MLKN - MillerKnoll: Still Undervalued But It Might Be A Good Time To Book A Profit

2023-10-01 07:57:35 ET

Summary

- MillerKnoll, Inc. has seen a 43% increase in stock price since the last report, but current market conditions may hinder future growth.

- Q1 FY24 net sales declined by 14.9% compared to Q1 FY23, with all three segments underperforming.

- The stock price is at a crucial level and may experience a fall if it fails to cross the $28 resistance zone. Hold rating advised.

MillerKnoll, Inc. ( MLKN ) distributes interior furnishings. In my last report, I presented a bullish case on MLKN, and it turned out quite well. The stock price has moved up around 43% since my last report , which was published two months back. I still believe it is undervalued, but I think it might be a good time to book profit because the current market conditions aren’t favorable, which can hamper the company’s growth in the coming quarters. So, I assign a hold rating on MLKN.

Financial Analysis

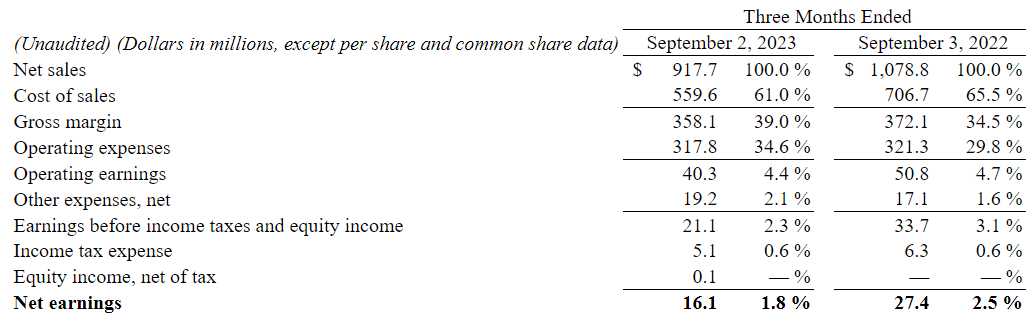

They recently posted their Q1 FY24 results . The net sales for Q1 FY24 were $917.7 million, a decline of 14.9% compared to Q1 FY23. Its International and Americas contract and global retail all three segments underperformed, which led to a decline in net sales. The sales from the International and Americas contract segments were down by 16.2% and 8.7%. The sales from the global retail segment were down by 26% in Q1 FY24 compared to Q1 FY23. The International contract segment was affected by weakness in Europe, and China brought on by unfavorable economic conditions. The downward trend in the North American housing market affected the Americas contract and global retail segment sales. Its gross margin in Q1 FY24 was 39%, which was 34.5% in Q1 FY23. I believe a higher pricing strategy and moderating input costs were the major reasons behind the margin improvement.

{kind=link}

The net earnings for Q1 FY24 was $16.1 million, a decline of 41.2% compared to Q1 FY23. Obviously, the decline in sales was the reason behind the decline in earnings, but Q1 FY23 included an extra week of operations, so if we take that extra week out, the earnings decline won't be as significant as it is right now. Sometimes, the numbers don't show the real picture, and here, the numbers are showing weakness. To some extent, it is true, but not entirely. The company had to face several macroeconomic headwinds, and its business was held in adverse economic conditions. They are still facing headwinds like high-interest rates and the housing market slowdown, which they faced in FY23. The interest rates in Europe are continuously rising, and the mortgage rates are at 20-year highs, affecting North America's housing market. So, I believe that until these conditions are normal, the company might find it difficult to record positive revenue growth.

