MLKN - MillerKnoll: Comfortable Chairs Not So Comfortable Valuation

2023-12-07 23:51:37 ET

Summary

- MillerKnoll's financial metrics are subpar, indicating it is not an attractive investment at the moment.

- MLKN has a high level of debt compared to its market cap, which may become hard to handle if not managed properly.

- The company's efficiency and profitability have declined in recent years, and its revenue growth is not impressive, making it an unexciting investment option.

Investment Thesis

I wanted to take a look at MillerKnoll's ( MLKN ) financials to see if it would be a good time to start a position in the company. Unfortunately, the metrics that I deem important in a sound investment are subpar, which means that the company is not an attractive candidate until I see solid proof that the new efficiency is here to stay.

Briefly on the Company

MillerKnoll is a company known for a range of commercial and residential furnishings, including office desks, and very comfortable office chairs, that I had the pleasure of sitting on for a good 5 years. One of the reasons I wanted to cover this company was because I am looking for a good office chair for my home office setup, which reminded me of how comfortable it was to sit for hours at my corporate job on the Herman Miller Aeron chair. Cheap chairs just don't cut it. Herman Miller merged with Knoll, back in 2021 creating a formidable leader in modern design, combining expertise for both companies.

Financials

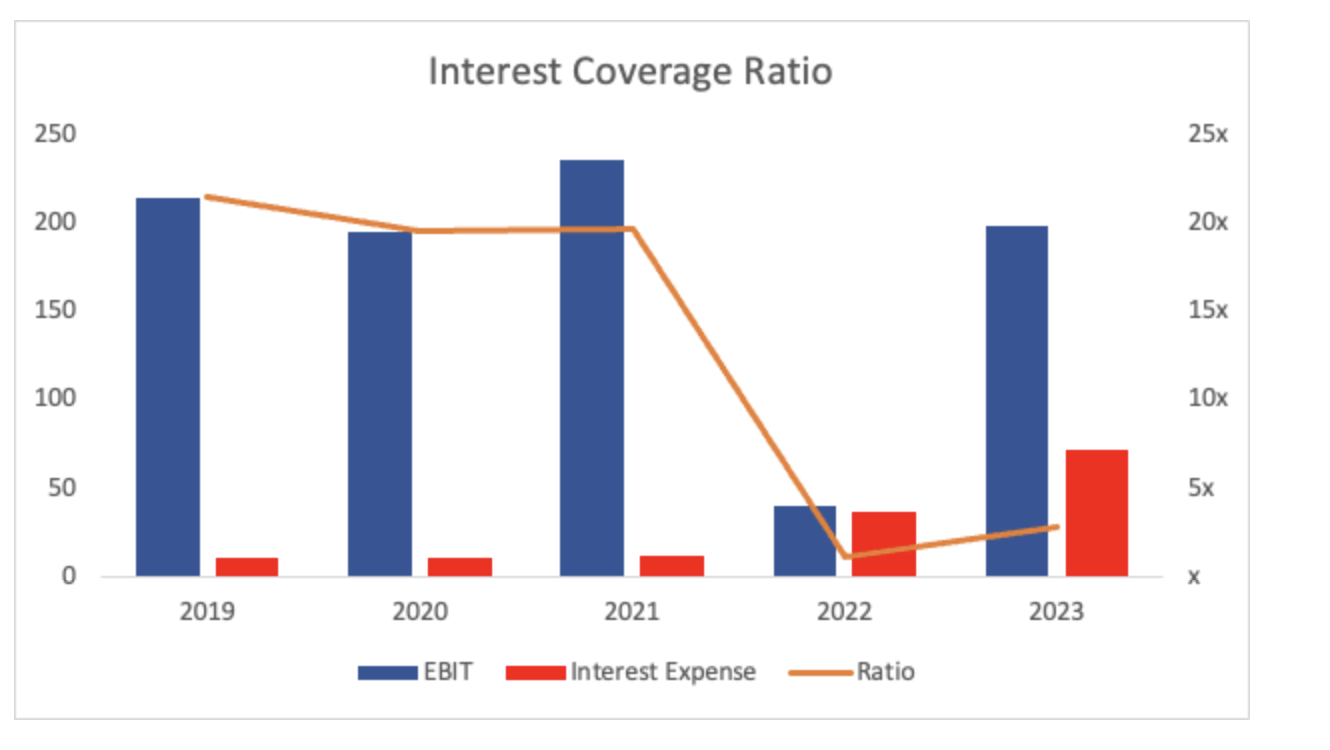

As of Q1 '24 , the company had around $217m in cash and equivalents, against $1.3B in long-term debt. That is more than half of the company's total market cap. A lot of investors would avoid overleveraged companies, and I would agree sometimes, especially if the debt is not manageable and excessive. So, does MLKN have too much debt on their books? To determine this, I like to look at how easily can the company cover annual interest expenses on debt. Historically, the interest coverage ratio was much more robust, and the company I would consider was managing its debt. Fast-forward to the last couple of years, the ratio dropped off a cliff as the company took on more debt while operating earnings did not improve that much. FY22 saw a massive reduction in operating earnings while interest expenses on debt tripled. EBIT recovered nicely as the company managed to curb expenses in FY23.

As of Q1 '24, the company's interest coverage ratio stood at around 2x. Many analysts consider this to be a healthy ratio, which means that EBIT can cover interest expense on debt twice over. To me, this is a little too close for comfort, as it allows for very little leeway for the bad years of performance, meaning if one year the company's expenses are not covered by revenues, it will make negative EBIT and that would mean it may have trouble meeting all the debt obligations. I prefer a ratio of at least 5x, which allows for some unexpected fluctuations in operations. So, I would say the company is at no risk of insolvency, however, I will have to add a little bit more margin of safety in my valuation.

