TIGO - Millicom International Cellular: Deleverage Is The Key Focus

2023-11-02 23:34:27 ET

Summary

- TIGO experienced slight deceleration in revenue growth but showed improvement in earnings, reaching breakeven point.

- Colombia exhibited commendable growth, driven by expansion in the mobile sector.

- Guatemala remains the least robust area, but there are indications of progress and expected growth in the future.

Summary

Following my coverage of Millicom International Cellular ( TIGO ), I recommended a buy rating due to my expectation that TIGO will capture more postpaid and broadband customers, which will improve underlying profitability. This post is to provide an update on my thoughts on the business and stock. I am reiterating my buy rating as the fundamentals remain strong in my view and management is committed to deleveraging the balance sheet, which I see as a catalyst that will close the valuation gap vs. peers.

Investment thesis

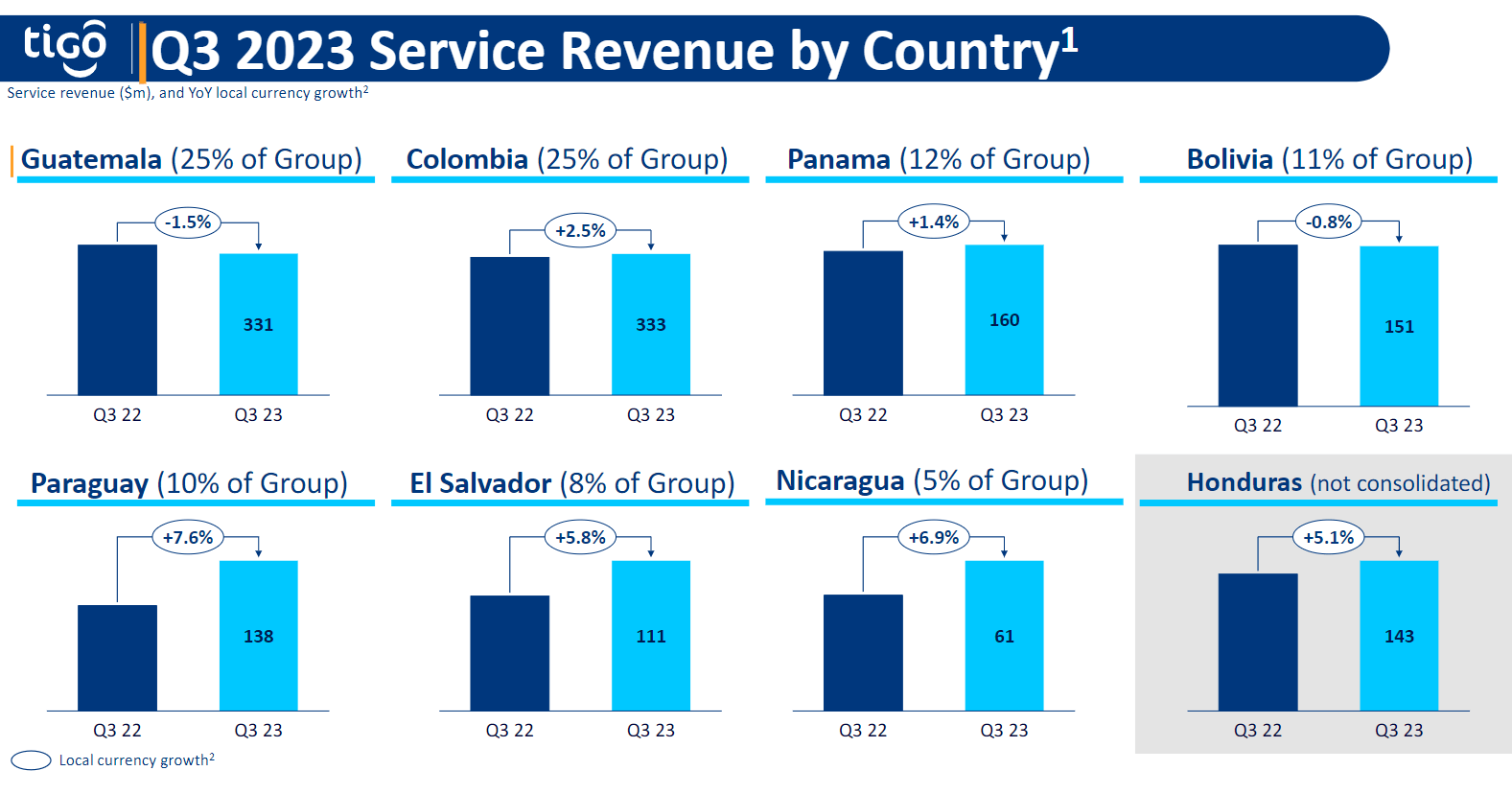

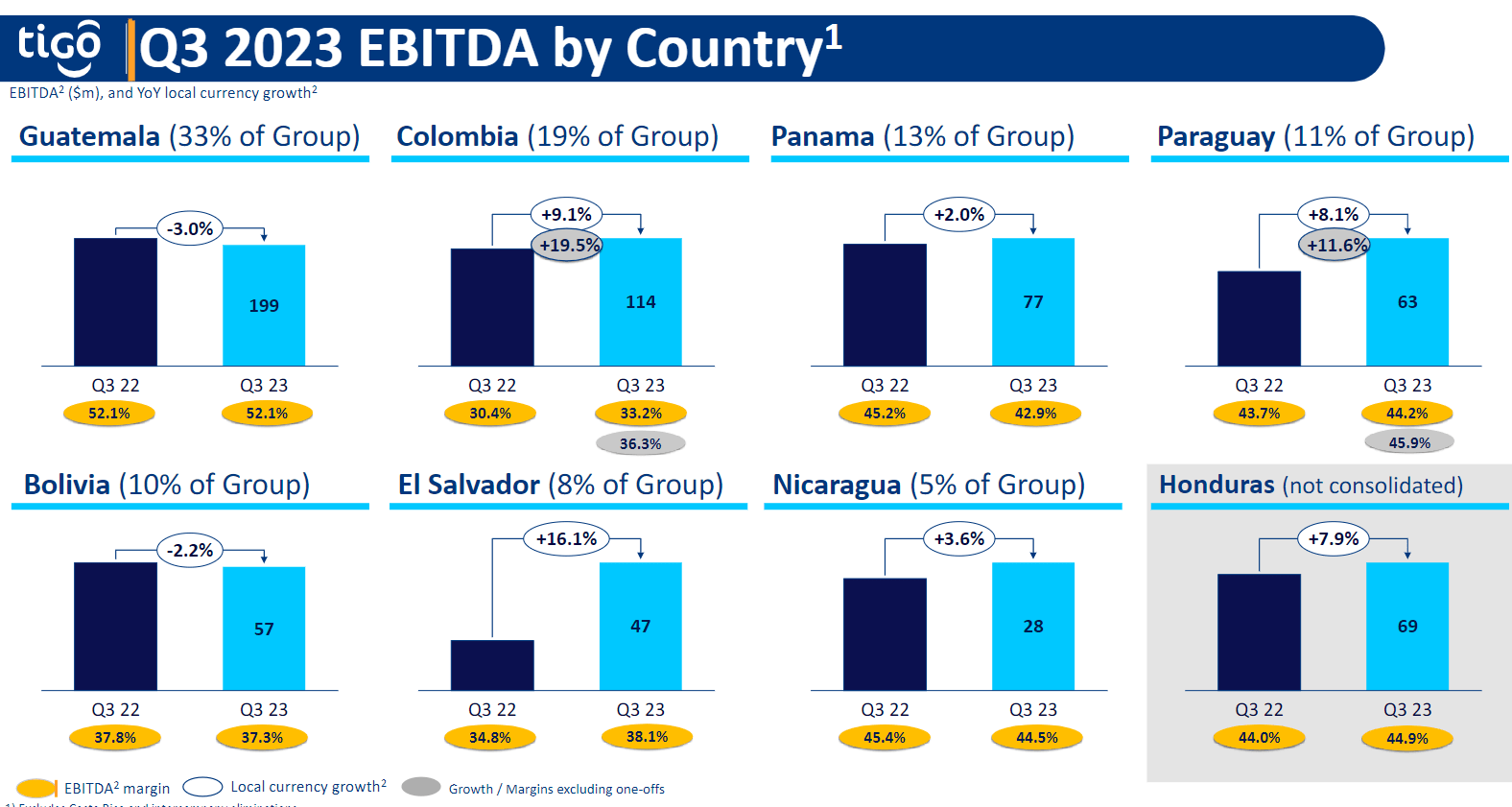

In 3Q23 , TIGO experienced a slight deceleration in revenue growth on a constant currency basis, with a growth rate of 1.8% compared to 1.9% in the preceding quarter. On a consolidated basis, the reported revenues exhibited a year-on-year increase of 2.6%. However, the EBITDA experienced a decline of 1.2%. The earnings, on the other hand, reached a breakeven point, which can be considered a notable improvement compared to the -$32 million recorded in the third quarter of 2022. In my perspective, a more effective approach to analyzing TIGO results and reading through the noise is to conduct analysis at a segmented level. The service revenue of TIGO experienced a growth of 1.8% when measured on a constant currency