TIGO - Millicom International Cellular Setting Up For A Great 2024

2024-01-19 14:57:13 ET

Summary

- The company has revised its 2022-2024 equity free cash flow guidance from $500 million to $600 million, indicating a positive outlook.

- Despite an expected dip in 2023 revenue and profit, the underlying business is improving, with cost restructuring efforts exceeding expectations and one-time items skewing profitability figures.

- Considering the current trends and updated free cash flow guidance, a DCF analysis yields a price target of $20.50, representing a 14% upside from current pricing.

I am following up on my previous thesis for Millicom International Cellular ( TIGO ) in light of a revision to guidance on equity-free-cash-flow. I previously rated Millicom a buy due to the following reasons:

- The business was pursuing growth opportunities on multiple fronts and it was starting to show in the results.

- Cost restructuring had the potential to reshape profitability if executed well.

- The market overreacted to Q1 results driving down the price and making valuation multiples extremely favorable.

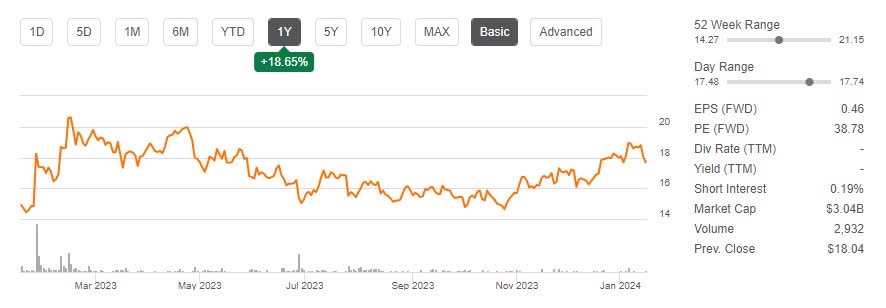

Since then, Millicom has risen 5.7%, beating the S&P 500 by 1.7 percentage points.

{kind=link}

Following 2022-2024 equity free cash flow guidance being revised from $500 million to $600 million, I reevaluated the business. I continue to maintain a buy rating with a DCF-generated price target of $20.5. The business continues to improve on multiple fronts and the cost restructuring is beating expectations. In addition, the significant improvement to free cash flow provides a wide margin of safety, and multiple valuation methods seem to agree on the potential upside.

Business Improvement On Multiple Fronts

At first glance it doesn't look like fiscal 2023 has been going well with revenue and profit expected to go backwards. However, there is a lot of good news buried in the results.

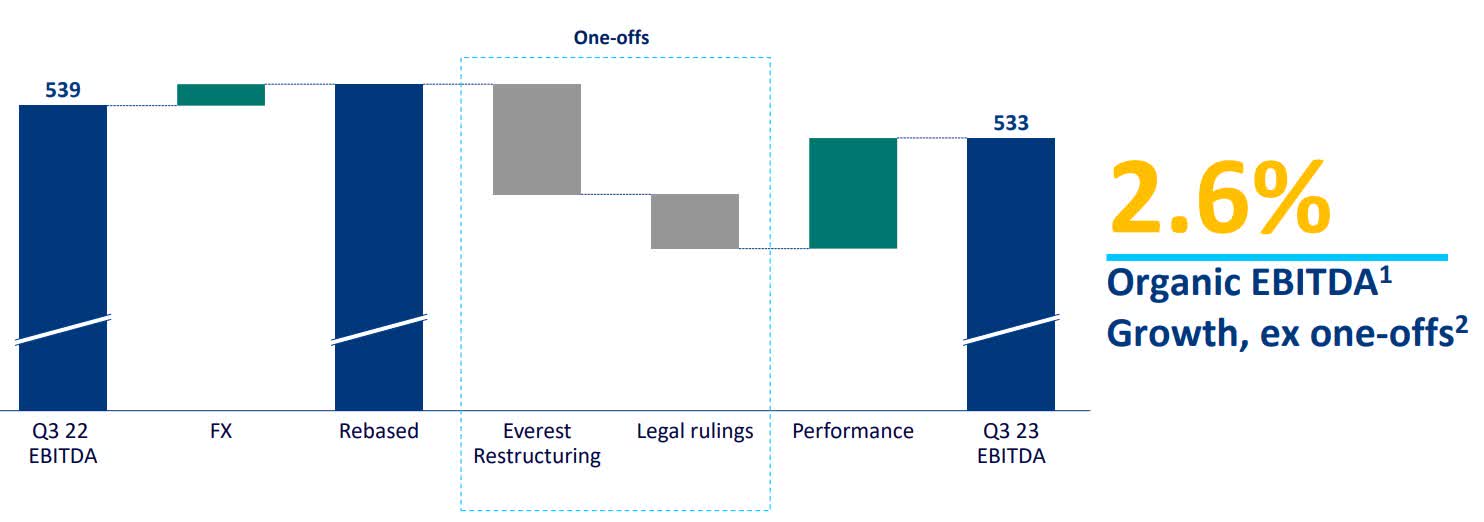

First, one-time items are having an outsized impact on 2023 profitability. Looking at Q3 2023 as an example, both revenue and EBITDA improved net of one-time items.