{kind=link}

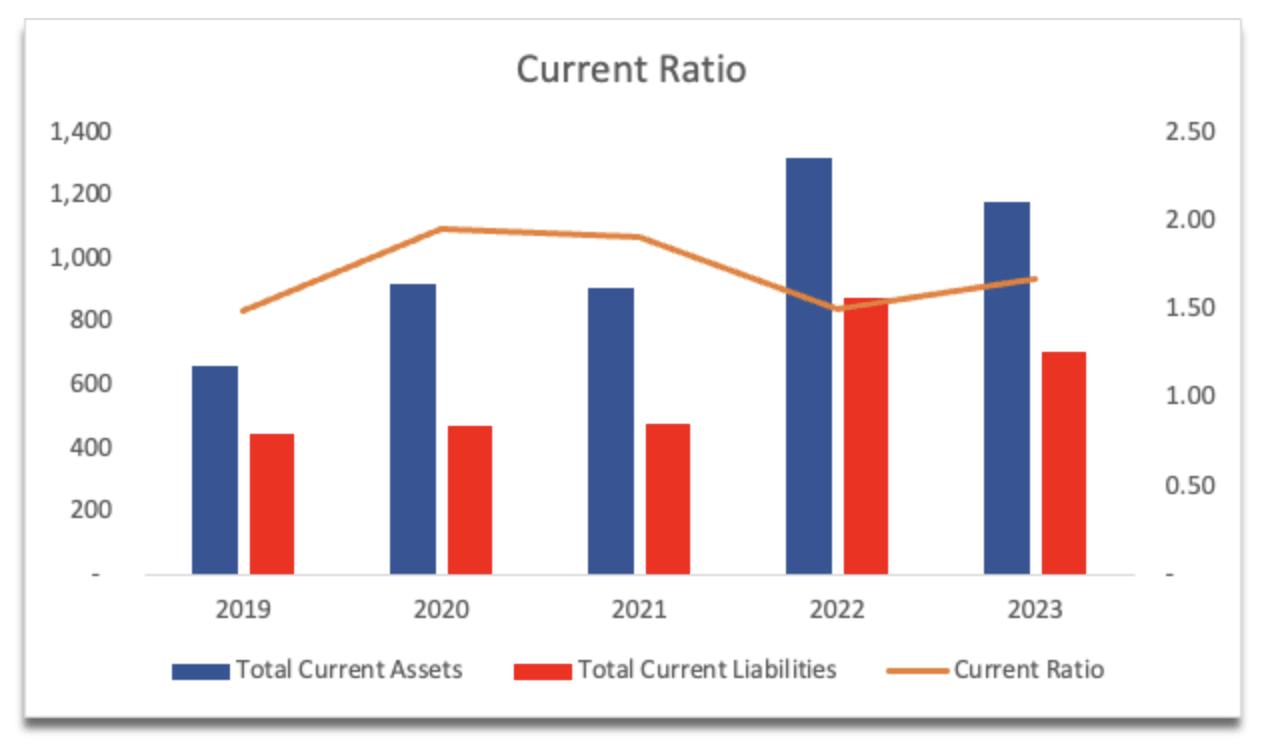

The company's historical current ratio has been decent over the years, and it's not different in the latest quarter, standing at around 1.5. This is at the lower range of what I believe is an efficient current ratio range of 1.5-2.0. This tells us that the company is not hoarding assets like cash, which could be used to further the growth of the company. Anything too much over 2.0 I consider an inefficient use of assets and a wasted opportunity to expand.