basis. This growth was primarily driven by a 3% increase in the mobile sector, which represents an acceleration compared to the growth rates of 1.9% in the second quarter of 2023 and 2.2% in the first quarter of 2023. The two regions of interest in this context are Colombia and Guatemala. The reason for the focus on these two is because they are the largest part of the TIGO business in both revenue and EBITDA. Collectively, they represent more than 50% of the business. More importantly, these two regions have become more important throughout the years, representing a bigger mix (as shown in the chart below).

{kind=link}

{kind=link}

Colombia exhibited a commendable growth rate of 2.5% in terms of local currency, a figure comparable to the growth observed in the second quarter of 2023. This growth can be primarily attributed to the significant expansion of the mobile sector, which experienced high single-digit growth. I maintain an optimistic outlook regarding Colombia due to the potential for continued enhancement in profit margins. The current performance indicates that TIGO is operating at a satisfactory level, which is indicative of the efficiency gains achieved through previous investments in network infrastructure and the expansion of its commercial presence. Significantly, the phenomenon of growth also implies the presence of increased price rationality within the market. Going forward, I expect that the primary source of progress will stem from the joint venture established with Telefonica. This is due to the anticipated benefits of streamlining operations through the utilization of a unified network and the consolidation of available spectrum resources.

In the case of Guatemala, it remains the least robust area, with a reported year-on-year growth rate of -1.5% in the third quarter of 2023. Nevertheless, there are indications of progress. Firstly, TIGO successfully implemented price adjustments to its prepaid offering during the latter part of September. The management successfully achieved this by acquiring additional spectrum and enhancing its network infrastructure, thereby narrowing the competitive disparity.

“two important and positive events are relevant in the last few months in Guatemala. One, after two consecutive spectrum auctions, spectrum positions in the marketplace have been increased and stabilized. We no longer have a spectrum deficiency or a spectrum disadvantage in Guatemala. This has an important positive effect on our network efficiency and costs, as well as on our service and product offerings. And two, we took some price increases in prepaid in mid-September

Second, in Guatemala, we are creating the conditions for a healthy and very sustainable long-term industry structure. In the last six months, we took part in two transparent and successful spectrum auctions in which both players were able to acquire all of the spectrum that was offered by the government. 2Q23 earnings results call

This development signifies a significant advancement, in my perspective, as it implies that Guatemala has attained the capacity to engage in competition of comparable magnitude with its counterparts and possesses increased resources (due to the price increase) to attract customers. However, it should be noted that the 4Q23 is expected to encounter challenging comparisons as a result of the occurrence of the World Cup in 2022. However, following the occurrence of 4Q23, I anticipate a resumption of growth that will propel it back into positive territory.

