MLKN - MillerKnoll Stock: On A Roll

2023-09-03 10:17:16 ET

Summary

- MillerKnoll, a designer and manufacturer of interior furnishings, has seen its stock rally recently off multi-year lows.

- The company operates through three segments: Americas Contract, International Contract & Specialty, and Global Retail.

- Despite myriad challenges, MillerKnoll expects to maintain flat earnings in FY24 and has made progress on its balance sheet.

- The shares also pay just north of a four percent dividend yield and saw some insider buying in July.

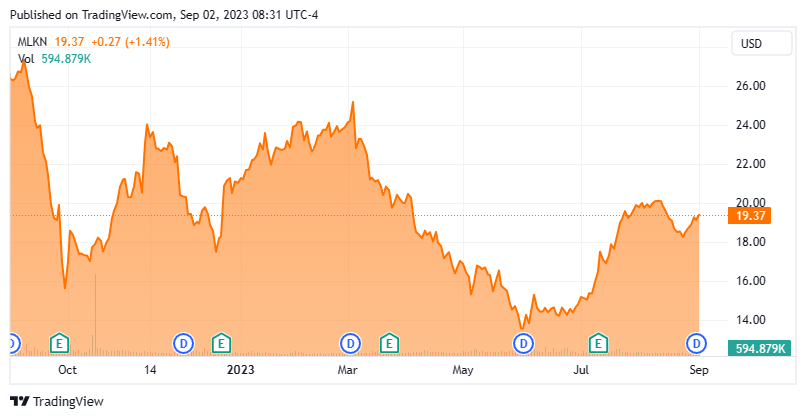

- With the stock up 45% from its recent lows, can the rally continue? A full investment analysis follows in the paragraphs below.

It's easier to die than to move ... at least for the Other Side you don't need trunks . ? Wallace Stegner, Angle of Repose

Today, we look at a housing related concern whose stock has been on a recent roll and whose shares have seen some insider buying of late as well. The company is seeing some significant synergies from a large acquisition made in 2021. Can the rally continue? A full analysis follows below.

{kind=link}

Company Overview

MillerKnoll, Inc. ( MLKN ) is a Zeeland, Michigan based designer, manufacturer, and distributor of interior furnishings for use in office, healthcare, educational, and residential environments throughout the world. Its portfolio of 16 higher-end or luxury brands is sold through office furniture dealers, retail studios, catalogs, and its ecommerce platform MillerKnoll Brand Collective . MillerKnoll was founded as Star Furniture in 1905, rebranded to Herman Miller in 1923, went public in 1970, and acquired Knoll (founded in 1938) in 2021. Shares of MLKN trade just under twenty bucks a share, translating to an approximate market cap of $1.45 billion.

Company Presentation

The company operates on a 52- or 53-week fiscal year (FY) ending the Saturday closest to May 31st. For the avoidance of doubt, the 53-week period ending June 3, 2023 is FY23.

Company Presentation

Acquisition of Knoll

In July 2021, Herman Miller completed its acquisition of Knoll for a total consideration of $1.89 billion, including cash of $1.18 billion (financed by debt) and 15.84 million shares of Herman Miller stock with a value of $710.7 million at transaction close. Designed to deliver cost synergies of $120 million over its first three years, the combination rebranded to its current moniker in September 2021.

Segments

Owing to this addition, management now views its performance through three operating segments: Americas Contract, International Contract & Specialty, and Global Retail.

Americas includes furniture sales to office, healthcare, and educational settings in North and South America. It generated FY23 Adj. operating earnings of $159.4 million on net sales of $2.03 billion versus Adj. operating earnings of $32.6 million on net sales of $1.93 billion in FY22, representing an increase of 5% at the top line (0.3% organic). The increase at the segment's bottom line was driven by better pricing and synergy benefits.

International is essentially ex-Americas and global sales of specialty brands that include Holly Hunt, Spinneybeck, Maharam, Edelman, and Knoll Textiles. It accounted for FY23 Adj. operating earnings of $112.5 million on net sales of $1.02 billion as compared to FY22 Adj. operating earnings of $98.0 million on net sales of $928.5 million, reflecting a 10% improvement (7% organic) at the top line. The rise at the bottom line was driven by better pricing and product mix.

Global Retail includes residential furnishings and accessories sold to third-party retailers, as well as ecommerce, direct-mail catalogs, and physical store sales. It includes the preponderance of the Knoll brand. It was responsible for FY23 Adj. operating earnings of $39.4 million on net sales of $1.04 billion versus FY22 Adj. operating earnings of $142.6 million on net sales of $1.09 billion, representing a 4.1% decline (-5.1% organic) at the top line. Lower volume, product mix, and increased freight expenses were cited for the significant drop at the segment's bottom line.

Share Price Performance

Obviously tethered to the macroeconomic environment, shares of then MLHR hovered around $30 a share for the middle portion of the 2010s, eventually rising to a then all-time high of $49.87 in December 2019, only to plummet to $14.39 in the throes of the pandemic selloff in March 2020. With the reopening of the economy and the gradual return of workforces to their offices, the company's stock rallied. Even the risk arbitrageur pressure from the Knoll deal announcement in April 2021 and the implied 45% premium paid could not keep its stock down for long, eventually reaching an all-time high of $51.25 per share in June 2021. Despite the disruption from the pandemic, pre-combination Herman Miller delivered surprisingly consistent results: non-GAAP net earnings of $2.98 per share in FY19; $2.61 per share in FY20; and $3.07 a share in FY21 (ending May 29, 2021).