{kind=link}

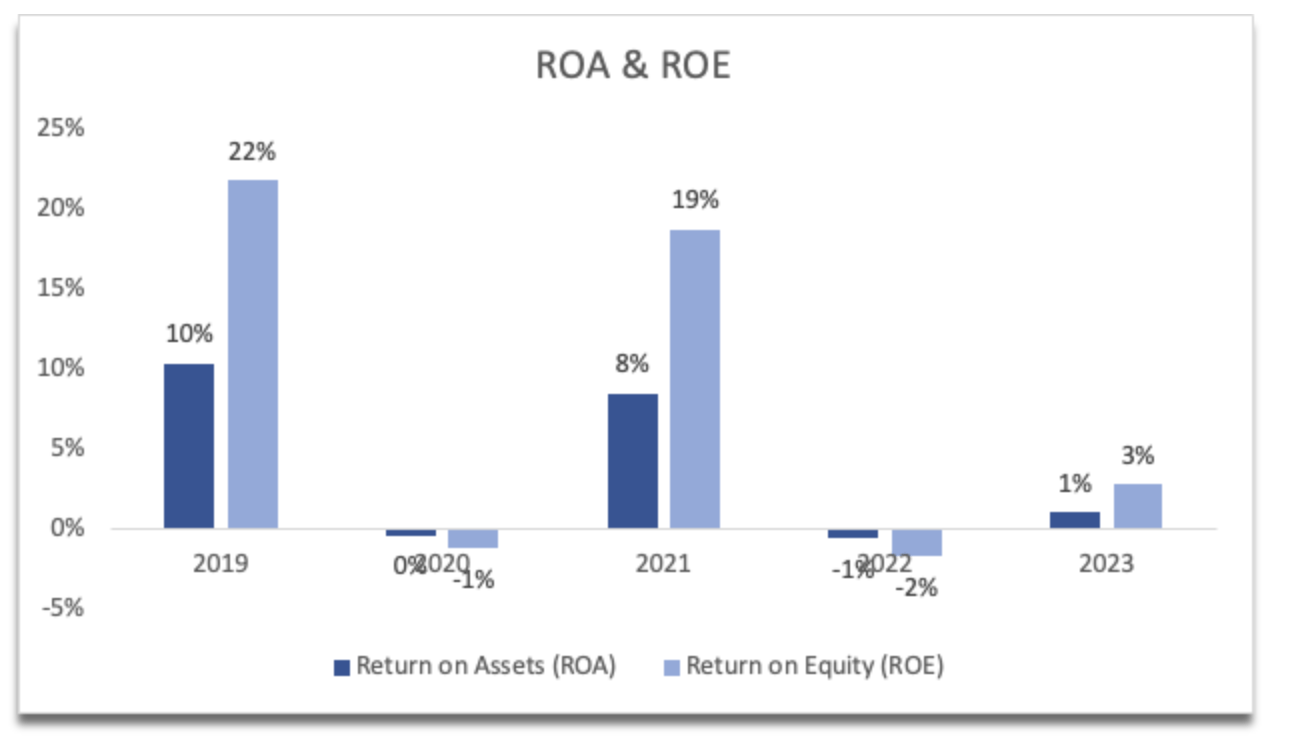

Speaking of efficiency, the company's assets and shareholder capital aren't being used very efficiently as the ROA and ROE have been quite poor in the last couple of years. That is not what I like to see when looking at historical trends. Unfortunately, the 60% increase in revenue in FY21 increased expenses and COGS by 83% and 71%, respectively, which tells me that there was mismanagement somewhere along the way in either spending too much on marketing that led to lower profit