“The chart on the left shows evolution of our mobile customer base and market share in Guatemala over the last four years. As you can see, we've picked up quite a bit of market share during the pandemic.” 2Q23 earnings results call

Another focus of mine for TIGO is its balance sheet, where its leverage ratio remains at 3.2x (same as 2Q23). Management reiterated their guidance to achieve a net-debt-to-EBITDA ratio of 2.5x by 2026. Additionally, they anticipate a significant improvement in free cash flow generation in 2024. The remarks made by management during the earnings call further emphasized the importance of exercising caution and sound judgment. The newly appointed President and Chief Operating Officer, Maxime Lombardini, explicitly recognized that Millicom operates in regions characterized by unpredictable macroeconomic and political conditions. Consequently, it is imperative for the company to mitigate risk by operating in an efficient manner and maintaining lower levels of leverage. Therefore, it is my belief that the new Board and management will maintain a focus on reducing leverage.

Valuation

Own calculation

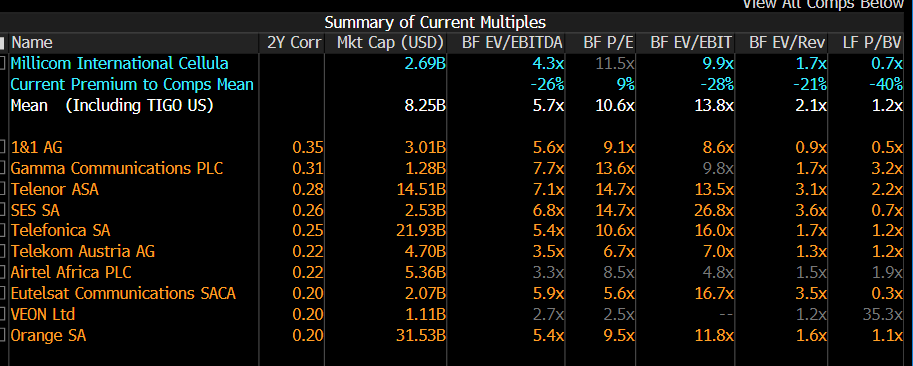

I believe the fair value for TIGO based on my model is $28.95. My model assumptions are that TIGO will grow towards the industry growth rate over the next 2 years and that margins will gradually improve as it gains further scale. My key variable assumption is that TIGO deserves to trade at 5x forward EBITDA, at the same level as peers, given that I expect TIGO to grow revenue at the same rate as what peers are growing at (low to mid-single-digits). In addition, TIGO margins are also in line with peers that have a median EBITDA margin of a low 40 percent. From my analysis, the key aspect that is weighing on the TIGO valuation is its leverage ratio, which is higher than peers' medians of 2.2x net-debt-to-EBIDA and 1.2x debt-to-equity ratio. TIGO's current net debt-to-equity ratio is 3.2x, and its debt-to-equity ratio is 2.15x. As TIGO deleverages, I expect multiples to go up.

{kind=link}

Risk

TIGO operates in places where FX risk is inherent, given the nature of developing/emerging markets. In addition, while TIGO is not directly affected by the conflict between Russia and Ukraine, it is still open to the effects of rising prices for energy and food. These big-picture economic factors could have an effect on the company's overall performance and financial health.

Conclusion

My buy rating on TIGO remains unchanged as the company exhibits strength in its fundamentals. Management's commitment to deleveraging the balance sheet is a significant catalyst that I believe will help close the valuation gap compared to industry peers. A key focus remains on the balance sheet, with management's guidance to achieve a net-debt-to-EBITDA ratio of 2.5x by 2026 and expectations of improved free cash flow generation in 2024. While TIGO's leverage ratio is currently higher than industry peers, I anticipate it will decrease over time, leading to higher valuation multiples.

For further details see:

Millicom International Cellular: Deleverage Is The Key Focus