{kind=link}

Second, Millicom has executed on a turnaround for its largest country of operation, Colombia, representing 25% of the service revenue.

{kind=link}

A lot of time in the most recent earnings call was spent on Colombia. A couple of highlights:

- Funding has been secured to fully capitalize the Colombia business with a $75 million contribution from Millicom

- The JV with Telefonica was approved and will improve mobile access for 35 million will reducing operating expenses

- Capital intensity in Colombia will decrease due to the JV with Telefonica

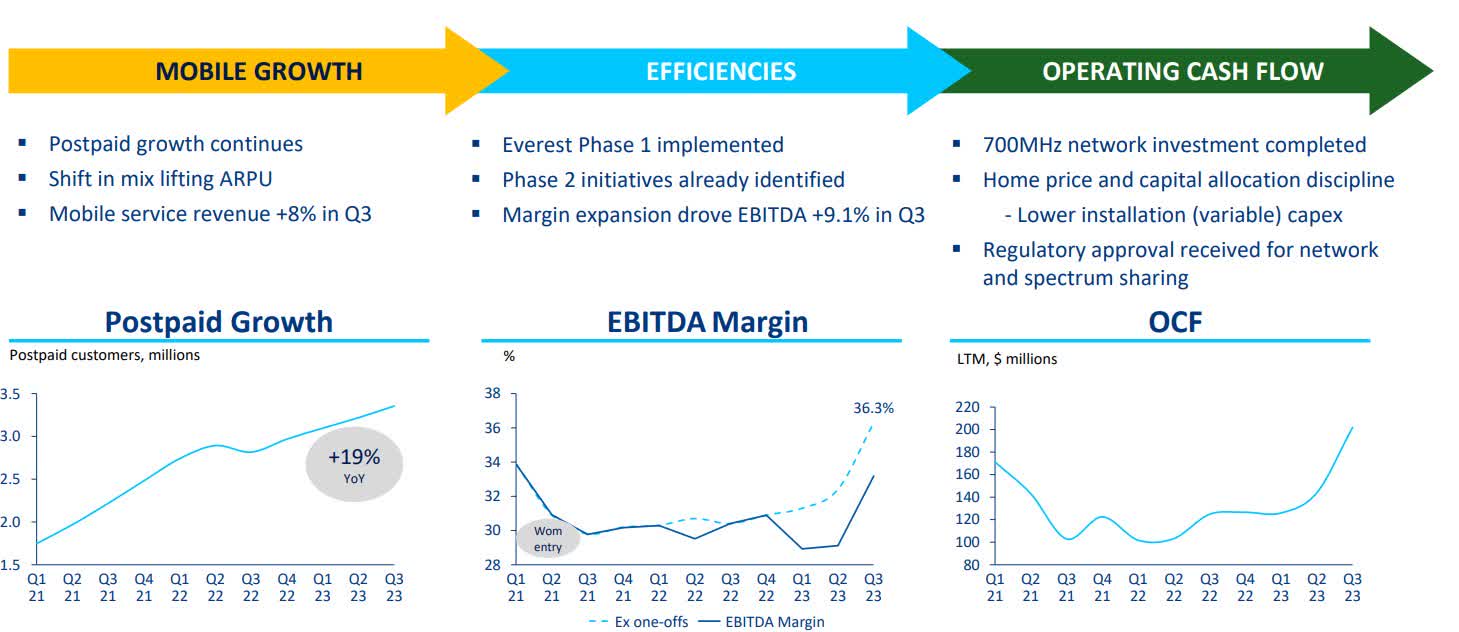

Third, and I think the biggest opportunity, is that Millicom started monetizing its tower infrastructure over the past few months through its subsidiary Lati. Lati has 9,000 towers in 7 countries with an average occupancy rate of 1.1x, well below the 2.1x average for Latam overall. This represents a significant opportunity for margin improvement and revenue growth.