margins, or the company is not very scalable, and that is a big red flag. I will have to consider this when valuing the company's intrinsic value.

{kind=link}

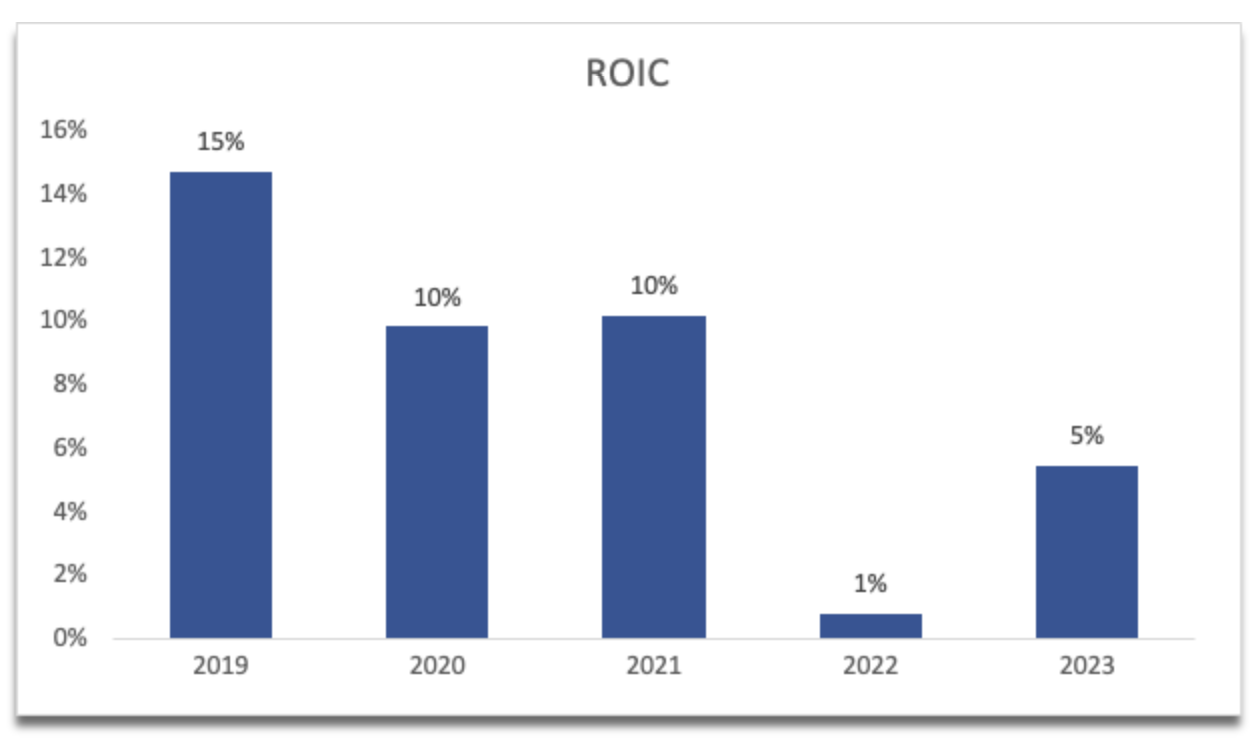

The same can be said about the company's return on invested capital, which has dropped significantly over the last couple of years. I usually look for at least 10%, and the company managed to achieve this in previous years, however, it seems that the management is struggling to find projects that would yield a better return on capital.

