and margins are still lower.

However, I believe Miller Industries is at an inflection point. It is just coming off of an $82 million investment cycle that expanded and modernized its operations, while at the same time, it has a record backlog to get through. When this revenue from the backlog is recognized, it will be at a higher margin due to the increased efficiencies and more of it will flow through to free cash flow due to lower capital expenditures as the modernization investment cycle is over.

Of course, demand must remain high for these increased efficiencies to mean anything, and investors must keep this in mind as they consider an investment in Miller Industries. At the moment, signs are pointing to the economy maintaining its strength into the second half of the year. Additionally, management has maintained 2023 guidance and is currently investing heavily into working capital in order to work through its backlog. I will incorporate this positive momentum with the economy and management's positive views on demand into the assumptions in my DCF, but investors should keep an eye on all signs of economic weakness that may lead to a drop in future demand or cancellation of orders.

Valuation and Price Target

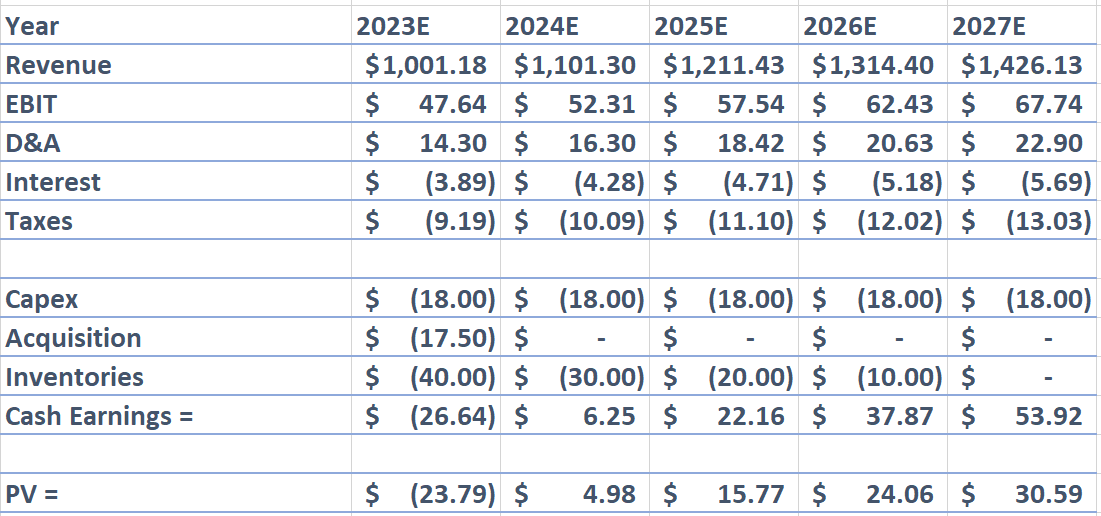

Miller Industries DCF (Created by Author) Miller Industries DCF (Created by Author)

{kind=link}

Miller's management is currently guiding for revenue in excess of $1 billion in 2023 with sustainably higher margins. I will use this as a starting point for my valuation.

I am assuming 18% revenue growth in 2023 followed by 10% in 2024 and 2025, followed by 8.5% in 2026 and 2027. I am assuming a constant 11.5% gross margin, operating expenses equal to a constant 6.75% of revenue through 2027, interest expense equal to a constant 1.7% of debt, a 21% tax rate, D&A equal to 11% of PPE, and capex equal to a constant $18 million through 2027 based on guidance from the Q4 2022 earnings call. I am also assuming significant investment in inventories, amounting to $40 million in 2023 and declining by $10 million per year to $0 in 2027.

For the continuing value, I am assuming a 2% terminal growth rate and a 12% WACC. These assumptions lead me to an intrinsic value of about $55 per share, or about 47% upside from today's price.

I believe this opportunity exists because investors aren't paying much attention to the stock and don't see this operating leverage story coming. For example, there were no analysts asking questions on the Q4 2022 earnings call and only 1 analyst on the Q1 2023 call. While these calls were short, they contained very relevant information to the value of the business, such as the call for reduced capital expenditures moving forward.

