MDXG - MiMedx Stock: Strategic Realignment Can Unlock Value

2023-07-25 08:11:12 ET

Summary

- MiMedx has announced its intention to exit the knee osteoarthritis business to instead focus efforts on the high-growth Wound biologics market.

- The restructuring is expected to improve cash flow and profitability, supporting a positive long-term outlook.

- We like MDXG stock but expect shares to remain volatile following a spectacular rally in recent months.

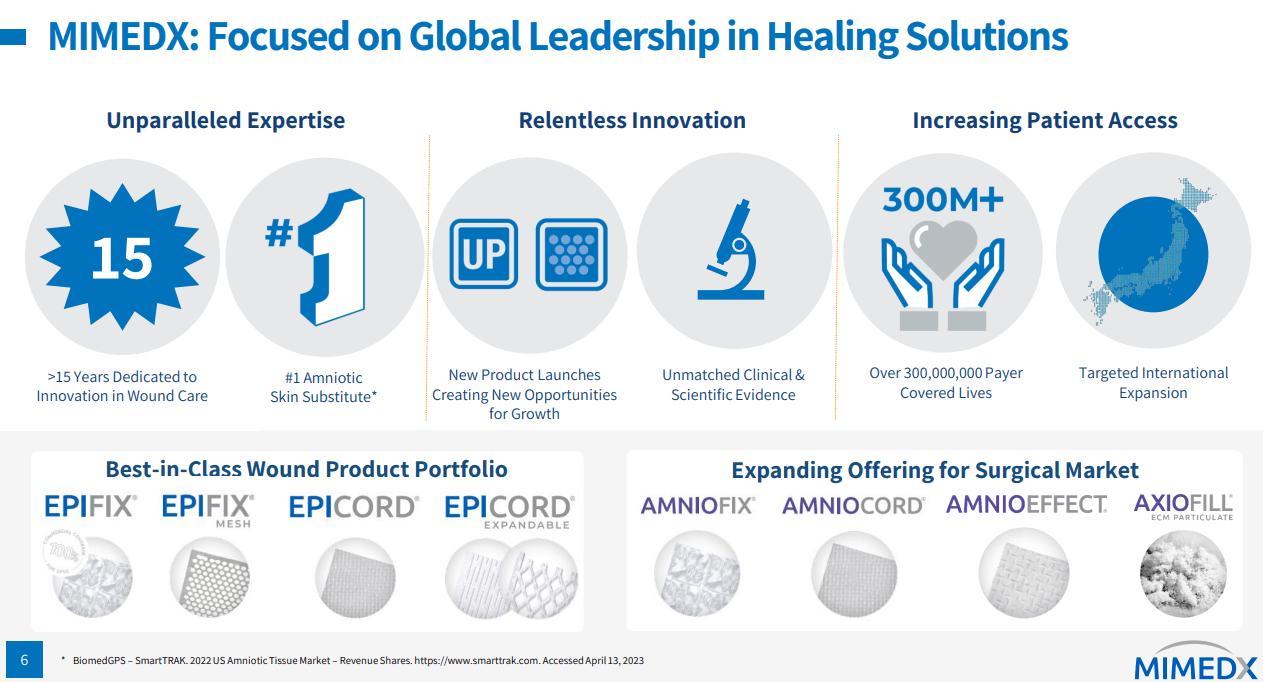

MiMedx Group, Inc. ( MDXG ) is a leader in placental biologics developing medical products that work as a skin substitute or "tissue allografts" to promote wound healing and reduce inflammation. This is a high-growth market with an expanding number of use cases from treating serious burn victims to accelerating regular surgical recoveries.