{kind=link}

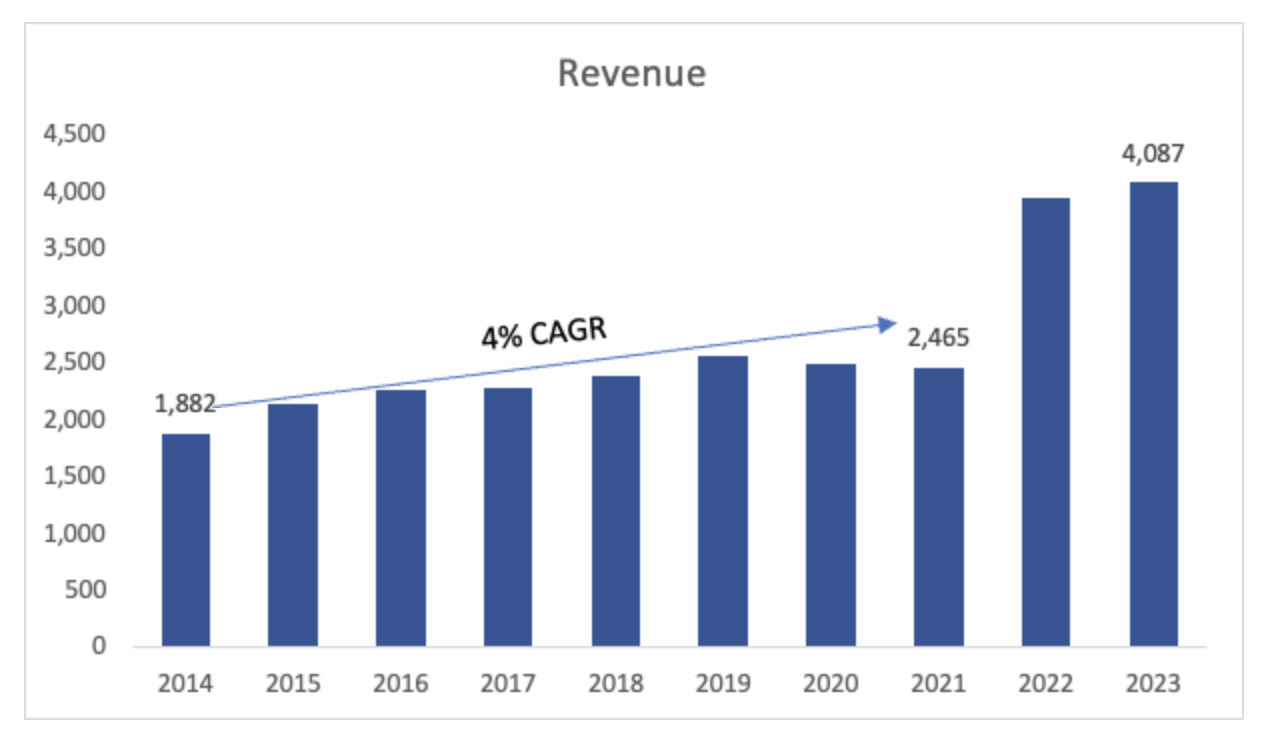

In terms of revenues, in the last decade, the company managed to grow at around 9% CAGR. It would have been much lower if it wasn't for the 60% increase in sales from FY21 to FY22, which was inorganically inflated by the acquisition of Knoll. If we exclude the acquisition, the CAGR would be 4%, which is not very impressive at all. Furthermore, the company experienced around 4% from FY22 to FY23, which matches the company's historic growth. Nothing impressive in terms of revenues here, which makes for an unexciting investment for many investors who are looking for growth. There are other important metrics to look at, for example, the next metric, which is the margins.