Risks

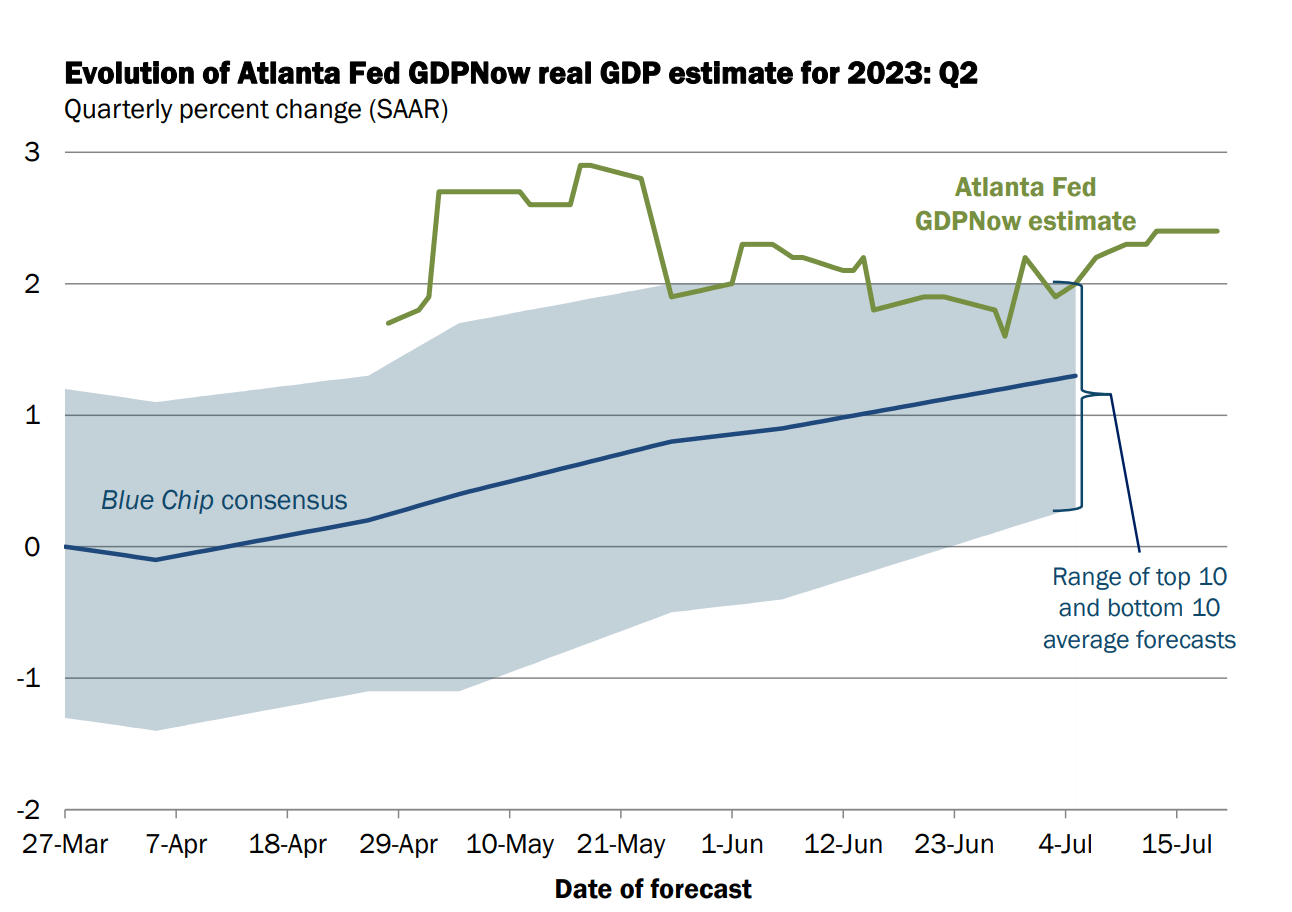

The main risk is that of economic risk. If the economy weakens through 2H 2023 and into 2024, the greater business efficiencies and supply chain improvements won't be able to stop sales and earnings from dropping. This makes it necessary to have some sort of opinion on the macroeconomic environment when investing in Miller Industries. For now, it seems that recession calls for 2H 2023 will get pushed into 2024 as the Atlanta Fed's GDPNow GDP growth estimate for 2023 rose a bit over the past few months.

Atlanta Fed GDPNow Real GDP Estimate (Atlanta Fed)

{kind=link}

Miller Industries investors should keep track of GDP growth going forward and be aware that this can cause the value of the business to differ from my forecast, as my assumptions are based on positive commentary from management.

This is also a micro-cap stock, so it can volatile if there is a large buyer or seller. It is also relatively illiquid, with less than $1 million in shares traded daily. If an investor is wary of volatility or may need to sell out of their position quickly, it is best to avoid investing in Miller Industries.

Final Thoughts

Investors are missing the operating leverage story that will play out for Miller Industries. They just completed a large investment cycle in which they modernized and expanded their operations in order to meet its record backlog. As the revenue from the backlog is recognized, it will be at a higher margin due to the improved efficiencies and more will flow through to operating cash flow. On top of this, capital expenditures will be lowered going forward as management guided for reduced investment going forward in the Q4 2022 earnings call. There were no analysts on that call, so it seems that investors aren't paying much attention to this news.

If demand holds up, margins will be sustainably higher, free cash flow will be higher, and my estimate of the value of the business is $55 per share. The main risk with an investment in Miller Industries is economic risk, so investors should pay attention to data that may indicate upcoming economic weakness.

For further details see:

Miller Industries: The Market Is Missing This Operating Leverage Story