Technical Analysis

{kind=link}

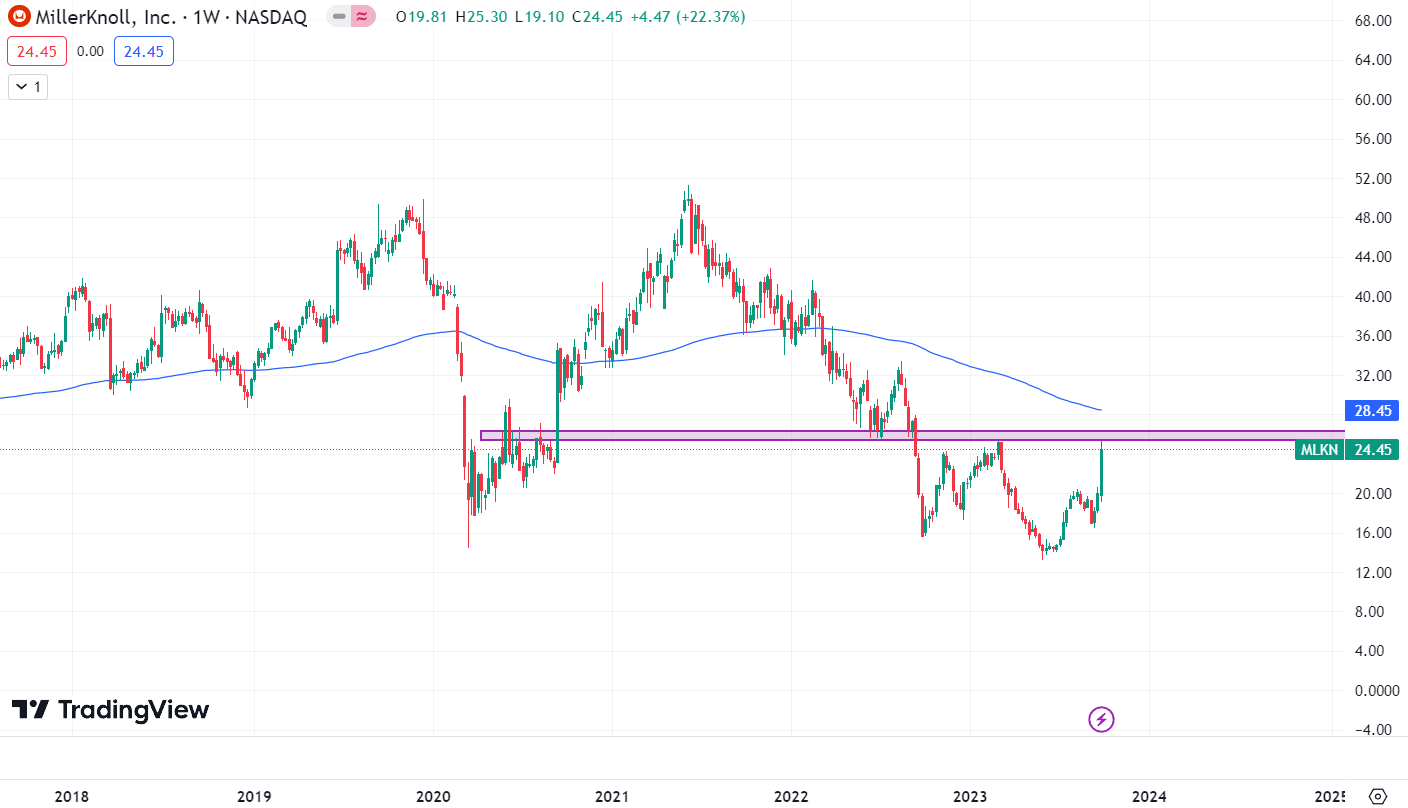

It is trading at $24.4. I mentioned in my last report that $17 is a strong support zone, and buyers are active around that area, and one can see that the stock price has rebounded strongly from that level. It has moved up more than 40% from that level and has reached an important resistance zone of $25-$28. It touched the $28 level recently and faced rejection, which can be a warning sign because the stock price has touched the resistance zone twice. The first time it happened was in November 2022, and the price fell almost 25%, and the second time the price touched the resistance zone was in February 2023; that time, the price fell about 45%. So, I believe the stock price is at a crucial level because if it fails to cross the $28 level, we might see a fall in the stock price. Hence, I would advise not to make any new buying positions in this stock until it crosses the $28 level.

Should One Invest In MLKN?

I still believe MLKN is undervalued and has a lot of potential. Their gross margin improved, and the management is trying to grow the company by introducing new products and opening stores if we look at its valuation. It is still trading below its historical averages and industry standards. It has a P/E [FWD] ratio of 14.58x, which is lower than the sector median of 19.43x, and has an EV / EBIT [FWD] ratio of 12.88x compared to the sector median of 14.99x. So, the valuation is still favorable, and management’s efforts to expand the company are impressive. However, the current market conditions are unfavorable, and it might affect its growth in the near term. In addition, the stock price is at a crucial level, or we can say at a make-or-break level. Hence, considering the current market conditions, it might be risky to make fresh buying positions. So, I assign a hold rating on MLKN.

Risk

As of June 3, 2023, MillerKnoll's combined long-term debt was $1.37 billion. They significantly increased their debt due to acquiring Knoll, which increased their interest costs and would, among other things, limit their ability to adjust to shifting business and economic situations. Additionally, they have suffered several fees related to this debt. The demands on their financial resources are greater than the cash flows previously needed to service their debt because of the amount of cash needed to pay interest on their higher debt levels. The rising debt levels will also decrease the amount of money available for working capital, capital investments, acquisitions, and other general corporate reasons, which could put MillerKnoll at a competitive disadvantage compared to other businesses with lower debt levels. Their capacity to service their debt could suffer if they fail to realize the anticipated advantages and cost reductions from the merger or if the merged company's financial performance falls short of current projections.

Bottom Line

I still believe it is undervalued, but the current market conditions aren’t favorable, and its growth might be hampered due to adverse market conditions. Additionally, the stock price is at a crucial level. Hence, it would be wise not to make a fresh buying position in this stock. So, I assign a hold rating on MLKN.

For further details see:

MillerKnoll: Still Undervalued But It Might Be A Good Time To Book A Profit