{kind=link}

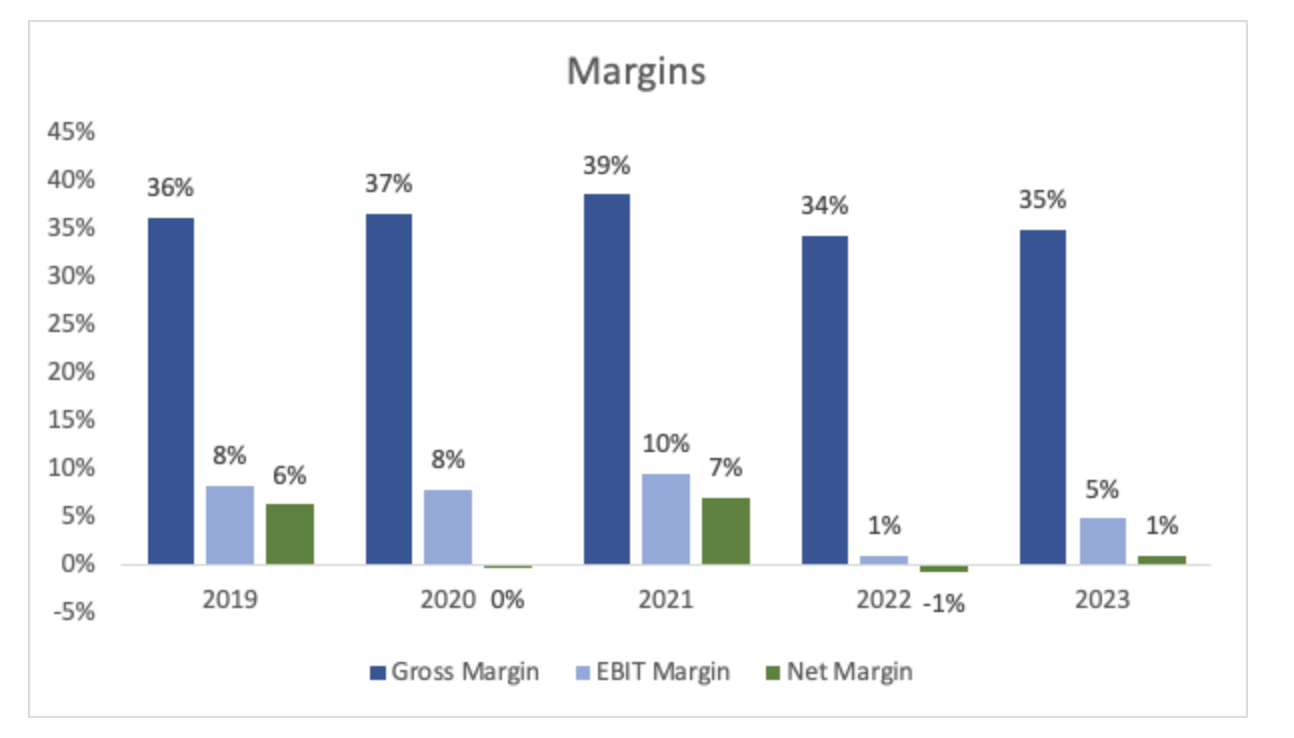

Margins have seen better days also. The company seems to have lost its efficiency and profitability over the last couple of years, which is not very encouraging in my opinion. However, it is not all bad. If we look at the most recent quarter, the company managed to increase gross margins to 39% citing "the impact of price increase actions, reduced costs associated with commodities, inventory handling, and freight costs, as well as from the realization of synergies associated with the Knoll integration."

So, it looks like the company is taking the right steps to improve profitability and efficiency, can these be sustained going forward? Only time will tell as we only have one quarter of improvements and that is not a lot of data to say for sure.