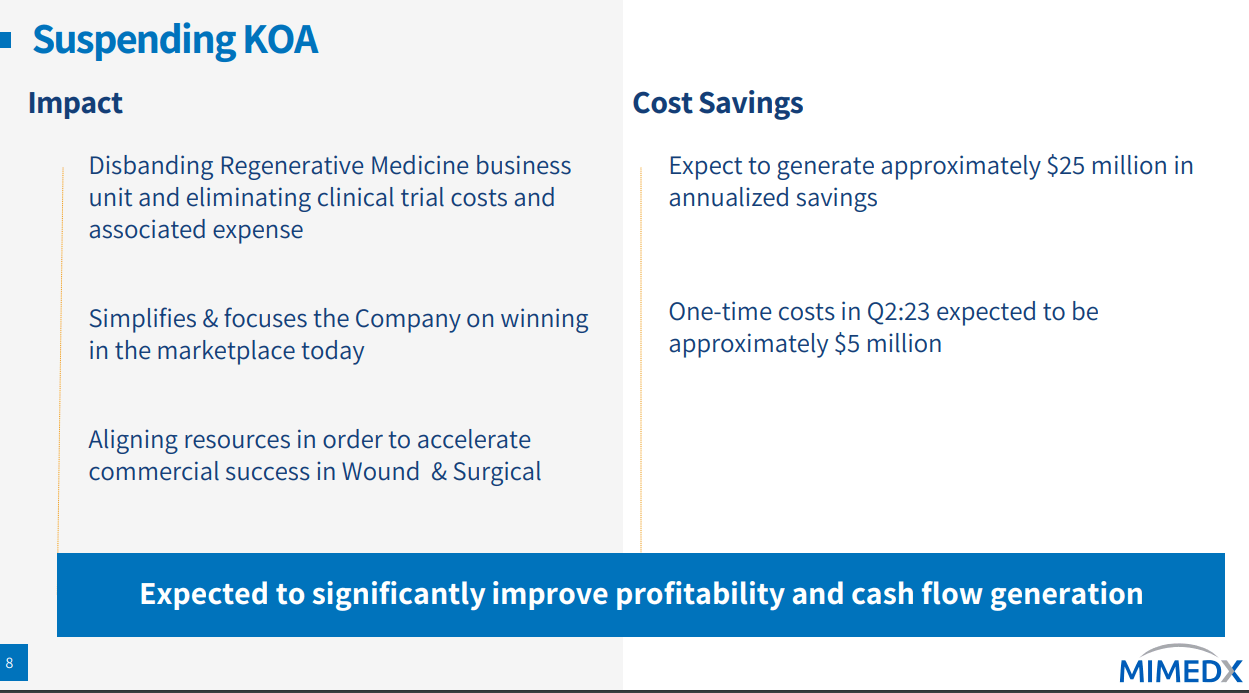

A key development this year is the recent announcement of a strategic realignment , with MiMedx exiting both its Knee Osteoarthritis and Regenerative Medicine programs to focus on the core Wound & Surgical business. The effort is expected to improve cash flows and drive profitability.

We like the stock and believe the restructuring will help to unlock value. While MDXG has already been a big winner this year, we see room for more upside but also urge some caution ahead of the upcoming Q2 earnings report.

MDXG Key Metrics

MiMedx last reported its Q1 earnings on May 2nd with revenue of $72 million, up 22% year-over-year, which beat the consensus estimate by $8 million.

The company is finding success with its "EPIFIX" and "EPICORD" wound care offerings, recognized as best-in-class amniotic skin substitute solutions. A theme this year has been a strong recovery in the surgical market with sales of products like "AMINIFIX" and "AMINICORD" rebounding compared to pandemic disruptions from 2021 and into the early part of 2022.

For reference, wound and surgical products are manufactured from human tissue, typically donated placentas from scheduled live birth C-sections or umbilical cords. These are sourced via a national network of hospitals that receive consent from expecting mothers.

Outside of intensive care settings, private practices including specialist offices for elective surgery types of applications have seen a strong uptake. Management explains that its targeted international expansion with initial sales of EPIFIX in Japan is also contributing to the momentum.

{kind=link}

While the company reported a Q1 EPS of -$0.06 , representing a net loss of -$5.0 million, the bigger story was that the trend improved from -$0.11 in the period last year. The adjusted EBITDA turned positive to reach $5.5 million compared to -$1.7 million in Q1 2022.

The company ended the quarter with $61 million in cash and equivalents against $48 million in long-term debt. During the earnings conference call , management reiterates a view that the company is well-capitalized and does not expect a need for external financing for the foreseeable future. We agree.

What's Next For MDXG?

We mentioned the plan to exit the Knee Osteoarthritis and Regenerative Medicine business. In Q1, this segment contributed to less than 10% of the top-line result but had a wider impact on pressuring income based on outsized expenses.