Cost Restructuring Is Beating Expectations

As mentioned above, it's hard to see the benefit of cost restructuring due to high severance and restructuring costs. As discussed in the most recent earnings call, the one-time costs will continue into early 2024.

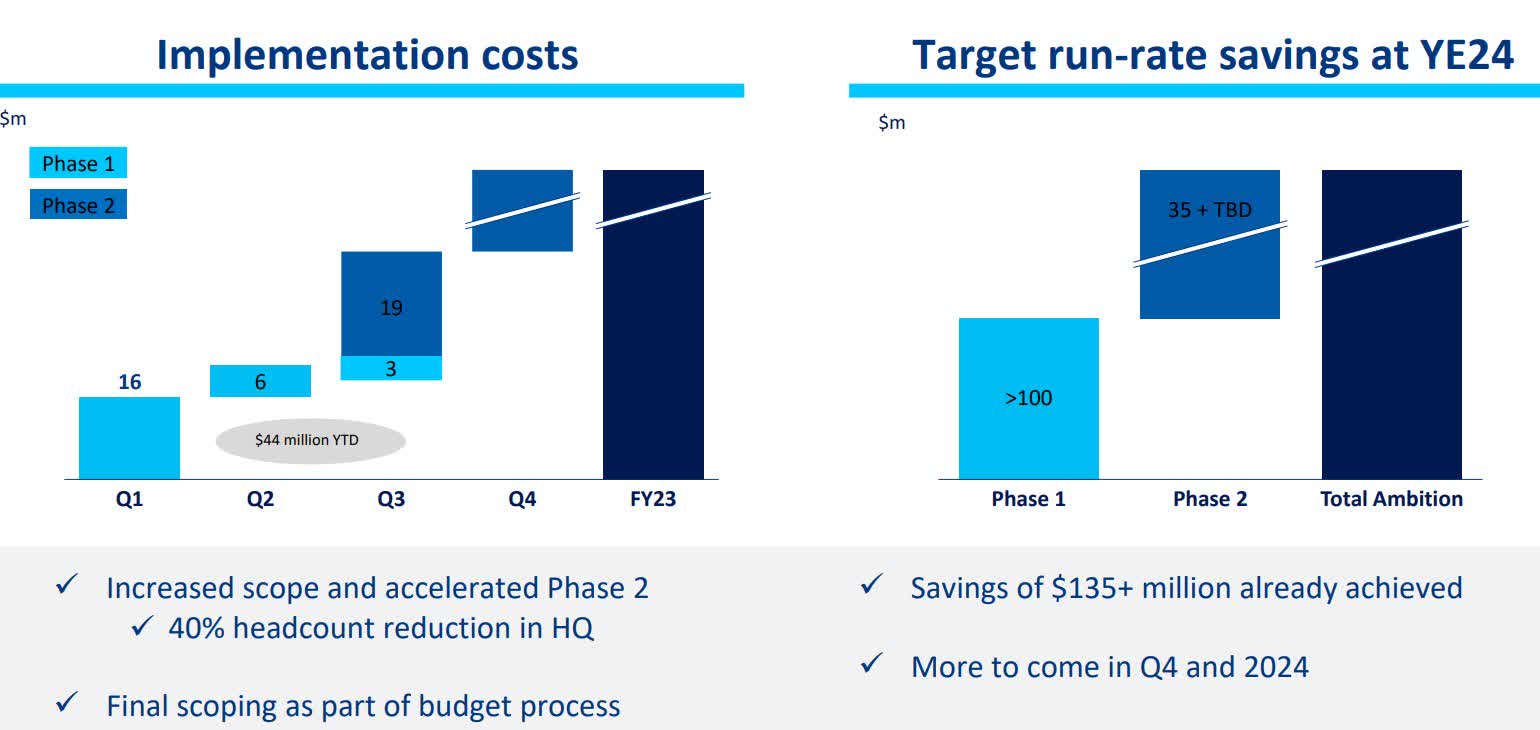

That said, Project Everest is beating expectations on every measure, being both ahead of schedule and ahead of savings target.

{kind=link}

While the project was already going well, new President and Chief Operating Officer Maxime Lombardi kicked it into overdrive. He immediately reduced Miami headcount by 40%, is reviewing every budget by line, and is going as far as personally approving every purchase order to get the point across.

The original savings target for Project Everest was $100 million, so being $35 million ahead with more to come is a great sign.