{kind=link}

Overall, it is too early to judge the improvements of the latest quarter because I like to look at the big picture to interpret the information and form assumptions, therefore, I will be approaching the valuation with a conservative mindset. There are quite a few important metrics above that the company was lacking in, especially in the efficiency and profitability ones.

Comments on the Outlook

As I mentioned, the improvement in margins is a welcome change, however, we cannot be sure that it is going to be sustainable in the long run. I have my doubts about one revenue segment, and that is the office. Yes, people are returning to offices these days, with over 69% of respondents in the survey saying they are back in the offices full-time. This sounds good in theory, however, once people had a taste of that remote work, where they feel a lot more productive and have a better work-life balance, it is very hard to convince people to have 2-3-hour daily commute when they could just open their laptop at home and do the same job. That is how I felt and my friends who quit jobs because it was required to be back 5 days a week in the office. A hybrid work environment is here to stay, and many companies are getting rid of their expensive leases in the big cities because working from home is a very viable and preferable option, and I agree.

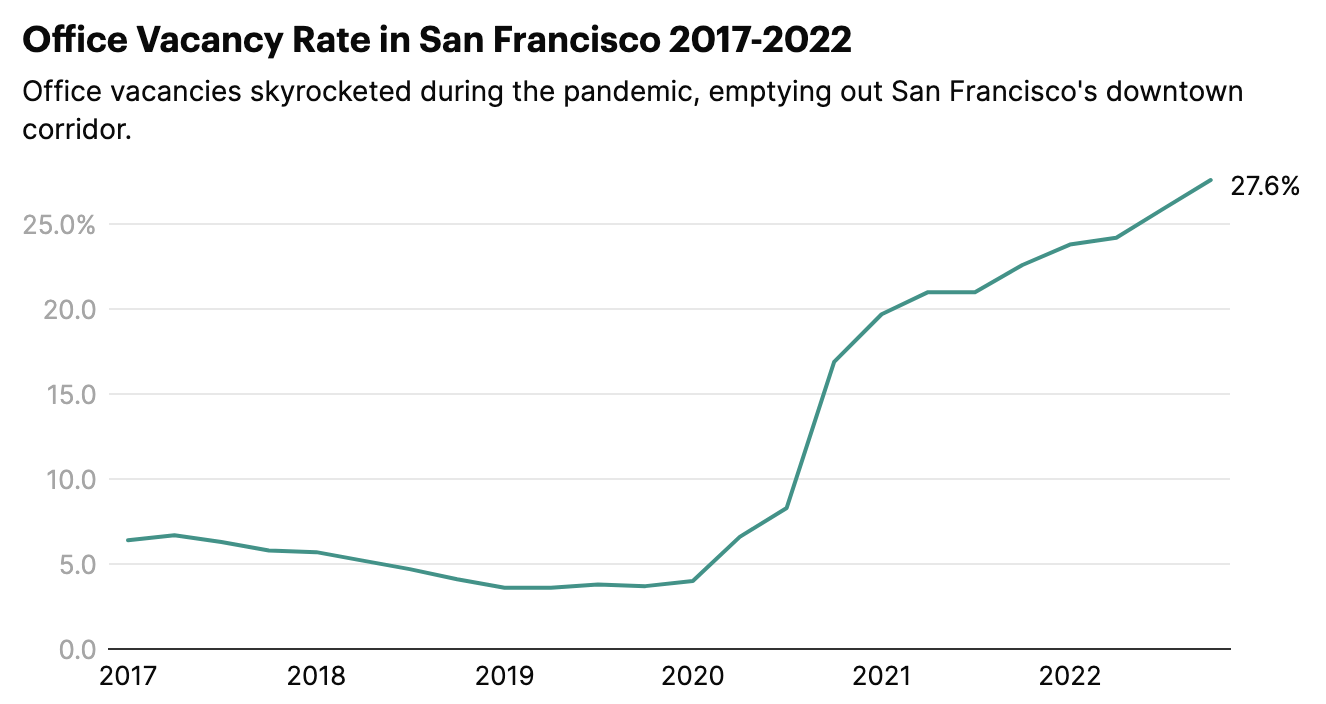

A prime example of this is the city of San Francisco. Ever since the pandemic hit, many people who used to come to work in SF for the big tech companies have moved back to their homes outside of SF because they can still get the same salary and live in a much more affordable place. Now the city is full of vacant office spaces . I don't think that is going to translate to a lot of chair sales. On the other hand, people may need a good office chair for their home offices, like me.