This was a clinical-trial stage program targeting drug candidates that would work by injecting placental biologics to help decrease pain and improve function in patients suffering from knee osteoarthritis.

The interpretation here is that the company is simply cutting its losses and choosing to not pursue further costly R&D on this side. In turn, the more streamlined corporate profile should benefit from efficiencies by diverting resources into its Wound & Surgical Business which is already on a path to underlying profitability.

In our view, this was a good move to consolidate the operation into the company's strong points. The guidance is that MiMedx expects to save approximately $25 million on an annualized basis following one-time separate costs of $5 million this Q2.

{kind=link}

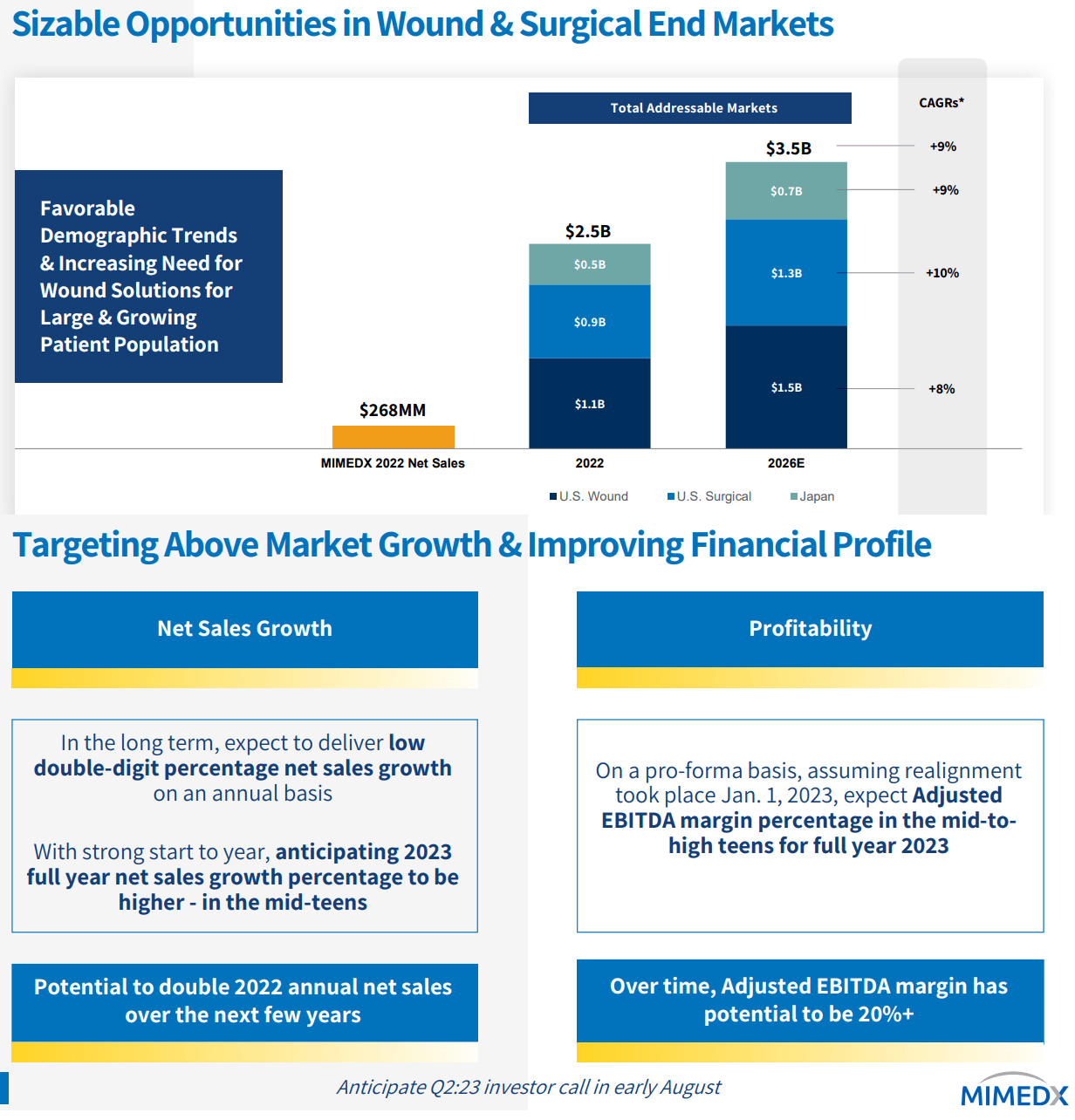

According to company estimates, the worldwide addressable Wound & Surgical end markets are expected to climb from $2.5 billion in 2022 to $3.5 billion by 2026, representing an annual growth rate of 9% over the period.