The efficiency improvement extends beyond operating expenses to capital. Cash capex is down 19.5% versus prior year , and it's expected to decrease further as the company continues its strategic review

Price Target Improves On Guidance Revision

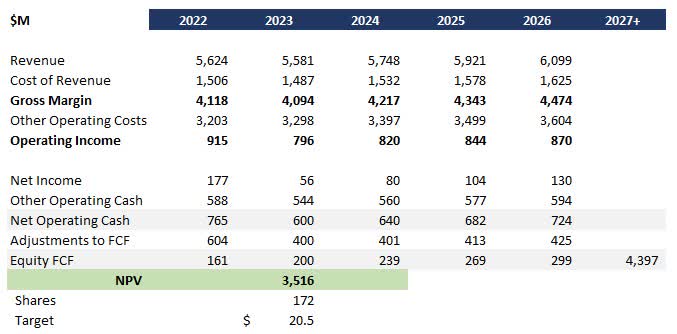

I ran a DCF using current trends and updating for the free cash flow guidance. I made the following assumptions:

- Near-term revenue growth of 3% based on current trends, management guidance, and industry long-term growth expectations

- Long-term growth of 3% based on industry CAGR forecast

- Discount rate of 10% based on the maturity of the telecom industry and cap size

Assuming $600 million of equity free cash flow from 2022-2024 and carrying trends forward, the DCF yields a price target of $20.50 or 14% upside from today's pricing.

{kind=link}

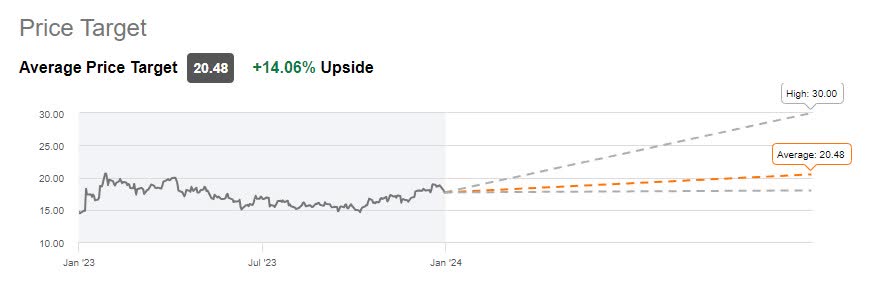

Wall Street analysts came to a similar consensus with a price target of $20.48 or 14% upside from today's pricing.

{kind=link}

The quant rating is more mixed at first glance with a hold rating.

TIGO Quant Rating (Seeking Alpha)

Digging in, I feel better about the rating. 3 of the 5 ratings are already at buy. The growth rating is being influenced by the one-time items we looked at above, which are largely related to restructuring. I believe that if the metrics were adjusted for one-time impacts, Growth and the overall Quant rating would move up to buy.

Downside Risk

Downside risks primarily come from execution as well as debt.

On the execution side, Millicom needs to maintain countries performing well while also executing its turnaround of the Guatemala business, which declined throughout 2023. They also need to maintain capital discipline to deliver the promised equity free cash flow growth as that underlies both my and Wall Street's price target.

On the debt side, Millicom is highly leveraged at 3.34x EBITDA to Net Debt. While maturity is low in 2023 and 2024, payments start to ramp up quickly in 2025 and 2026. If interest rates don't begin to moderate, this will be a drag on net income as loans come due. That said, leadership is focused on deleveraging to the mid 2s which may mitigate some of this risk.

Verdict

Millicom has revised its 2022-2024 equity free cash flow guidance from $500 million to $600 million, indicating a positive outlook. Despite an expected dip in 2023 revenue and profit, the underlying business is improving, with cost restructuring efforts exceeding expectations and one-time items skewing profitability figures.

Notably, Millicom has successfully turned around operations in Colombia, which accounts for 25% of its service revenue. The joint venture with Telefonica, approved recently, is set to enhance mobile access for 35 million people while reducing operating expenses. Also, Millicom's monetization of its tower infrastructure through subsidiary Lati presents a significant growth opportunity, given the potential for margin improvement and increased revenue.

The company's Project Everest, focused on cost savings, is ahead of schedule and exceeding targets, further boosted by new President and COO Maxime Lombardi's stringent budget reviews. Cash capex is down 19.5% compared to the previous year, and it's expected to decrease further as Lombardi continues his strategic review.

However, there are downside risks from execution and debt. Millicom needs to maintain performance in well-performing countries and turn around the declining Guatemala business. The high leverage of 3.34x EBITDA to Net Debt is also a concern, especially with payments ramping up in 2025 and 2026. However, the leadership's focus on deleveraging may mitigate some of this risk.

With a price target of $20.50, representing a 14% upside from current levels, I continue to rate Millicom a buy.

For further details see:

Millicom International Cellular Setting Up For A Great 2024