{kind=link}

Valuation

For the revenue growth, I decided to go with the company's historical average of around 4% and not the 9% if we include the acquisition inorganic growth. All segments in the most recent quarter saw single-digit to low double-digit declines, so that doesn't provide confidence for future growth, as I don't see any catalysts currently. Below are the assumptions for the base, optimistic, and conservative cases with their respective CAGRS.

{kind=link}

In terms of margins and EPS, I decided to be more optimistic here and increased the company's profitability and efficiency going forward compared to FY23. I'm assuming that the cost-cutting measures of Q1 '24 are maintained and these margins become the new norm going forward. Below are my assumptions for margins and EPS.

{kind=link}

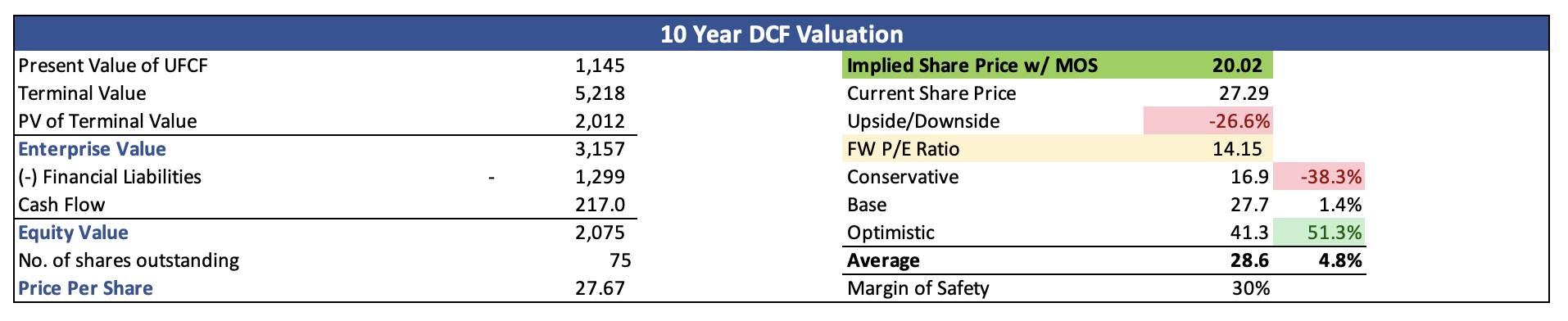

On top of these assumptions, I went with a 10% discount rate instead of the company's WACC of around 7% because I would like to have a little extra margin of safety for the lackluster efficiency in the above financials and high debt. Furthermore, I added another 30% margin of safety to take on the risks of the company and the lack of growth catalysts, coupled with macroeconomic headwinds of high interest rates and lingering inflation.

With that said, MillerKnoll's intrinsic value and what I would be willing to pay for it is $20 a share, which means the company is too expensive for me and not worth the risk.

{kind=link}

Closing Comments

Just half a year ago the company was worth half of what it is now, riding the improvement in margins higher, which I think is an overreaction to the upside and not worth such a quick appreciation in price. One-quarter of good numbers doesn't mean it is going to be like that for the rest of the year, with so much uncertainty lingering globally.

Even with an improved margin in my model, the company is not worth the price it is trading at, therefore, I am assigning a hold rating and will wait for the right entry, which may or may not present itself in the next few months or so. I will be setting a price alert at around $20 a share and will revisit if it hits.

For further details see:

MillerKnoll: Comfortable Chairs, Not So Comfortable Valuation