However, with the addition of Knoll, emerging supply chain and labor issues were further amplified, responsible for a 430-basis point decline in gross margin (FY22 vs FY21) to 34.3%. These issues could not be made up through operating synergies, with non-GAAP EPS decreasing 37% to $1.92 a share in FY22. As such, shares of MLKN essentially halved to an intraday low of $25.86 53 weeks after reaching their all-time high. Approximately one year later (on June 1, 2023), MillerKnoll stock made a 14-year low, halving again to $13.20.

Q4 FY23 and FY24 Financials and Outlook

This performance was due to the challenges of FY22 continuing into FY23, with the company earning $1.85 a share (non-GAAP) on revenue of $4.1 billion, when Street analysts 18 months prior were expecting it to earn $3.23 a share (non-GAAP).

MillerKnoll's Q4 FY23 financials, reported on July 12, 2023, were even worse relative to the balance of the fiscal year, as it earned $0.41 a share (non-GAAP) on net sales of $956.7 million as compared to $0.58 a share (non-GAAP) on net sales of $1.10 billion in the prior year period, representing declines of 29% and 13%, respectively. Weakness was spread out pretty much evenly across all three segments, with low CEO and consumer confidence levels blamed on reduced office furnishing and high-end residential spends.

That said, there were some positives to take away. First, the bottom line ($0.02 better) and the top line ($11.1 million better) both beat Street consensus. Second, non-GAAP gross margin improved 220 basis points year-over-year to 37.0% as a layered price increase commencing in October 2022 began to take hold. Third, the synergies from the Knoll deal were on a run-rate of $130 million at YEFY23, meaningfully exceeding prior expectations of $120 million after three years.

Despite the positives, management anticipates the challenging macro environment to continue, with backlogs entering FY24 ($698 million) and Q4 FY23 new orders ($922 million) down 25% and 9% from a year ago, respectively. As such, MillerKnoll expects earnings to be flat with FY23 at $1.85 (based on a range midpoint) and its top line to be slightly lower, which gives effect to FY23's 53-week year versus FY24's 52-week year. It also expects FY24 to be back-end loaded with Q1 FY24 earnings at $0.21 on net sales of $900 million.

Balance Sheet and Analyst Commentary:

Even though the company is forecasted to run in place in FY24, it did make progress on its balance sheet during FY23, generating cash from operations of $162.9 million, which was used to lower debt to $1.37 billion, bringing its net leverage under its loan covenants to 2.5. MillerKnoll held cash of $223.5 million and had total liquidity of $507.7 million, after factoring in its revolving line of credit. It pays a quarterly dividend of $0.1875, translating to a current yield of 4.1%.

There has been scant commentary on the company over the past twelve months; however, it has all been negative with both Benchmark and Craig Hallum downgrading shares of MLKN from buys to holds in calendar 2H22. According to Yahoo! Finance, the average price objective is currently $26. On average, Street analysts expect MillerKnoll to earn $1.83 a share (non-GAAP) on net sales of $3.84 billion in FY24, followed by $2.27 a share (non-GAAP) on net sales of $3.99 billion in FY25.

Board member Lisa Kro has a considerably more bullish outlook on her own company than the Street, acquiring 5,950 shares of MLKN at $16.80 on July 17, 2023.

Verdict:

Possible reasons for Ms. Kro's optimism include: the U.S. Architects Billing Index turning positive in May 2023: orders during the first five weeks of Q1 FY24 in its Americas segment being up 5% year-over-year organically after experiencing an 8% decline year-over-year in Q4 FY23; and legacy Kroll and legacy Herman Miller sales teams having a full year of cross-selling experience.

That said, mortgage rates are still very high and will likely remain elevated for the next year, impacting both new home sales and existing home sales, especially when giving effect to the extraordinarily low rate mortgages many existing homeowners are boxed into. Moving drives demand for furnishings and they should remain depressed as long as mortgage rates are elevated. Furthermore, people are returning to their work settings but on a more hybrid basis, likely meaning a structural change in the demand for work environment furnishings, save healthcare.

These macro headwinds dictate that shares of MLKN shouldn't command market multiples. In other words, 10.6 times FY24E EPS of $1.83 and an EV/TTM Adj. EBITDA of 5.6 are fair values for MillerKnoll.

Furthermore, the company's stock has rebounded some 45% off its 14-year low set less than two months prior, providing Ms. Kro with a tidy short-term profit. However, there is nothing to suggest that a V-shaped rally is in the offing, meaning a pull back to the $15-$16 range, denoting a dividend yield of ~4.8%, a forward PE of ~8.4, and an EV/TTM Adj. EBITDA of 5.0, would be a buying opportunity. Until then, the recommendation is to stay on the sidelines.

He is ill clothed, who is bare of virtue . ? Benjamin Franklin

For further details see:

MillerKnoll Stock: On A Roll