By this measure, MiMedx is expected to capture market share given its target of double-digit sales growth over the long run with a path to double 2022 results in the next few years. Management also expects to generate a positive adjusted EBITDA margin in the "mid-to-high teens" for the full year 2023 on a pro-forma basis.

{kind=link}

Is MDXG a Good Stock?

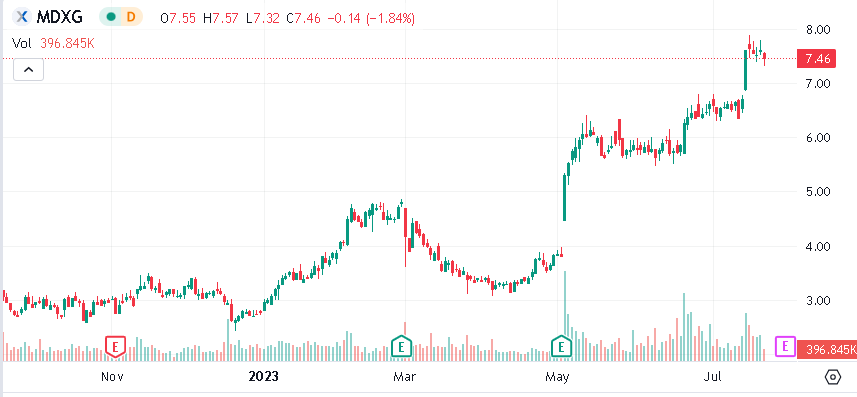

MiMedx presents an interesting setup with the company effectively refreshing its corporate focus supporting an improved long-term outlook. At the same time, the story here is hardly a secret as shares have rallied more than 100% in just the past three months.

In terms of valuation, MDXG is trading at a sales multiple of around 3x considering its current market cap of $900 million and $280 million in revenue over the trailing twelve months. This alone is a compelling metric for a "biotech" segment leader that is generated solid operating momentum with a solid net-cash balance sheet.

Based on management guidance for net sales growth this year in the "higher in the mid-teens" along with an adjusted EBITDA margin of around 15%, we can extrapolate those figures to suggest shares are trading at an EV to forward EBITDA multiple under 7x. Again, reasonable pricing for a company that appears to be moving in the right direction.

While MDXG has some key technological advantages and leadership positioning in certain segments, the broader market for wound care biologics is competitive.

The company's annual report cites names like Integra LifeSciences Holdings Corp. ( IART ), Organogenesis Holdings Inc. ( ORGO ), and Smith & Nephew plc ( SNN ) are all targeting similar opportunities with alternative technologies. The point here is to say that MiMedx is not the only game in town, and the long-term outlook faces uncertainty including on some regulatory frameworks that vary by region.

MDXG Stock Price Forecast

The question here is what will be the next upside catalyst? Our take is that with the stock already incorporating many of the positives, some other development presenting an accelerating growth opportunity will be necessary to drive a new wave of momentum.

Overall, we like the stock but rate shares as a hold meaning a neutral view on the direction over the near term. There's a lot to like about MiMedx, but our sense is that it's a bit too late to chase shares higher without more clarity on the financial positioning.

The bullish case for the stock is simply that results exceed expectations, opening a path for higher and more sustained long-term profitability sooner rather than later. On the other hand, the risk is that we get disappointment in terms of the sales momentum which could be indicative of a weaker demand or that the market is moving toward an alternative solution from a larger competitor.

Looking ahead to the upcoming Q2 earnings report set to be released on August 1st, the market will be looking for evidence the growth trends have built on the momentum from Q1 while the financial impact of the restructuring will also be a key monitoring point.

{kind=link}

For further details see:

MiMedx Stock: Strategic Realignment Can Unlock Value